The economy sailed smoothly in 2024. The first half of 2025 looks good, but the second is less certain. This year, the Federal Reserve aims for an inflation target of 2%. Keep your life jacket on and the seasickness pills handy. We may hit some choppy waters.

For the construction community, 2024 was, by and large, a good year. Several sectors exceeded performance projections, and stronger growth is expected in 2025.

2025: Trying to keep an even keel

ELECTRICAL CONTRACTOR’s economist Chris Kuehl, managing director of Armada Corporate Intelligence, Kansas City, Kan., said the economy is much stronger than many had expected as we head into 2025.

“Growth has been over 2% throughout 2024 (after Q1’s 1.6% pace),” he said. “Unemployment rates have remained at record lows (2.4% in November 2024), and consumers are still spending. If there is a concern regarding this growth, it is that most of this spending comes from the upper third of consumers (those making $100,000 or more). The lower third (making less than $50,000) has all but checked out of the system as they cope with inflation.

“There will be three developments to watch: Interest rate policy and how it connects to inflation; a possible shift in government priority with infrastructure projects; and an old problem—labor shortage.”

The Federal Reserve reduced interest rates three times in 2024, an unexpected half-point in September, and two quarter-point reductions in November and December, bringing rates down to about 4.4%. Two more cuts are anticipated this year.

“This is certainly lower than in recent years, but much higher than it had been for almost a decade,” Kuehl said. “What happens next depends on inflation. The major weapon the Fed has against inflation is higher rates.”

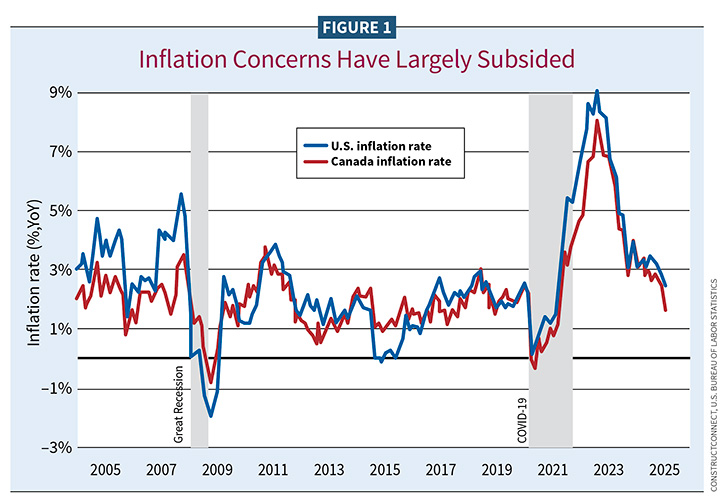

As of Dec. 11, 2024, the inflation rate stands at 2.7%, which is “close to the goal of 2.0% set by the Fed, but a rise from an earlier 2.3%.” See Figure 1.

“The Fed continues to worry about increased wage pressure and has now expressed concern over the impact of higher tariffs on imported goods. If these are all implemented, it would mean the average consumer would be paying $8,000 more for what they purchased last year,” he said.

Kuehl added that government priorities are likely to shift, such as infrastructure spending connected to alternative energy losing some importance and traditional projects expanding.

“There is a growing demand for electricity [supporting artificial intelligence alone will require 43 terawatts of additional power]. This has revitalized an expansion of nuclear power as well as interest in fossil fuels and alternatives,” he said.

Demographically, Kuehl continues to see the migration of people and businesses to locations where the cost of living and taxes are lower, which means expansion into the Southwest, Southeast and Midwest.

Labor shortages remain challenging.

“By the end of the decade, every boomer will have reached retirement age, and that is 76 million people,” Kuehl said. “There are not enough trained people to fill these vacated jobs. Changes in immigration policies will affect jobs as well. The burden of determining legal status will fall on business, and that can be an expensive process. Addressing labor training demands is a state and local issue, and there will be wide variations between states.”

A closer look

Cristian deRitis, deputy chief economist for Moody’s Analytics, New York, said the economy has achieved a soft landing. The Fed’s rate cutting last year was the tip-off.

“Overall, consumer balance sheets are still quite strong [middle- and upper-income],” he said. “Wealth is up about 50% from the start of the pandemic. House prices have risen; stock portfolios have gained in value. Consumers or households still have quite a bit of savings, so lots of liquid assets still power their spending. I don’t foresee a crash in either housing or the stock market, and, for that reason, I would expect that spending could continue for those groups. Employment is strong, too.”

Another plus is the U.S. debt-service ratio. This points to the sustainability of debt and how easy it is for people to make their monthly payments. According to deRitis, it is around 10%, considered quite low.

“Wage growth remains relatively robust, particularly for lower-wage jobs,” deRitis added. “That has helped offset some of the inflationary pressures. As these pressures reduce, wage growth may weaken but not collapse. That should provide some relief for those households to catch up on their debt and rebuild some savings.”

The strength of small businesses also indicated a strong economy. Applications to start businesses remain robust.

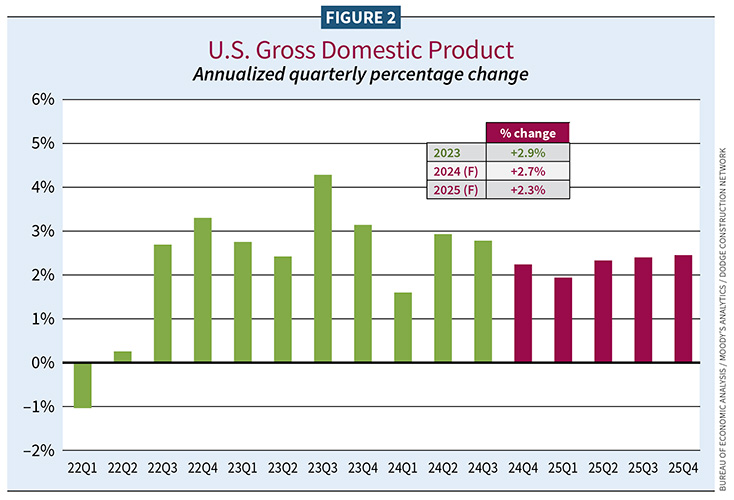

“I expect the GDP [gross domestic product] will be right under 3% or very close to it for 2024, very strong by historical standards. In 2025, I think 2.3%–2.5%, so some slowing in the economy, but still significant growth,” he said. Third quarter 2024 GDP stood at 3.1%. See Figure 2.

Speaking to “what ifs,” the new administration’s immigration plans could slow employment numbers. But that would be a cooling off from red-hot growth.

“At the very least, the threats of deportation are going to reduce some of the immigration into the country. From that standpoint, the economy slows to an equilibrium. My guess is job growth should slow to something closer to 80,000–100,000 per month,” deRitis said.

Other headwinds are coming this year, deRitis said, adding that not all Americans benefited equally in the recovery.

“The part of the household population we must worry about is at the lower end of the distribution,” he said. “With higher levels of inflation, it’s those consumers, those households who have had to turn to more credit to supplement their income. They have exhausted all their savings. That’s worrisome.”

If inflation were to creep up to a troubling degree, the Fed might freeze rates or even raise them again. That could hurt economic momentum. In October 2024, deRitis was confident the Fed would cut rates a quarter-point each fiscal quarter in 2025. In December, the Fed predicted only two cuts would come in 2025.

“If investors are expecting tariffs, deportations and lower taxes to be inflationary, that’s something that the Fed must consider or react to before that inflation takes on a life of itself. The higher interest rate environment that we just went through is still influencing business, including some small businesses,” deRitis added. “That’s clearly a risk that I see.”

Global events, particularly in the Middle East, also are a concern.

“If we think about oil prices as a potential threat to the U.S. economy, that certainly must be high on the list,” he said. “But I also believe that any oil price shock could be short-lived.

“Large deficits are also worrying. Global investors could sour on U.S. debt or become uncomfortable, demand a premium. Borrowing costs could rise and further contribute to the fiscal imbalance of the country,” he said.

He thinks that if tariff programs are more targeted, at China for example, they might not be nearly as damaging.

“We have higher tariffs on China already and the economy is performing quite well,” deRitis said.

President-elect Trump has also threatened higher tariffs on Mexico and Canada.

Three key policies

Three key policies coming up for renewal shouldn’t be ignored. One is the debt ceiling.

“The Treasury will adjust the books to buy some time, but at some point, probably by midyear, we will hit that ceiling once again without some type of adjustment,” deRitis said. “Secondly, we have the Tax Cuts and Jobs Act coming up for renewal in September, at the end of the fiscal year. If it expires, tax rates will rise. That could be a real shock to the system.”

Subsidies for Affordable Care Act premiums expire at the end of the fiscal year and will require attention. “Let’s address and move these obstacles out of the way and let the economy grow,” deRitis said.

The third policy to watch is The Conference Board’s Consumer Confidence Index. October’s readings showed people are not expressing confidence.

“I do draw a line back to prices. The inflation rate may be coming down, but the inflation level is still high. I think that certainly colors opinions. And yet, spending is still strong—a bit of a contradiction, it would seem,” he said.

In encouraging news, the index increased in November to 111.7 (1985=100), up 2.1 points from 109.6 in October.

Against all this uncertainty, deRitis remains “bullish” on construction.

“I think there’s still lots of demand. Lower interest rates should help to spur even more activity,” he said.

The year behind and the year ahead

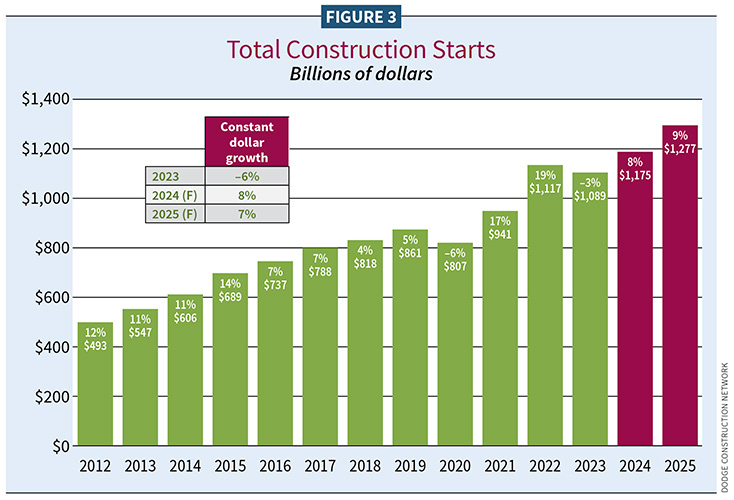

Dodge Construction Network, Bedford, Mass., put total starts (residential and nonresidential) growth at 8% ($1.175 trillion) in 2024. This year, it projects further growth at 9% ($1.277 trillion). See Figure 3.

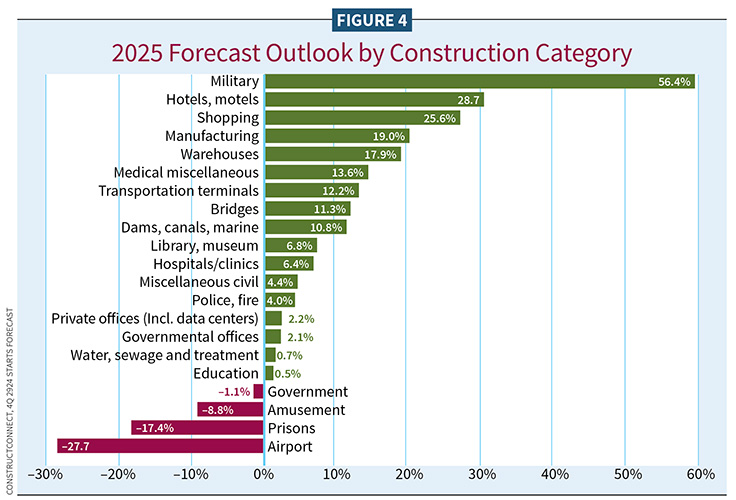

Cincinnati-based ConstructConnect and its partner Oxford Economics, New York, saw a retraction in 2024 of 2.4% ($939 billion). For 2025, they predict a healthy rebound at 8.5% ($1.018 trillion) and growth beyond. ConstructConnect also reports on nonresidential put-in-place spending, which in September 2024 year-over-year (y/y) gained 6.8% ($626.7 billion). See Figure 4 for specific sectors.

Put-in-place construction for all of 2024 is expected to total $2.15 trillion, an increase of 6.4% from 2023.

“We’ve been working under the stress of high interest rates combined with a stew of high material prices, labor issues, land costs and just the psychological—a beatdown of news cycles,” said Richard Branch, chief economist for Dodge Construction Network. “Will those things go away in 2025? Absolutely not. But I do think, as we look forward into the year, the outlook for construction is positive.”

Branch also pointed to the Fed rate cuts and further cuts in 2025 that will hopefully result in an “equilibrium” where interest rates are neither helping nor hurting the economy. Healthy employment, a relatively stable geopolitical situation and avoiding government shutdowns were other key assumptions in Dodge’s forecast.

“We need to process that there’s not going to be a massive uptick in construction or a massive uptick in economic activity just because the Fed cut rates so far up to 75 basis points [100 basis points as of Dec. 18, 2024],” Branch said. “Rates even now are still higher than they’ve been over the past couple of years. We think it’s going to take probably about 125 or even 150 basis points of cuts before we start seeing more consistent growth in the economy and more consistent growth in the construction market.”

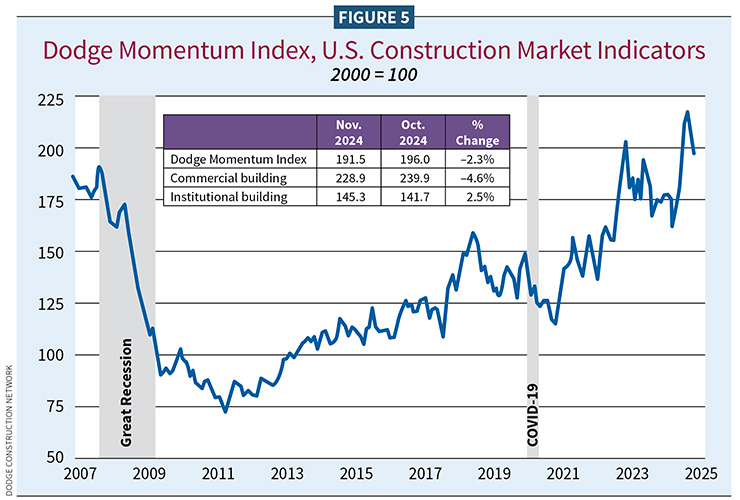

The Dodge Momentum Index (DMI) tracks nonresidential building projects under $500 billion in the earliest stages of planning, excluding manufacturing.

“What we’re really trying to track here is middle-class construction—schools, hospitals, retail, warehouses—the real bread and butter of the construction industry,” Branch said. “From late 2023 into 2024, the DMI was fairly stable. We had a slew of data center projects entering the pipeline. While the DMI has been lower over the last couple of months [of 2024], there’s still a lot of projects. Developers are essentially just slow-walking projects through the planning cycle, facing a mix of high rates, labor and land costs.”

The DMI decreased 5.3% in October to 197.2 (2000=100) from a revised September reading of 208.2. Nonetheless, it was 13% higher y/y. Commercial was up 18% y/y thanks to data centers, and institutional was up 3% y/y. See Figure 5.

November 2024’s DMI contracted 2.3% to 191.5 from the revised October reading of 196.0, but was 12% higher than year-ago levels. Over the month, commercial planning fell 4.6% while institutional planning improved 2.5%.

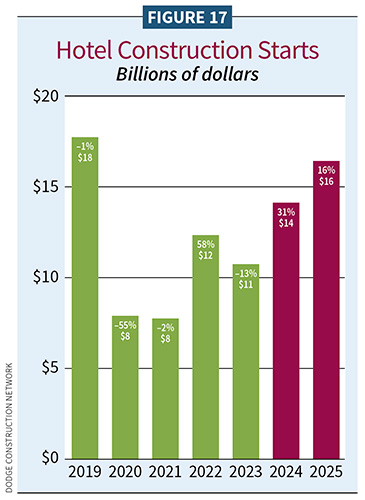

“Hotels have been probably the best news story in commercial, other than data centers,” Branch said.

He cited occupancy rates of 70% (close to prepandemic), healthy room rates and good shareholder reports for leisure and business travel. In 2024, square footage went up 5%, and the dollar value rose 31%. Alterations of existing properties comprised a significant portion of hotel construction activity. Some work represents a lower-tier brand redeveloped into an upper tier to accommodate new demands of leisure traveling after COVID. Some renovation work represents one chain taking over another.

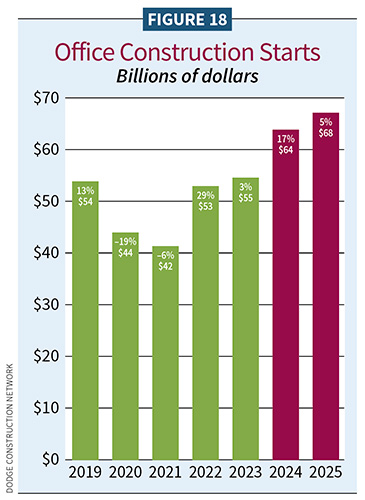

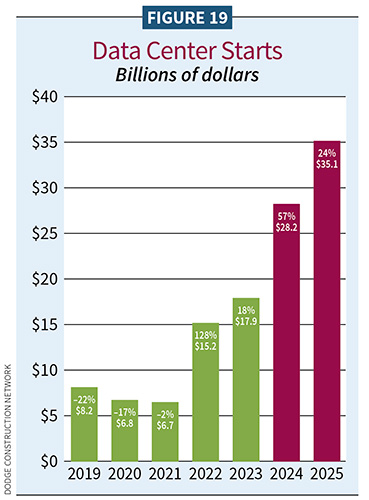

Data centers were the office sector’s main strength, which represented 30%–35% of office activity; this sector continues to grow.

“Whether they’re A.I.-related, cloud-security-related, back up national security, a lot of these data centers coming into planning are moving through quickly and breaking ground,” Branch said. “Our projected growth rates are probably a little conservative. I think the bigger question is what happens past 2025, perhaps more of a plateau in activity.”

Branch added that the traditional office space is also enjoying some healthy renovation activity. Close to 50%–55% of the market is renovation to accommodate a hybrid workforce, attract new employees and rethink office space with a smaller footprint.

“We’ve lost about 30% of the square footage of starts since 2019,” Branch said. “I do think we could see some new office buildout in 2026, enough for some small increases.”

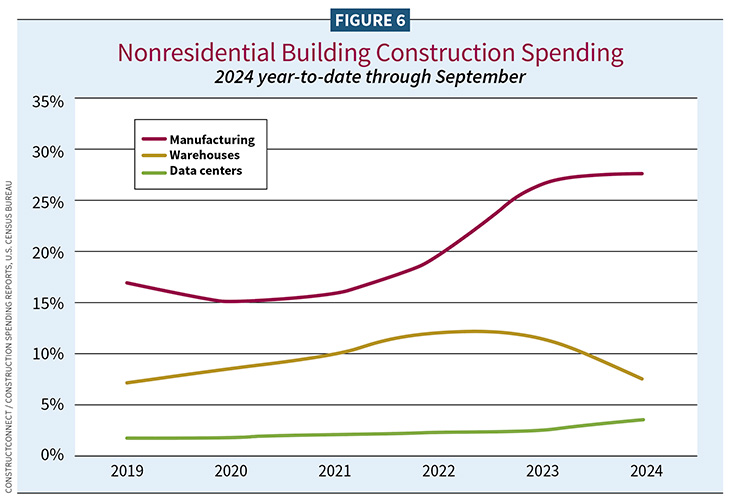

ConstructConnect economists found nonresidential showing some weakness in 2024. A warehouse sector contraction was expected for 2024. See Figure 6.

“Our starts grand totals are higher due to heavy engineering and civil construction. We expect nearly 18% growth for 2024. Numbers start to cool down in 2025 with 5%–6% growth, which is still excellent,” said Michael Guckes, chief economist for ConstructConnect. “Well over two-thirds or even three-quarters of sectors are expected to experience strong growth next year. We’re really excited about that. Some sectors, like military, are up 50+% [in 2025]. That is a turnaround from 2024.”

Guckes also cited the hotel/motel sector’s success and sees continued growth in 2025. Starts were down in 2024 in education and in some subcategories, such as parking lots. Manufacturing remained a strength.

“Manufacturing surged in our numbers,” Guckes said.

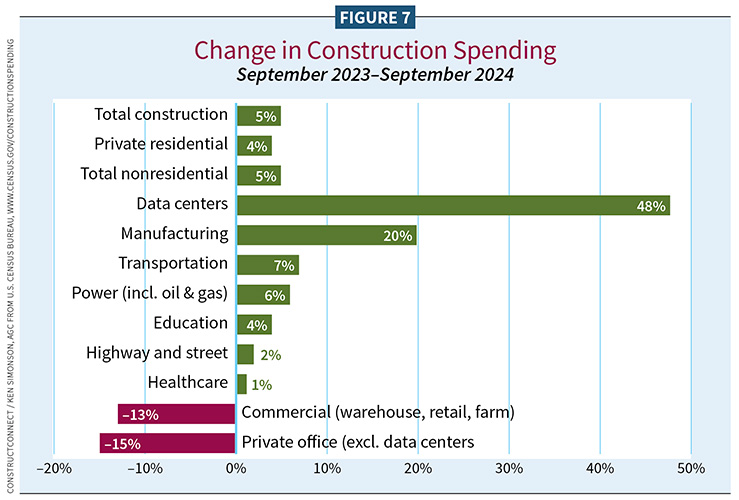

The American Institute of Architects (AIA), Washington, D.C., found manufacturing grew 23% y/y as of September 2024.

“It [manufacturing] accounts for over a quarter of all spending in the commercial, industrial and institutional sectors as of October 2024,” said Kermit Baker, AIA’s chief economist. See figures 6 and 7.

October 2024’s capacity utilization rate stood at 77.13 (percentage of resources used by corporations and factories to produce goods in manufacturing, mining and electric and gas utilities). It hovered in this range through much of 2024.

ConstructConnect found warehouse starts coming in second in 2024 (see Figure 6).

“This sector has peaked,” Guckes said. “It is still a large piece of the commercial market but returning to more traditional levels.”

Megaprojects ($1 billion or more starts) continue to show their strength, in Guckes’ view. “On average, we’re seeing about $10.2 billion of megaprojects per month,” he said. “Into 2025 and beyond, we have hundreds of billions of dollars’ worth of megaprojects that we continue to track. Not all those projects will break ground in 2025,” he said.

Guckes said that pipeline of existing megaprojects on the horizon is very encouraging, while Branch has some concerns.

In news from other sectors, Ken Simonson, chief economist for the Associated General Contractors of America (AGC), shared this information from the American Public Transportation Association: “There have been a total of 46 wins out of 53 measures for public transit in 2024, an 86.7% win rate [November 2024].”

In November, Education Week showed mixed results for school bond measures.

Guckes still sees challenges with banks financing commercial real estate.

“There’s about $400 billion worth of commercial real estate projects right now that are in this situation where owners are not making their monthly mortgage payments, but the bank says, ‘Look, we don’t want the property back. You keep the property and do the best you can, and we’ll talk later about how to make things right.’ It’s a headwind moving forward. Hopefully, we will see some regulation changes in 2025 and beyond,” he said.

After nearly two years of monthly decline, AIA’s Architecture Billings Index/Deltek (ABI) rose to 50.3 in October 2024, signaling that more architects had an increase in billings than a decrease.

Reflecting cautious optimism, Baker said, “Billings finally stabilized this month, and firms are feeling more optimistic about revenue projections for 2025. Overall, 41% of responding firm leaders expect to see net revenue growth from 2024 to 2025, with 32% projecting growth in the 5%–9% range.”

Averages regionally were South (52.1); West (47.6); Midwest (46.9); and Northeast (45.6). By sector, institutional (50.5); mixed practice (firms without half of their billings in any one other category) (48.0); commercial/industrial (47.0); and multifamily residential (45.6).

Within the ABI, the Project Inquiries Index was strong at 54.1, but its Design Contracts Index was 45.3.

Architecture firm billings remained flat in November with an ABI of 49.6.

The residential engine

Branch often uses a train analogy for the construction market: residential is the engine, and its health reflects the fitness of other (nonresidential) markets. Fortunately, this market is in recovery and making gains.

Danushka Nanayakkara serves as assistant vice president of forecasting and analysis for the National Association of Home Builders (NAHB), Washington, D.C. NAHB’s economic forecast is based on housing starts data from the U.S Census Bureau, Building Permits Survey and the Survey of Construction partially funded by the Department of Housing and Urban Development.

“In 2024, we are projected to hit a million units for single-family, which is good news. The forecast for 2025 is yet more growth getting us to 1.3 million units. We were expecting a decline for multifamily of 27% in 2024, only 340,00 units. It holds down our total residential number to –5.5% for 2024,” she said.

Nanayakkara called single-family gains “modest.”

“I think we ideally should be building around 1.1 single-family units to 1.2 single-family units yearly. Because of high mortgage interest rates, existing home sales have seen 14-year lows.

“Owners are holding on to their lower mortgage rates rather than selling. I think 2026 is the ‘magic year’ where single-family normalizes,” she said.

Though it may seem like the sky is falling on multifamily, looks can be deceiving. “Multifamily may be tamped down, but as market conditions improve, it will once again make gains,” Nanayakkara said. “There’s about 900,000 units under construction at this point. The higher interest rates for commercial lending remain expensive for builders, which has put a drag on this sector.”

NAHB reported that, in September 2024, seventeen states recorded growth in multifamily permits. Rhode Island (+135%) led the way, (while D.C.) had the biggest decline at –71%. In the top 10 metros by number of multifamily permits, permits jumped 51% for the New York-Newark-Jersey City area.

Mortgage rates were expected to move steadily down in 2024. They did for a short time but reversed and continued to rise.

“Due to the election, 10-year treasury rates increased, and the bond market reacted the other way, pushing the 30-year mortgage rate higher. I expect the mortgage rates to remain in the 6% range in 2024,” Nanayakkara said. NAHB is forecasting 6% by year’s end in 2025.

Residential continues to face stubborn headwinds, including not enough skilled labor, building material cost, tight lending and home shortages. Some of these expenses are especially acute for smaller builders (the majority of whom engage in home building).

“Regulation costs are about one-fourth of a home price at this point,” Nanayakkara added. “The right zoning allows us to be building for density. That’s the opportunity for multifamily, town homes for example. If lots are only zoned for single-family detached housing, that leaves out other housing answers to our housing shortage and housing affordability.”

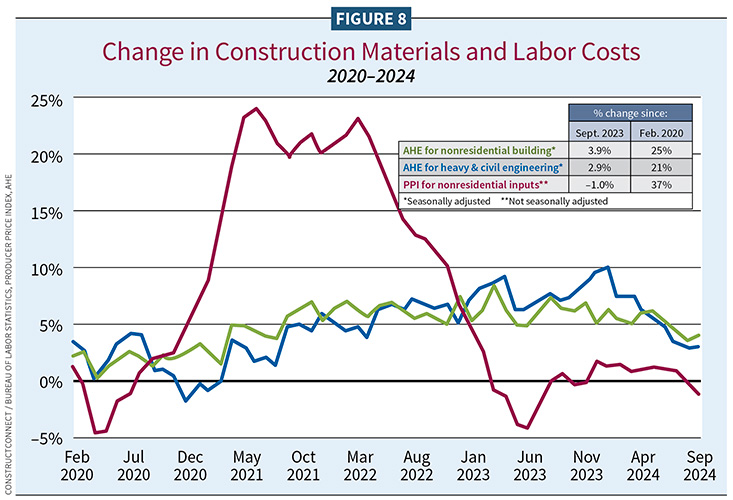

Selective material cost remains a problem, and some supply chain issues remain for housing construction. See Figure 8.

“Different building materials have become an issue,” Nanayakkara said. “Transformers are the biggest issue. In the last four years, transformer prices have skyrocketed 73%. Steel mill products are up over 50%, drywall products are up over 50% in the last four years. Ready-mix concrete is up over 30%. The good news is lumber prices have fallen compared to highs of 2021, but they are inching up. Right now [October 2024] lumber is hovering around $440 per thousand plank-feet. Pandemic averages ranged from 350 to 500. Tariffs increased between 8% and 14% from the Canadian lumber, and that accounts for about 30% of the lumber that we get to the into the U.S.”

Right now, Nanayakkara finds too many obstacles thrown at single-family.

“I think the reduction of the regulatory policies will help the housing market,” she said. “Increased tariffs, however, could be a problem. About 10% of overall residential construction materials are imported, so [there will be] possible inflationary impacts.”

She also noted that the uncertainty around immigration policy could affect the labor supply, primarily in the residential market. Immigrant workers represent about 25% of the labor force in construction.

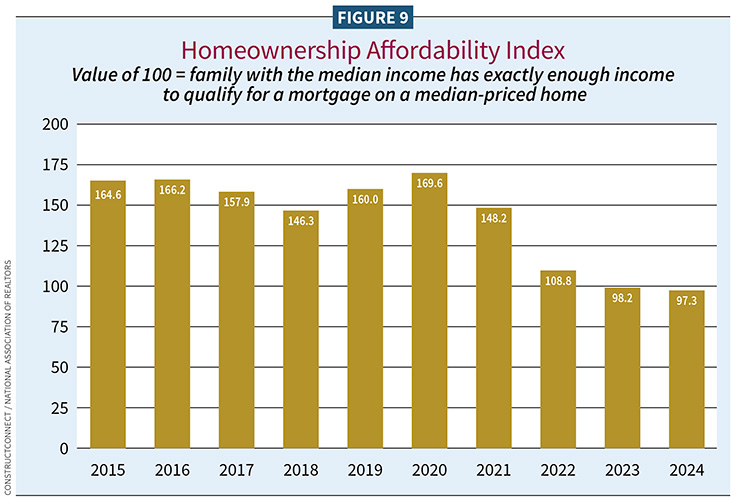

AIA’s Baker added, “House prices nationally have increased 76% since their high point heading into the Great Recession. They have increased over 50% from their prepandemic level, and they’ve increased even 5% since the beginning of 2024. We have relatively high mortgage rates, so coupled with rising insurance costs and other issues, this has exacerbated the housing affordability crisis for households looking to purchase a home and enter the market.” See Figure 9.

Along with NAHB, economists from Dodge and ConstructConnect agree that, with the right market conditions—including favorable mortgage rates, cash flow and home affordability—stronger single-family and improved multifamily markets will soon return.

The other storyline as it relates to residential construction is where it’s happening.

“The strongest residential growth is in those counties and ZIP codes that are further away from dense urban,” Branch said. “Home affordability is a key reason for people moving. Continued growth in hybrid work options is allowing people to move. This move away from dense urban cores is going to influence nonresidential, too.”

“I think there is cautious optimism among our members,” Nanayakkara said. “The simple fact is we need more housing.”

Navigating rough seas

“We know that construction activity, for the most part, has been moving sideways. What’s really going to get the gears turning is about 125 basis points of cuts, or maybe even 150, which puts us into Q1 or Q2 2025,” Branch said.

While possible negative impacts from the new administration have been discussed, deRitis offered this view: “I’m reluctant to take on the rhetoric from the campaign trail and declare, ‘We’re going to have a 20% tariff across the board, and it’s going to start on Jan. 20.’ I suspect it’s going to be much more nuanced. The timing is likely to be more phased in. That should give the construction industry some time to react. I don’t want them to overreact. I still see the general trend economically is the Fed moving toward that 2% inflation target.”

Simonson is also seeing some action to bolster an understaffed construction workforce.

“Companies are trying a lot of ways of recruiting more workers and upskilling the workers that they do have, partly through physical technology, partly through software. They are engaging much more with school districts, with local workforce agencies, and letting people know that construction has a ‘Help Wanted’ sign out. They are conveying a message that construction offers a great career ladder to start your own firm or rise to the top of a firm. You start with higher pay than other entry positions, which remain above other industry averages,” he said.

Branch added he thinks the Infrastructure Investment and Jobs Act (IIJA) will largely be left alone.

“I think there’s some concern about the tax credits for EVs and EV-related manufacturing. Time will tell. I also don’t think [President-elect Trump] touches the extension of the investment tax credit and production tax credit for utility-scale wind and solar. A lot of those projects are occurring in red states, which has been positive for those local economies. He says he wants an all-in energy policy,” he said.

All the economists interviewed in this forecast believe, at best, any immediate effects from the new administration’s possible policies won’t affect construction until the second half of the year.

Bidding

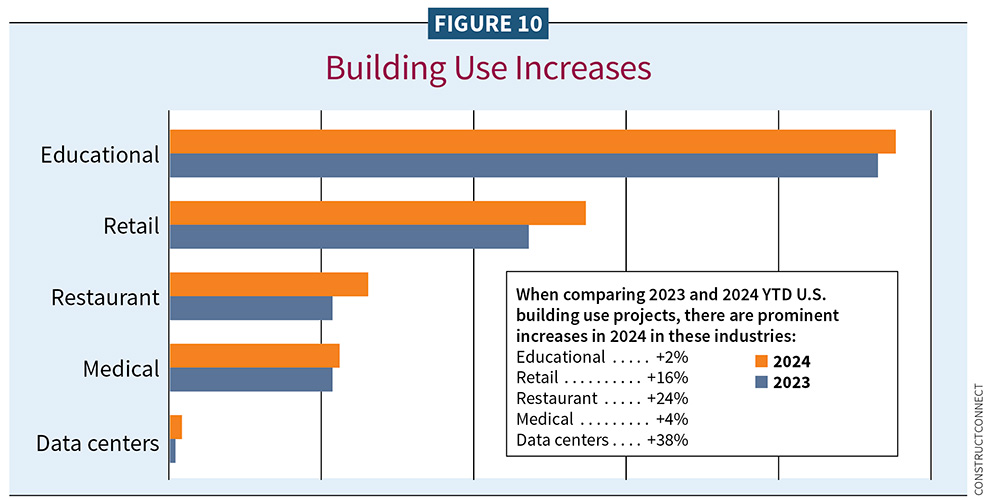

Kristy O’Brien, director of private content acquisition for ConstructConnect, reported on the stabilization of commercial bidding in 2023 continued into 2024: “We have observed a 7% increase [in 2024]. In the United States, we continue to witness growth in sectors like retail and restaurants. We have seen an upswing in new grocery store construction and companies repurposing existing locations from one brand to another.

“Former office spaces are being converted into commercial use. Additionally, there has been a rise in construction for educational and medical facilities. Several experts suggest that healthcare facilities could be a prime candidate for repurposed spaces, which may contribute to the observed increase in medical building uses,” she said. See Figure 10.

O’Brien also discussed sectors that saw a decline in bidding in 2024. She said municipal projects have slightly retracted, largely driven by the escalating cost of construction and the decline for large office spaces.

Bidding on warehouses, distribution centers and education projects declined in 2024, as well.

Employment and population movement

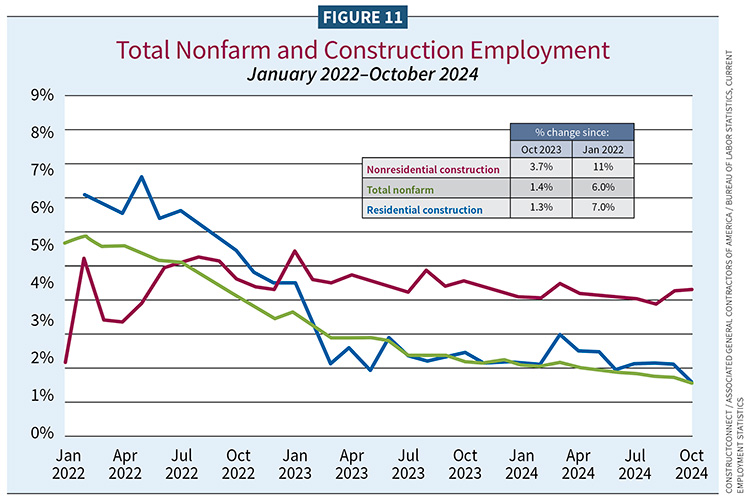

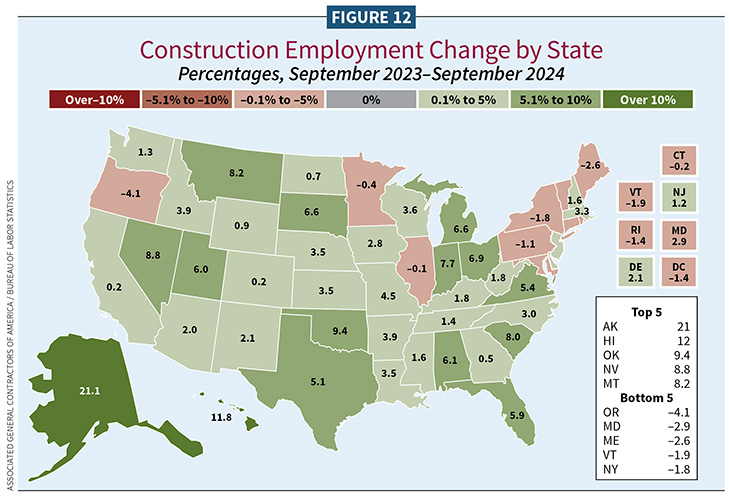

AGC reported in late November 2024 that construction employment increased in 41 states in October y/y. This represented the largest 12-month gain to date in 2024. See Figure 11. Texas added the most construction employees, followed by Florida, Michigan and Virginia. Employment losses y/y included New York, Oregon, Maryland, California and Minnesota. See Figure 12.

Construction employment in November 2024 grew another 10,000 workers.

“Year-over-year job growth has become more widespread in construction despite slowing down in other sectors,” Simonson said. “Still more states would have posted gains in construction employment if there were enough qualified workers available to hire. Contractors tell us that finding workers is still their No. 1 challenge. Our survey of almost 1,500 responses from every state showed that 94% of the firms who had an opening for craft workers say they were hard to fill, as did 92% of the firms with openings for salaried workers. Surveyors, estimating personnel, pipefitters and welders were occupations that became difficult to fill from a year earlier. Positions that don’t require prior training or industry experience have gotten easier. More people are showing up to apply for entry-level construction jobs than previously.”

Sector performance and forecast

Starts information is supplied by Dodge (cited first), followed by ConstructConnect, unless otherwise noted. Some predictions differ between the firms. Many are attributable to different vertical mixes and differences in date collection. We try to reconcile those differences or cite them when they occur. Dollars are not adjusted for inflation unless otherwise stated. ConstructConnect starts percentage differences for structures were often under 1%, and so are not listed.

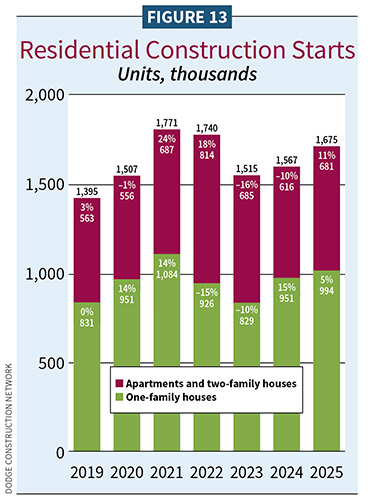

RESIDENTIAL

Itching to roar back

- 2024: 5%/1.567 billion units (Dodge Construction Network);–7.2%/$296.7 billion (ConstructConnect); 1.344 billion units (NAHB)

- 2025: 16%/1.675 billion units (Dodge); 12%/$332.5 billion (ConstructConnect); 1.337 billion units (NAHB)

*Dodge and NAHB did not provide dollar amounts.

**ConstructConnect did not provide units.

Higher mortgage rates, housing affordability and builder financing are getting in the way of a sector looking to run. Nonetheless, single-family and multifamily starts will continue to climb in 2025. See Figure 13. As market conditions ease, expect some notable momentum in single-family and multifamily in the coming years. According to Multi-Housing News, the top five emerging markets for multifamily in 2024 included Omaha, Neb.; Greenville, S.C.; the Southwest Florida Coast (Tampa to Fort Myers); Wilmington, N.C.; and Eugene, Ore. One of the bigger projects of 2024 was One Beverly Hills Residences in Beverly Hills, Calif. ($1.4 billion), being built around the historic Beverly Hilton Hotel. Rent has stabilized, too.

Single-family

- 2024: 15%/951,000 units (Dodge); $206.4 billion (ConstructConnect); 1 million units (NAHB)

- 2025: 5%/994,000 units (Dodge); $233.5 billion (ConstructConnect); 1.01 million units (NAHB)

Multifamily

- 2024: –10%/616,000 units (Dodge); $90.3 billion (ConstructConnect); 343,000 units (NAHB)

- 2025: 11%/681,000 units (Dodge); $98.9 billion (ConstructConnect); 323,000 units (NAHB)

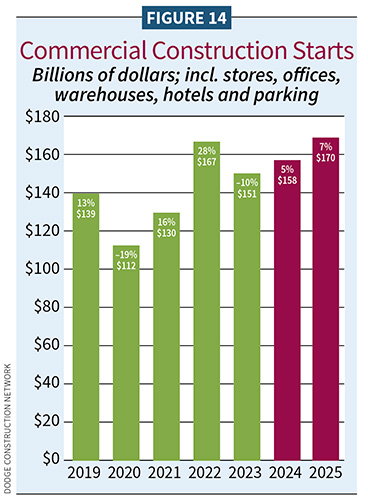

COMMERCIAL

Things are looking up with a big helping hand

- 2024: 5%/$158 billion (Dodge); 0.7%/$143 billion (ConstructConnect)

- 2025: 7% /$170 billion (Dodge); 7.0%/$153 billion (ConstructConnect)

Commercial starts in 2024 returned from 2023’s –10% contraction to a 5% gain, per Dodge. Another 7% is expected this year. See Figure 14. ConstructConnect numbers are on a similar trajectory: 0.7 in 2024 to a projected 7% growth this year. Warehouse softness remains, but the starts in planning are big ones, supporting a still-large market.

Other bright-spot sectors continue to be hotels, sports stadiums and convention centers, transportation terminals, retail, and a return to growth for parking lots in 2025. There may not be a run on newly constructed offices, but add in data centers and the sector grew a noticeable 17% last year (Dodge). Seventy percent of data center activity is centered in 10 states: Virginia, Texas, Arizona, Illinois, Georgia, Oregon, Iowa, Indiana, Wisconsin and Ohio. Dodge has broken out data centers: starts gained a whopping 57% ($28.2 billion) and are expected to grow another 24% ($35.1 billion) in 2025.

Plenty of existing office spaces are being renovated and are driving substantial work. An additional 8% growth in renovation is expected in 2025. One example is The Reckmeyer project ($38 million) in downtown Detroit. Three historic, contiguous buildings are being renovated as mixed commercial and multifamily, with an additional residential complex set behind.

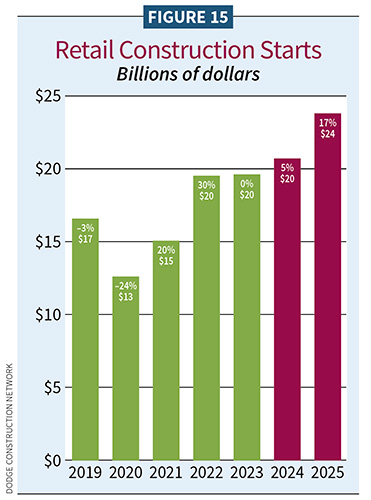

Retail

- 2024: 5%/$20 billion (Dodge); $13 billion (ConstructConnect)

- 2025: 17%/$24 billion (Dodge); $16.4 billion (ConstructConnect)

See Figure 15.

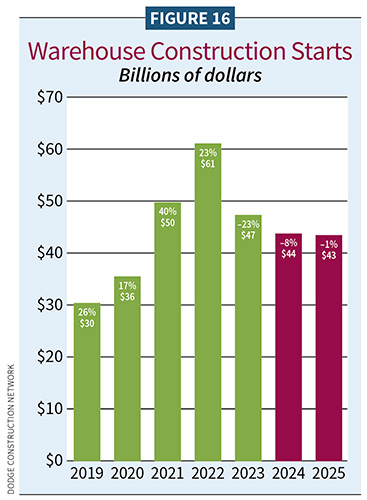

Warehouses

- 2024: –8%/$44 billion (Dodge); $20.5 billion (ConstructConnect)

- 2025: –1%/$43 billion(Dodge); $24.2 billion (ConstructConnect)

See Figure 16.

Hotels

- 2024: 31%/$14 billion (Dodge); $11.9 billion (ConstructConnect/with motels)

- 2025: 16%/$16 billion (Dodge); $15.4 billion (ConstructConnect/with motels)

See Figure 17.

Office buildings

- 2024: 17%/$64 billion (Dodge); $34.9 billion (ConstructConnect/private offices only)

- 2025: 5%/$68 billion (Dodge); $35.6 billion (ConstructConnect/private offices only)

See figures 18 and 19.

|  |

The top three commercial projects in 2024 (as of September 2024) were the AWS Amazon Data Center Megasite/Phase 1, Canton, Miss. ($1.6 billion/1.1 million square feet); QTS New Albany 1 and New Albany 2, New Albany, Ohio ($1.5 billion/1.4 million sf); and Meta Data Center, Montgomery, Ala. ($800 million/715,000 sf).

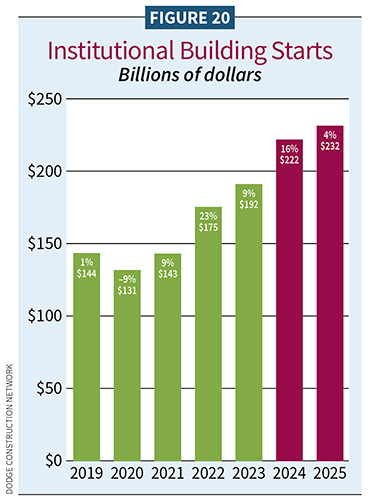

INSTITUTIONAL

Strong growth will slow

- 2024:16%/$222 billion (Dodge); 3.5%/$169 billion (ConstructConnect)

- 2025:4%/$232 billion (Dodge); 5.3%/$178.8 billion (ConstructConnect)

*ConstructConnect projections for this sector are harder to neatly quantify alongside Dodge. The estimates addressed below are largely within related Dodge subsectors.

Institutional starts have been climbing since 2021. The early forecast 7% gain for 2024 ended up a 16% advance (Dodge). Growth will settle down to 4% ($232 billion) this year. See Figure 20.

ConstructConnect starts indicate $169 billion last year rising to $178 billion this year. Education K-12 was boosted by state and local funding. Both sources had healthy budgets. In the education sector overall, Branch described state and local funding as mixed in 2024. He expects state spending will fall in 2025 but sees that as a return to normal after a boost in spending levels thanks to pandemic-related cash.

“I think some of that will be made up by increases in local funding,” he said. “Higher property values are helping some local budgets. Really strong employment, too.”

Branch said that demographic growth is reasonably positive for education, most notably in the Sunbelt—particularly Texas, Nevada, Arizona and New Mexico—and the West in general, except California. K-12 and colleges/universities are trending up, per Dodge. Lab projects, which showed several years of growth, are slipping. State and local budgets also continued to support healthy starts of religious buildings, courthouses, police and fire buildings, detention, and others. This year will show continued growth in these sector categories.

Branch also noted that starts for healthcare clinics continued their growth, extending into 2025. Hospital starts activity is starting to increase, too. Nursing homes and assisted living construction retreated in 2024 but comes back this year.

Education

- 2024: 5%/$89 billion (Dodge); $101 billion (ConstructConnect)

- 2025: 8%/$96 billion (Dodge); $102 billion (ConstructConnect)

College and universities

- 2024: $28.7 billion (ConstructConnect)

- 2025: $29.2 billion (ConstructConnect)

*Dodge did not provide a segment-specific forecast.

K-12

- 2024: $70 billion (ConstructConnect)

- 2025: $70.6 billion (ConstructConnect)

*Dodge did not provide a segment-specific forecast

Healthcare

- 2024: 19%/$46 billion (Dodge); $36.4 billion (ConstructConnect)

- 2025: 11%/$51 billion (Dodge); $40.2 billion (ConstructConnect)

Transportation

- 2024: $7.4 billion (ConstructConnect)

- 2025: $8.3 billion (ConstructConnect)

Recreation

- 2024: $11.8 billion (ConstructConnect)

- 2025: $10.1 billion (ConstructConnect)

“Recreation” refers to sports arenas and convention centers.

Miscellaneous institutional

- 2024: $33.2 billion (ConstructConnect)

- 2025: $32.6 billion (ConstructConnect)

“Miscellaneous” encompasses religious buildings and public buildings, including capitols, courthouses, police and fire buildings, detention and other government buildings.

The top three institutional projects (as of September 2024) were the University of California Davis Medical Center, California Hospital Tower, Sacramento, Calif. ($3.7 billion/909,000 sf); Terminal 3 West Modernization/Expansion, San Francisco ($2.6 billion/200,000 sf); and UCSF Helen Diller Medical Center, San Francisco ($2.3 billion/875,000 sf).

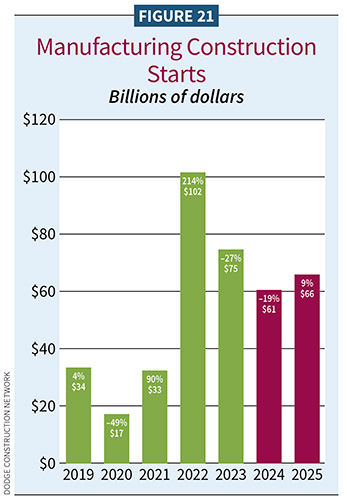

MANUFACTURING

- 2024: –19%/$61 billion (Dodge); –47.8%/$54.8 billion (ConstructConnect)

- 2025: 9%/$66 billion (Dodge); 19%/$65.2 billion (ConstructConnect)

Manufacturing is an instance of a sector underperforming from earlier 2024 projections. See Figure 21.

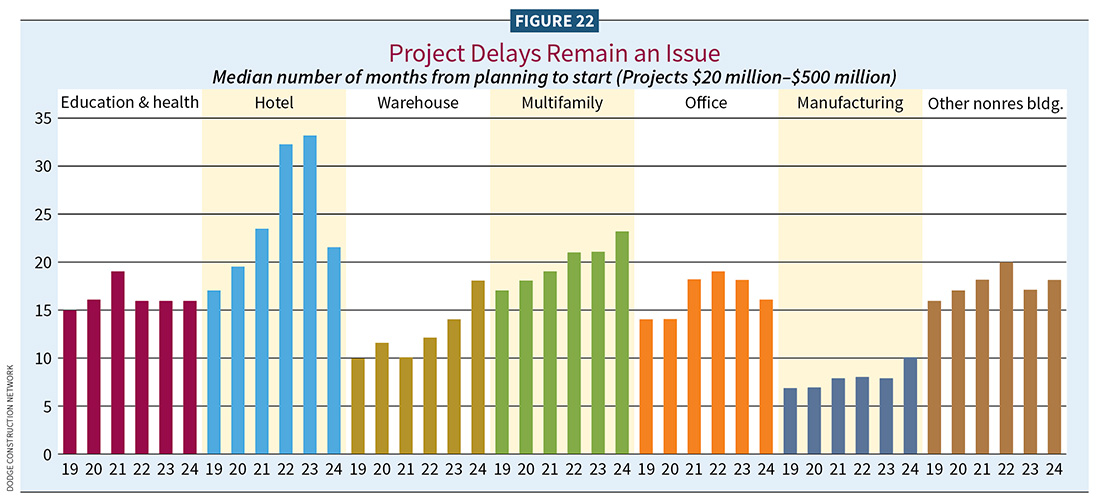

Though ConstructConnect 2024 starts clawed from –31% in 2023 to –19% in 2024, Dodge’s Branch shared, “What really changed our manufacturing outlook over the last year has been the growing number of projects that have been delayed or canceled. In our October 2023 forecast, we included $25 billion worth of projects in our forecast. The vast majority started on time or just a little bit late. Very few were delayed or canceled.” See Figure 22.

“In 2024, we saw fewer megaprojects and a growing share of them are either being delayed because they are still in planning or canceled outright. From our perspective, maybe lesser starts are an over-recalibration around potentially slower activity for EV batteries. There are still a lot of chip plants that we expect will break ground this year. We have several petrochemical plants built into the forecast and manufacturing projects that are a function of reshoring or onshore,” he said.

Projects that have been delayed from the original target start include the Rivian Electric Vehicle Plant ($5 billion), LG Energy Battery Plant/Pouch-Type Batteries Building ($1.2 billion), and the Integra Technologies Semiconductor Manufacturing Plant ($900 million).

Dodge and ConstructConnect expect to see growth in manufacturing in 2025.

Noted manufacturing starts in 2024 are continued development of the Texas Instruments Fabrication Plant (Project Bruno), Lehi City, Utah ($5.5 billion); Hyundai/SK EV battery plant, Cartersville, Ga. ($2.5 billion); and LG Electric Battery plant expansion (phase 3) for Toyota vehicles, Holland, Mich. ($1.4 billion).

NONBUILDING

Massive dollars, maintained growth

- 2024: 6%/$441 billion (Dodge); 18.3%/$273.6 billion (ConstructConnect)

- 2025: 6%/$467 billion (Dodge); 5.3%/$288 billion (ConstructConnect)

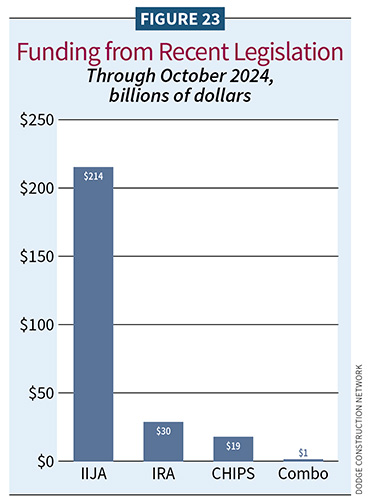

Infrastructure sails along. According to Dodge, project work since 2022 has reached well over $400 billion, with support from the IIJA and Inflation Reduction Act and, of course, federal appropriations. Many starts were renewable energy projects. See Figure 23. The American Clean Power Association predicted a record-breaking year for the U.S. solar industry, with more than 32 gigawatts of installations in 2024. ConstructConnect’s starts figures are smaller but still show the effect and growth of stimulus dollars.

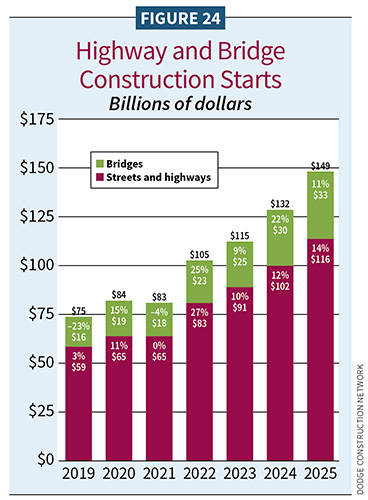

Roads and bridges have received the lion’s share of IIJA dollars, but continued growth also is assured in dams, water supply and sewer/waste disposal systems. Energy-related starts remained very strong in 2024, softening just a bit. Expect a small gain adding to healthy dollars in 2025.

Under the IIJA, the Biden administration provided more than $600 million to bolster grid resilience and reliability in the face of extreme weather and increased electricity demand across the states affected by hurricanes Helene and Milton. Helping to harden the electric grid across the Southeast, project work in 2025 includes the installation of advanced conductors and controls, devices for more efficient and precise dispatching of field teams during outages, and upgraded lines to meet projected load growth and renewable integration. The law also provides additional funding for ports and waterways, airports, rail and clean transportation.

Bridges and streets/highways

- 2024: Bridges: 22%/$30 billion (Dodge); $29 billion (ConstructConnect)

- 2025: Bridges: 11%/$33 billion (Dodge); $33 billion (ConstructConnect)

- 2024: Street and highways: 12%/$102 billion (Dodge); $99 billion (ConstructConnect)

- 2025: Street and highways: 14%/$116 billion (Dodge); $110.6 billion (ConstructConnect)

See Figure 24.

Environmental public works

- 2024: Dams and reservoirs: 1%/$26 billion (Dodge); $11.9 billion (ConstructConnect)

- 2025: Dams and reservoirs: 13%/$30 billion (Dodge); $13.2 billion (Construct Connect)

- 2024: Water supply systems: 30%/$29 billion (Dodge)

- 2025: Water supply systems: 6%/$31 billion (Dodge)

- 2024: Sewage and waste: 18%/$28 billion (Dodge)

- 2025: Sewage and waste: 14%/$31 billion (Dodge)

*ConstructConnect combines water and sewage treatment: $57.8 billion (2024); $58.2 billion (2025).

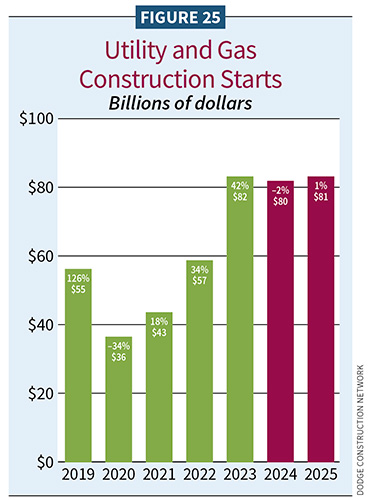

Power and utilities

- 2024: –2%/$80 billion (Dodge); $59.6 billion (ConstructConnect)

- 2025: 1%/$81 billion (Dodge); $62.3 billion (ConstructConnect)

See Figure 25.

Notable nonbuilding projects for 2024 are Dominion Energy Offshore Wind project off the Virginia coast ($9.8 Billion), the Sun Zia transmission line across Arizona and New Mexico ($4.5 billion), and the TransWest Transmission Project spanning Wyoming, Colorado, Utah and Nevada ($3.5 billion).

Conclusion

Uncertainty is the challenge of 2025 set against a strong economy. A party trifecta in Washington takes on governance and campaign promises. World events remain uncomfortably unsettled. Inflation is controlled, for now. The United States continues to lead the world in economic performance coming out of the pandemic. If construction planning grows more confident, it will add ballast to a year that looks very strong. The tide of residential is waiting its turn to roar back. It certainly is a winner in construction employment. Be a shrewd sailor in 2025. Calm seas may make way for big waves.

Bonotom Studio, Inc. / Stock.Adobe.com / WILASINEE

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].