If you are interested in reading the 2020 topline report, click here.

Our Profile of the Electrical Contractor happens every two years. In 2020, it overlaps with the presidential election, the U.S. Census and the coronavirus pandemic. Of course, we didn’t expect that last one. Our survey asks you to take a look back at your previous year’s business. As such, our 2020 report provides a unique snapshot of the year before COVID-19 hit. For many ECs, 2019 was a good year, expanding on growth seen in our 2018 report. Many firms grew in size and revenue, and a number also expanded into more lines of work. A majority of ECs expressed strong confidence in continued economic strength over the next few years.

Those positive attitudes were based on real data points gathered from more than 1,600 readers who responded online and by mail to this year’s survey. Twice as many firms added employees as lost them in 2019. There are signs that the steady aging in the industry could be leveling off. Also, firms continue to move beyond traditional electric power/distribution into new areas, including higher percentages of ECs expanding into installations such as lighting controls, building automation and the growing electric vehicle charging industry.

Upbeat predictions could seem overly optimistic in at least the near term, given the impact massive stay-at-home orders have had on economists’ outlooks, but ELECTRICAL CONTRACTOR sees reason for hope in your responses. Notably, ECs’ confidence in the growth of the economy over the next few years persisted during the course of our survey process, even as economic conditions began shifting dramatically. Those completing the questionnaire from the second half of March into early April were every bit as positive about future business as those who responded before any coronavirus-related lockdowns began.

There’s much more to learn about your views on the state of electrical contruction in 2019. Read on for the details. In addition, you can check out the full report online, at profile.ecmag.com and ecmag.com/market-research, where we also provide an archive of past results for easy, over-time comparisons.

Aging slowdown

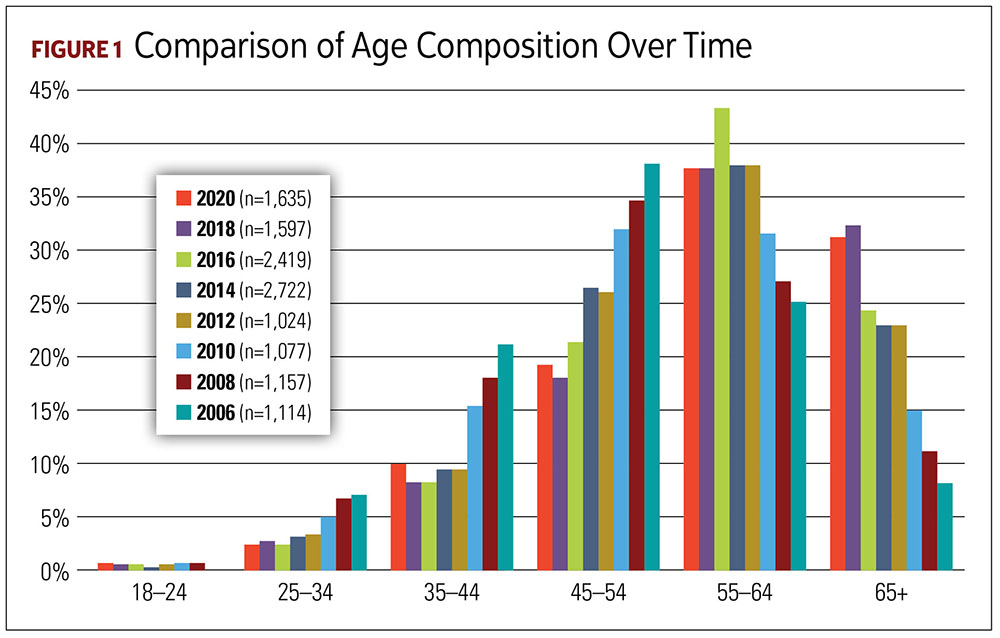

Perhaps the most interesting data point when it comes to EC demographics is how little things have changed. This is the first EC profile in at least a decade in which the average age remained virtually flat from the previous edition—in this case, 57.9, versus 58.2 in 2018, a statistically insignificant difference. Additionally, Figure 1, Comparison of Age Composition Over Time, illustrates the age brackets of 55-64 (37%) and 65-plus (31%) also remain essentially flat, compared to 2018 results. In fact, the combined 35–54 age ranges were the only ones to show growth, up to 29% from 26% in 2018, a statistically significant increase. This is the first time in many years that we’ve seen growth in an age group younger than 65.

Also, as has been the case in the recent past, those working in smaller companies are older than those working in larger operations, though there has been some leveling off. Average ages didn’t rise in firms with 1–4 employees (59.9) and declined among those with 1-9 employees (59.3). It did rise, though, in companies with 10-plus employees, to 55.2 from 53.8.

As in 2016 and 2018, 3% of the electrical contractors who participated in this survey are female. Women are more prevalent in larger firms (5% in firms with 10-plus employees versus 3% among firms with 1–9).

In 2018, we asked about years of experience in electrical contracting for the first time. This year’s responses mirrored those of two years ago, remaining statistically unchanged, at 32.4 years, on average (versus 32.6 years, previously). We found 5% of you have been in the industry more than 50 years—not surprisingly, 92% with that much experience are older than 65.

What has changed, however, is our respondents’ level of responsibility. Company owners and managers make up 69% of the total respondents this year, down from 77% in 2018. And a higher percentage now say their title is master electrician (14%), project manager (6%) or other (6%). In another shift from 2018, the national percentage of owners/top managers doesn’t vary by region; in the previous two surveys, Western ECs were more likely to be owners/top managers.

This year for the first time, we asked companies with three or more employees about the breakdown of the workforce between what they considered on-site electrical workers compared to those considered primarily business/office workers. The answer was a consistent 80% on-site and 20% office.

Firm size trending larger

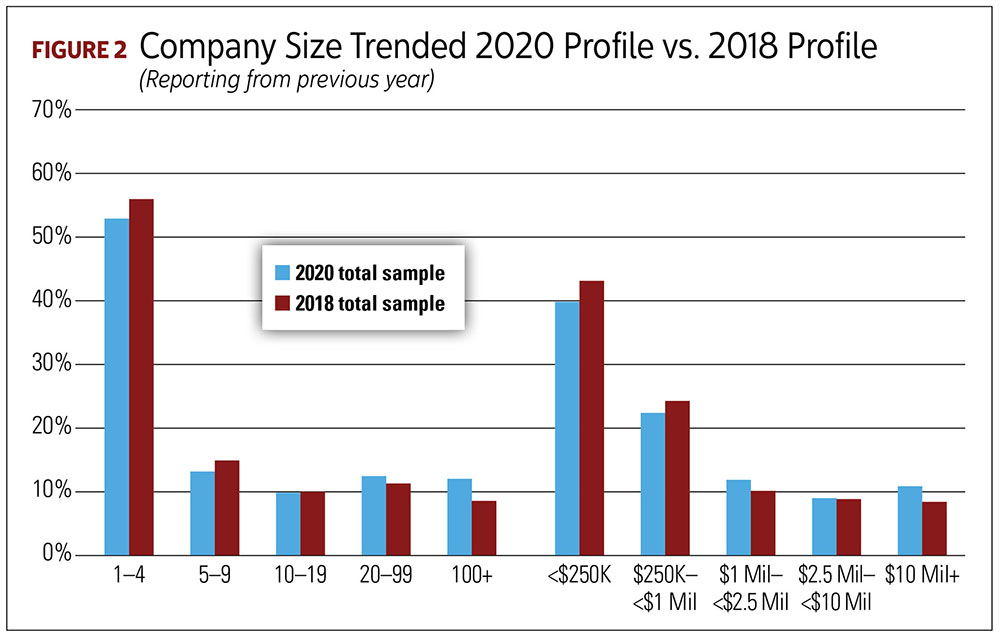

While the majority of EC firms continue to be smaller companies, that percentage has declined significantly since 2018, as seen in Figure 2, Company Size Trended 2020 Profile vs. 2018 Profile. While 56% worked in firms of 1–4 employees two years ago, that figure has dropped to 53% in this year’s survey. Similarly, 43% were in companies with annual revenues under $250,000 in 2018, compared to 40% in 2020. However, the proportion of the largest firms has grown over the last two years, with 12% reporting organizations with 100-plus employees, versus 8% in 2018. And 11% reported annual company revenues of $10 million or more, versus 8% two years ago. A similar pattern was seen between our 2014 and 2016 reports, but 2018’s figures remained stable.

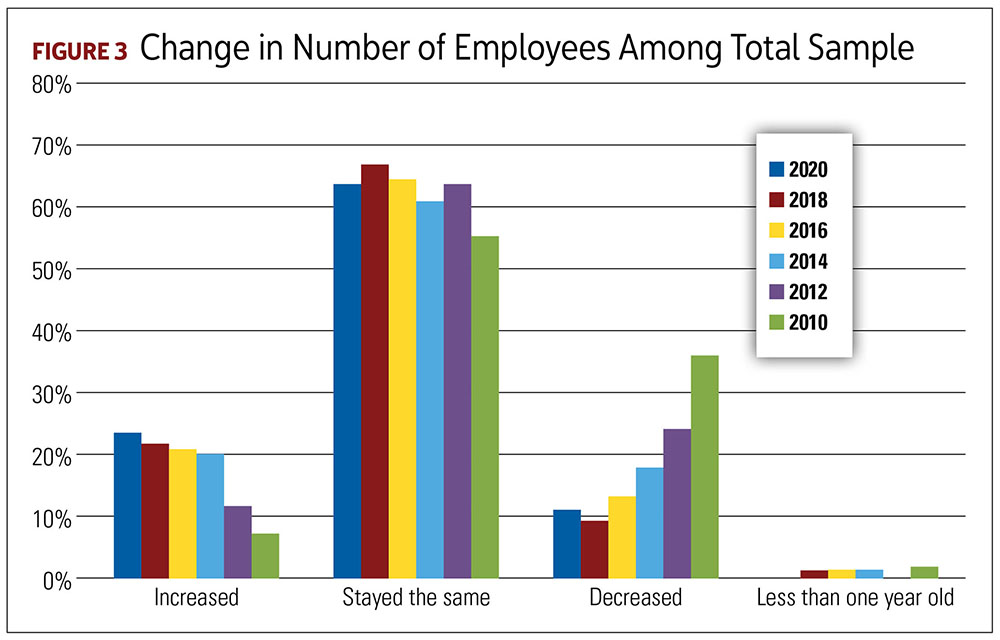

When asked about changes in their company, more than twice as many ECs said their firm had added employees (24%) rather than decreased in size (11%) (see Figure 3, Change in Number of Employees Among Total Sample).

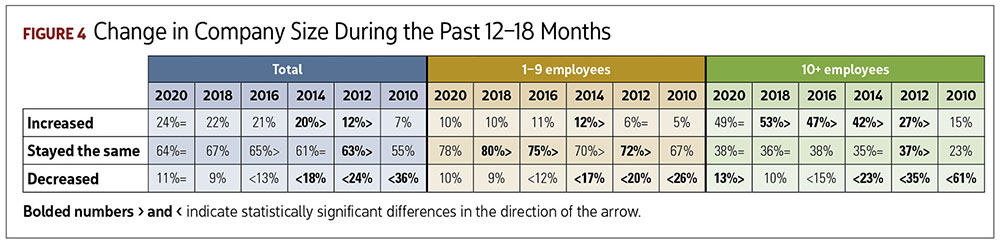

The remaining 64% said company size had remained stable. This is statistically unchanged from 2018. However, there was a small shift, specifically for firms with 10-plus employees. Figure 4, Change in Company Size During Past 12–18 Months, shows these companies were slightly more likely to have decreased in size in the past 12–18 months, versus 2018’s results. The percentage is 13% this year, compared to 10% two years ago.

With reported company growth came the unsurprising fact that 65% of electrical contracting firms said they had difficulty finding trained workers and 29% had trouble retaining them.

The overall trend toward growth carried over into company revenues. Compared to two years ago, more firms now fall into the $1 million or more revenue category, at 31% this year, versus 27% in 2018. Similar increases were seen in the period between 2014 and 2016, but numbers remained stable in the 2018 survey.

Breaking down revenues by firm size illustrates just how broad the electrical contracting field can be. At the smallest end of the spectrum, 71% of firms with 1–4 employees had revenues of less than $250,000. At the largest end, for 53% of companies with 100-plus employees, that figure was more than $25 million.

New this year

Every Profile year, we add new lines of questioning. This year, in one version of the survey, we asked respondents about employee benefits. Overall, 71% of companies offer at least one benefit. Benefits may include paid vacation, health and life insurance, tool reimbursement, paid time off for training, and a pension plan, plus several others.

Also for the first time, we asked about project bid requirements. Fewer than half (44%) of the total firms say they must have a prequalified standards and safety program to bid on a project. Of course, small firms (1–4 employees) are far less likely to have such requirements placed on them. Approximately 55% of firms with 5–9 or 10–19 employees encounter this requirement compared with 24% of firms with 1–4 employees. In contrast, three-quarters of firms with 20-plus employees encounter these requirements.

Across the total sample, about one in five (19%) answered that they must have man-hour requirements for women/minorities or veterans in order to bid on a project. Only 13% of firms qualify as or claim those designations. This requirement generally applies to larger firms and increases significantly and steadily from 9% among firms with 1–4 employees to about 40% for firms with 20-plus employees.

Nevertheless, almost six in 10 firms (59%) say that they already have a certified safety program or they plan to institute one in 2020; the likelihood of having a certified safety plan increases steadily with company size.

Projecting confidence

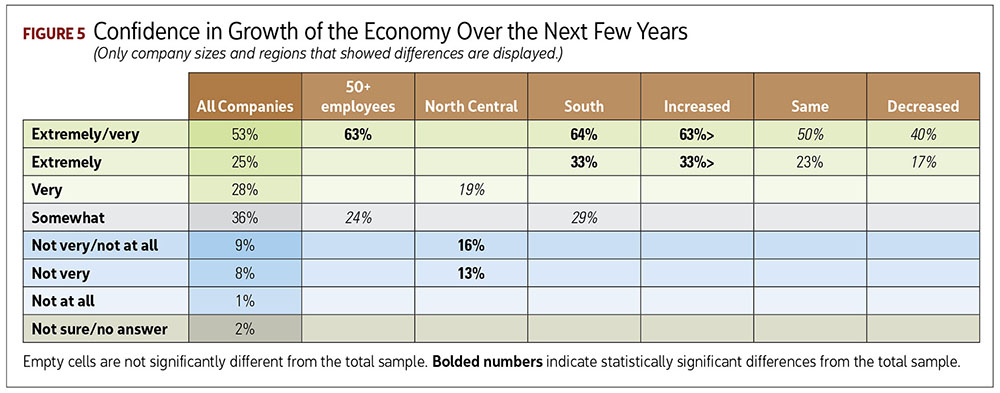

We regularly poll ECs on their confidence in the growth of the overall economy over the next few years, and their answers have remained as positive in 2020 as they were in 2018. Figure 5, Confidence in Growth of the Economy Over the Next Few Years, breaks these answers down, showing that more than half of respondents (53%) described themselves as either “extremely” or “very” confident of economic growth over the next few years, which is virtually unchanged from 2018’s figure. What is particularly interesting, though, is the relatively small (and not statistically significant) drop in confidence between those who completed the survey before the COVID-19 pandemic began having a real economic impact compared to those who completed it once stay-at-home orders went into effect. Of those who completed the survey before March 12, 57% fell into the extremely or very confident categories. That figure fell to 50% among those completing the survey between March 13, when President Donald Trump declared a national emergency, and April 7. Additionally, those saying they were not very or not at all confident of growth remained steady, at 9%, between the two groups. This may reflect the good years leading up to when the question was asked.

2018’s economic shifts continue

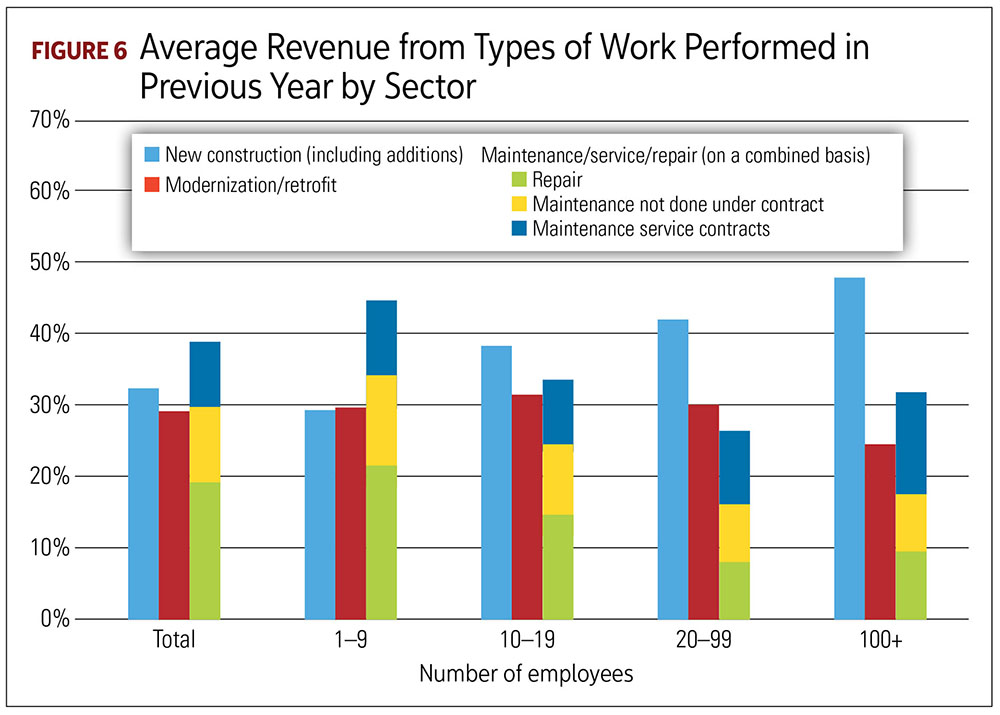

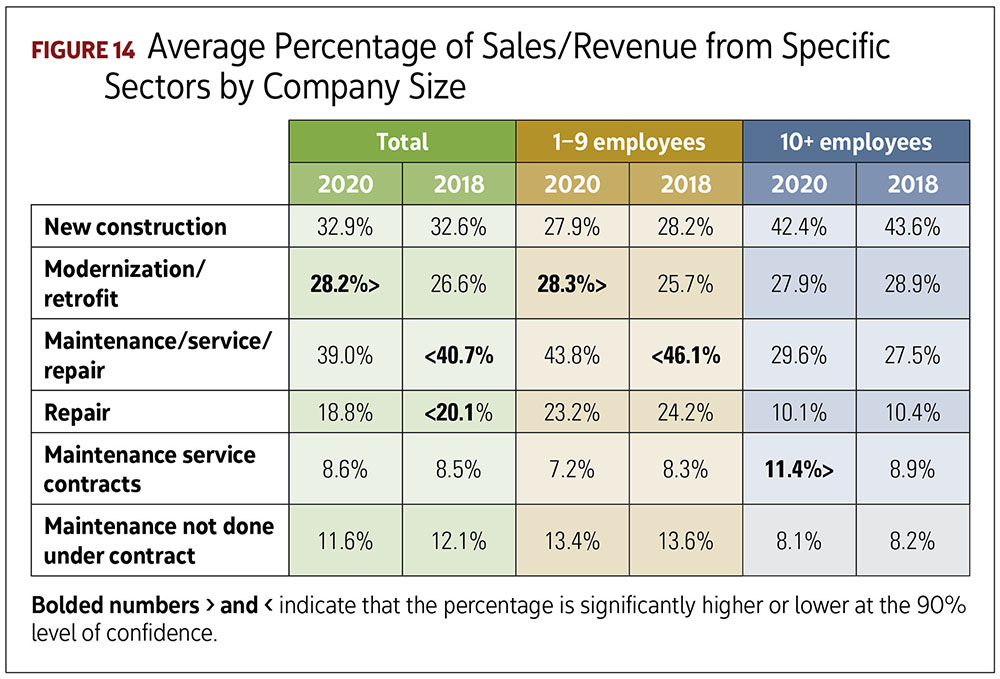

One EC income source that has yet to recover from the 2008 financial crisis is new construction, which accounted for 33% of revenue, on average, in 2019, compared to 43% of 2007 revenue, as reported in our 2008 profile. However, it is important to note that ECs’ average revenue from new construction grows significantly with firm size, as Figure 6, Average Revenue From Types of Work Performed in Previous Years by Sector, shows. Though it accounts for only an average of 27.9% of revenue for the smallest firms with 1–9 employees, it moves up to an average of 46.3% when employee numbers top 100.

Maintenance done on service contracts also is a somewhat bigger slice of business for those largest firms. For firms with 1–9 employees, however, maintenance, service and repair, on a combined basis, remains the most significant revenue contributor (see Figures 6 and 14).

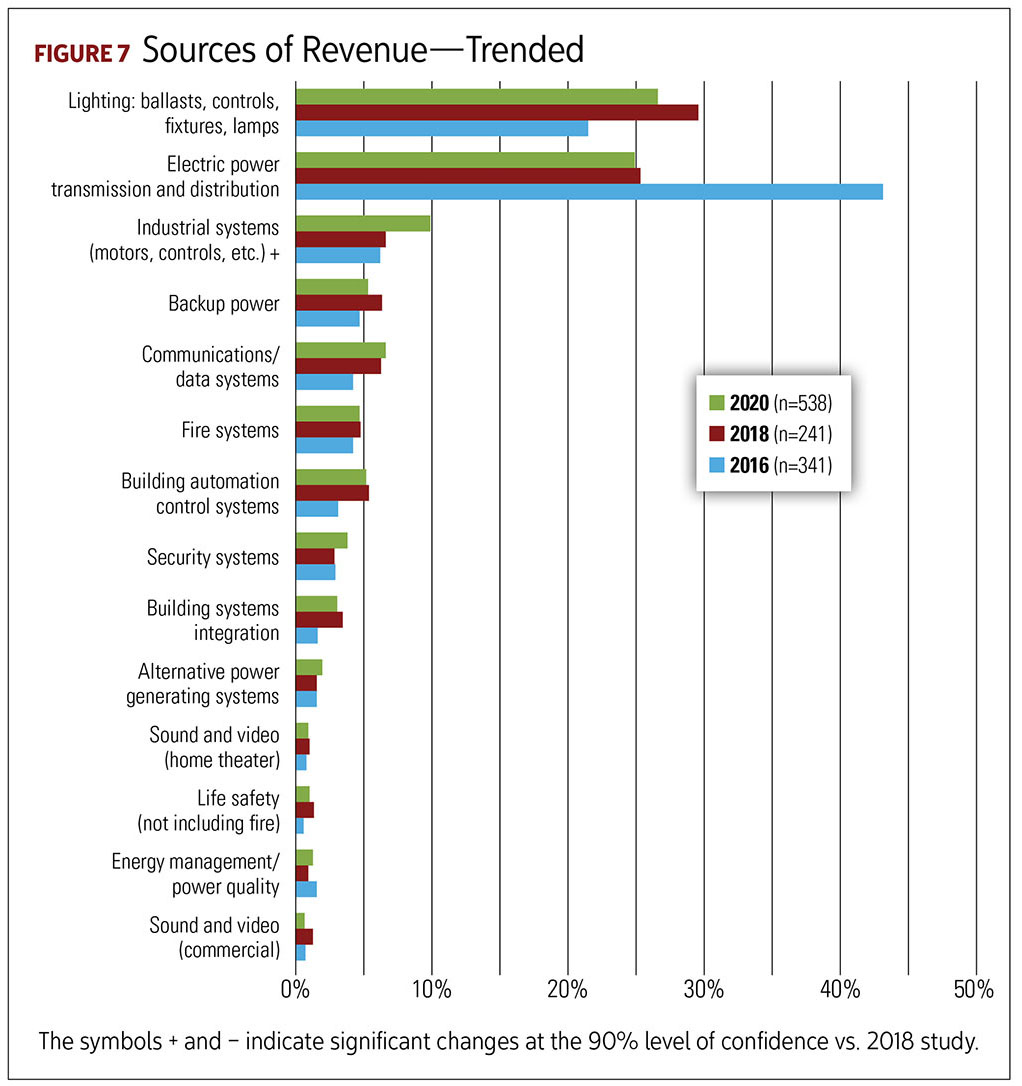

Our 2020 results show a continuation of a shift we first noted in the 2018 Profile, specifically in the proportion of revenue related to various types of electrical work. Electric power transmission and distribution fell dramatically in 2018’s survey, to an average of 25.4% of revenue, from 43% in 2016, as shown in Figure 7, Sources of Revenue—Trended. That result remains statistically unchanged, at 24.8%, indicating a possibly lasting move.

As in 2018, lighting remains the top revenue category, statistically unchanged from 2018. Industrial systems/controls took a step up, though, to an average of 9.7%, from 6.8% in 2018. This move upward doesn’t seem to have significantly taken away from any other specific project type, indicating an overall broadening of work types.

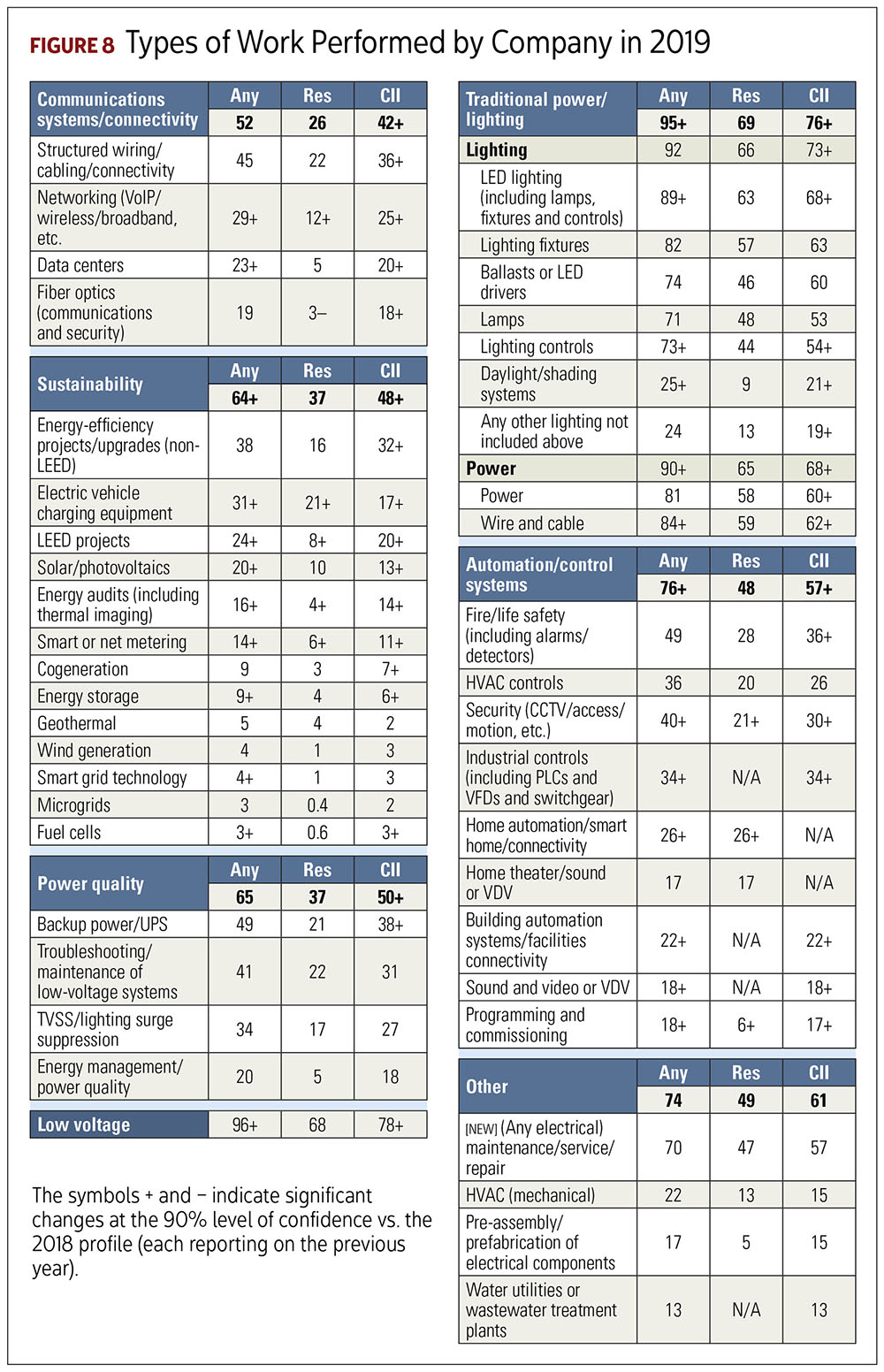

Digging deeper into more specific work categories for 2019, we asked ECs about their involvement in each of a list of up to 43 different project types, in residential and commercial/institutional/industrial (CII) settings. You can see the results in Figure 8, Types of Work Performed by Company in 2019. Power and lighting jobs remain the most important across all job settings and are essentially tied.

Beyond the biggest categories, we see possibly unexpected project types spanning the residential and CII categories. These include several sustainability-related jobs. For example, solar projects come in at a close 10% for residential and 13% for CII. Also, 21% of firms report working with EV charging equipment in residential settings, versus 17% for CII clients. And underscoring the crossover potential of HVAC/mechanical projects for ECs, perhaps as controls become more important, 13% reported working on these jobs in residential settings, with 15% noting involvement in CII job sites.

Combining residential and CII projects, 19 of the up to 43 work types shifted significantly compared to two years ago. This year’s changes were all on the plus side, however, unlike the mix of losses and gains in 2018’s results. Compared with two years ago, more companies worked on:

- Traditional power and lighting, with LED lighting, lighting controls and daylighting posting significant increases, along with wire and cable

Automation/control systems, specifically security, industrial controls, home and building automation, sound and video, and programming and commissioning

- Sustainability, notably EV charging equipment, energy-efficiency LEED projects, solar/photovoltaics, energy audits, smart or net metering, energy-storage systems, smart-grid technology and fuel cells

- Low-voltage work, as a broad category (This area overlaps with many of the other listed project types, especially controls and sound and video installation and maintenance.)

- Looking only at residential construction, there were changes in nine of the up to 39 work types listed for the sector, compared to 2018’s results:

- Growth in networking (which includes voice-over-internet, wireless/broadband and other such efforts), along with several sustainability subcategories and home automation

- Decline in fiber optic work, which seems to contradict the positive trends in networking, controls and communications (Growing adoption of wireless solutions could be one explanation for this data point.

In CII construction, 25 of the up to 41 listed work types showed increases, compared against 2018, including the following broad categories:

- Communications systems/connectivity

- Sustainability

- Traditional power/lighting

- Automation/control systems

- Low-voltage

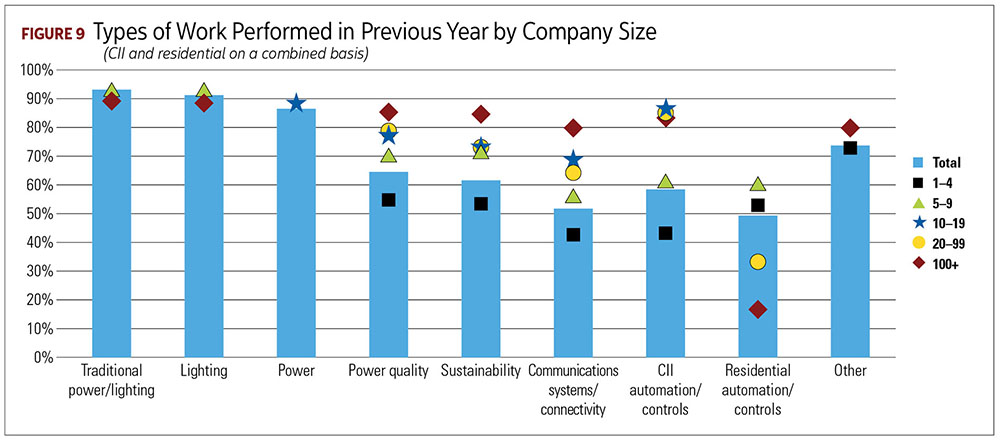

We noted an interesting development, considering types of work by firm size, outlined in Figure 9, Types of Work Performed in Previous Year by Company Size. In a change from recent Profiles, firms with 5–9 employees, rather than the largest firms, are more likely than average to participate in more of the major project-type categories, reporting work in seven of the nine categories. In past surveys, larger firms—especially those with more than 100 employees and also those with 20–99 employees—were more likely to participate in a broader range of work.

As we’ve noted in previous Profiles, firms with 5–9 employees operate much more like larger firms than smaller companies in the range of projects they undertake. However, when it comes to residential construction, the smallest firms are, themselves, pretty diverse in the many aspects of traditional power and lighting projects they work on. These companies also engage with some aspects of power quality, HVAC controls and mechanical work, along with electrical maintenance, service and repair and low-voltage jobs.

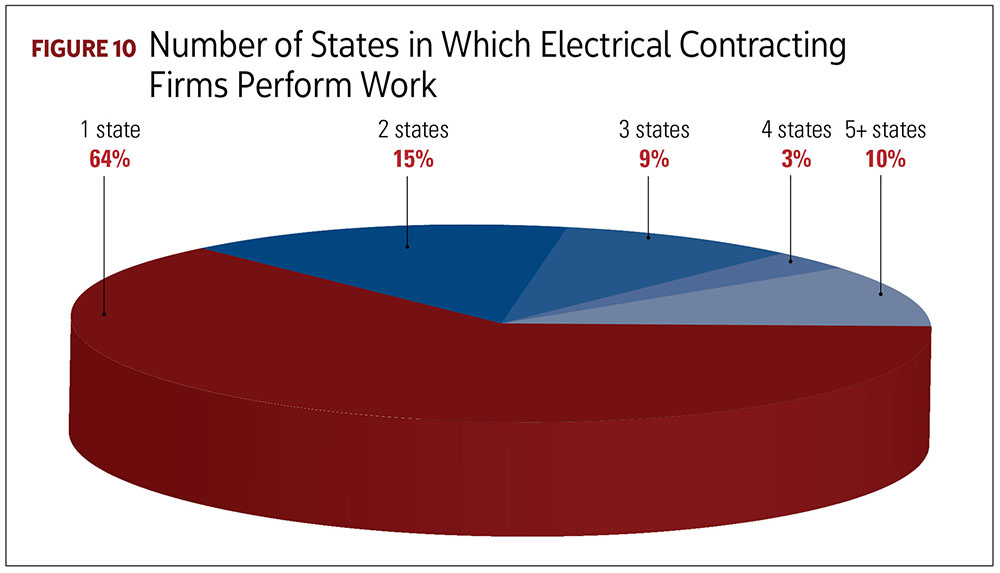

When it comes to where ECs are doing their work, about 36% of respondents say their firms have projects in two or more states (Figure 10, Number of States in Which Electrical Contracting Firms Performs Work), a significant tick upward from 33% in 2018. This shift could correspond to the move upward in firm size. Additionally, the numbers working in 3-plus, 4-plus and 5-plus states also all rose significantly, compared to 2018’s figures.

Wired on low-voltage

Low-voltage projects continue to be common engagements for this year’s respondents, with 96% of the entire sample saying their firm performs low-voltage work. However, these projects seem to be becoming more important to ECs’ bottom lines, with 22% now reporting their firms have a separate low-voltage division—twice the percentage reported in 2018. As was the case in 2018 and 2016, firms with 10 or more employees are more likely to have such a division than their smaller counterparts. And the growth in low-voltage divisions has been especially significant among this group, with 40% of firms reporting their adoption, up from 25% just two years ago.

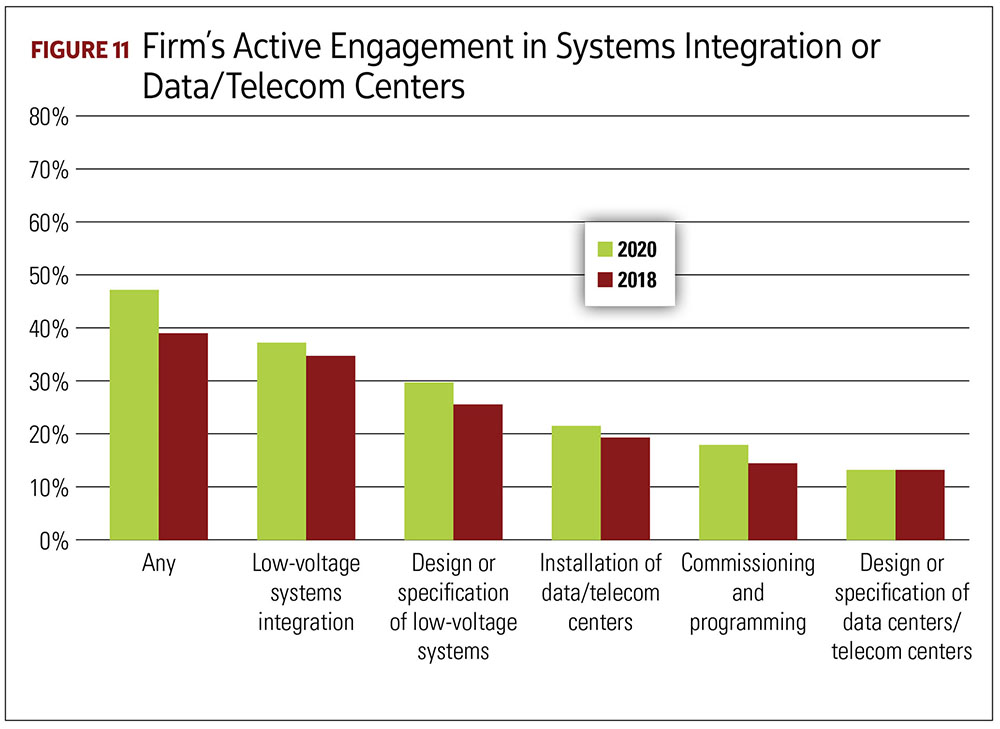

Of course, systems integration and data centers are two big opportunities for low-voltage business, and almost half of ECs are actively involved in either or both of these types of projects. While it might appear from Figure 11, Firm’s Active Engagement in Systems Integration or Data/Telecom Centers, that such projects have increased since 2018, those differences are not statistically significant. Low-voltage systems integration makes up the biggest part of this business, at 36%, followed by design or specification of low-voltage systems, at 30%. Other related project types include:

- Data/telecom centers installation, at 21%

- Commissioning and programming, at 18%

- Design or specification of data/telecom centers, at 13%

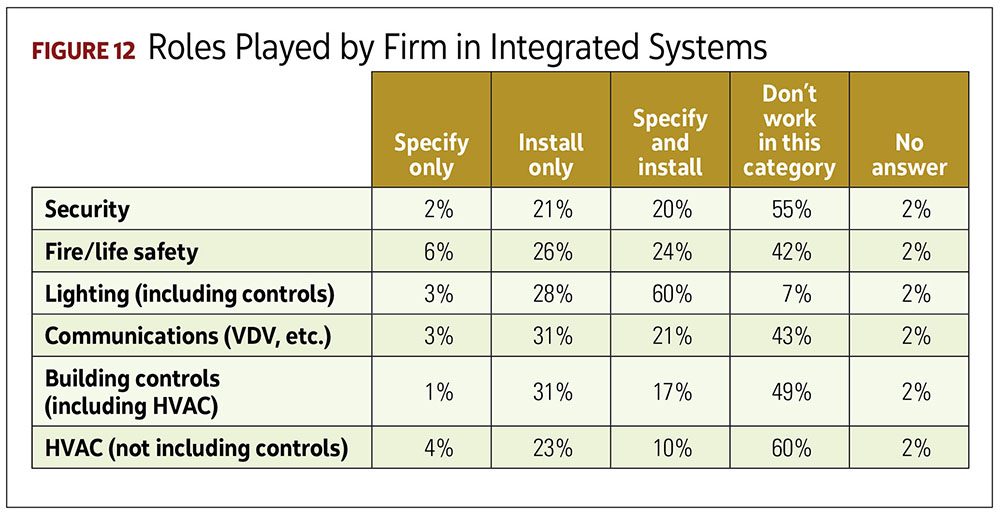

In integrated systems work, 60% of ECs say they both specify and install lighting systems, including controls, which isn’t surprising, given lighting’s overall prominence. As Figure 12, Roles Played by Firm in Integrated Systems, shows, about 20% to 25% specify and install other types of integrated systems, except for HVAC (not including controls), where the number falls to 10%.

Where’s the money?

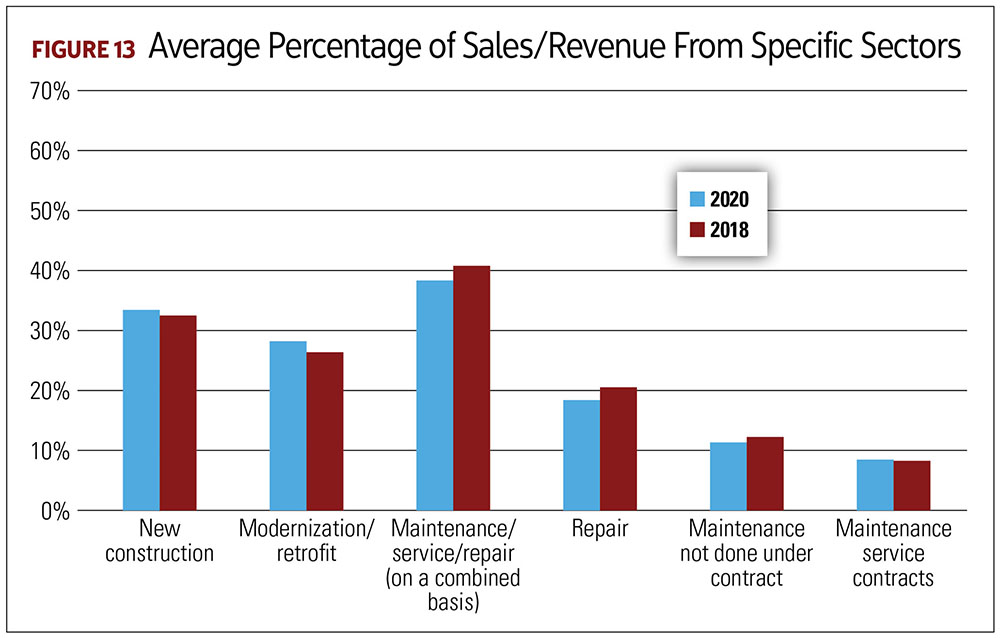

As Figure 13, Average Percentage of Sales/Revenue From Specific Sectors, shows, 39% of electrical contractors’ 2019 revenue on average came from maintenance/service or repair, which is a small, yet statistically significant drop from the average of 40.7% reported two years ago. New construction, as noted above, accounted for an average of 33% of revenue, statistically unchanged from two years ago. Third in importance, on average, is modernization and retrofit, which posted a slight, but statistically significant, bump up to an average of 28.2%, from 26.6% in 2018’s Profile.

This revenue order varies a bit when considered by firm size. New construction is more important for firms with more than 10 employees than it is to smaller firms. However, maintenance, service and repair, on a combined basis, accounted for a proportionally larger share of 2019 revenue for smaller firms. Maintenance service contracts, though, play a larger role for firms with more than 20 employees.

We found three new significant differences between firms of varying sizes, outlined in Figure 14, Average Percentage of Sales/Revenue From Specific Sectors by Company Size. On average, revenue from modernization and retrofit increased compared to two years ago, driven by increases among firms with 1–9 employees, while repair revenue declined. Maintenance/service/repair on a combined basis also decreased, driven by declines among firms with 1–9 employees. Although there wasn’t a significant change across the total, revenue from maintenance service contracts increased among firms with more than 10 employees.

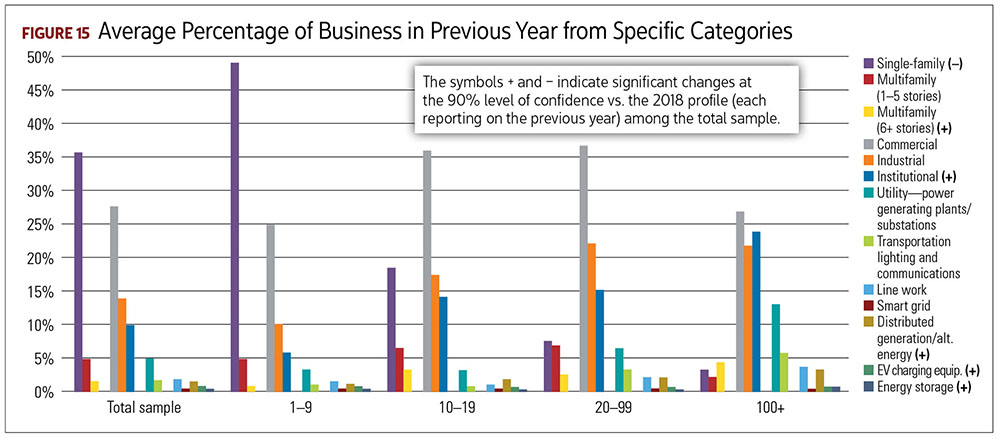

Looking at revenue by building category—residential, CII and nonbuilding (which includes transportation/lighting and utility)—CII continues to be ECs’ top revenue category, at 50.9%, on average. Residential projects come in at an average of 41.8%, a drop from 44.4% in 2018, while nonbuilding projects account for about 7% of EC revenue.

There were no statistically significant changes in average revenue derived from the broad CII and nonbuilding categories. However, average revenue from institutional work increased across the total sample, while revenue from single-family housing decreased across the total sample, and revenue from multifamily housing of six or more stories rose significantly.

Breaking these three major categories into their respective subcategories, we see the importance of single-family housing. CII, as a broad category might make up the greatest portion of EC revenue, on average, but single-family housing is the single largest revenue source, at 35.2% in this year’s profile. (See Figure 15, Average Percentage of Business in Previous Year from Specific Categories.)

These broad figures shift proportionally when they’re broken down by company size. For example, firms with 1–9 employees earned almost half their 2019 revenue from single-family projects. Also of note:

- EC firms with 10–99 employees earned the largest share of their revenue from commercial projects.

- Firms with 20 or more employees earned a disproportionate percentage from industrial work.

- Firms with 100 or more employees earned a disproportionate percentage from institutional and utility/nonbuilding work.

Continuing education

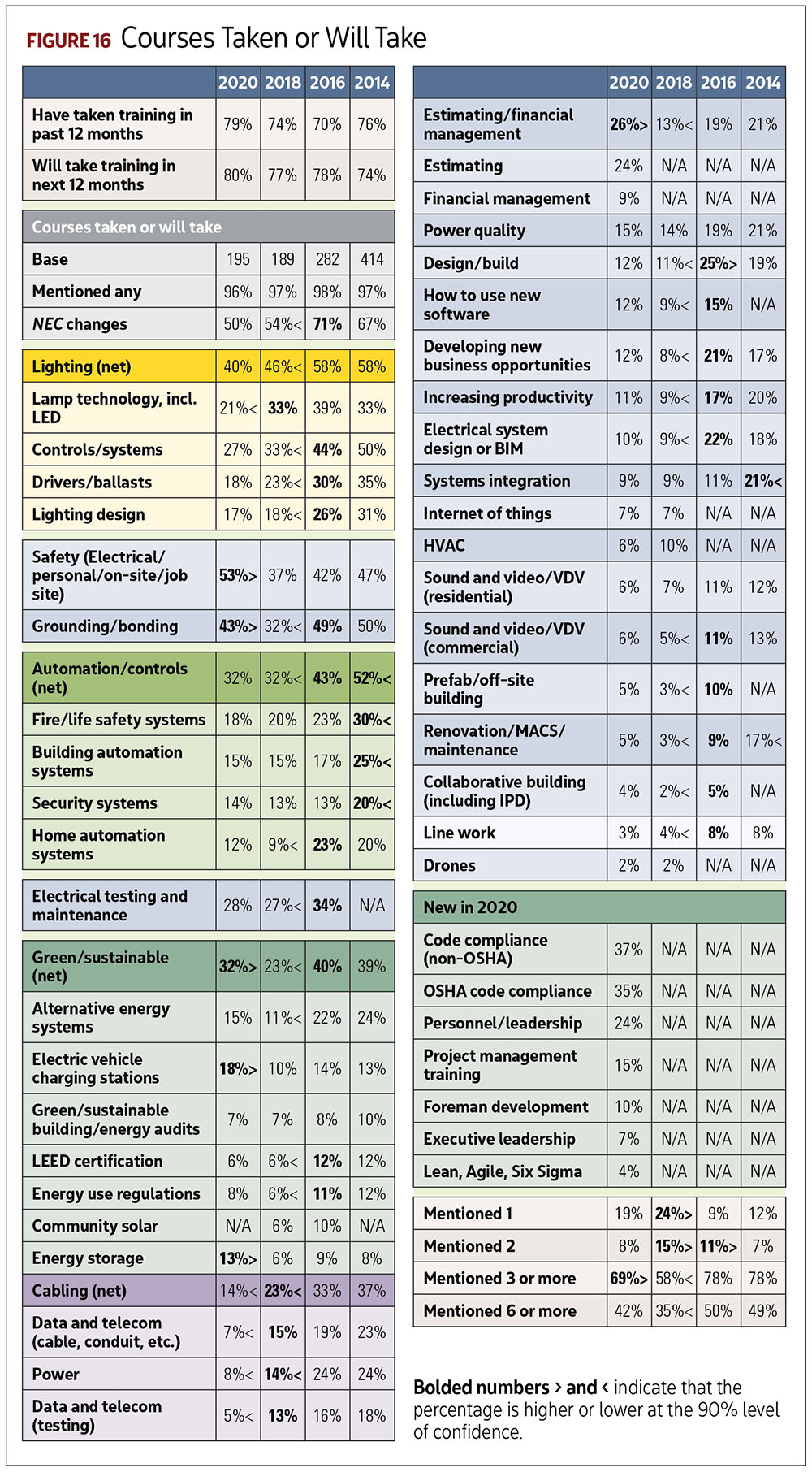

ECs remain interested in improving their skills and gaining new knowledge regarding emerging technologies, according to 2020 Profile responses. About 80% of ECs said they or someone in their firm has taken training in the past 12 months, or plan to do so in the next 12 months. These percentages are similar to those reported in 2018. However, as Figure 16, Courses Taken or Will Take, indicates, interest in a number of specific topic areas has increased since our last Profile, including:

- Safety tops the chart at 53%, up from 37%.

- Grounding/bonding: 43%, up from 32%

- Green/sustainable: 32%, up from 23% (notably, interest in EV charging stations is up to 18%, from 10%)

- Estimating/financial management: 26%, up from 13%

In 2018, we considered that the drop in training interest might have been due to a particularly busy work schedule. However, this explanation doesn’t ring true, given that the past year’s increase was paired with an even busier work environment. Now, we’re hypothesizing that this profile’s training boost could relate to areas ECs see as particularly promising, with new subjects to be mastered.

In 2018, we considered that the drop in training interest might have been due to a particularly busy work schedule. However, this explanation doesn’t ring true, given that the past year’s increase was paired with an even busier work environment. Now, we’re hypothesizing that this profile’s training boost could relate to areas ECs see as particularly promising, with new subjects to be mastered.

The payoff

In many ways, this year’s findings show a solidification of trends we saw in 2018. Notably, the top-tier importance of lighting to ECs’ work and revenue, the slow return of new construction from its prerecession highs, and the steady rise of solar, storage and EV charging equipment across all building sectors. There’s also no doubt the economic environment has shifted dramatically in 2020, from the 2019 trends we asked you about for this year’s survey. But we feel the resulting Profile provides a unique benchmark, for both near- and far-term comparisons.

Stay tuned

We couldn’t fit all we learned about electrical contractors and their work into a single article, so we have a second part planned for next month. It will dive deeper into the business side of operations, including project arrangements, such as design/build and more traditional bidding formats. We’ll also analyze the role electrical contractors play in specifying and substituting the products they install.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].