Twenty-five is the most significant number in the 2018 Profile of the Electrical Contractor research study findings. It means you’re wearing many more and different hats than ever before. In the 2004 study, traditional electrical power/distribution made up 69 percent of the EC’s revenue. Today, after decreasing over the subsequent 14 years, that number is only 25 percent, which indicates ECs are taking on a wide variety of disciplines and markets.

Almost 1,600 readers responded online and by mail to this year’s Profile of the Electrical Contractor survey, which covers work performed in 2017.

The previous Profile of the Electrical Contractor in 2016 demonstrated economic recovery had taken hold, and the good news is the construction economy has solidified further since then. Most firms report employment stayed steady or grew, and a majority of respondents report confidence in the economy’s growth over the next few years. Of course, the skilled labor shortage still looms.

As for the hands already on the front lines, standard wiring and maintenance jobs remain the bread and butter of electrical contractors’ business, but this year’s survey finds the growing importance of lighting to ECs’ bottom lines, perhaps a result of the rapid growth in LEDs and related control systems. In addition, as indicated in the 2016 Profile’s responses, firms are looking outside traditional electrical boundaries. For instance, a significant number of companies work on heating, ventilating and air conditioning (HVAC).

These are just the highest level findings. Dive into the details and see how ECs’ businesses are faring. Because there is just too much data to cover in a single article, we will continue the 2018 Profile next month.

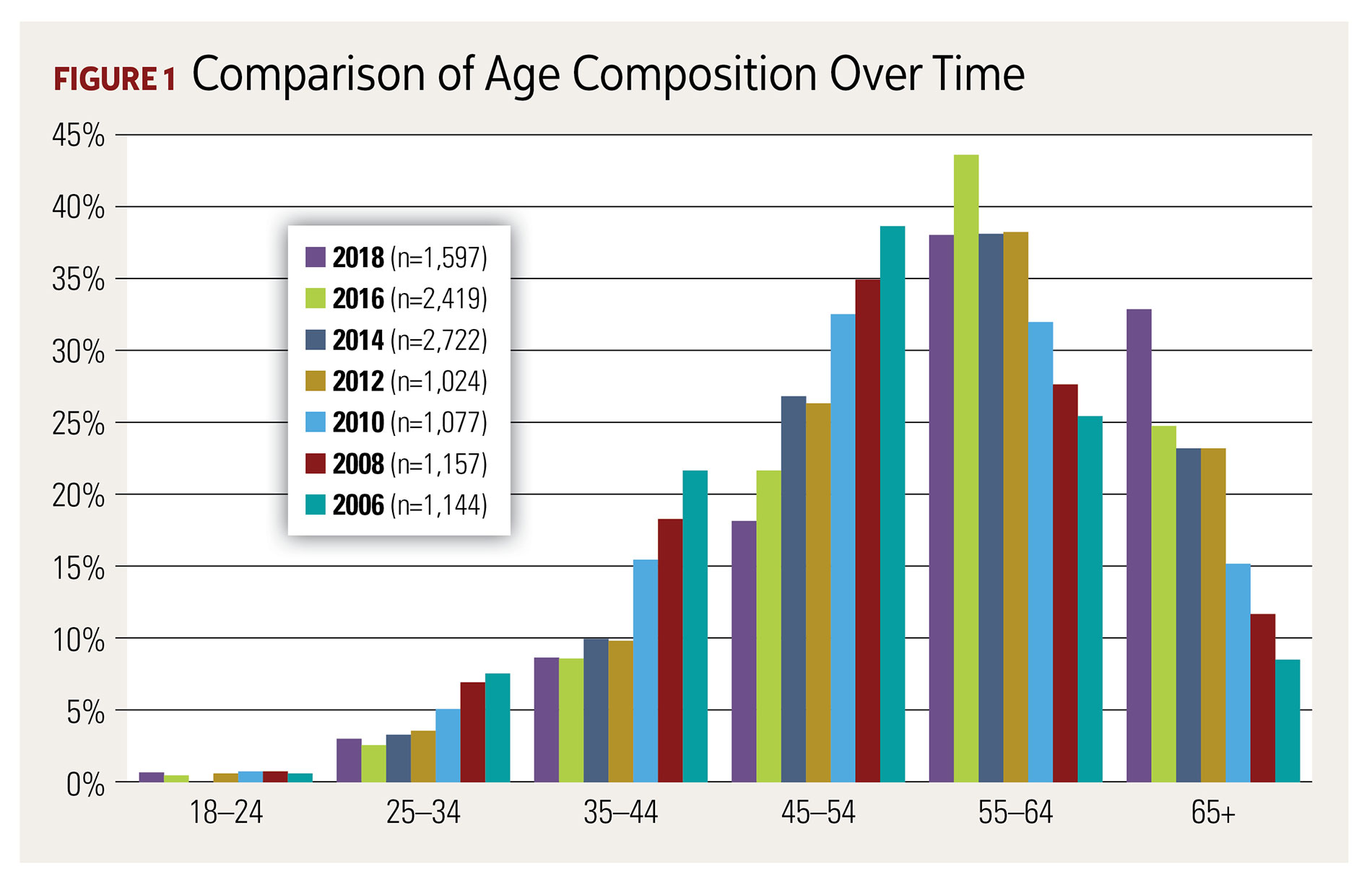

Average age still on the rise

Basic demographic information regarding individual contractors presents some the most significant statistics for the future of electrical contracting. Critically, as Figure 1 shows, the average age of electrical contractors continued to rise to 58.2, which is up from 57.3 in the 2016 study. Wrapped up in this average (not shown) are two even more noteworthy statistics: 69 percent of respondents are over the age of 55, and the 65-plus age bracket has jumped 8 percentage points in just two years and now totals 32 percent of respondents, versus 24 percent in 2016.

The aging of the electrical contracting labor force is not news. We have noted the trend for more than a decade. The average reported age in our 2008 Profile was 51.2, and that figure has steadily risen across firms of all sizes. Another constant over this decade is the relationship between firm size and respondent age. This year, respondents working for firms with 1–4 employees were an average of 60.6 years old (a jump from 58.7 in 2016), while respondents working for firms with 10 or more employees have an average age of 53.8.

In a new question this year, we asked how long respondents had worked in the electrical contracting field, and we learned ECs are a very experienced bunch with an average of 32.6 years in the field. An impressive 5 percent of respondents have been in the field more than 50 years. This exceptional tenure is more likely to be found in firms with 5–9 employees.

With age comes responsibility, apparently, as 77 percent of the study’s respondents are company owners and top management, and only 10 percent have the title of master electrician or its equivalent. This is consistent with 2016’s responses, as is an interesting geographical variation: Western ECs are more likely to describe their responsibility as “owner/top management” (82 percent, compared to 77 percent of the total), and less likely to fall into the category of “master electrician or equivalent” (5 percent, versus 10 percent of the total).

Size of firms remain steady

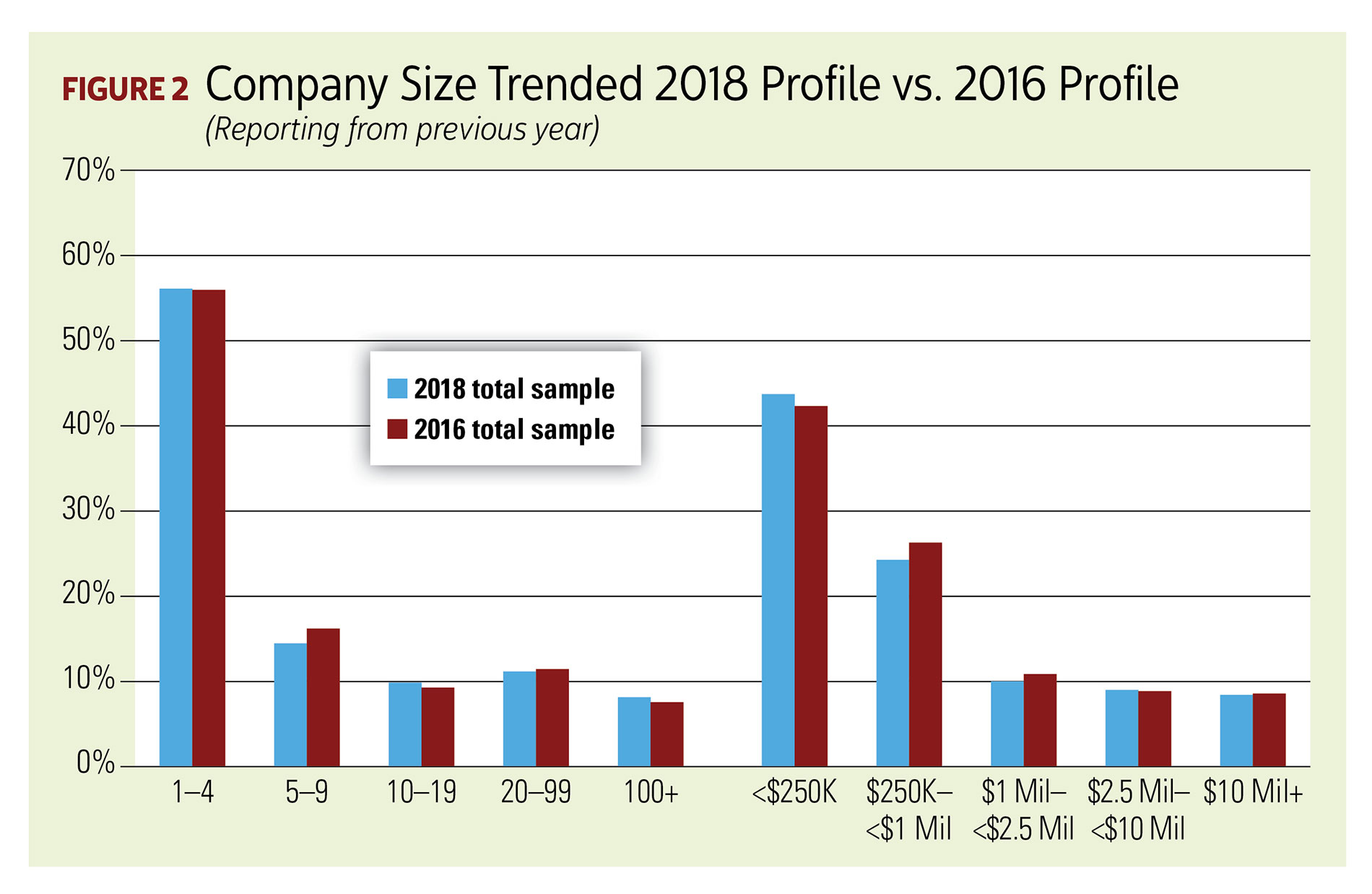

What about the firm size? ECs are primarily smaller companies. Of all respondents, 71 percent work for organizations with 1–9 employees, and 68 percent work for firms with annual revenues of less than $1 million. These figures are statistically unchanged compared to our 2016 survey. At 43 percent, the largest single income segment consists of firms with revenues under $250,000. As Figure 2 illustrates, the decline in the percentage of smaller firms seen between the 2014 and 2016 studies has not continued.

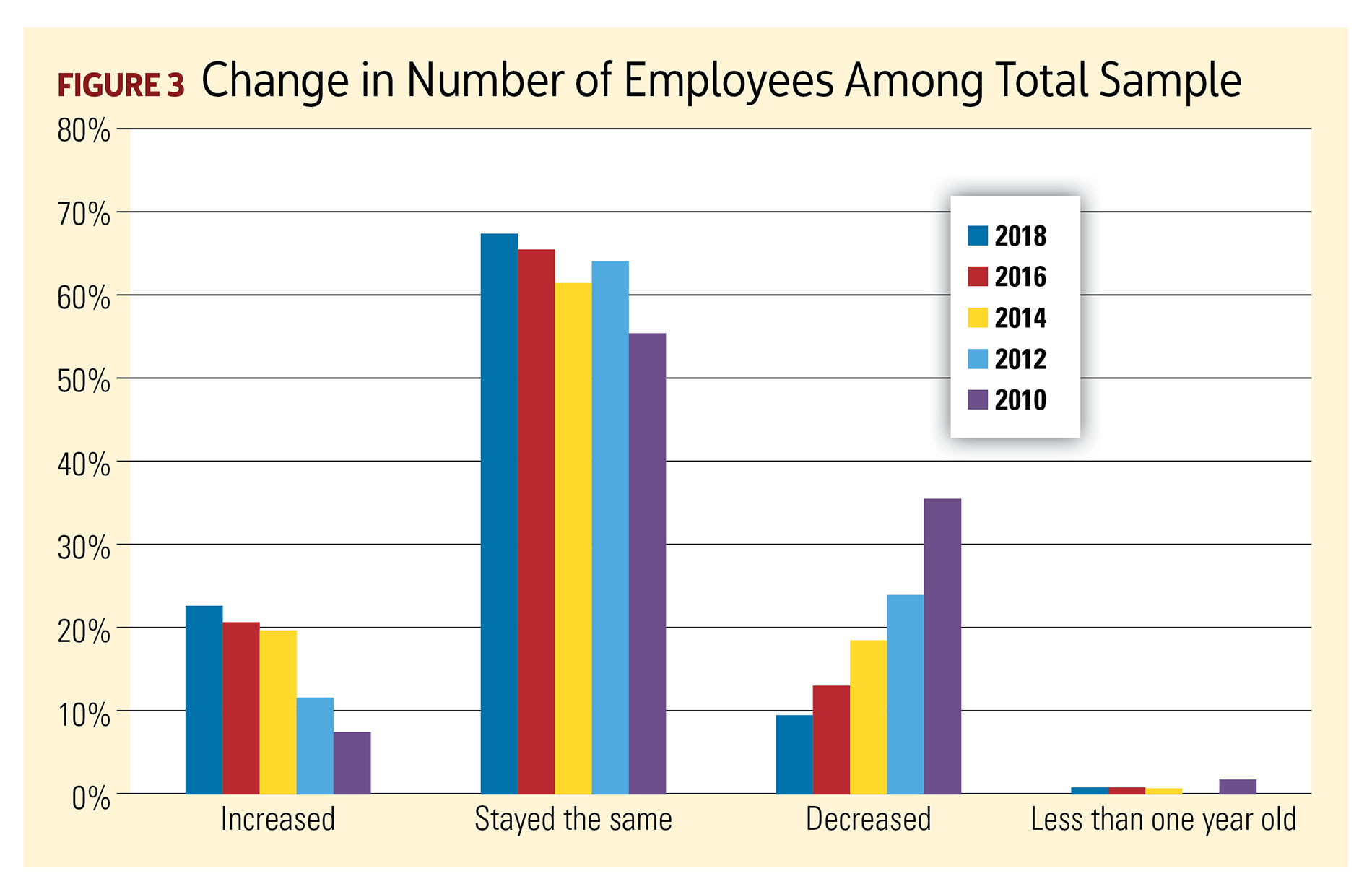

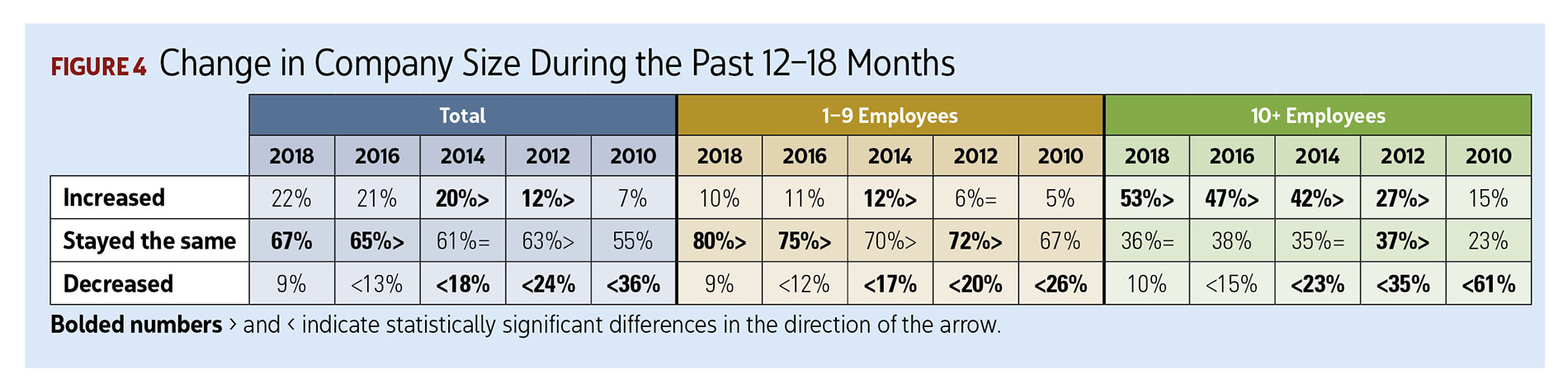

In terms of employee rosters, two-thirds of respondents said their company had stayed the same size in the last 12–18 months, represented in Figures 3 and 4. However, of the remainder, the percentage of companies that added employees (22 percent) is more than twice the percentage of those that lost employees (9 percent). As a further indicator of economic health, that latter figure represents a statistically significant drop from 2016, when 13 percent of firms had lost employees, and an even bigger difference from 2014, when 18 percent had lost staff.

The shifts in employee counts become more distinct as company size increases. Figure 4 shows the largest firms are responsible for the biggest share. Over the last 12–18 months, 22 percent of all companies report more employees; however, while 10 percent of firms with 1–9 employees added staff during that period, 53 percent of firms with 10 or more employees report an increase in staff size. This number represents a significant increase over the 47 percent figure reported by those companies in 2016.

Illustrating how far we’ve come since the last downturn, 36 percent of all firms in 2010 (and a whopping 61 percent of those with 10 or more employees) reported staff reductions.

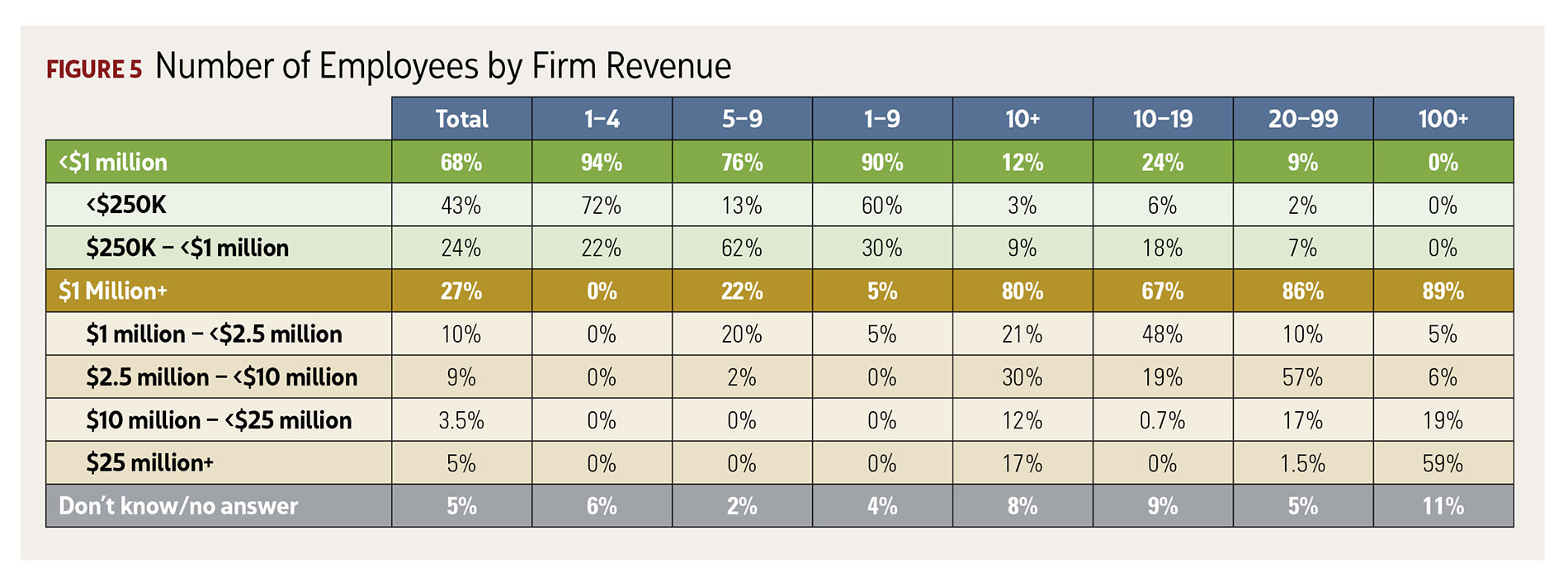

Income distribution, by firm size, remains unchanged in the 2018 survey, compared to 2016’s results. However, Figure 5 breaks those revenues down by company size and illustrates the breadth of today’s electrical contracting industry. Of those working for the smallest firms (1–4 employees), 72 percent reported annual company revenues of less than $250,000, while 59 percent of those at firms with 100 or more on staff reported company revenues at $25 million-plus.

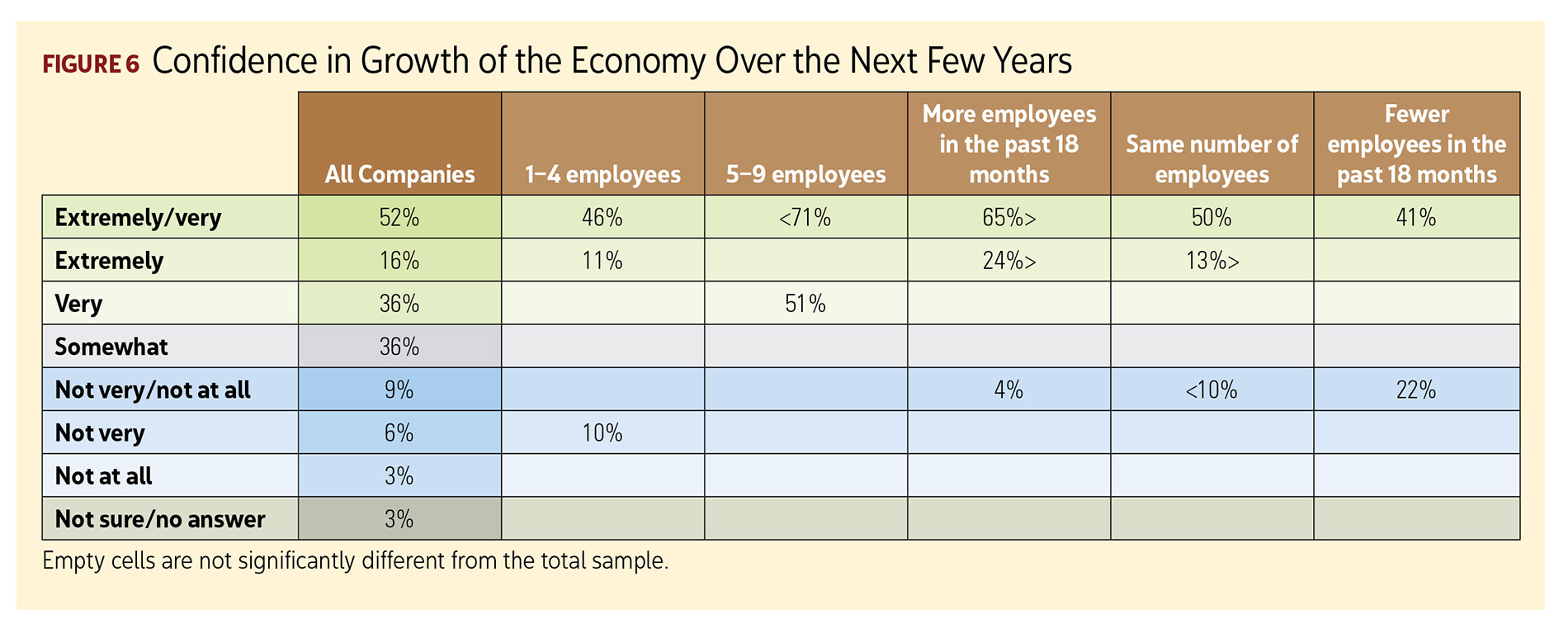

While these earnings figures remained virtually flat compared to the 2016 study, ECs are confident the larger economy will continue to grow over the next few years. This positive outlook, which Figure 6 details, is especially high among respondents working for companies with 5–9 employees. In this group, 71 percent of respondents are “extremely/very confident.” Of respondents whose companies have added staff, 65 percent report a similar outlook. Overall, 52 percent are in the “extremely/very confident” category. Additionally, 36 percent of respondents reported being “somewhat” confident in continued growth. That makes a total of 88 percent with a positive outlook.

Markets and sources of revenue

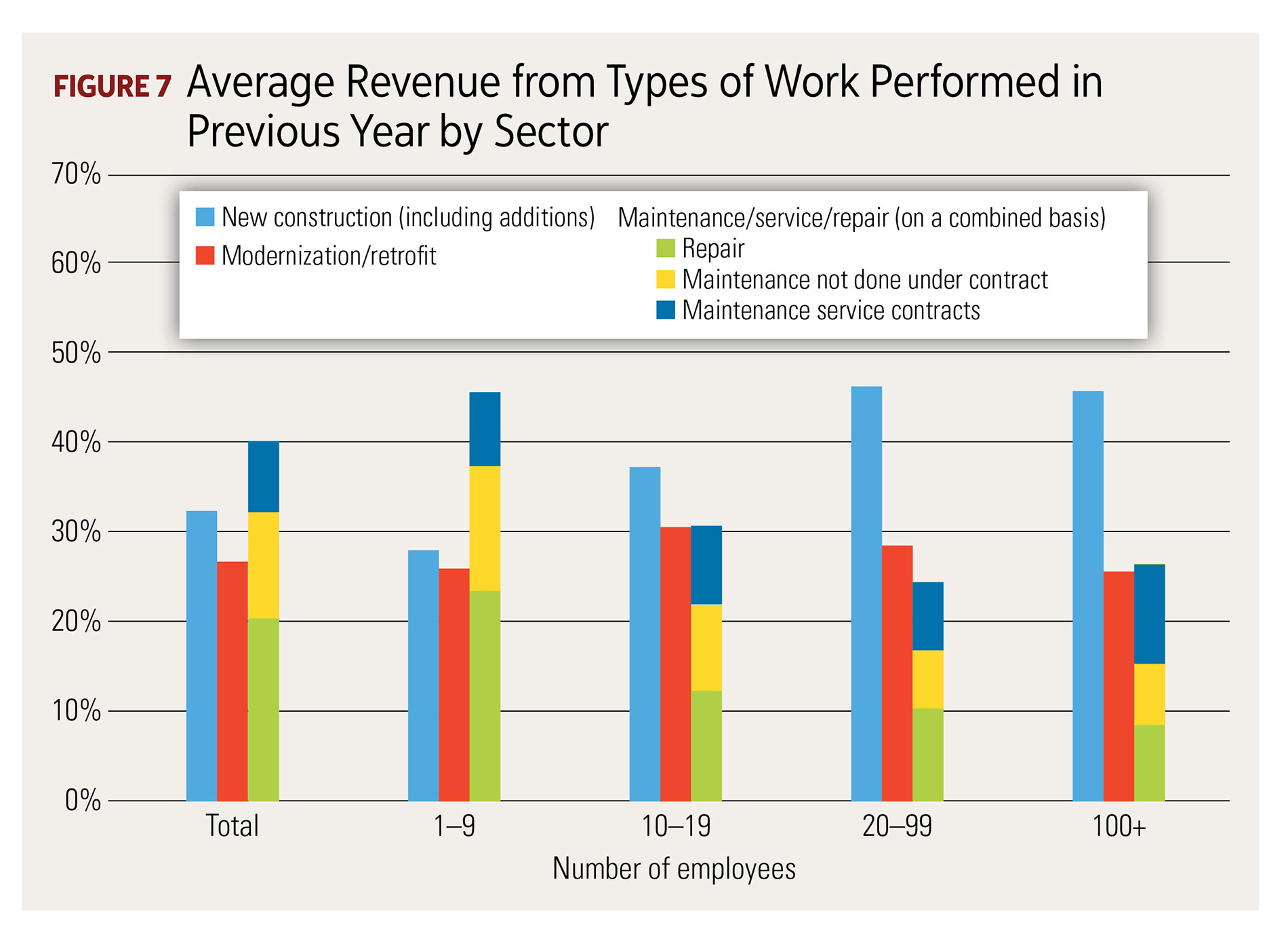

Confidence in continued economic growth may be high, but survey respondents still haven’t seen new construction return to its prerecession highs. In this study, only 33 percent of their firms’ revenues, on average, came from new construction. This is down from 43 percent in the 2008 Profile. As firm size grows, however, new construction becomes more important, pushing toward 40 percent for firms with 10–19 employees and close to 50 percent for companies with 20 employees or more. Figure 7 shows the biggest revenue line for smaller firms remains maintenance, service and repair on a combined basis.

An interesting piece of business growth for firms with 1–9 employees over the past two years has been work performed under maintenance/service contracts. This work now makes up 8.3 percent of smaller firms’ revenues, compared with 6.5 percent reported in 2016.

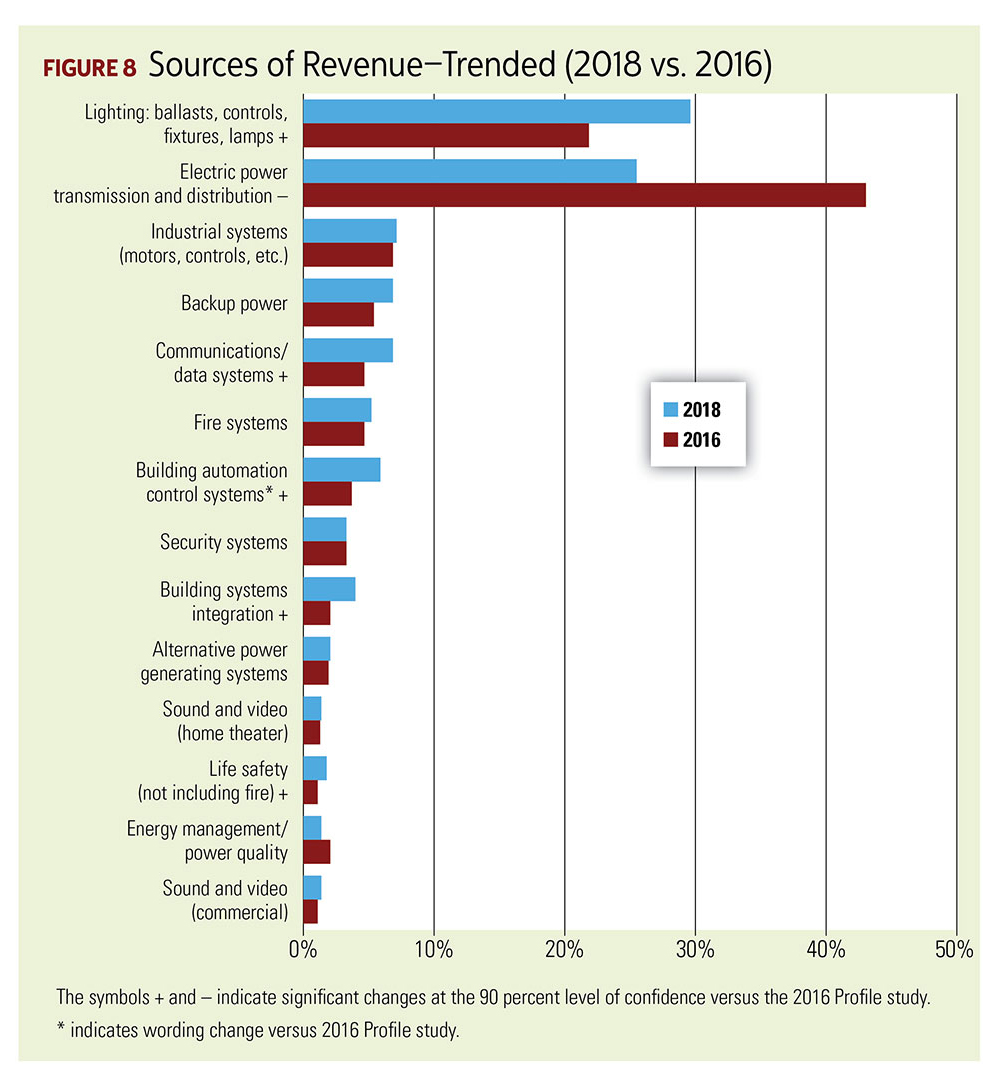

The proportion of company revenue contributed by various types of electrical work has shifted dramatically. As Figure 8 shows, electric power transmission and distribution is no longer the most important money-earning category for electrical contracting firms. In terms of related revenue, it dropped from 43 percent in 2016 to 25.4 percent. Looking back to the 2004 Profile, it was 69 percent. The nearly 18-point difference in the last two years has spread across several other categories, and lighting grabbed the top spot, accounting for almost 30 percent of revenue, which is an 8-point climb for the category.

Other categories showing growth include communications/data systems, building automation and control systems, and building systems integration. Each of these areas ticked up 2 percentage points over 2016’s results. Life safety also posted a small but significant increase.

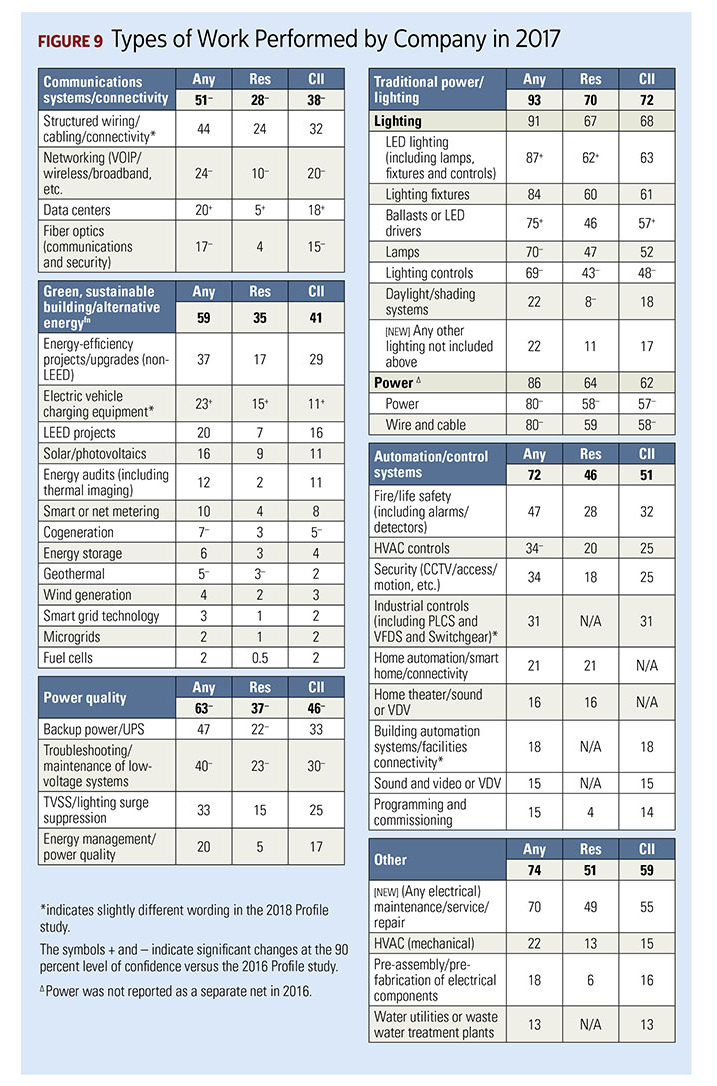

Getting into more specific types of work performed in the previous year, we queried ECs on a list of up to 42 different kinds of projects they had worked on in both residential and commercial/institutional/industrial (CII) settings. Figure 9 shows, across both residential and CII, 93 percent of firms worked on traditional power and lighting; however, again illustrating lighting’s increased importance, that combined category can be broken down into 91 percent working on lighting and 86 percent working on traditional power.

When looking beyond these top-tier categories, we see continuing evidence of ECs stretching into new territory. Across residential and CII assignments, almost three-quarters of respondents worked on various “Other” aspects, which include pre-assembly/prefabrication of electrical components, HVAC mechanical, water utilities/waste water treatment plants and electrical maintenance/service/repair. Furthermore, 72 percent of the study’s respondents work on some aspect of automation and controls, including 51 percent in CII settings and, underscoring how smart our homes are becoming, 46 percent in residential projects.

While some of the more sophisticated types of work (e.g., structured wiring) are more prevalent in CII settings, some green building categories, such as energy storage and geothermal, are relatively evenly distributed across CII and residential projects.

Across the totality of the work in residential and CII projects, there are some interesting changes from the 2016 results:

- LED lighting and ballasts/LED drivers posted significant increases, while lamps and lighting controls declined. One possible explanation is LED technology has become the standard option for new and replacement lighting installations, so a greater percentage of all lighting work may be reported in the LED categories.

- In the case of automation/control systems, HVAC controls declined.

- In the sustainability categories, EV charging increased, while cogeneration and geothermal posted small but significant declines.

- Under communications systems/connectivity, data centers increased, while fewer ECs reported working on fiber optics or networking. In fact, of all the project types we covered, networking showed the steepest decline compared with 2016’s results, dropping to 24 percent from 35 percent two years ago. Under power quality, troubleshooting/maintenance of low-voltage systems declined. In the traditional power/lighting section, power, and wire and cable also declined. This all may indicate ECs are getting better at following market trends.

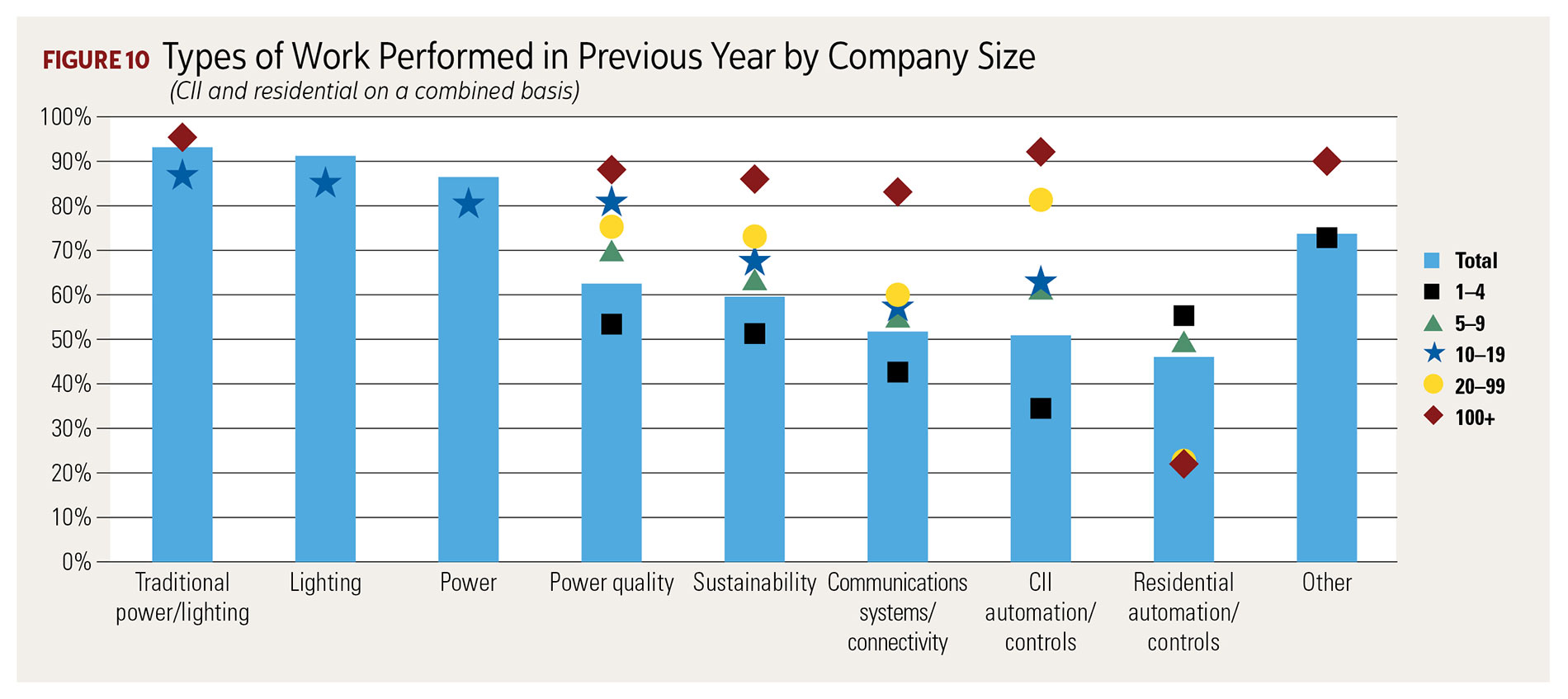

Analyzing the types of work performed by company size, Figure 10 reveals a finding seen in our previous two surveys has continued: when it comes to the range of work, firms with 5–9 employees look more like larger firms than firms with 1–4 employees. For example, they are more likely than smaller firms to work in a number of categories, including power quality, sustainability and communication systems/connectivity.

However, for residential contractors, this year’s survey finds the smallest firms are getting into a broader range of project types. In these settings, firms with 1–4 employees are much more like companies with 5–9 employees. There are two exceptions, however. The larger companies are more likely to work on geothermal and cogeneration projects, and the smallest companies are more likely to work on HVAC mechanical and electrical maintenance, service and repair projects.

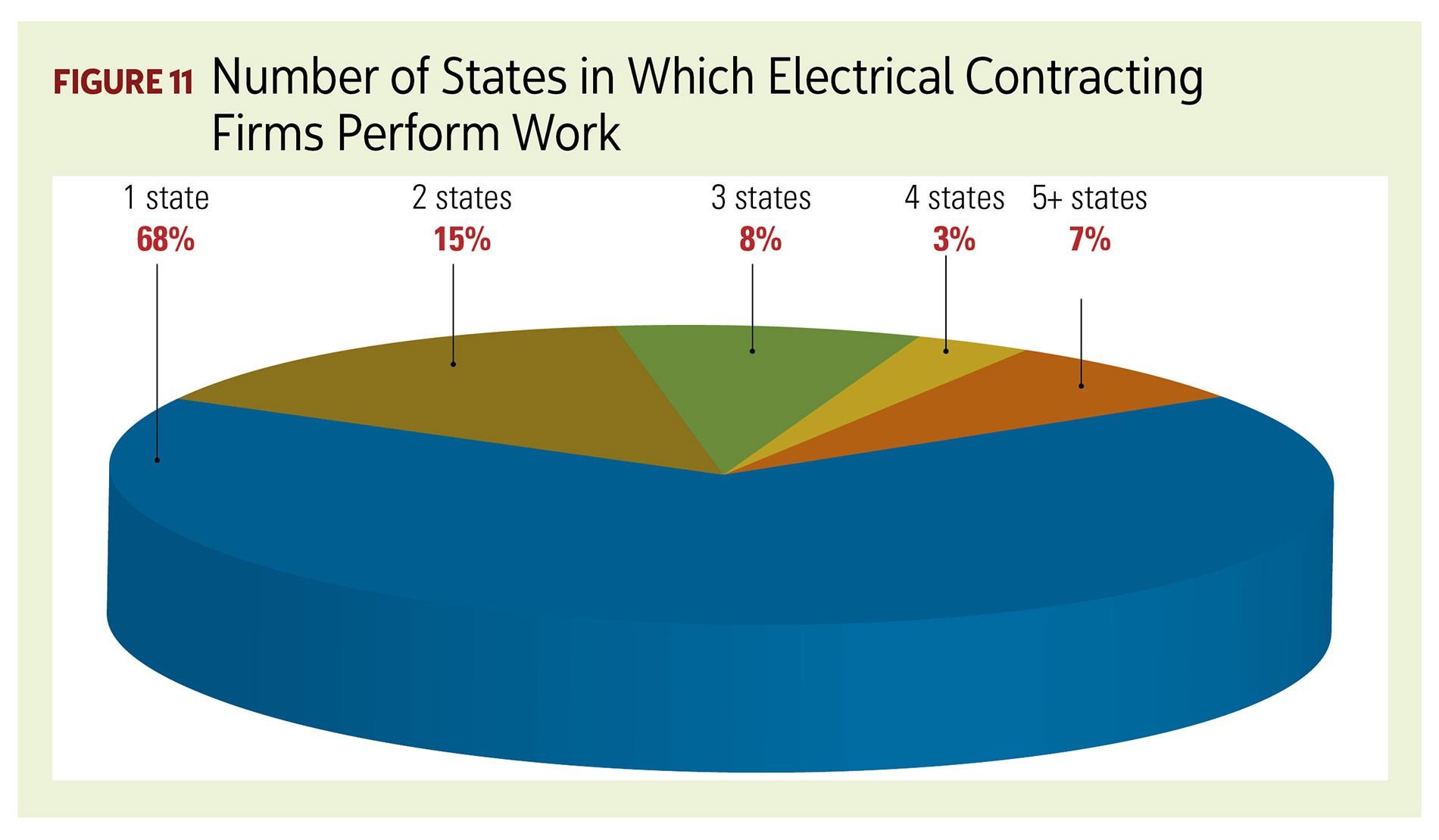

Along with what types of work ECs are doing, survey respondents also were asked where they do it. About one-third of firms perform work in multiple states, as Figure 11 shows. As noted in the past, this suggests there may be licensing and certification issues. The proportion of firms working in two or more states is unchanged over the past three profile studies. Not surprisingly, 55 percent of firms with 10-plus employees are working in multiple states, compared with less than 35 percent of ECs with 1—9 employees.

High involvement in low-voltage

Low-voltage work is still exceedingly common across companies of all sizes. A vast majority (95 percent) of respondents reported their firms performed low-voltage work. As in our 2016 Profile, 10 percent of firms reported having a separate low-voltage division, and as was true in the previous two Profile studies, firms with 10 or more employees are more likely than their smaller counterparts to have separate low-voltage divisions. Larger companies also are more likely to be planning to add one (8 percent, versus 5 percent for the total sample).

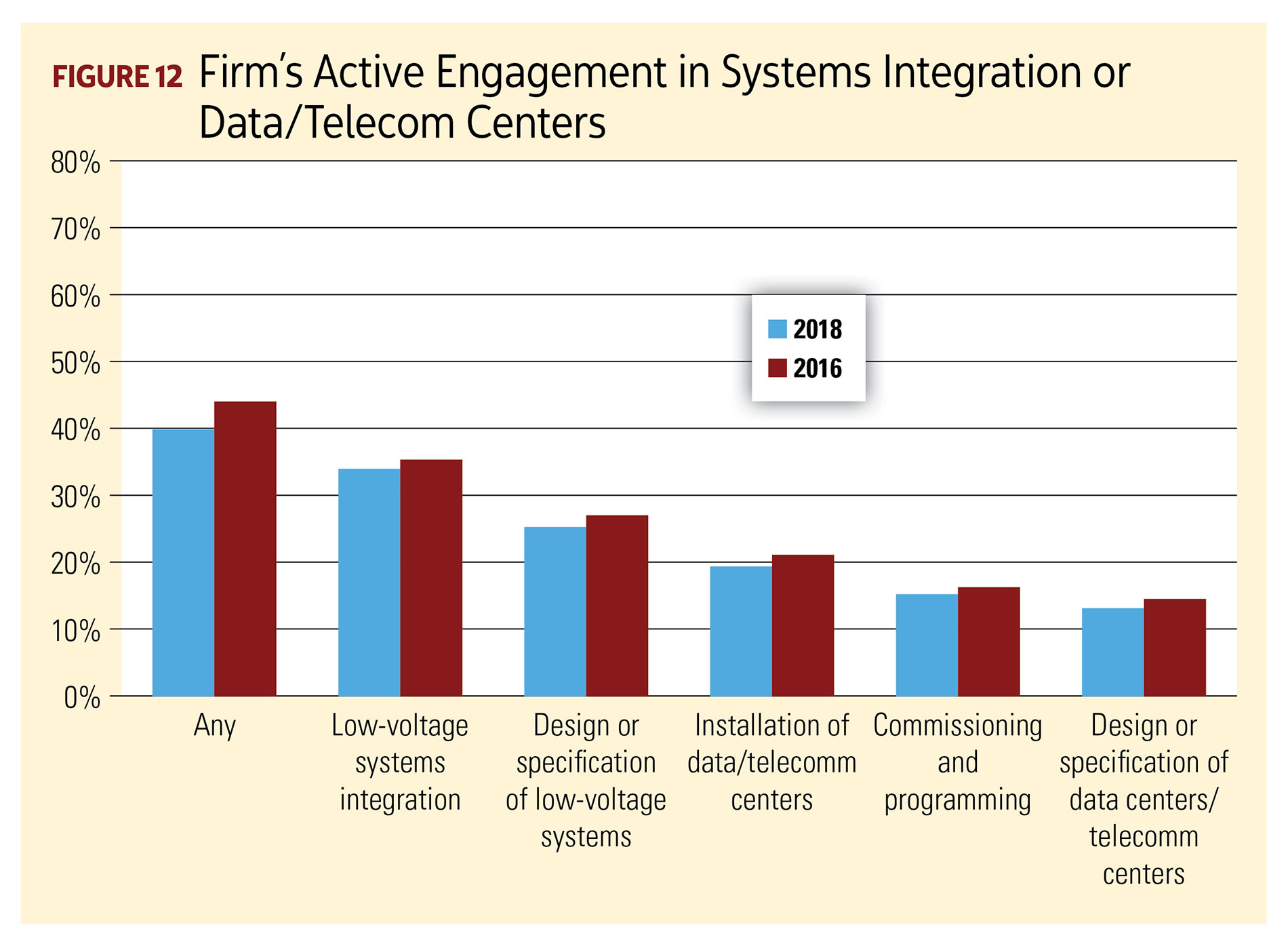

However, while Figure 12 appears to show a slight decline in integration work from two years ago, none of the differences are statistically significant. In this study, about 40 percent of firms reported working in these areas. Also, 34 percent of firms reported participation in low-voltage systems integration, but it is the most frequent project type cited in this category, followed by low-voltage systems design or specification, at 25 percent. Additional data points include the following:

- Almost 20 percent of firms said they installed data or telecom centers in 2017.

- 15 percent of firms performed commissioning and programming.

- 14 percent were involved in data center design or specification.

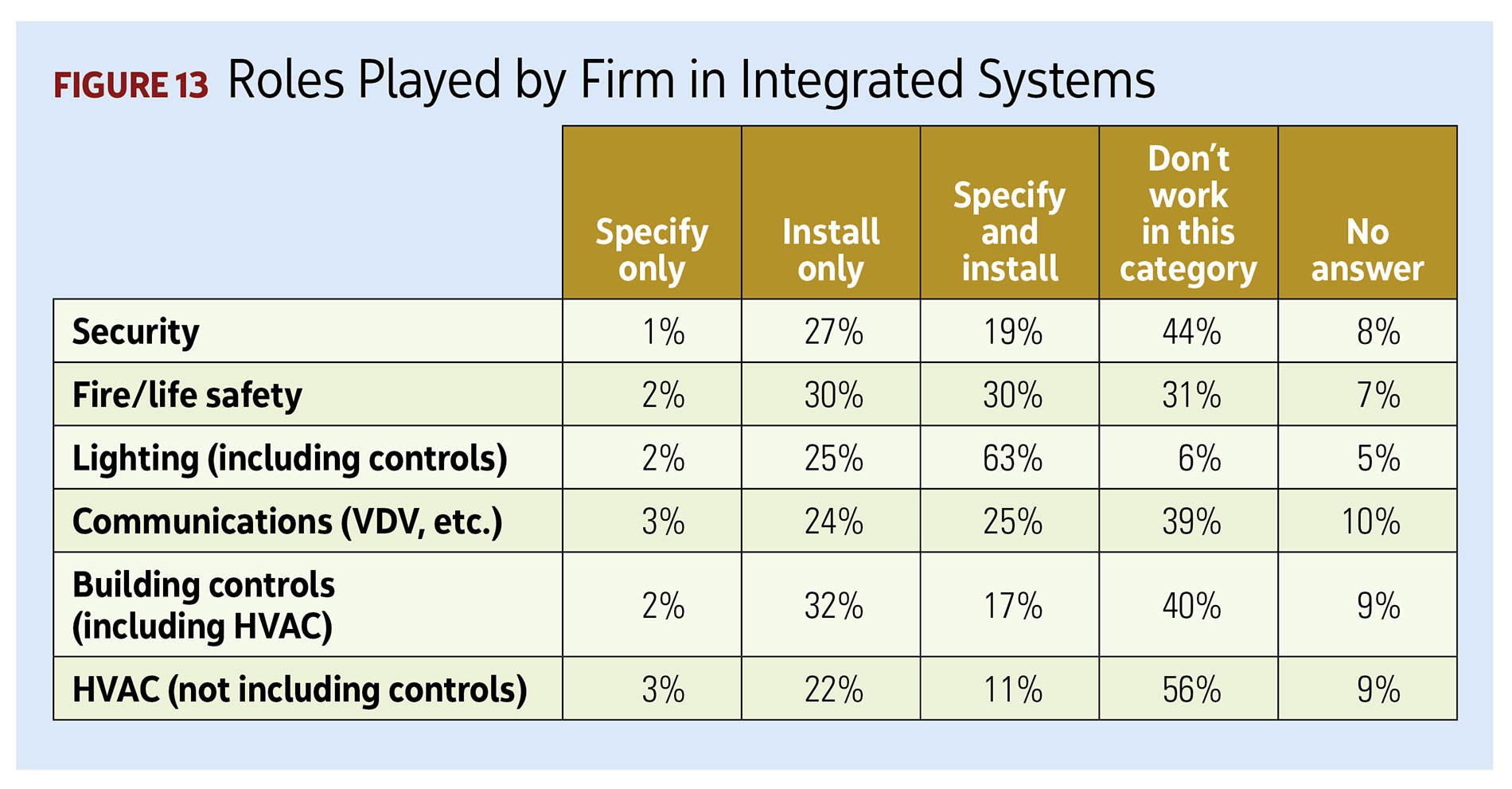

For integrated systems, it’s not surprising that lighting is the most prominent category for ECs with 63 percent reporting they both specify and install lighting systems (see Figure 13). This is more than twice the number that only install such equipment.

Slicing up the revenue pie

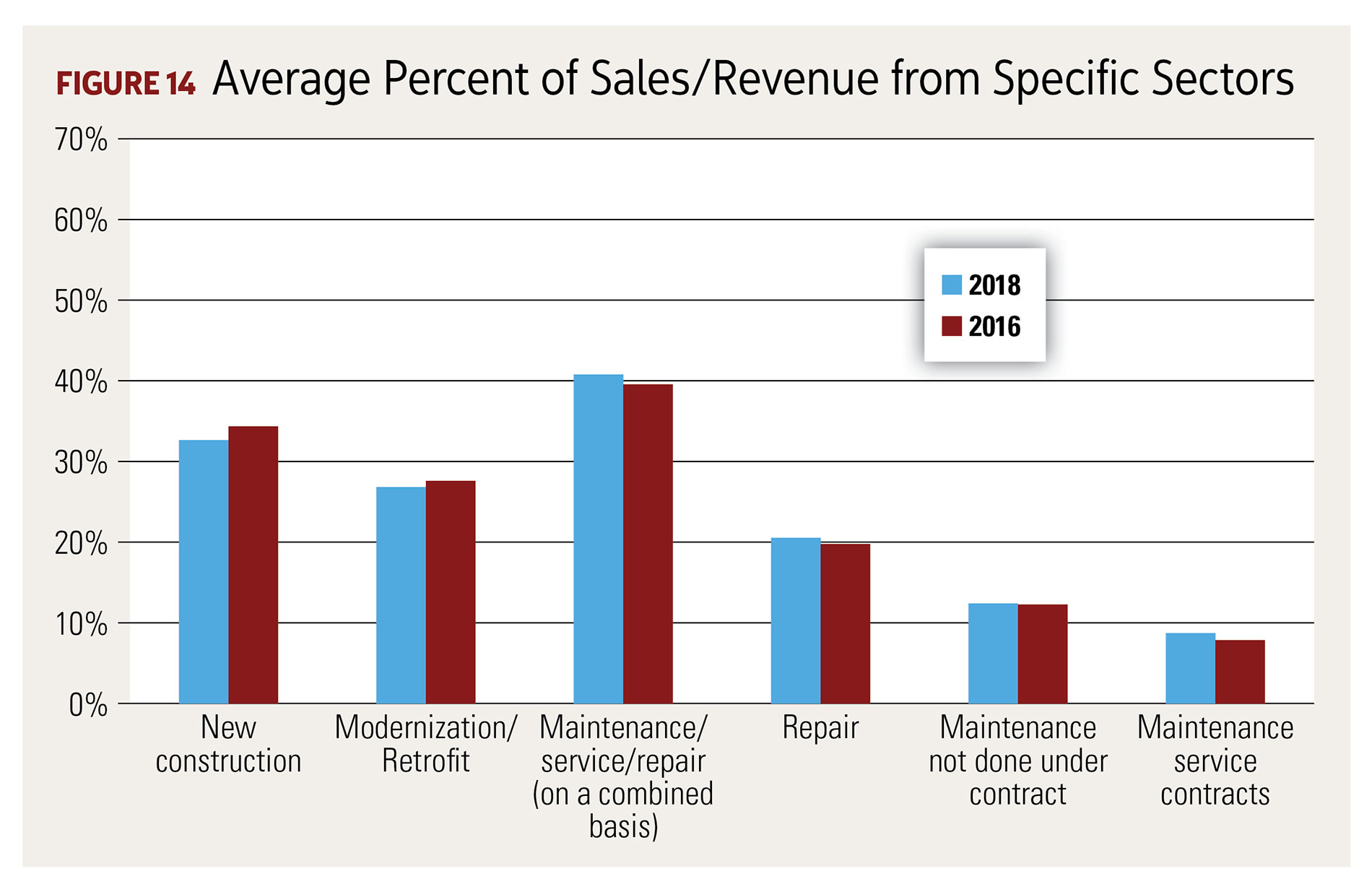

As noted above, while 2016’s survey showed an uptick in the role of new construction in electrical contractors’ revenue, that figure remained the same at 33 percent. Also statistically unchanged is the 41 percent of revenue from maintenance/service or repair. The remaining 27 percent comes from modernization/retrofit projects (Figure 14). New construction plays a proportionally larger role for firms with 10-plus employees, while the combination of maintenance, service and repair is significantly more important to the bottom lines of smaller companies. The only significant difference from 2016 is the increasing role of maintenance service contracts in the work of companies with 1–9 employees. Though still relatively small, these contracts now generate 8.3 percent of revenue for these companies, versus 6.5 percent two years ago.

The biggest change in revenue sources across the total sample is lighting’s move into the top money-making spot, climbing to an average of almost 30 percent of company revenue, which is up from 21 percent in 2016. Taking an equally significant hit, electric power transmission and distribution (previously titled “electrical/power distribution”) dropped to 25.4 percent, down from 43 percent two years ago, continuing a trend that began in 2004.

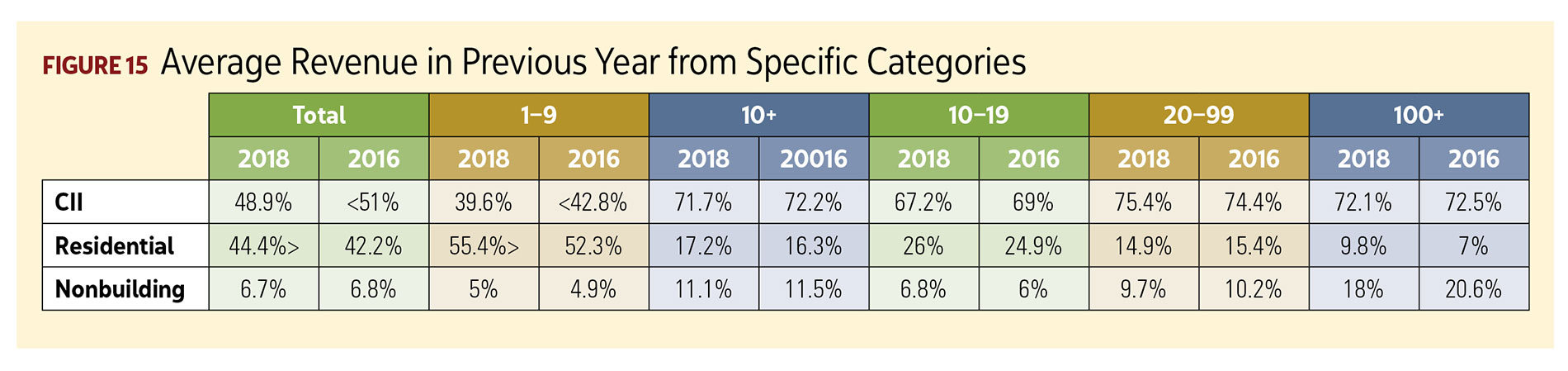

Looking at revenue derived from each of the three major building categories—residential, CII and nonbuilding, including transportation/lighting and utility—CII continues to contribute most to contractors’ bottom lines at 49 percent.

However, as Figure 15 details, this is a drop from the 51 percent reported two years ago, while residential projects’ share rose to 44 percent, from 42 percent in 2016. This change may be due to the residential market finally rebounding.

Interestingly, these 2-point shifts averaged across the total sample were largely driven by more significant movement in companies with 1–9 employees. In those firms, CII’s share dropped to 39.6 percent, from 42.8 percent in 2016, while residential rose to 55.4 percent, from 2016’s 52.3 percent.

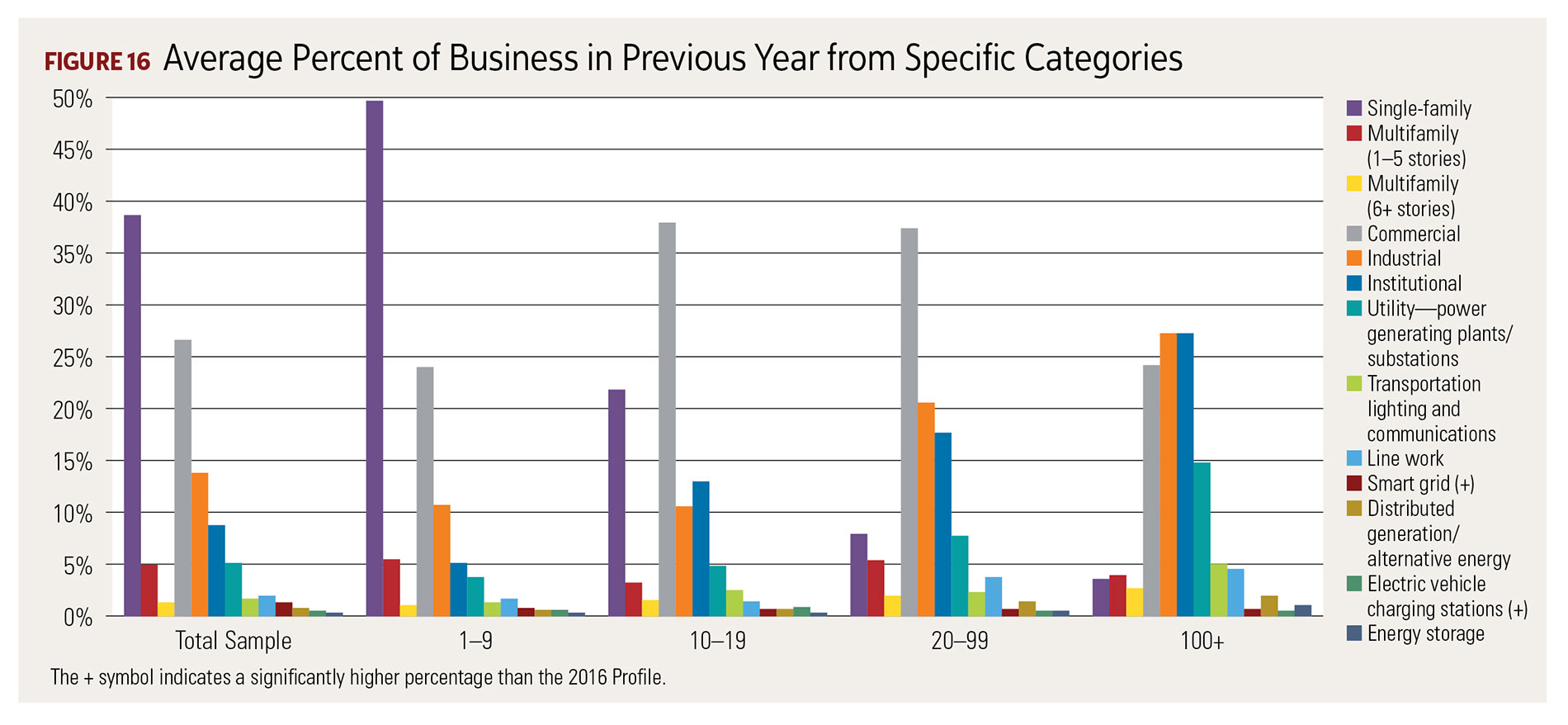

When the residential and CII categories are broken into their respective subsets, single-family homes are the largest single source of revenue at 38.4 percent (see Figure 16). Also, within the broad CII category, commercial construction is the top money maker at 26.7 percent of revenue, versus 13.6 percent for industrial projects and 8.6 percent for institutional work.

Unsurprisingly, though, revenue shares shift when we study them by company size. Firms with 1–9 employees earn almost half their revenue from single-family projects, while commercial projects take the lead for those with 10–99 employees. The largest firms with 100-plus employees get a disproportionate share of revenue from industrial and institutional projects and utility/nonbuilding work.

Green building and EV charging

We also looked into how many ECs had worked on green/sustainable building and renewableenergy projects in 2017. Across the sample, a substantial 59 percent of respondents reported participating in such efforts. Non-LEED-related efficiency projects and upgrades topped the list, with 37 percent reporting working on these jobs. As with almost all the project types in this category, it was more common in CII settings (at 29 percent) than residential (at 17 percent).

There was one notable exception, where sustainability-related work was more prevalent for residential customers than CII clients. More contractors reported installing EV charging equipment in residential settings (15 percent) than CII environments (11 percent), perhaps a sign that more homeowners are leaving fossil fuels behind.

Training priorities

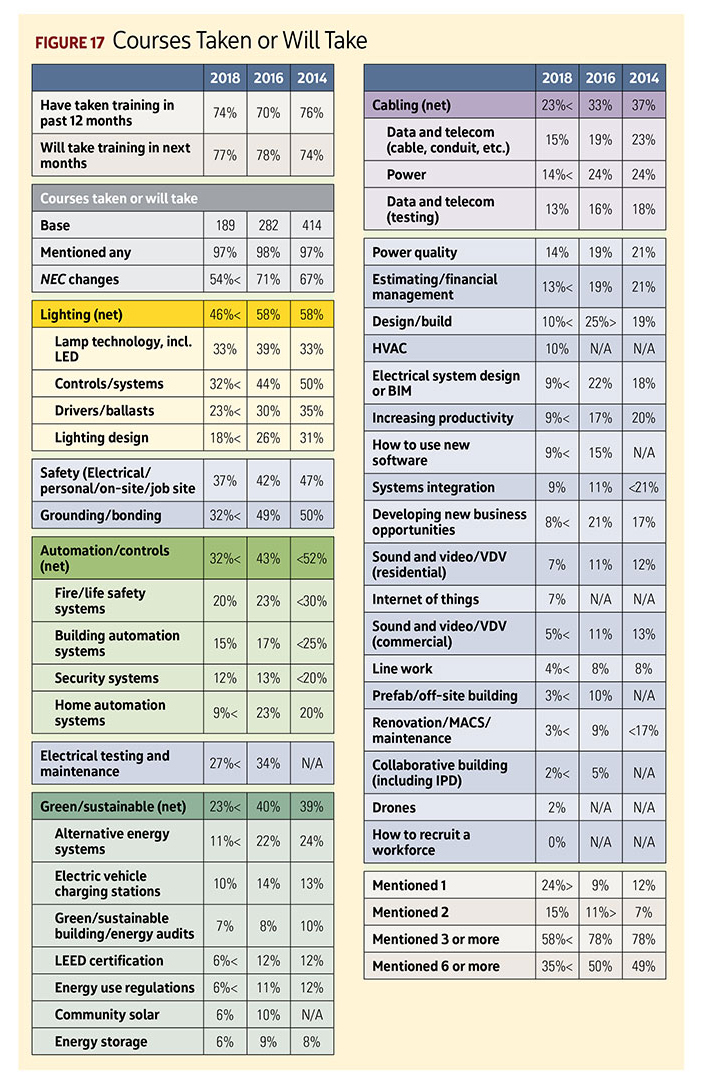

With numerous new technologies rising in importance and electrical codes updating every three years, electrical contracting is certainly an evolving field. To keep up with all of the changes, more than seven in 10 ECs say they or someone in their firm has taken a training course in the past 12 months or plans to do so in the next 12 months. This level of interest remains the same as reported in 2016.

However, when queried about specific topics of courses they have taken or will take, interest in specific courses has declined since our last survey, which, as Figure 17 shows, is a continuing trend. For example, National Electrical Code (NEC) changes, though still the biggest draw for contractor training, dropped to 54 percent from 71 percent in spite of the fact 2017 was an update year.

Other notable training topics and the change in their level of interest include the following:

- Lighting: including lamp technology, controls, drivers and ballasts and lighting design—46 percent, down from 58 percent

- Safety: 37 percent (It climbed into third place, above grounding and bonding, since 2016)

- Grounding/bonding: 32 percent, down from 49 percent

- Automation/controls: 32 percent, down from 43 percent

- Electrical testing and maintenance: 27 percent, down from 34 percent

- Green/sustainable: 23 percent, down from 40 percent

It is possible that ECs have less time available for formal training because they are busier with paid work. Or, they might be focusing more in-depth on fewer single subjects.

The bottom line

One thing is clear based on this year’s findings: the most successful ECs today wear many hats. It is a trend ECs have increasingly faced for the past couple of decades, but now, with traditional electrical power/distribution declining from 69 percent in the 2004 study to 25 percent of the EC’s revenue, the trend is a reality for many contractors.

Overall, things are looking good and prosperous. ECs are confident in the economy and future growth. The majority of larger contractors are increasing their workforce, and small contractors are holding their numbers. However, a continually rising average age and a skilled labor shortage loom as stymieing factors. Furthermore, survey respondents still haven’t seen new construction return to its prerecession highs. Residential reclaimed some of its market share, suggesting housing has finally made a comeback. In the split between CII and residential work, the market divide between the smallest and biggest ECs is still very much alive.

Across the spectrum, lighting supplanted electric power transmission and distribution as the greatest revenue earner. Though mileage may vary by region, locale and business size, ECs shouldn’t be surprised or feel ashamed if lighting work now brings in the most money. If it doesn’t, perhaps there’s more opportunity out there for it.

More than ever, this Profile of the Electrical Contractor is a testament to a theme of diversification. It’s true the industry is growing as a whole, but the contractors who venture into new markets are growing the most.

More to come

We couldn’t fit all we learned about electrical contractors and their work into a single article, so we published part two in the August issue. It dives deeper into the business side of operations, including project arrangements, such as design/build as well as more traditional bidding formats. It also analyzes the role electrical contractors play in specifying and substituting the products they install.

Methodology

The survey was conducted by postal mail and through the internet among a random sample of ELECTRICAL CONTRACTOR subscribers. The field period for the survey began on March 7, 2018, (for both the internet and postal mail versions), and ended on April 3, which was the deadline for the July 2018 article. A total of 1,597 interviews were completed—901 through the internet and 696 by postal mail. The data were weighted to equalize the influence of the two modes so that it was in line with the 50/50 split, which was the case in the most recent Profile studies.

Each respondent who received the survey through the internet was sent two follow-up emails. However, follow-up mailings were not made to nonresponders in the postal mail sample. An incentive was offered for participation in the survey: For each completed survey, ELECTRICAL CONTRACTOR would contribute $5 to charity, up to a total of $10,000. For the first time, the magazine also offered a sweepstakes drawing for one of five $150 Amazon e-gift cards.

The internet option was first introduced in 2004. In 2004 and 2006, the proportion of surveys completed using the internet versus postal mail was approximately 60/40. Since 2008, the proportion has been closer to 50/50. As noted above, in 2014, the data were weighted to equalize the proportion that participated by postal mail and through the internet.

As was the case since 2004, the survey was produced in different versions. Starting with the 2008 Profile study, there were four versions of the survey, which differed from each other on fewer than 10 questions. The first three pages were common to all versions, while the differences among the versions occurred on the last page. The major difference was that in the internet portion, respondents were required in almost all cases to have percentage questions add to 100 percent.

In 2014, in order to accommodate a longer list of questions while at the same time lessening the burden on the respondent, the survey was shortened from five print pages to four. In order to accommodate all of the questions, the survey was produced in eight versions (up from four). This required a much larger sample size so that each of the questions would be asked of a large enough sample to allow for analysis—particularly by subgroups. In 2016, there were seven versions; the two versions that deal with training (past 12 months and next 12 months) were combined. In 2018, there were also seven versions.

This research was conducted by New York-based Renaissance Research & Consulting Inc. (www.renaiss.com), an independent marketing research firm that has, as one of its specialties, market research for the construction industry.

Statistics

The margin of error on the total sample of 1597 is +/– 2.1 percent for percentages around 50 percent (i.e., we are confident that a reported 50 percent will fall between 52.1 percent on the plus side and 47.9 percent on the minus side 90 percent of the time.) Please note that different rules apply to testing of averages, which were also tested at the 90 percent level of confidence and are noted in the report.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].