If the electrical construction market was presented like the local news, the weatherman might say, “Looking at the 2024 construction weather map, we see sunny skies sweeping across Texas, with sustained headwinds hitting California. High pressure builds ahead of a coming storm of government funds pouring into the construction infrastructure market ... .“ But there’s no need to fret about the mixed predictions. After all, there’s no such thing as bad weather, only bad clothing. Chris Kuehl, who adds his expertise to the Construction Outlook this year, said economists “are eternally grateful for meteorologists because they [have] made us look good over the last few months.”

So, what can we do to navigate an economy that is both strong and challenging? In 2023, rather than fitting into familiar economic cycles, periods of strength churned together with weaker moments. The partly sunny forecast will probably continue. Though economists expect a softening in the first half of 2024, projections for the second half of the year indicate a return to stronger growth, more normalcy and momentum building into 2025. Meanwhile, the fog of inflation should continue to lift.

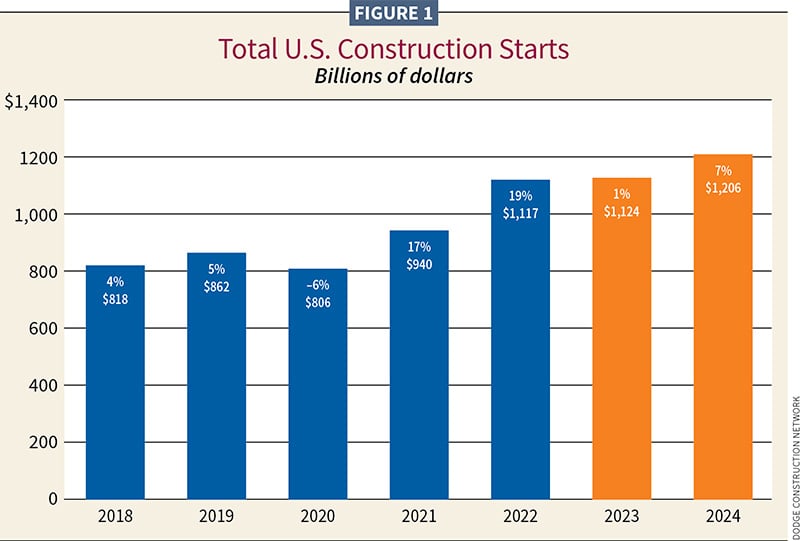

Construction helps tell the tale of the current economy. In 2023, Dodge Construction Network forecast a 1% gain ($1.124 trillion) for total construction starts, building off a 19% advance in 2022. This year (2024), Dodge sees a further gain of 7% ($1.206 trillion). (See Figure 1.)

ConstructConnect, in collaboration with Oxford Economics, estimated an 8.1% contraction of total construction starts for 2023 ($884.1 billion) and gains of 2.8% ($909 billion) in 2024. The firm’s put-in-place (PIP) construction spending for 2023 represented a gain of 4% ($1.922 trillion) and a 2024 projected gain of 3.4% ($1.988 trillion).

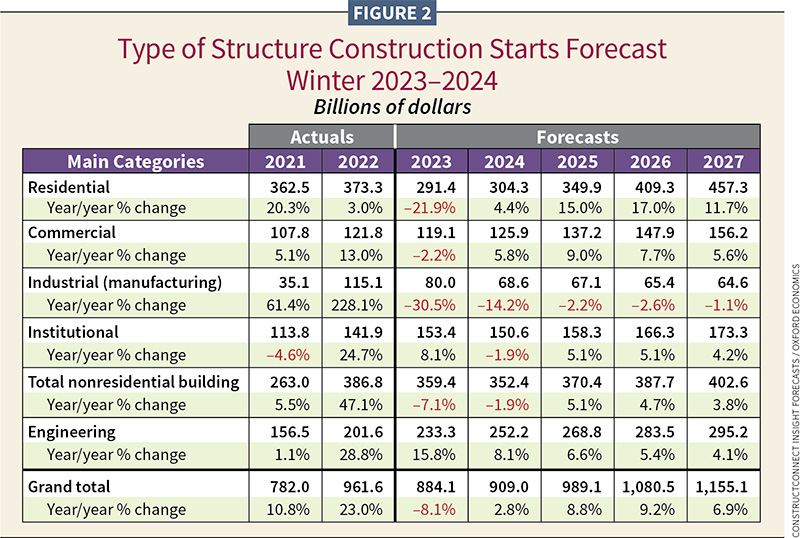

Repeatedly, 2023 construction performance bested earlier projections. Hot segments such as warehousing and utilities cooled a bit, but overall, there were good things to cheer, including in manufacturing, lodging, retail, healthcare and education. Infrastructure stayed strong and is poised to roar ahead as federal stimulus and appropriations dollars are applied. (See Figure 2.)

Chris Kuehl is chief economist at Armada Corporate Intelligence in Lawrence, Kan. He provides forecasts and strategic guidance and is the economic analyst for several state accounting societies. Here, he specifically focuses on the electrical industry.

Strong but challenged

Kuehl and other economists will tell you that the long arm of pandemic recovery upset economic forecasting. Inflation, stockpiling, consumer behavior and world events influenced the early part of 2023. However, the second half was unexpectedly stronger.

With 2024 predictions showing slower growth, no one will complain if performance exceeds expectations. Kuehl expects 2024 will continue to offer uneven results for electrical contractors and the construction industry depending on sectors served and service territory.

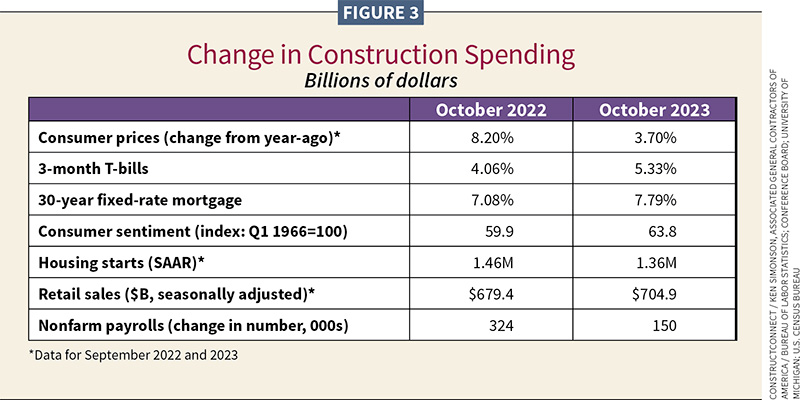

Historically speaking, normal economic cycles would have put us in a recession by now, except COVID-19 served as the disruptor. Even the data that economic prognosticators have typically relied on to project economic performance has been a bit wonky. We are in a time when two things can be true at once—the economy is strong and there are some wobbles within. (See Figure 3.)

According to Cristian deRitis, deputy chief economist for Moody’s Analytics, New York, “Data collection is still suffering from some of the pandemic issues. The typical seasonal patterns we observe in economic indicators such as employment or retail sales were disrupted during the pandemic as activity was restricted ... and households shifted their spending towards buying more physical goods rather than services.

“It remains to be seen if consumers will return to their old habits or if some of these changes will be permanent,” he said.

Is a recession coming?

When it comes to an imminent recession, deRitis sees no consensus either way. He pointed to several factors. One was the 2023 gross domestic product (GDP), which was revised from 4.9% to 5.2% in the third quarter of 2023, building from Q2’s 2.1%, per the Bureau of Economic Analysis. Q3 strength was expected to lift 2023’s year-end average to perhaps as high as 2.4%. As of November 2023, Moody’s projected real GDP to average out to 1.7% in 2024.

“For [Moody’s], we tell people just stay calm and ride out a bumpy but good economy,” deRitis said.

“If you had looked at 2023 Q3 growth projections six or seven months ago, you would have seen 1% or less,” Kuehl said.

“We got 4.9% in part because we started to see a dramatic rebuilding of inventory. People reacted to the supply chain crisis by buying as much as they could and stockpiling. Inventories built up. That threw off the whole reorder cycle (in Q2). That inventory build got pushed to the third quarter as inventory began to erode,” he said.

Alex Carrick, chief economist for ConstructConnect, Cincinnati, added that Q3 strength was also driven by a sharp fall in the saving rate and a strong rise in government spending.

ConstructConnect’s senior economist, Michael Guckes, had an additional thought regarding inventory: “This might be a good opportunity to right-size inventories and take advantage of some cost savings with things like just-in-time inventory management.”

Regarding the possibility of a recession, Kuehl said, “For contractors, a recessionary chill can be a matter of where you live and what industry you’re serving.

“I don’t see a recession in 2024, though there will be parts of the country, like California, that might feel recessionary as their economy has slowed. For contrast, Texas is the opposite story—it’s booming.”

Kuehl added that consumer buying was strong in the latter half of 2023.

“We had a good Halloween and a pretty decent November,” he said. “What used to be Black Friday is now Black November, a whole month full of discounts.”

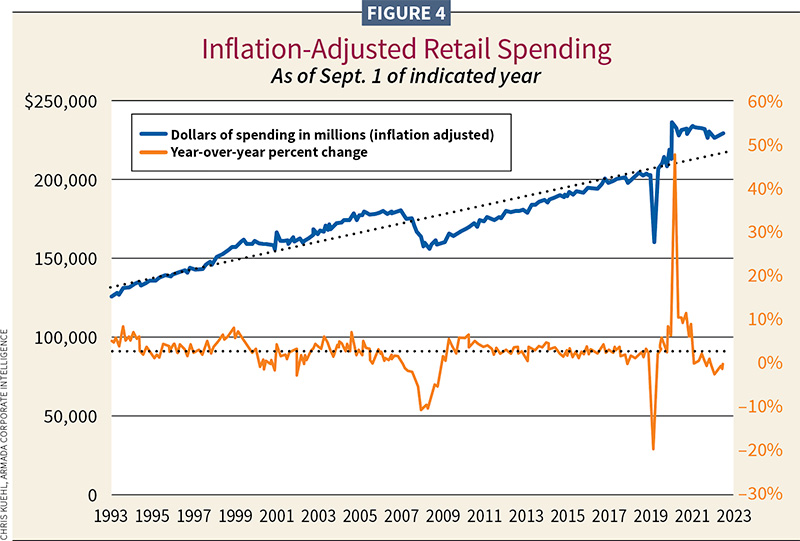

The National Retail Federation, Washington, D.C., reported a record 200.4 million consumers shopped over the five-day holiday weekend from Thanksgiving through Cyber Monday. It reported 121.4 million people visited brick-and-mortar locations. Online shoppers totaled 134.2 million, up from 130.2 million in 2022. (See Figure 4.) Total holiday sales for 2023 were expected to increase between 3% and 4% over 2022.

What’s the Fed going to do?

“The U.S. economy has remained recession-free, paying off in 2023 in a lot of ways that will shift over into 2024,” said Richard Branch, chief economist for Dodge Construction Network, Hamilton Township, N.J. “We’re anticipating that 2024 will bring about more consistent growth and more opportunity, but the economy will remain challenged at least over the next three to six months. Key in this forecast is the Federal Reserve.”

Branch and deRitis believe the Fed is done raising rates. Rates stayed between 5.25%–5.5% in December 2023. So, when will the Fed start cutting rates?

“We’re assuming that they are going to start in the third quarter of 2024, but in increments of 1.4 basis point every quarter,” Branch said. “That means we reach an equilibrium rate around 2.5% in early 2026. Could be a little more, it could be a little less. The economy performs at its full potential probably around 2.5%.”

Branch expects construction in 2024, particularly in the residential sector, to show some inhibited growth.

“Nonetheless, we think by the end of the year, the U.S. economy is going to be on much more stable footing, which should create more opportunity in the construction market,” he said.

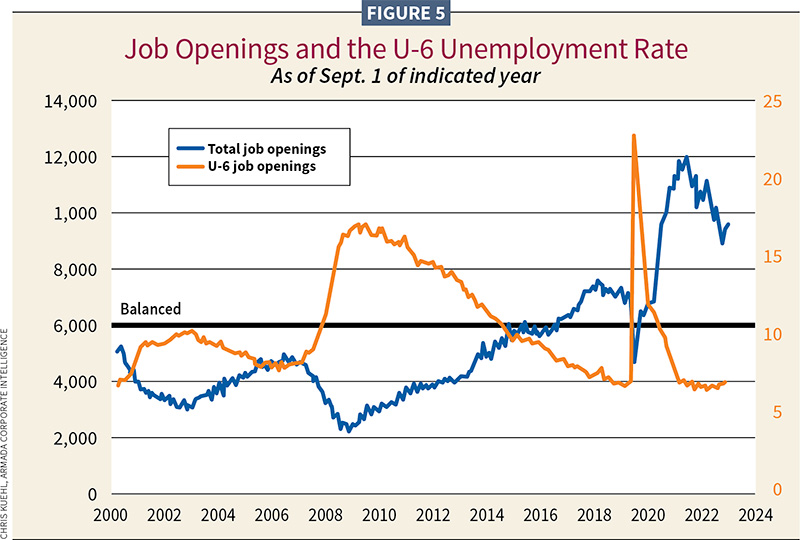

Kuehl added that there is cushion even if rates do rise during a period in 2024. He pointed to a rarely looked-at cut of data provided by the U.S. Bureau of Labor Statistics (BLS) called U-6. BLS has six classifications of unemployment, U-1 through U-6. U-3 (the number of people receiving unemployment benefits) is most often quoted when monthly unemployment numbers are announced. U-6 includes discouraged workers and underemployed (involuntarily part-time) workers, neither of which typically applies for unemployment.

“U-6 numbers are as low as they have been in years,” Kuehl said. “That gives us room to keep rates where they are or maybe even raise them. People are still getting jobs during inflationary times.” (See Figure 5.)

Regarding GDP, Kuehl made a point not usually considered in this report.

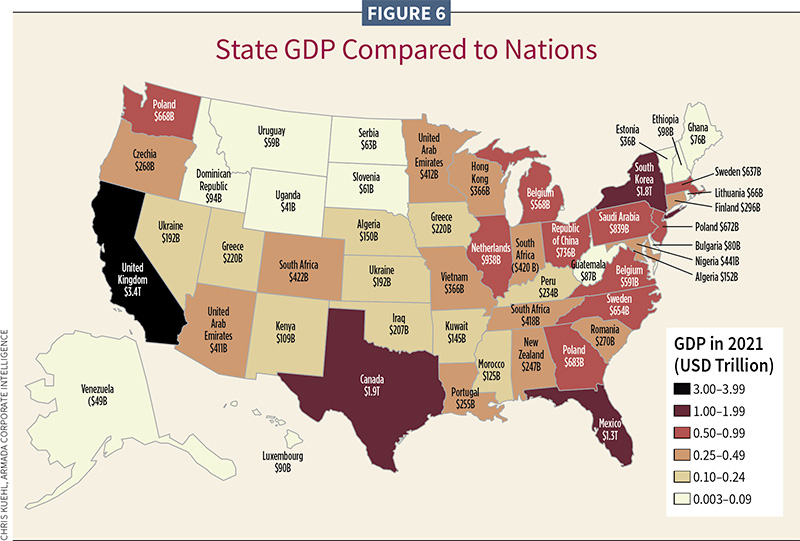

“Lest we forget, globally, we are the big economic dog by a long shot,” he said. “No other country or collection of countries like the European Union come even close. Further, every single U.S. state matches another country’s GDP. Kansas corresponds to Ukraine. California alone has the same GDP as the United Kingdom. That makes it one of the sixth or seventh largest economies in the world.” (See Figure 6.)

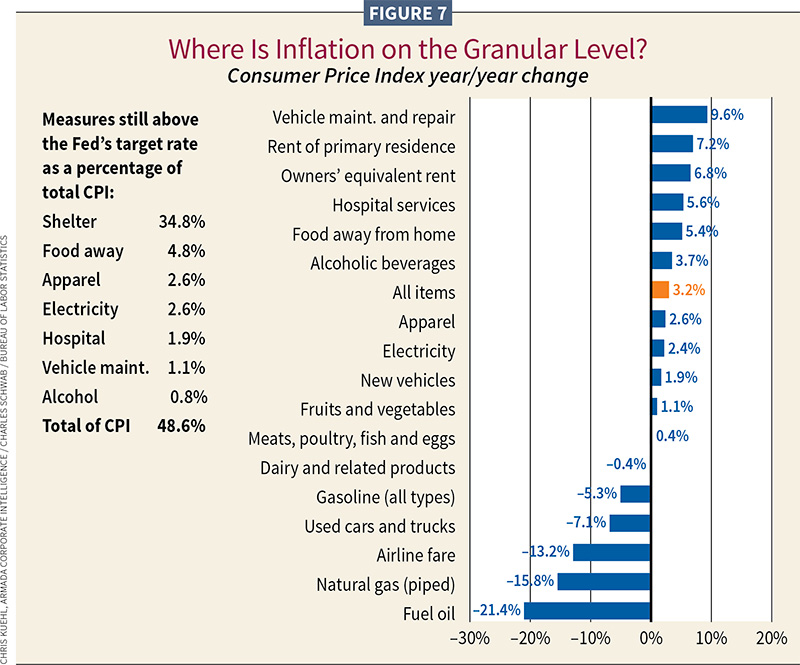

He also pointed to strengths shown in the Consumer Price Index (CPI) (See Figure 7).

“We have seen a real drop in prices for natural gas, oil and gasoline. Those have all been big factors in dropping the inflation rate to where it is now [3.1% for the 12 months ending November 2023]. These, however, are historically volatile commodities. It doesn’t take much to suddenly jack the price of oil up. For now, oil prices have been in the lower $80 range, be it Brent Crude or West Texas Intermediate. That is going to be a big contributor to keeping inflation down,” he said.

Other tailwinds bolster growth

“There are still lots of projects coming online that are supporting construction activity,” deRitis said. “We have the Infrastructure Investment and Jobs Act (IIJA) favoring construction of roads, bridges and other public works. The Inflation Reduction Act (IRA) supports construction of battery plants and other green-energy projects. Finally, the CHIPS and Science Act favors the construction of semiconductor plants.” For more on this, read ”We’re in the Money” on page 70.

“Manufacturing is really taking off,” deRitis said. “Semiconductor plants are making their way through the economy. Infrastructure projects take a little bit longer to be allocated, but you could think of that as actually a benefit. It’s a constant source of support over the next few years rather than coming in all at once.”

“The economic benefits of working toward a greener energy world [are] coming to focus, with such commitments from battery manufacturers for electric vehicles of all sorts. And there’s onshoring going on across different industries, not just chip manufacturing, everything from other electronics, and even apparel,” he said.

“You are seeing production moving to Central and South America or East Asian countries other than China. In general, all this activity is going to support the construction of manufacturing facilities as well as additional warehouses to lower the risk to supply chains,” deRitis said.

Kuehl said that the United States now imports more from Mexico than China. Factoring in lower transportation costs, Mexico makes even more sense.

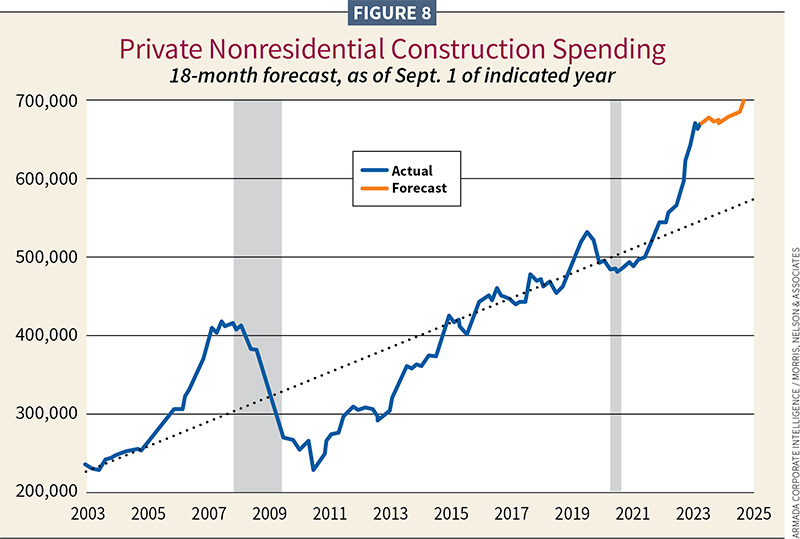

Kuehl’s Armada Corporate Intelligence, in partnership with Morris, Nelson & Associates, provides 18-month forward forecasts called “The Watch,” using seven major areas of durable manufacturing as a basis. The monthly forecasts hit 98% accuracy.

“Construction spending is almost exponential,” Kuehl said. “It just keeps going. Even with a little bit of a decline, we’re still growing, and the expectation is continued growth in 2024” (e.g., see figures 8 and 17). The Watch covers manufacturing in automotive, aerospace, machinery, computers and electronics, electrical equipment and appliances, fabricated metals and others.

Carrick weighed in with his tailwinds to the economy, as well.

“The whole energy transition shift that’s underway virtually guarantees that there’s going to be huge capital spending, which is good for the construction industry,” he said. “Consumer spending on travel and entertainment leads to strength in hotel construction.

“There are all kinds of upcoming projects in the transportation area including rapid transit and airports. Also, it gladdened my heart when I learned of private equity firms becoming involved in megaprojects [$1 billion or more]. One of those is Plus Power LLC, which announced completion of $1.8 billion in new financing for standalone battery storage projects,” Carrick said.

The incorporation of wind and solar to help clean the grid continue. The projects are being developed to help stabilize the U.S. electrical grid.

Carrick pointed to continued strength in megaprojects. In ConstructConnect’s “Winter 2023–2024 Construction Starts Forecast,” he wrote, “Large projects started in Q3 included two prisons, two data centers and a single megaproject categorized in hotels, multifamily residential, power and miscellaneous civil engineering.” He also pointed to new pipeline work.

The risks

There are plenty of risks that continue to bump up against the economy.

According to Kermit Baker, chief economist for the American Institute of Architects (AIA), Washington, D.C., while the overall economic outlook has improved, there are dark clouds on the horizon.

These include persistent regional banking concerns, which could lead to tighter lending standards; economic fallout from likely future federal budget showdowns; return of student loan repayments; ongoing labor issues; potential reacceleration of inflation (rising oil prices, higher labor costs); and ongoing geopolitical tensions. He also said that the meltdown of the Chinese economy may be felt in the United States

“We worry about the unexpected sending a shock to the system,” deRitis added. “We’ve seen U.S. [oil] production pick up, but a shock here could impact consumers and make life difficult for the Fed. All of this could disrupt the forecast for the economy.”

Banking and credit

Potential disruptions, such as failing banks, are a concern for deRitis and others.

“You do have certain construction loans getting harder to come by, as banks are reluctant to preserve capital at this point,” deRitis said. He noted that commercial real estate loans will come due over the next five years, which is “going to be more corrosive than an immediate shock to the system.”

Kuehl thinks some effects may be felt sooner.

“There’s $1.4 trillion worth of commercial real estate loans coming to maturity,” he said. “They’re going to be renegotiated, and with much higher interest rates. That may serve as a real blow to the construction sector for at least the next two years.”

Kuehl also pointed to funding as his chief inhibitor to construction projects.

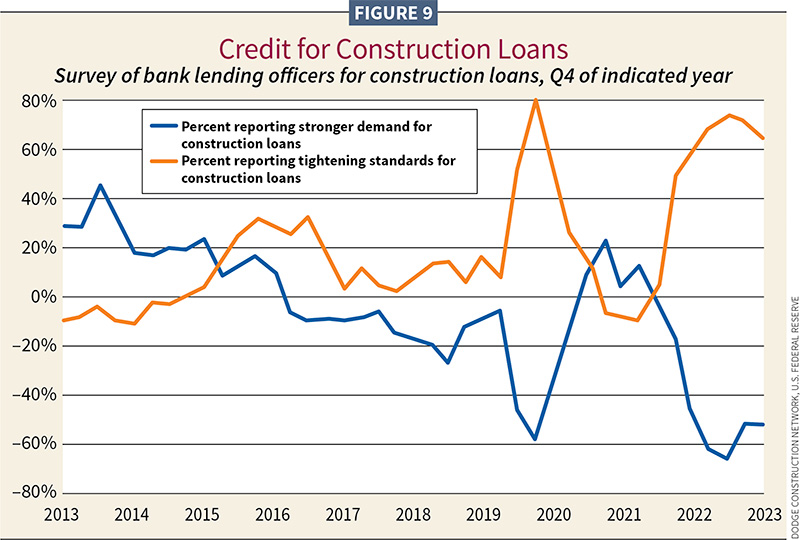

“It used to be that if your company is well run and your books are right, then you’re commercially acceptable and financial institutions will loan you money. Now, financiers are also looking at the industry you’re in. If you are involved with residential housing, or office buildings, loans will be harder to get. If you’re in warehouse development and logistics, that’s a different story. If you’re a manufacturer that is servicing, say, the automotive sector or the aerospace sector, bankers may be happier.” (See Figure 9.)

The consumer could play a role in slowing the economy.

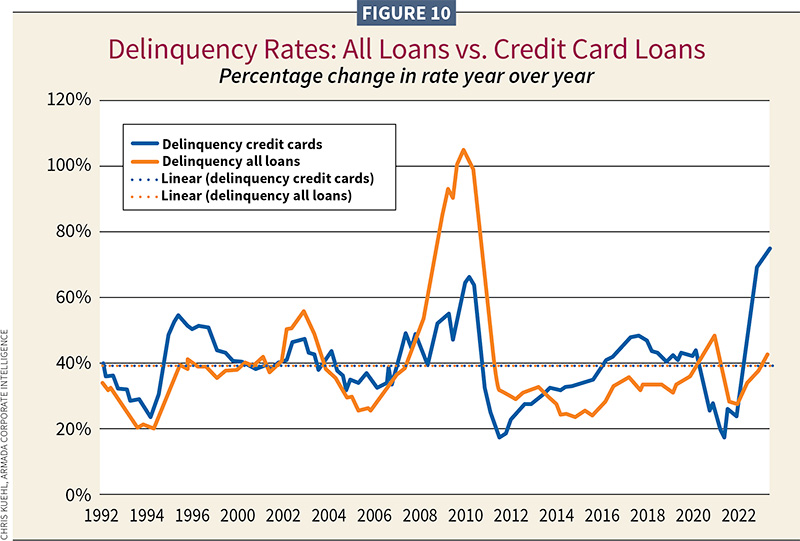

“Credit card loans are now sliding into delinquency,” Kuehl said. “Currently, the U.S. consumer collectively has $70 trillion in debt; $7 trillion of that is credit cards. So, there’s a lot of trepidation, particularly for the lower third of income earners. They’re the ones living paycheck-to-paycheck, using their MasterCard to pay their Visa. You’re beginning to see some of that distress floating up into the other two-thirds of income earners. It isn’t a crisis yet, but it’s moving in that direction.” (See Figure 10.)

“I think the important question is when the next economic crisis comes, are we going to be able to replicate the kind of monetary and fiscal stimulus that we’ve had in the last two recessions? I think that’s somewhat problematic,” Carrick said.

“We’re closing in on $2 trillion a year in deficit spending by the government in recent years, annually,” Dodge’s Guckes added. “This increase is dramatically faster than at any time other than during a major war. At present, money from the IIJA and some of the other funds represent billions and billions of dollars—a huge influx.”

But risks could to lead to a benefit, Guckes said. “The government ... has taken a solid long-term vision as to where it wants construction to go—a green, carbon-neutral environment. When you put that kind of money behind it and, if you can put the right kind of regulations or stipulations behind it, I think private industry does a very good job of getting behind it when the rules are clear, [which is] a tailwind for manufacturers.”

Geopolitics

Economists look at geopolitical events or risks, ranging from an expanding war in the Middle East to the ongoing conflict between Russia and Ukraine and tension between China and Taiwan.

Branch noted that if other actors get meaningfully involved in the Middle East conflict, there could be a run up in oil prices that could affect growth in 2024. Kuehl said that, while the United States does not depend on Mideast oil, the commodity is still priced internationally.

“Treasury bills were yielding less than 1% as recently as late 2020. T-bills are now reaching 5.5%. This takes a grade of money away from investors that might have gone into construction real estate,” AIA’s Baker said. He also pointed to a decline in commercial property values (–9%) and residential with multifamily leading (–13%).

“I’m also telling people to factor in risk management with our forecast,” deRitis said. “You want to be prepared for the uncertainty. With little control over these risks, it’s important to be guarded and mindful.”

Residential, the canary in a coal mine

If there is one thing most economists agree on, the residential sector is fuel for the entire economy, including sectors such as retail and commercial to hospitals and schools. Unfortunately, the tank isn’t full.

The National Association of Homebuilders (NAHB), Washington, D.C., was expecting starts of about 1.4 million units (single-family and multifamily combined) in 2023. That would represent an 11% decline. This year, an additional but smaller 3% decline (around 1.3 million units) is forecast. In 2025, however, NAHB expects a 7% increase (1.4 million total starts).

Danushka Nanayakkara-Skillington, assistant vice president, forecasting and analysis for NAHB, defined the current landscape for the residential market.

“Mortgage rates, sometimes nearly as high as 8%, are really hurting the buyer traffic. Meanwhile, builders are struggling on the other side because of the construction loans and acquisition development.

“Loan rates at this point have doubled from what they were paying in 2020–2021. These loan rates and the consumer’s higher mortgage rates are really hurting the single-family market,” she said.

Asked what she felt might be a sweet spot mortgage rate to trigger a housing rebound, Nanayakkara-Skillington said, “Probably around 6%, which we might not see until 2025.”

“A 6% rate would be reflective of numbers in 2018–2019 when the federal rate and mortgage rates were a little bit higher than previous years but kept home purchases healthy. In 2024, we expect some rebound landing at around 950,000 units.”

Single-family numbers for 2023 settled in a little over 900,000 units, a 9% decline compared to just over a million in 2022.

“If you are a homeowner, you’re essentially in the ‘golden handcuff’ situation,” Nanayakkara-Skillington explained. “An existing 2%–4% mortgage rate might prevent you from moving or selling your home, creating an artificially low supply of homes in the existing market. We have a deficit of 1.5 million homes.”

NAHB derives its housing estimates from data supplied by the U.S. Census Bureau’s Building Permits Survey and from the Survey of Construction, which is partially funded by the United States Department of Housing and Urban Development.

“[Millennials] are in the peak home-buying years, and there’s not enough houses at this point. We’ve had a decade of under-building since the end of the Great Recession [between 2007 and mid-2009],” Nanayakkara-Skillington said. “The demand for housing is there; the problem is supply. It’s waiting to be unleashed. People are waiting to buy houses.”

She said the multifamily housing market did well, though it suffered a decline in starts. Currently, there are more than a million units of multifamily under construction.

“Looking at 2024, we have some headwinds such as high commercial lending standards and interest rates. For 2024, we forecast around 386,000 units,” she said, adding that NAHB expects growth at 400,000 units in 2025.

NAHB expects housing costs and mortgage rates to moderate as inflation eases and the Fed draws down interest rates. Finally, remodeling has been a strong component to prop up housing start weaknesses, though it too has slowed.

“In 2022, remodeling work increased 9%,” Nanayakkara-Skillington said. “We added 1% growth in 2023. In 2024, we expect flat growth and perhaps 2% gains in 2025. Housing stock is around 40 years old, so there’s going to be a lot of upgrades that need to happen for many of these homes.”

In encouraging news, the U.S. Census Bureau reported that housing units in November 2023 rose 15% over the previous month representing a 9.3% y/y gain. For single-family, that represented an 18% gain (34% y/y). For multifamily, there was growth of 8.9% but an overall loss of 34% y/y.

A smaller queue for projects

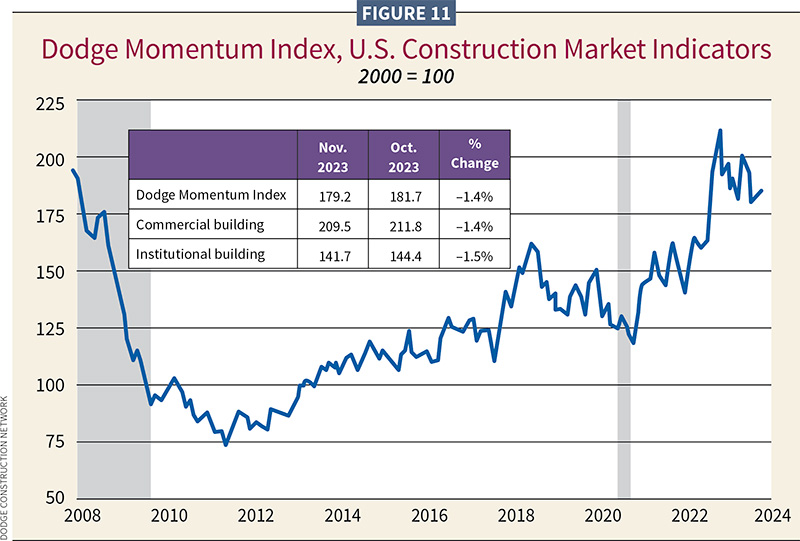

The Dodge Momentum Index is Dodge’s leading indicator of nonresidential construction activity. It tracks building projects (under $500 million) when they first enter the early stages of planning. Manufacturing is excluded to keep the DMI data less volatile (see Figure 11). November 2023’s DMI report showed a 1% decrease to 179.2 after October’s 1% gain of 181.7, and September’s reading of 180.3. Year-over-year (y/y) the DMI was 14% lower than in November 2022. The commercial segment was down 20% from year-ago levels, while the institutional segment was up 2% over the same period.

Branch sees the 2023 DMI as projects in the queue are being delayed while developers bide their time until they feel more confident (e.g., better credit availability and interest rates). He expects those projects will then break ground. He added that he is seeing numbers stabilize.

“The planning data is telling us more about what’s going to happen in the back half of 2024 once the interest rate market stabilizes and reverses, the economy itself feeling more stable,” Branch said. “That’s when these projects will start moving through to groundbreaking.”

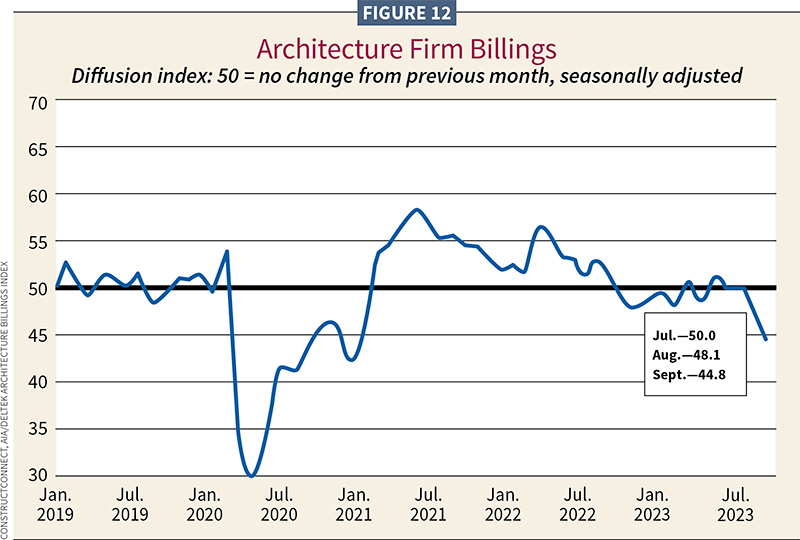

Another metric of work in queue is the AIA/Deltek Architecture Billings Index (ABI), an economic indicator for nonresidential construction activity. Any score below 50 indicates a decline in firm billings. In November 2023 the ABI repeated October’s score of 44.3, seasonally adjusted, the lowest reading since December 2020 and down from 44.8 in September (see Figure 12).

“A slowdown in buildings and architecture firms has been matched by a slowdown in new project work coming into firms,” Baker said. However, the ABI downturn was much sharper in previous recessions. He added that levels of backlog work, while shrinking, remain a bright spot.

“[Backlogs] were as high as 7.2 months on average in early 2022 but have been drifting down since with a reading of 6.5 months in the third quarter of 2023. All things considered, backlogs have held out quite well when compared to prior cycles,” he said.

The AIA Consensus Construction Forecast of nonresidential is another useful snapshot. Produced twice a year, the survey of the nation’s leading construction economists forecasts business conditions (put-in-place spending) over the next 12–18 months. The panel includes U.S. nonresidential construction forecasters from the Dodge Construction Network, ConstructConnect, Moody’s Analytics and six others. Baker shared results from the July 2023 iteration.

“The panel was very optimistic about how [2023] will turn out. Of the almost 20% growth projected for the year, a good chunk comes from the industrial side, but the commercial side and the institutional side are also seeing very healthy growth,” Baker said.

In 2024, the picture looks a good deal different. The panel sees modest declines on the commercial and industrial sides. The institutional side shows a 1% gain in 2024.

Bid but not built

“In a lot of ways, 2022 was a boom year, so it was entirely expected to see an 8% decline this year (2023),” said Claire Stubblefield, ConstructConnect’s vice president of product strategy for data products.

“Meanwhile, U.S. planning project data (projects in any prebid stage) are also experiencing a decline compared to 2022. We’re trending –7% this year compared to last with planning numbers in line with 2019, back to prepandemic levels. In the United States, warehouses and distribution facilities continue to grow. Hotels, motels, manufacturing, amusement, recreation and data centers are all seeing healthy growth this year compared to last year.

“Conversely, recent data is revealing a slowdown in education, medical and restaurant projects and, of course, office.” Stubblefield cited inflation and labor shortages as headwinds that are slowing bidding.

“A national chain restaurant developer reported that in pre-COVID years, a restaurant would cost them $350,000 to build, but with inflation, that number has tripled to $1 million on average for just the labor and materials.”

“Once you factor in the cost of the land, kitchen equipment, point of sale systems, they reported that the cost typically climbs to $2 million,” she said.

Employment grows, but not enough

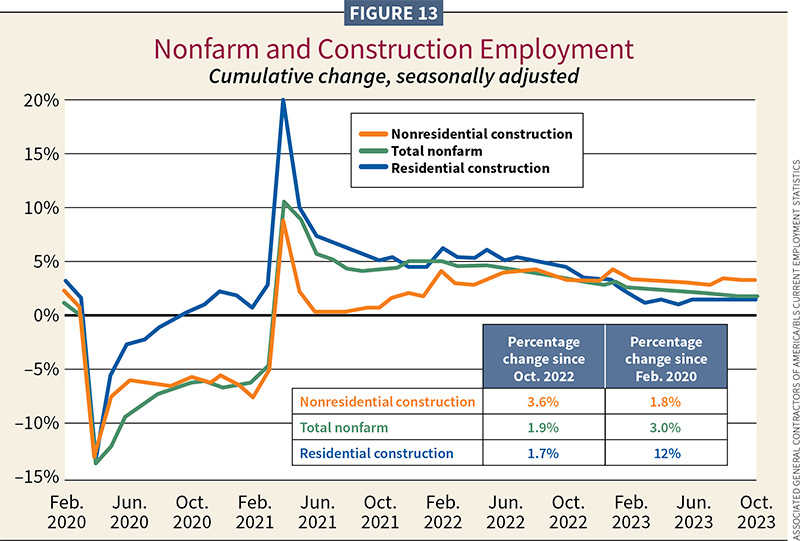

BLS reported nonfarm employment increased 199,000 in November 2023, and the unemployment rate stood at 3.7%. (see Figure 13).

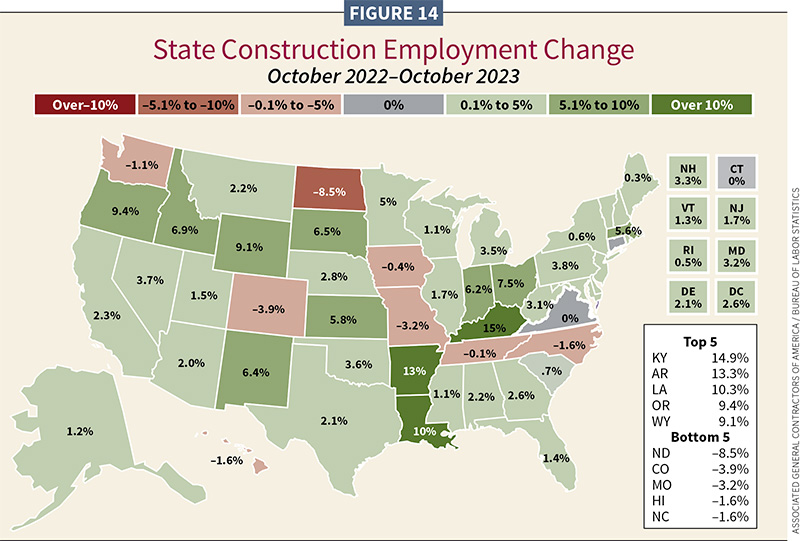

Ken Simonson, chief economist for the Associated General Contractors of America (AGC), Arlington, Va., found construction employment rising steadily in 2023. Construction employment, seasonally adjusted, totaled 8,033,000 in November, a gain of 2,000 from October and 200,000 (2.6%) y/y. From October 2022 to October 2023, construction employment rose 3.6% compared to 1.9% for total nonfarm employment. Seasonally adjusted construction employment rose in 40 states and the District of Columbia, fell in eight states and held steady in Connecticut and Virginia. (See Figure 14.) Residential construction employment came as a surprise.

“It’s still growing at a rate almost as much as total nonfarm payroll,” Simonson said, adding that multifamily is providing the strength. He also suspects a decline in single-family employment bottoming out. Multifamily is a bit of a paradox.

“While the number of units under construction is hovering around a million, starts have been dropping at a rate of 30% or so,” he said.

He pointed to problems finding switchgear, transformers and electronic components for elevators and HVAC systems slowing projects but keeping workers employed.

“Once that equipment comes through, employment here is going to drop. That may be an opportunity for nonresidential firms that have really been having trouble finding employees,” Simonson said.

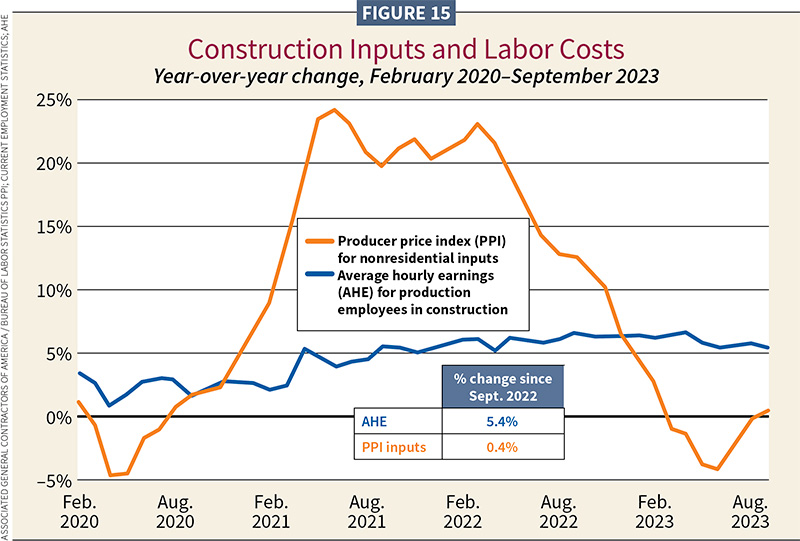

“The unemployment rate in construction has come all the way down to the same level as the overall economy, 4% or less,” Simonson said. “That’s exceptional, but there still are not enough workers available for construction. The industry has reacted to the difficulty of finding workers by paying more.

“Construction pay is going up a little faster than it is in the rest of the private sector, up 5.4% (fastest since 1983) versus 4.4% for production workers in the private sector,” he said. (See Figure 15.) He thinks the construction industry is going to have to raise pay more as it is at a greater disadvantage, since jobs cannot be done remotely or on a hybrid basis with flexible hours.

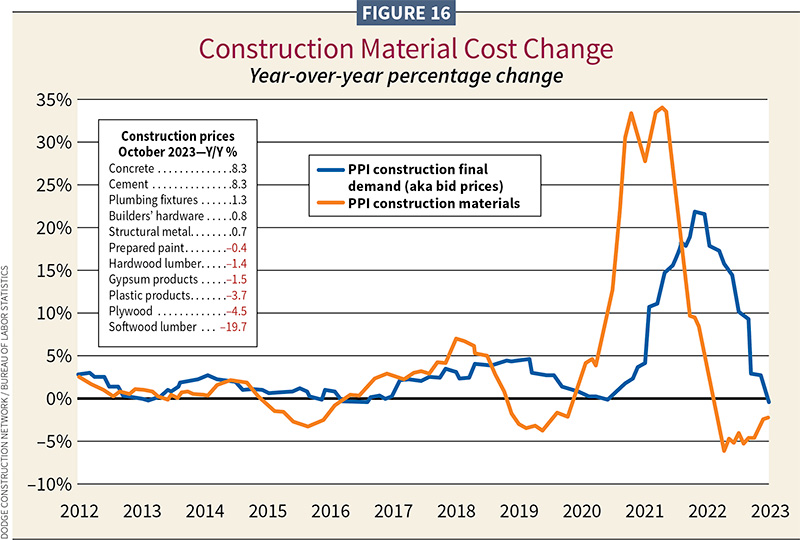

Materials costs

Materials costs, while going down in some areas, remain volatile. (See Figure 16.)

“After the economy shut down, we saw record prices for lumber, steel, copper [and] frequent and steeper than usual price increases for things as diverse as concrete, plastics products, roofing materials and gypsum,” Simonson said.

“It’s a different story in 2023, for the most part. On a y/y basis (2022–2023), the Producer Price Index (PPI) has shown materials cost prices tapering off for a few months. They were negative on a year-over-year basis. The last couple of months, they’ve been basically level to where they were the previous year.”

AGC reported November 2023 PPI for material and service inputs to new nonresidential construction were little changed from October, declining 0.2% (rising 0.1% y/y. Most inputs had modest changes. A dramatic exception was diesel fuel, up 0.9% but showing a steep 30% y/y decline in price.

In other materials, ready-mix concrete rose 0.2% and 9.4% y/y; while cement fell 0.7% and rose 8.3% y/y. Other PPI declines included steel mill products (-1.5% and -8.4% y/y); lumber and plywood (-0.2% and -11% y/y); and truck transportation of freight (-0.6% and -8.7% y/y). Changes in PPIs y/y for new, repair and maintenance work by electrical subcontractors was 0.1% and 2.5% y/y.

Simonson added, “Despite the recent moderation, the cumulative change in the inputs PPI since February 2020 is 37%, nearly double the 19% increase in the CPI, the most cited measure of inflation.

“My own guess is that we’ve seen the end of declining materials cost and in the next year will likely see a 4% to 6% increase,” he said. “We’re already starting to hear about a further round of cement and concrete product price increases to take effect early [in 2024].”

Kuehl said that nickel and aluminum prices are not moving even though there is an inventory dive. Copper, crucial in the electrical contracting world, is behaving oddly.

Internal population migration

“We are seeing a lot of redistribution of where people live,” Kuehl said. “The West Coast is losing population rapidly and it’s being driven out predominantly by the high cost of living. People are leaving high taxed and high cost-of-living states. This has always been a motivator, but it’s been more accelerated because of the ability to work remotely while living in a more affordable state. Lower-cost locales, such as Tulsa, are incentivizing people to move to their city.”

Kuehl added that urban areas, such as Dallas, are losing population. Conversely, that city is also representative of a trend of gaining suburban population. Rural areas are gaining, too.

Simonson shared that 18 states—a record number—lost population in 2023.

According to the U.S. Census Bureau, the South accounted for 87% of the nation’s growth in 2023.

“Population growth has also been concentrated in the Intermountain West,” Simonson said. “Southeast Florida became the fastest growing state for the first time since 1957, just nosing out Idaho, which had been number one for five years, and it’s still strong. In addition, folks from all over the country are moving to Texas.”

Sector performance and forecasts

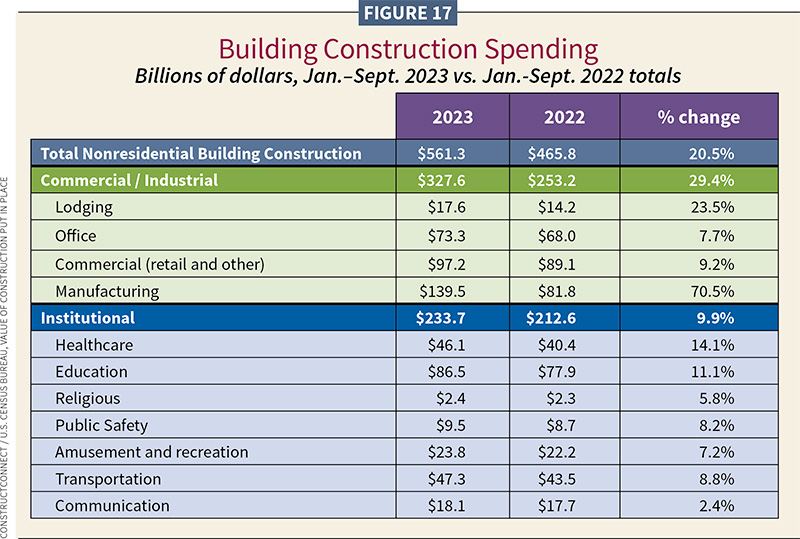

Starts information is supplied by Dodge (cited first), followed by ConstructConnect, unless otherwise noted. Some of the starts can differ widely between the firms. Many are attributable to different vertical mixes. We try to reconcile those differences or cite them when they occur. Dollars are not adjusted for inflation unless otherwise stated. See Figure 17 for an overall view of construction spending.

RESIDENTIAL

“Stilted growth”

- 2023: –13%/$363B (Dodge Construction Network); –21.9%/$291.3B (ConstructConnect); –11% (NAHB)

- 2024: 11%/$406B (DCN); 4.4%/$304.3B (CC); –3% (NAHB)

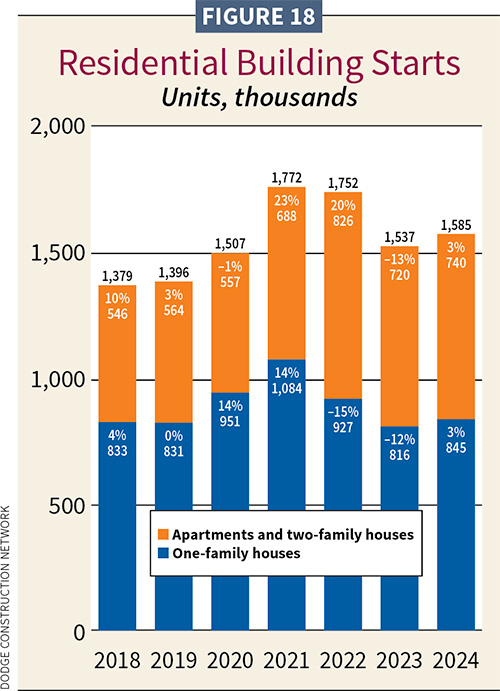

The residential sector continues to bear the brunt of higher mortgage rates and affordability issues retracting growth in 2023. Rates for a 30-year mortgage rose to nearly 8% in 2023 but are expected to steadily decrease, stimulating single-family starts. Dodge’s Branch categorized this year as “stilted growth.” Multifamily will also see a return to growth, though modest. (See Figure 18.) National vacancy rates as reported by iProperty Management stood at 6.6%, as of late November 2023, up 13.8% from the 2022 average.

“Higher vacancy rates will suppress multifamily construction,” Branch said. He sees a realignment in multifamily after the development “sugar rush” in 2021 and 2022. The top hot markets for multifamily in 2023—after New York, still home to some of the bigger high-end projects—were Miami, Los Angeles, Dallas, Boston and Atlanta.

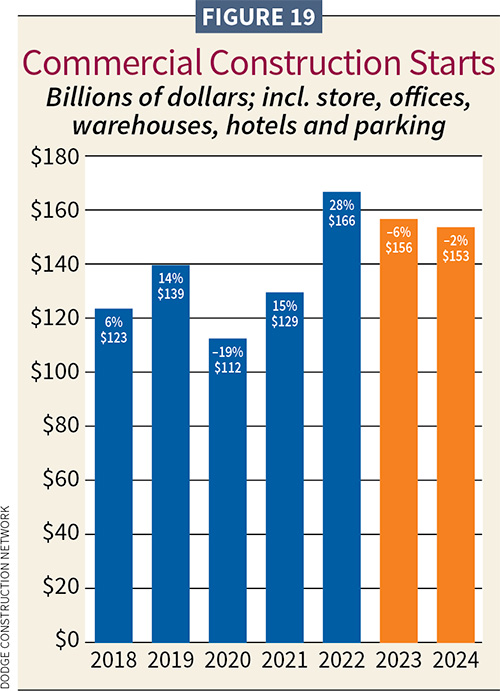

COMMERCIAL

Mixed performance with weaker sectors

- 2023: –6%/$156B (DCN); –2.2%/$119B (CC)

- 2024: –2%/$153B (DCN); 5.8%/$125.9B (CC)

Commercial starts lost some ground in 2023. Dodge and ConstructConnect reported negative growth. (See Figure 19.)

“When the economy slows down, commercial starts slow down,” Branch said.

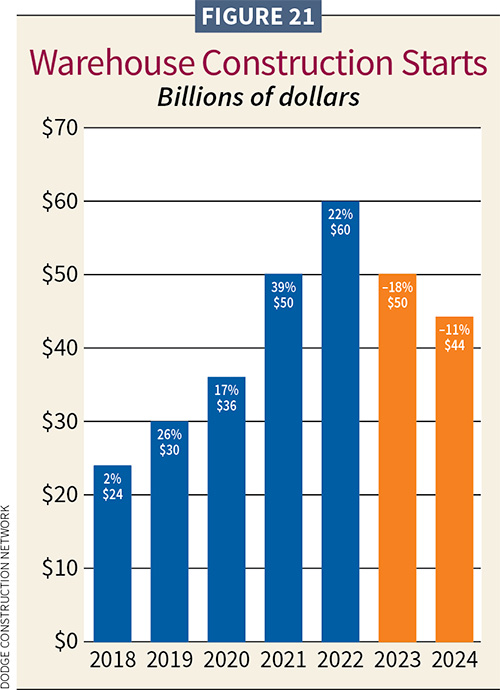

Warehouse activity was soft. If you removed warehouses, Dodge’s –2% prediction for commercial in 2024 would be positive.

“Amazon, which is about 16% of all warehouse construction, has essentially stepped aside,” he said.

He sees this sector also undergoing a realignment into 2024 as it continues to diversify, e.g., high-tech logistics centers. ConstructConnect, meanwhile, sees commercial growth this year at 5.8%.

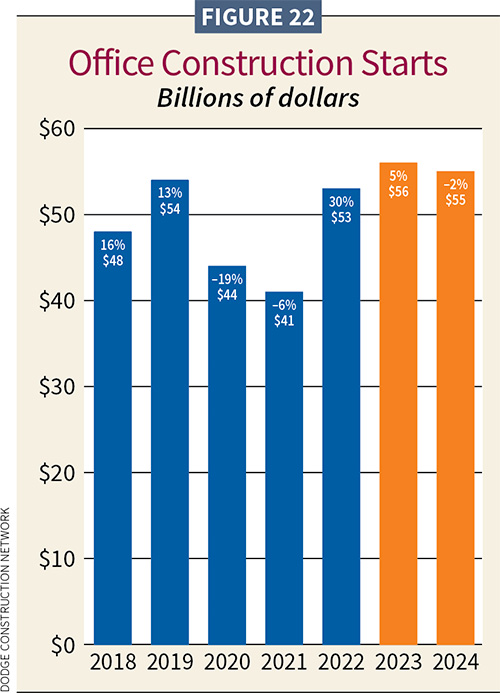

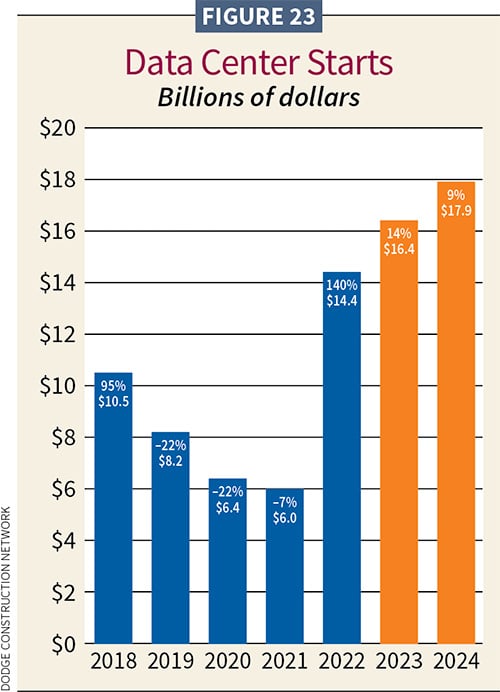

According to Dodge, data centers, which grew 14% ($16.4B) in 2023, with an expected 9% ($17.9B) gain in 2024, helped the office sector. Meanwhile, a slow residential market held back retail starts in 2023, but some better growth is expected this year.

AIA’s Baker said, “On the office side, we’re seeing a fair emphasis on fixing up buildings to attract tenants, reconstruction work.”

Kastle Systems, an access control company based in Falls Church, Va., reported a current 50.3% return-to-office rate.

Hotel starts retreated 5% ($12B) in 2023 from amazing 62% growth in 2022. Starts will climb again in 2024 at 16% ($14B).

“People are traveling, and we’re back to vacationing,” Kuehl said. “It’s catch-up time for the hospitality sector.”

The top commercial starts in 2023 were data centers: Prime Data Center Campus, Elk Grove Village, Ill., $1B; Microsoft (Southern Campus), Mount Pleasant, Wis., $1B; and Facebook Stanton Springs Phase 1, Social Circle, Ga., $642M.

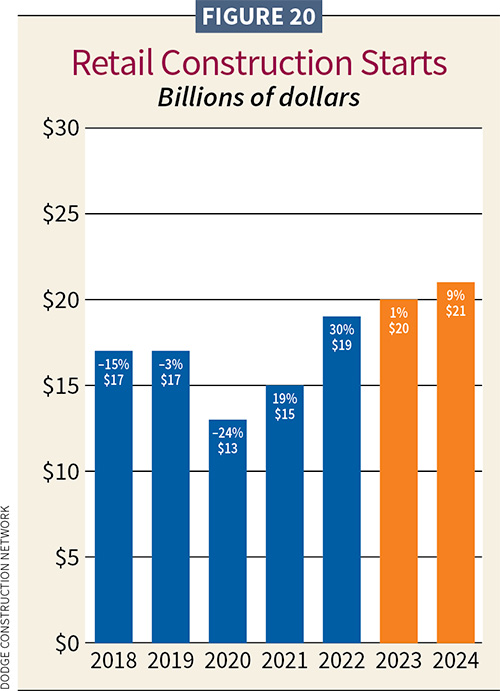

Retail (see Figure 20)

- 2023: 1%/$20B (DCN); –8.5%/$14B (CC)

- 2024: 9%/$21B (DCN); 22.4%/$17.2B (CC)

Warehouses (see Figure 21)

- 2023: –18%/$50B (DCN); –24.7%/$22.4B (CC)

- 2024: –11%/$44B (DCN); 4.6%/$23.4B (CC)

|  |

Hotels

- 2023: –5%/$12B (DCN); 16.2%/$12.8B (CC with motels)

- 2024: 16%/$14B (DCN); 13.8%/$14.6B (CC with motels)

In the classes of hotels—from luxury to economy—midmarket with breakfast and other food is most linked to business travel. Hotels are betting on a big return to that.

Office buildings (see Figures 22 and 23)

- 2023: 5%/$56B (DCN); –6%/$22.8B (CC)

- 2024: –2%/$55B (DCN); –7%/$22.4B (CC)

|  |

INSTITUTIONAL

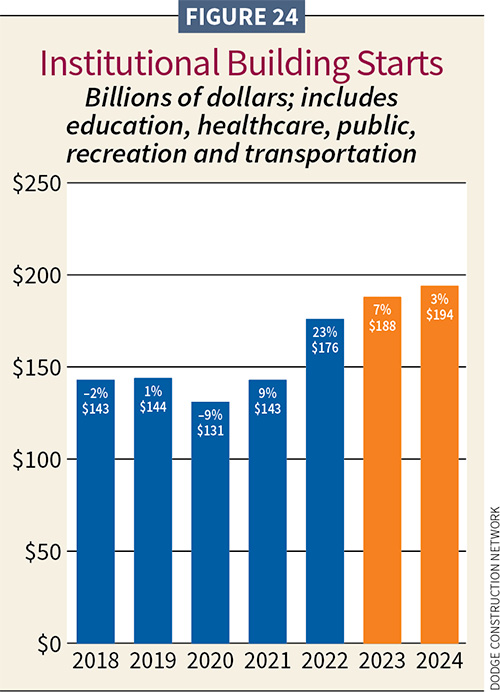

Small cooling, yet record growth

- 2023: 7%/$188B (DCN); 8.1%/$153B (CC)

- 2024: 3%/$194B (DCN); –1.9%/$150.5B (CC)

*ConstructConnect projections for this sector are harder to neatly quantify alongside Dodge. Its estimates are addressed below, largely within related Dodge subsectors.

Dodge saw institutional gain (7%/$188B) in 2023, its best performance in 13 years. Smaller growth in 2024 (3%/$194B) elevates record-breaking gains. ConstructConnect saw 8.1%/$153B in 2023 growth but expects a small contraction (–1.9%/$150B) in 2024 (see Figure 24).

Education K-12 was boosted by state and local funding. Both sources had healthy budgets. Though demographics soften (number of children) as one looks ahead, for now it depends on location. Branch said that the demographic trends in the South and West are much stronger than the Northeast or the Great Lakes states.

In 2022, the square footage of K-12 building was nearly five times the size of the post-secondary market.

College construction also did well in 2023. ConstructConnect showed those starts rising 11.5% in 2023, but this year it sees starts declining maybe by $2.7B. State and local budgets also supported healthy starts of religious buildings, public buildings including capitals, courthouses, police and fire buildings, detention facilities and others.

Healthcare is looking solid, with strong activity in the “doc-in-a-box” market (urgent care clinics). Branch added that as retail construction grows in the suburbs, urgent care clinics should follow.

“We are starting to see some reinvestment in the healthcare and the hospital market,” Branch said.

Life sciences buildings and labs continue to provide strength for institutional construction, too.

Education

- 2023: 11%/$83B (DCN); 17.7%/$70.4B (CC)

- 2024: 4%/$86B (DCN); –1.2%/$69.6B (CC)

K-12

- 2023: 18.4%/$59B (CC)

- 2023: –2.5%/$57.5B (CC)

DCN does not break out this sector.

College and Universities

- 2023: 11.5%/$24.5B (CC)

- 2024: –24.5%/$21.8.B (CC)

DCN does not break out this sector.

Healthcare

- 2023: –1%/$37B (DCN); –15%/$21.9B (CC)

- 2024: 5%/$39B (DCN); 10%/$24.1B (CC)

Transportation buildings

- 2023: –13%/$21B (DCN); 5.9%/$7.5B (CC)

- 2024: –4%/$20B (DCN); 7.5%/$9B (CC)

Recreation buildings

- 2023: 10%/$21B (DCN); 33.4%/$9.2B (CC)

- 2024: 2%/$22B (DCN);–9.2%/$8.8B (CC)

Miscellaneous institutional

- 2023: 33.3%/$13.1B (CC)

- 2024: –13.1%/$11.4B (CC)

DCN does not break out this sector.

“Miscellaneous” encompasses religious and public buildings including capitols, courthouses, police and fire buildings, detention and other administrative facilities.

The top three commercial-related institutional projects as of October 2023 were the JetBlue Terminal Expansion JFK (Terminal 6), Jamaica, N.Y. ($2.2B/1.2 million sf); Hartsfield Jackson Airport Concourse D, Atlanta ($1.4B/350,000 sf); and Midfield Satellite Concourse South, Los Angeles ($1.4B/150,000 sf).

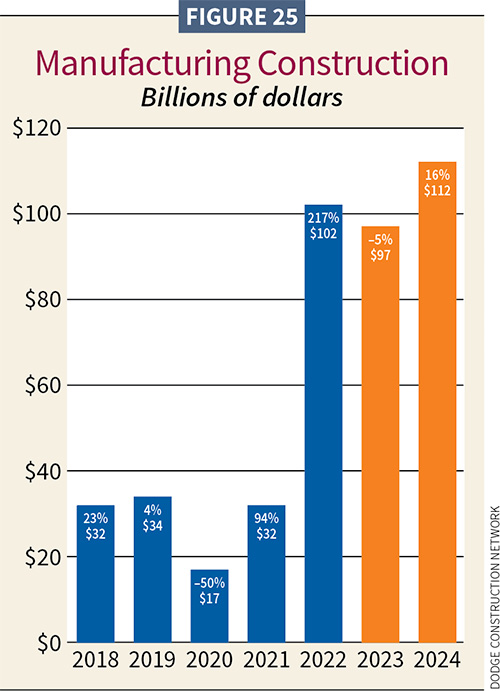

MANUFACTURING

- 2023: –5%/$97B (DCN); –30.35%/$79.9B (CC)

- 2024: 16%/$112B (DCN); –14.2%/$68.59B (CC)

While manufacturing grew an astounding 217% in 2022, softening in 2023 still represented enormous construction starts for this sector. Dodge found manufacturing starts declined 5% ($97B) in 2023. This year, gains of 16% ($112B) are forecast. (See Figure 25.) Reshoring efforts are having an impact (e.g., chip fabrication plants and others), as are electric vehicle (EV) battery plants and more. The CHIPS and Science Act and the IRA will stimulate activity for several years. ConstructConnect verticals may not line up directly with Dodge, which may explain their capturing of negative growth in 2023 (–30.34%) and continuing into 2024 (–14.2%).

In October 2023, capacity utilization for U.S. manufacturing output moved down 0.6 percentage points to 77.2%. The rate was 1% below an average held between 1972 and 2022. The 2023 UAW automotive strike took a bite out of production, drawing down the durable manufacturing index by 1.3%. Capacity utilization measures the rate at which potential output levels are being met or used.

Of note, EV manufacturing is expected to grow. Reported recent sales weakness may be temporary, as supply chain issues have resolved—that will help alleviate EV shortages and delays for customers. Although Ford scaled back some of its battery manufacturing, U.S. automakers have invested an estimated $210B to develop and make EVs, according to the Natural Resources Defense Council. The Energy Information Administration reports that U.S. sales of hybrid, plug-in hybrid and battery electric vehicles reached 17.7% of new light-duty vehicle sales in Q3 2023.

Top manufacturing starts in 2023 included the Texas Instruments Fabrication Plant (Project Bruno) in Lehi City, Utah ($11B); Micron Microchip Fabrication Building in Boise, Idaho ($7.5B); and Micron Technology Semiconductor Megafab/Phase 1, Clay, N.Y. ($6.4B).

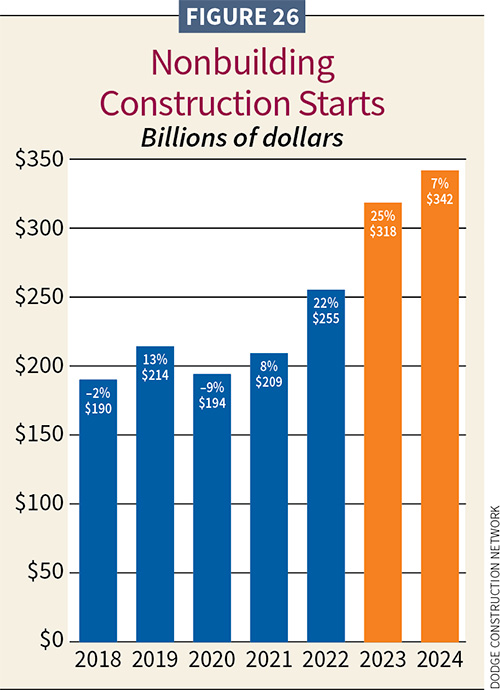

NONBUILDING

Growth continues, lifted by stimulus

- 2023: 25%/$318B (DCN); 15.8%/$233B (CC)

- 2024: 7%/$342B (DCN); 8.1%/$252B (CC)

2023–24 infrastructure—it’s all good

“In measuring the impact of infrastructure dollars coming out of Washington [D.C.], we are just getting a sense of how much money is sitting out there in the market,” Branch said. “We do know that in roads and bridges, 60% of the federal dollars have been announced. Work in this sector is also accelerating in 2024. In public works projects, dollars are rapidly increasing.”

When the federal appropriations pass, as anticipated this month, Branch expects infrastructure work will accelerate by the middle of the year.

Dodge and ConstructConnect see continued growth, though forecast less robustness in 2024 (see Figure 26).

Meanwhile, power and utilities work was very strong in 2023 per ConstructConnect, with starts advancing 51.5%. Advances will slow in 2024 to 19.2%. Dodge saw a 57%/$87 billion advance for this sector in 2023. It sees starts in 2024 retracting 17%/$72 billion.

Influencing 2024 and beyond and serving as a portend for future utility work is the Grid Resilience and Innovation Partnerships (GRIP) program. Part of the IIJA, the $10.5B GRIP program offers competitive grants for grid resilience, smart grid and other grid innovation. The U.S. Department of Energy is also involved in related cost-sharing projects with utilities.

Bridges and streets/highways

(see Figure 27)

- 2023, Bridges: 14%/$26B (DCN); –12.08%/$24B (CC)

- 2024, Bridges: 25%/$32B (DCN); 15%/$27.6B (CC)

- 2023, Streets and highways: 14%/$94B (DCN); 12.66%/$95.2B (CC)

- 2024, Streets and highways: 23%/$115B (DCN); 4.2%/$99.2B (CC)

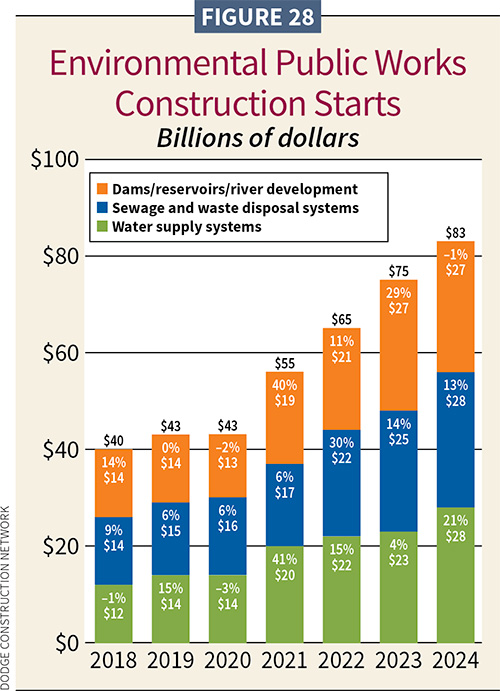

Environmental Public Works

(see Figure 28)

- 2023, Dams and reservoirs: 29%/$27B (DCN); 9.4%/$11.4B (CC)

- 2024, Dams and reservoirs: –1%/$27B (DCN); 9.4%/$11.3B (CC)

- 2023, Water supply systems: 4%/$23B (DCN)

- 2024, Water supply systems: 21%/$28B (DCN)

- 2023, Sewage and waste: 14%/$25B (DCN)

- 2024, Sewage and waste: 13%/$28B (DCN)

*ConstructConnect combines water supply systems and sewage treatment: 12.97%/$48.8B (2023); 5.15%/$51.4B (2024).

|  |

Power and utilities

- 2023: 56%/$87B (DCN); 51.5%/$44.53B (CC)

- 2024:–17%/$72B (DCN); 19.2%/$53.10B (CC)

One of the top nonbuilding projects of 2023 was the Rio Grand LNG Export Terminal Phase 1, Brownsville, Texas ($12B).

SUMMARY

World events loom larger than in the recent past, which could throw off growth. Meanwhile, the Fed may be done raising rates, but do not expect rates to decline until the second half of the year, and then very tepidly until the Fed feels inflation has been tamed. The funds provided to the construction industry through the IIJA, IRA and CHIPS and Science Act are making their way into the economy, which bodes very well for the manufacturing and nonbuilding sectors. The decline in single-family construction may have bottomed out if mortgage rates drop a few points. Multifamily will slow. Nonresidential will continue enjoying some strengths and navigating challenges.

ConstructConnect’s Guckes offered this overall good advice on multiple fronts: “Finding workers is hard. Figure out how to make them more productive. I think this is really what’s going to separate the winners from those who simply do well [in 2024]. Think about, too, how you can diversify your revenue stream to temper weak performing markets.”

Look forward to a pretty decent forecast as 2024 progresses. As this forecast concludes, the construction weatherman says, “Over to you, electrical contractors.”

Bonotom Studio, Inc. / Stock.Adobe.com / DURIS Guillaume/ dStudio / lesniewski

Information found in this year's forecast was provided in part from three webinars: The Construction Economy Forecast, Nov. 8, 2023 (ConstructConnect); Outlook 2024: Under Pressure, Nov. 16, 2023 (Dodge Construction Network); and The Artful Dodger Economy: How Much Longer? 2024 Economic Update, Nov. 28, 2023 (Chris Kuehl/ELECTRICAL CONTRACTOR magazine).

Click here to watch the on-demand recording of ELECTRICAL CONTRACTOR's webinar, or watch it below.

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].