You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

It’s that time again when we call on expert pollsters to help us learn more about our readers and the work they are doing in the field. More than 2,400 of you responded to our questionnaire earlier this year, through snail mail or online, describing the work you did in 2015. These 2,419 responses paint a portrait of an industry that’s both continuing to mend following the financial meltdown eight years ago and expanding into new business areas.

ELECTRICAL CONTRACTOR conducts this survey every two years, each time asking about the previous full year’s business. The 2014 edition (covering work completed in 2013) indicated a recovery was taking hold, and we’re happy to report that trend has continued. Fewer firms lost employees during the last 12 to 18 months, and a large majority of companies stood firm. Though large firms—those with 20 employees or more—remain a minority, their percentage grew, while the percentage of companies with 1–9 employees dropped slightly.

Such growth might, at least partly, be the result of a broadening in the kinds of work electrical contractors (ECs) now perform in addition to traditional power and lighting jobs. With new questions this year, we found that a large percentage of our respondents is working in heating, ventilating and air conditioning (HVAC) projects—both in controls and mechanical—and a significant number has even worked for water utilities and on wastewater treatment plants.

This article, along with a follow-up next month, explores the rest of what we learned about the work ECs are doing and how their businesses are faring. You can also check out the full 2016 topline report online. There you will find additional details and see how 2015’s results compare to those from previous years.

More gray matter

First, what do we know about individual ECs? Well, for one thing, they’re getting older, with an average age of 57.3, a statistically significant increase from 2014’s result of 56.2 (which had remained unchanged from the 2012 figure). Even more significant, the percentage of respondents aged between 35–54 decreased to 30 percent, from 36 percent in 2014. However, age goes down as firm size increases, with an average age of 54.1 in firms with 10 or more employees, versus 58.7 in companies with 1–4 employees. One explanation for this disparity is the possibility that older electrical pros might be more likely to go out on their own, after gaining experience in a larger organization. Or they worked in small companies their entire career and are now close to retirement.

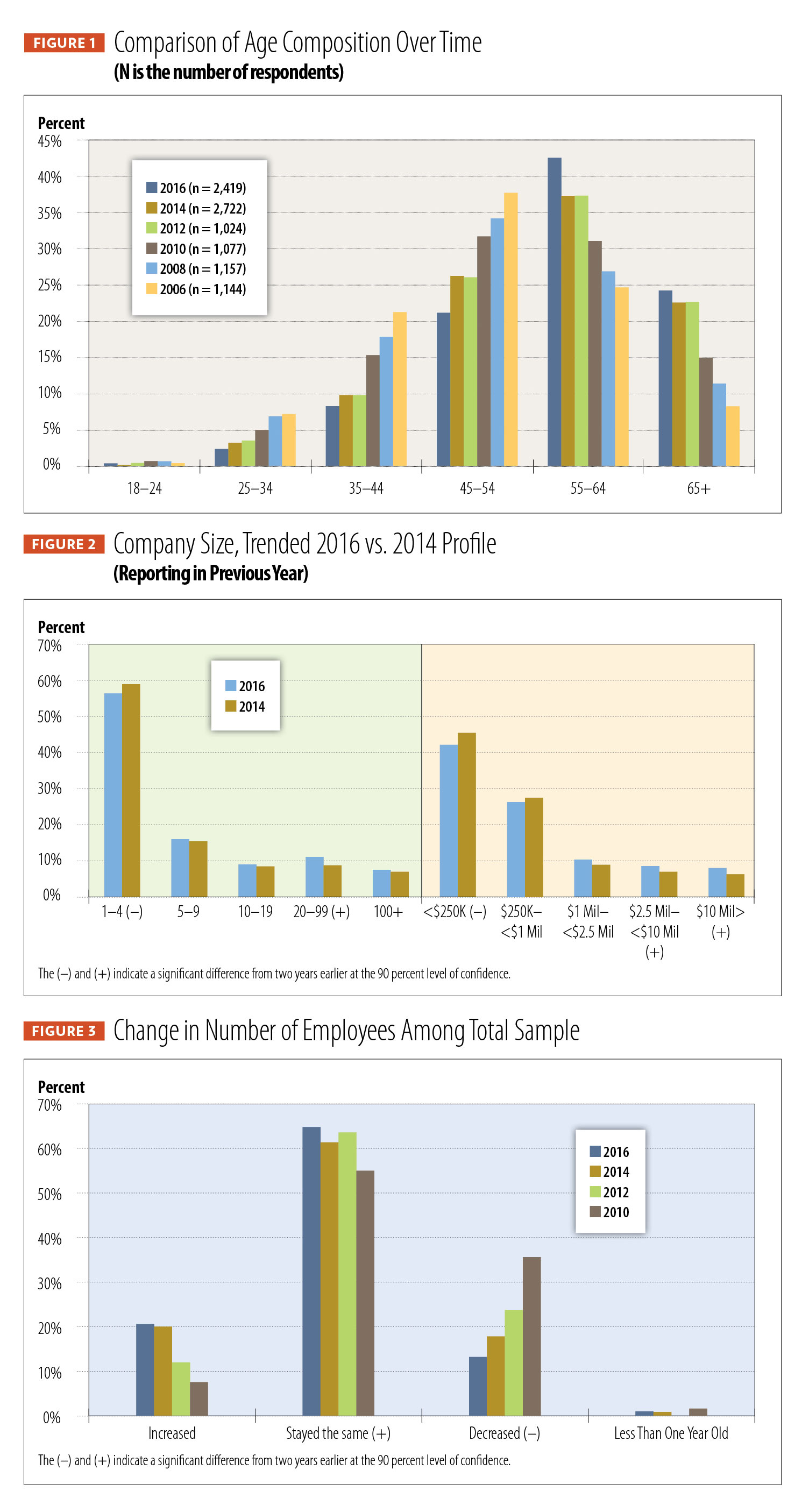

The aging trend is a long-term phenomenon. For example, as shown in Figure 1, Comparison of Age Composition Over Time, the percentage of ECs aged 35–54 has dropped to 30 percent, from 59 percent in 2006. At the same time, the percentage aged 55 and older has risen to 67 percent, largely driven by an increase in the 55–64 age bracket, to 43 percent from 38 percent two years ago.

However, one demographic in our sample breaks this aging pattern: women. However, at only 3 percent of total respondents, their numbers don’t make a big impact on the overall picture. In this survey, 42 percent of women in the industry are aged 35–54 (compared to 30 percent of the total sample), and only 7 percent are 65 or older (compared to 24 percent of the total). These women are more likely to work with larger companies, with 35 percent working for firms with 5–9 employees and 46 percent working for firms with 10-plus employees.

The increased respondent age also is reflected in their stated level of responsibility, with 79 percent of our sample composed of company owners and top management. In addition, 10 percent are master electricians (or an equivalent title). A new title category, “project manager,” was added to this year’s survey, accounting for 4 percent of respondents. Women are less likely than men to have the title of owner/top management, with 63 percent falling into this category; however, they are just as likely as men to be a master electrician or project manager.

A firm recovery

The large number of higher management titles also might be a side effect of the large number of small firms in our sample—with 72 percent of reporting firms having 1–9 employees, there’s a much better chance the respondent will be an owner, manager or master electrician. However, as shown in Figure 2, Company Size, Trended 2016 vs. 2014 Profile, the proportion of firms in the smallest category, 1–4 employees, has declined to 56 percent, from 59 percent in 2014, while representation by firms with 20–99 employees grew to 11 percent, versus 9 percent two years ago.

Across the industry as a whole, most firms have at least maintained a status quo in their employee rolls over the last 12–18 months, with the percentage of companies across the total sample holding steady and climbing to 65 percent (versus 61 percent in 2014). The proportion of those who lost employees during the reporting period fell to 13 percent, from 18 percent two years ago. Twenty-one percent reported adding employees, virtually identical to the last survey results. See Figure 3, Change in Number of Employees Among Total Sample.

However, these averages hide some interesting differences in hiring activity between smaller and larger companies, as you can see in Figure 4, Change in Company Size During Past 12–18 Months. Smaller companies of 1–9 employees were most likely to report stable employee numbers, with 75 percent falling into this category and only 11 percent stating they had added staff. For firms with 10 or more employees, however, the hiring climate has been much more bullish, with 47 percent reporting an increase in their numbers, from 42 percent in 2014. This kind of growth is a great reminder of how far the economy has recovered in the last 6 years; in 2010, 61 percent of the larger firms reported decreased staff numbers, and only 15 percent said they added employees.

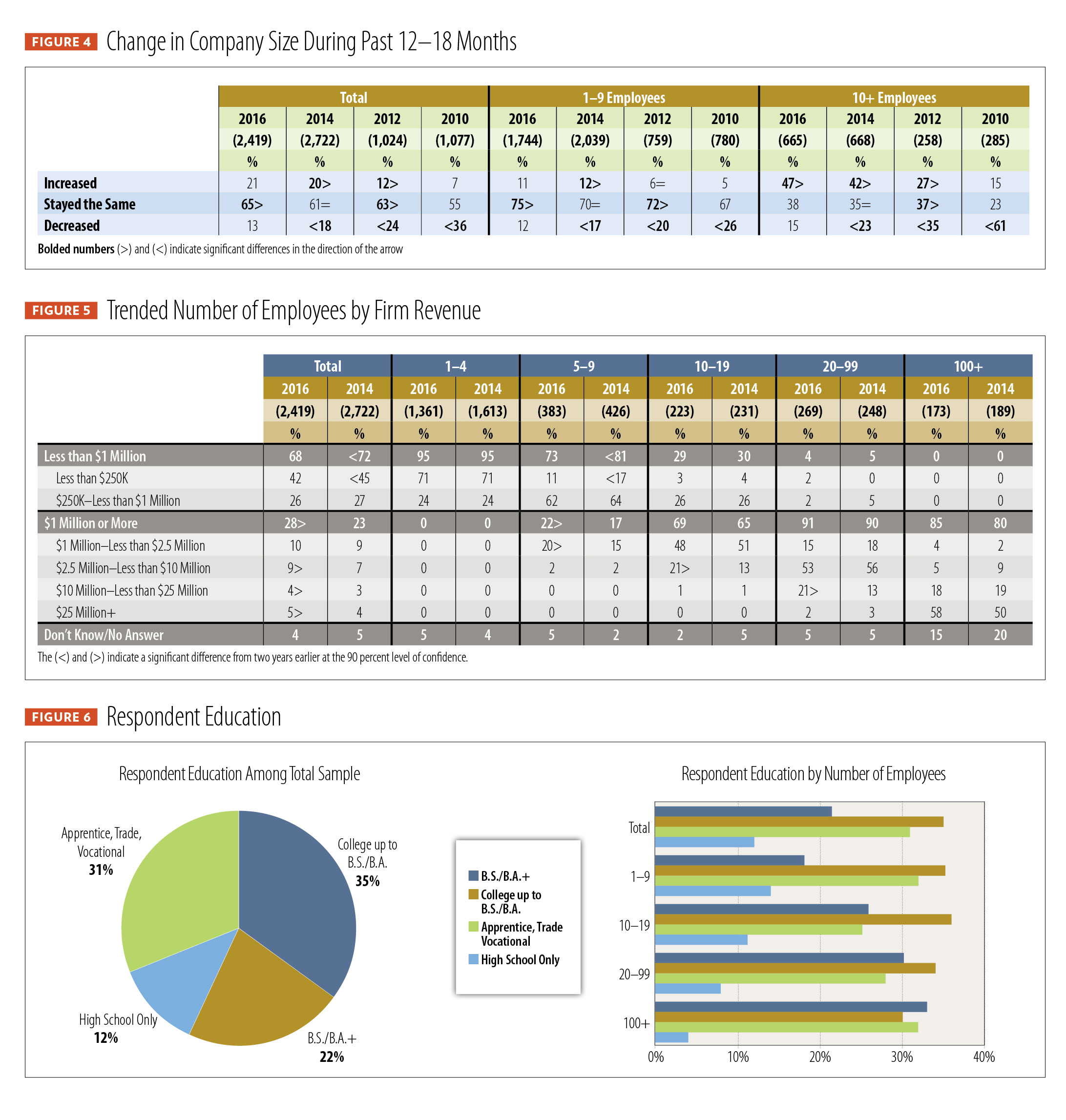

Firms, as a whole, also reported higher revenues for 2015, versus their figures for two years earlier, with a significantly smaller percentage of ECs working for firms with revenue under $1 million (68 percent this year, versus 72 percent in 2014) and a significantly higher percentage with firms of revenue over $1 million.

Again, though, this big-picture view obscures an interesting segmentation. As shown in Figure 5, Trended Number of Employees by Firm Revenue, the upward shift is driven primarily by improvements in the fortunes of firms with 5–9 employees. Seventy-three percent of ECs working in such companies reported their firm’s revenues totaled less than $1 million, versus 81 percent in 2014, and, correspondingly, 22 percent reported firm revenue of $1 million or more, versus 17 percent two years ago. These results support findings from the 2014 survey that companies with 5–9 employees are becoming more like larger firms and less like those with 1–4 workers.

Education level of electrical contractors has remained consistent with this survey, versus 2014’s results, with 57 percent across the total sample having some college education. However, a significantly higher percentage report having a bachelor’s degree in 2016—22 percent, versus 19 percent in 2014. Those working for firms with 10 or more employees are more likely to have at least some college education than those in smaller organizations (63 percent, versus 54 percent) and are more likely to have a B.A. or B.S. degree (30 percent, versus 18 percent). See Figure 6, Respondent Education.

What are you doing?

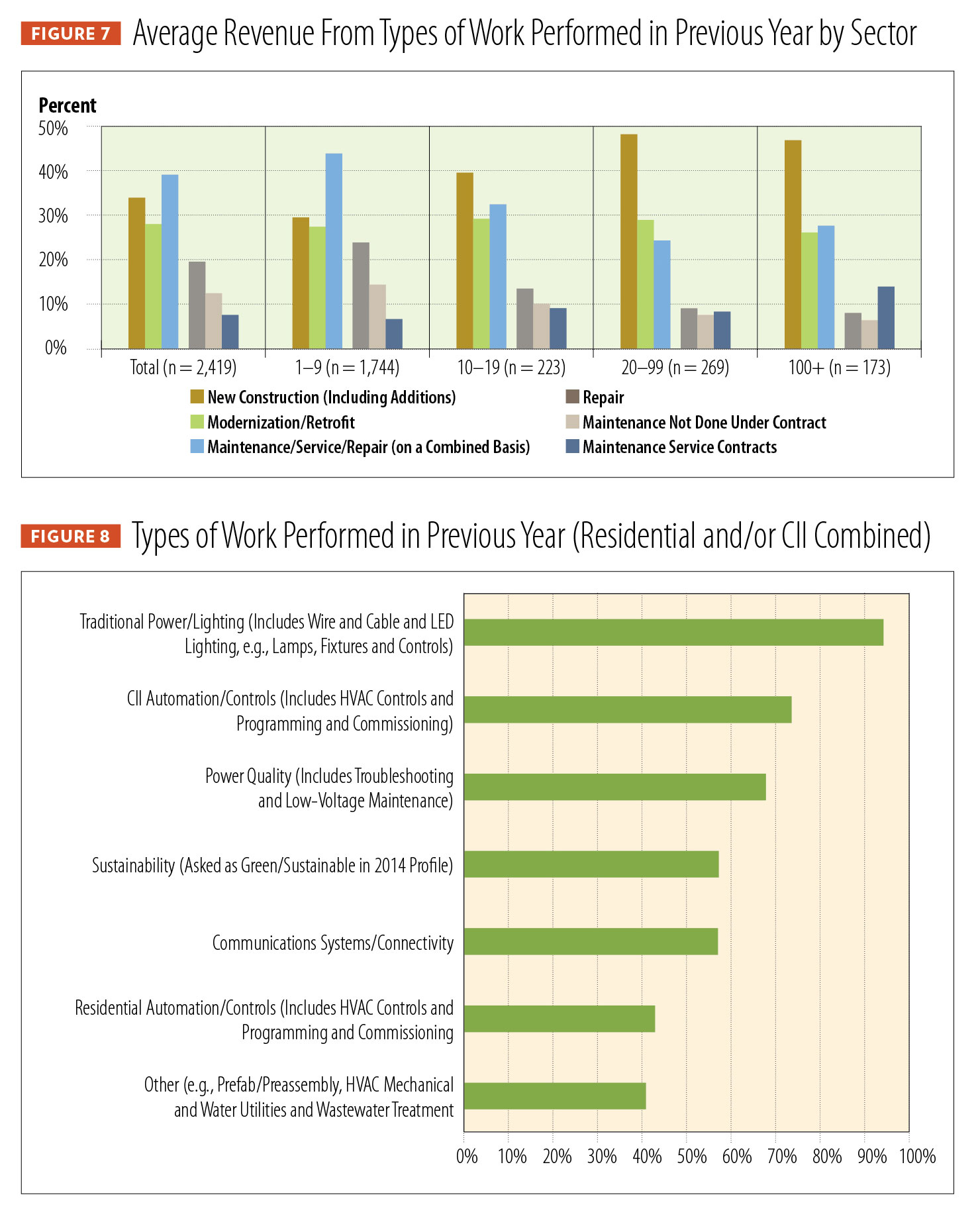

Looking at the type of work today’s ECs are doing indicates continuing improvement, if not a full return to the boom years of the early 2000s. For example, the average percentage of revenue derived from new construction has risen to 34 percent from 32 percent in 2014, a statistically significant increase, while the contribution of maintenance/service or repair has dropped to 39 percent from 41 percent. (As a benchmark, new construction accounted for 43 percent of average revenue in 2007.) At 27 percent of revenue, the contribution of modernization and retrofit work is unchanged since 2014.

Figure 7, Average Revenue From Types of Work Performed in Previous Year by Sector further breaks these results down, showing new construction is a bigger part of business for firms with 10 or more employees than it is for their smaller counterparts. Maintenance under service contracts also plays a bigger role in overall revenues with the largest firms than with the smallest.

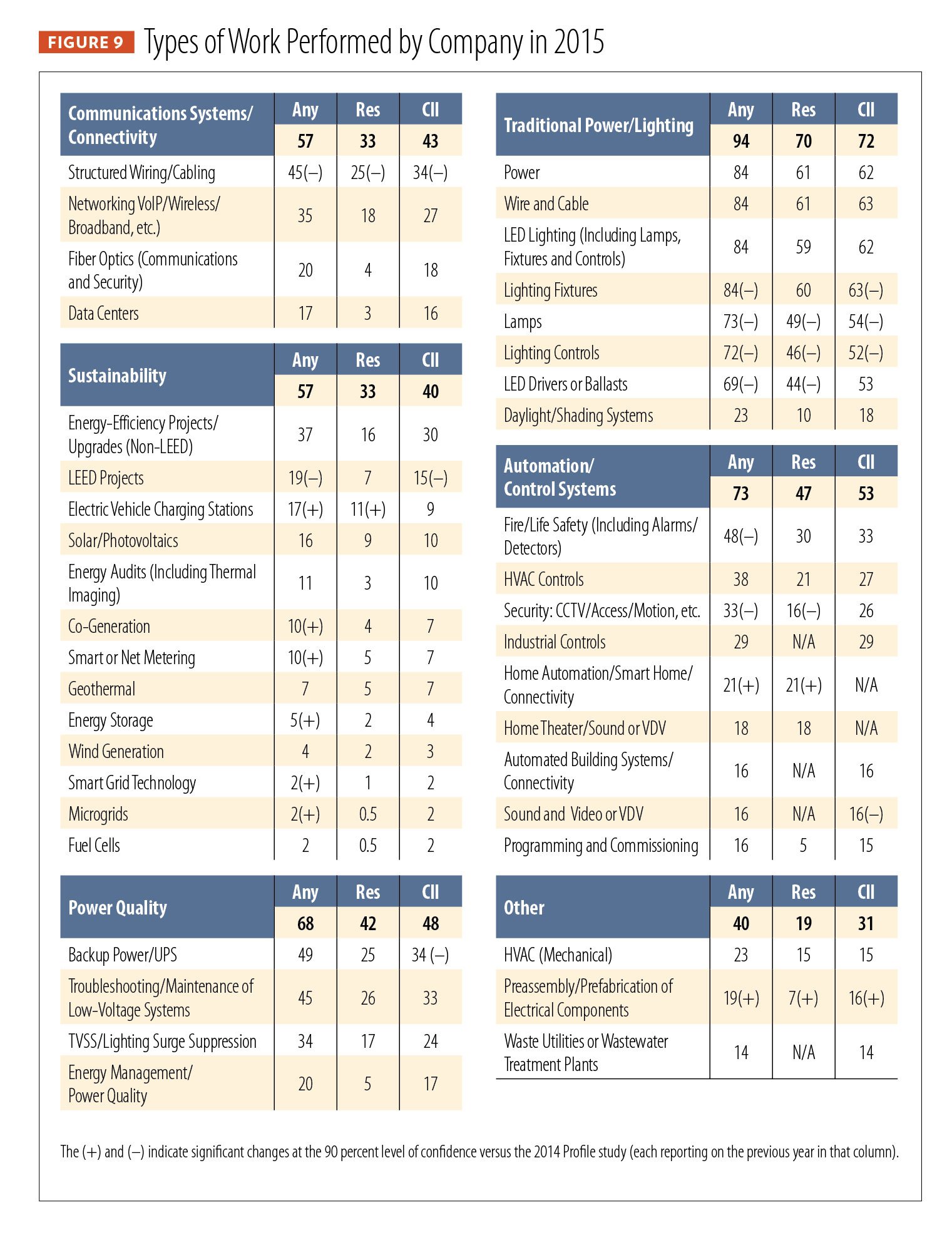

At a high level, considering both residential and commercial/industrial/institutional (CII) projects, traditional power and lighting projects were included in the work of 94 percent of respondents through the course of 2015. Second on the list, as shown in Figure 8, Types of Work Performed in Previous Year, is automation and controls, including HVAC controls and programming (CII and residential automation/controls are shown separately in Figure 10). Power quality, sustainability, communications systems/connectivity form a new tier, as does “other.”

At a more detailed level, we polled respondents on their participation in 41 specific project types, including five new categories for 2016: wire and cable; LED lighting (including lamps, fixtures, controls); HVAC controls; HVAC mechanical; water utilities or wastewater treatment plants. Among the key findings in this part of the research is the fact that higher percentages of ECs perform these individual tasks in CII settings than in residential construction. For example, as shown in Figure 9, Types of Work Performed by Company in 2015, 34 percent of ECs said they worked on structured wiring/cabling in CII, compared with 25 percent who did this kind of work in residential construction.

However, exceptions to this general rule are seen in five categories—power, wire and cable, fire alarms, HVAC mechanical and electric vehicle (EV) charging stations—in which residential and CII involvement are quite similar.

In reviewing the combined total of residential and CII projects, we found some notable changes over the 2014 survey’s results:

- Six sustainability-related work types posted significant increases, including EV charging stations, smart or net metering, co-generation, energy storage, smart grid technology and microgrids. Preassembly/prefabrication of electrical components also posted an increase over 2014.

- LEED-related work declined, despite the growth of the green-leaning project types above.

- Structured wiring declined; however, respondents might have reported some of this work as part of the new wiring and cabling category added in 2016.

- Similarly, fewer respondents reported working on lighting fixtures, lamps and lighting controls or LED drivers or ballasts, which could simply reflect the addition of a new LED lighting category (including lamps, fixtures and controls).

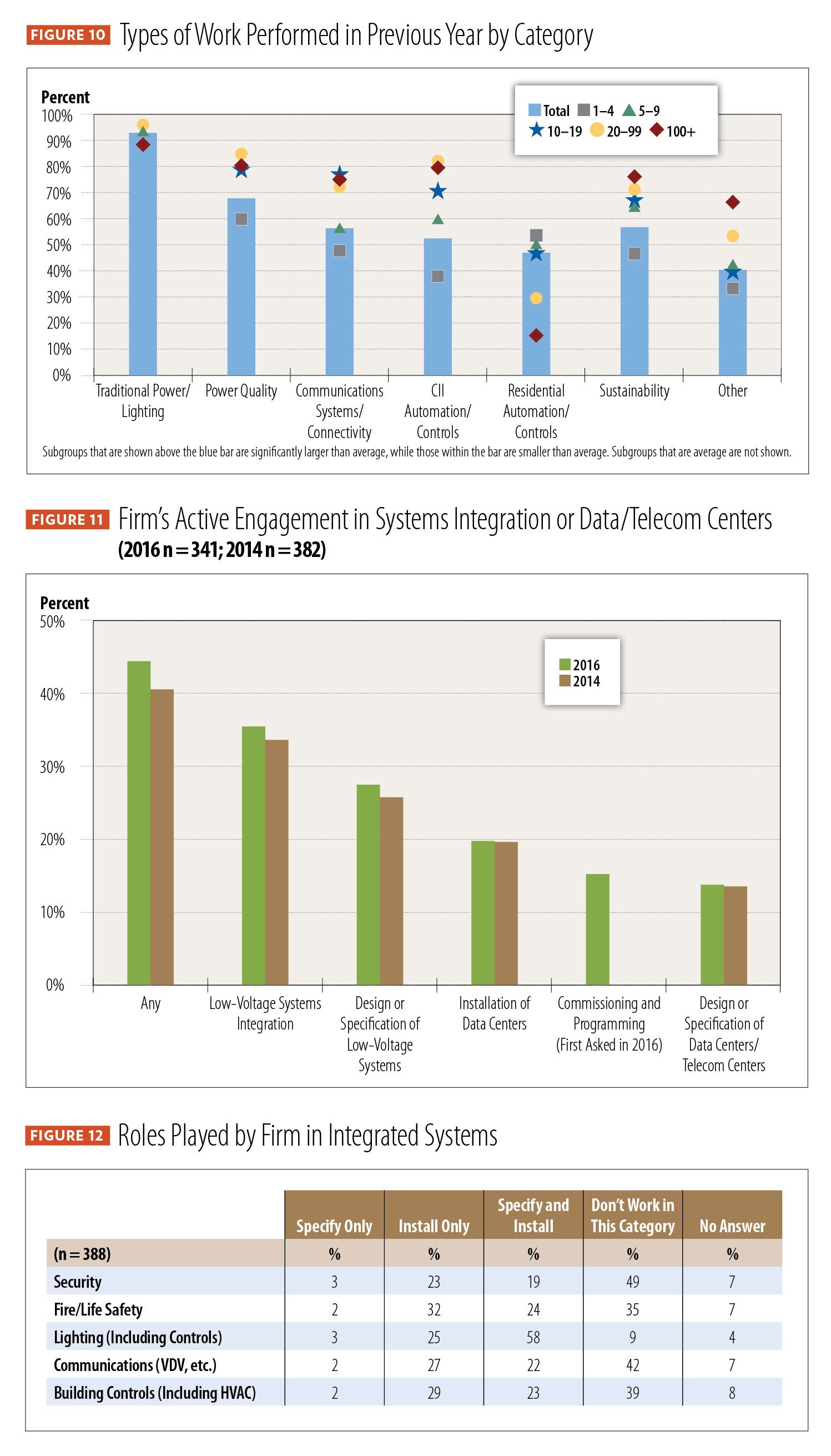

Figure 10, Types of Work Performed in Previous Year by Category, provides a snapshot of the kinds of work done by firms of different sizes during 2015. Note the trend spotted in the 2014 survey that firms with 5–9 employees are starting to look more like companies that are slightly larger than those that are slightly smaller. Another notable point is the broad range of project types the smallest firms are working on within the residential sector. Companies with 1–4 employees are performing many aspects of traditional power and lighting, low-voltage, automation and even HVAC work. In addition, the fact that so much of this kind of work is now being done in residential settings demonstrates how complex our homes are becoming.

Low-voltage projects

The 2016 survey results show low-voltage projects have a big presence in the work of today’s ECs. Across the total sample, 95 percent of respondents reported they had completed such projects, and 10 percent of all firms noted they now have a separate division dedicated to low- voltage efforts, up from 7 percent in 2014. There has been a significant uptick since 2014 in low-voltage interest among firms with 10 or more employees—25 percent of such firms reported having a separate low-voltage division, which is up from 20 percent in 2014.

As indicated in Figure 11, Firm’s Active Engagement in Systems Integration or Data/Telecom Centers, the kinds of work ECs are doing in this field does not differ much from what was reported in 2014. However, a category just added to this year’s list of questions indicates how broad EC involvement is becoming, with 16 percent reporting experience in commissioning and programming assignments. Low-voltage systems integration is the biggest category of low-voltage work for respondents, with 35 percent stating involvement in such projects.

Looking at several specific integrated systems product categories, one can see the overwhelming importance of ECs in lighting selection and installation. Figure 12, Roles Played by Firm in Integrated Systems, shows that almost 60 percent of ECs said they both specify and install lighting—about double the percentage that say they only install such systems, without also specifying them.

Where’s the money?

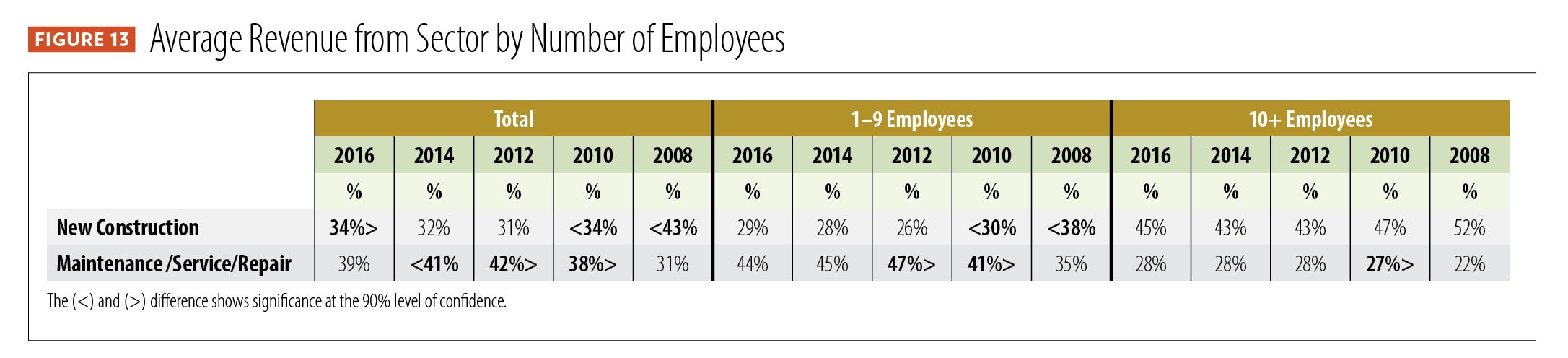

In small but statistically significant ways, new construction has become more important to ECs’ bottom lines, accounting for 34 percent of 2015’s revenue, across our total sample, up from 32 percent in 2013. It was especially important for larger firms, responsible for almost 50 percent of revenue for firms with 20 or more employees (not shown). On the flip side, the maintenance/service/repair sector is at the top for billings among smaller companies. While the revenue percentages for each sector remained fairly steady compared to 2014’s survey results, Figure 13, Average Revenue From Sector by Number of Employees, shows how much more important new construction was eight years ago, when it represented 52 percent of revenue for larger companies.

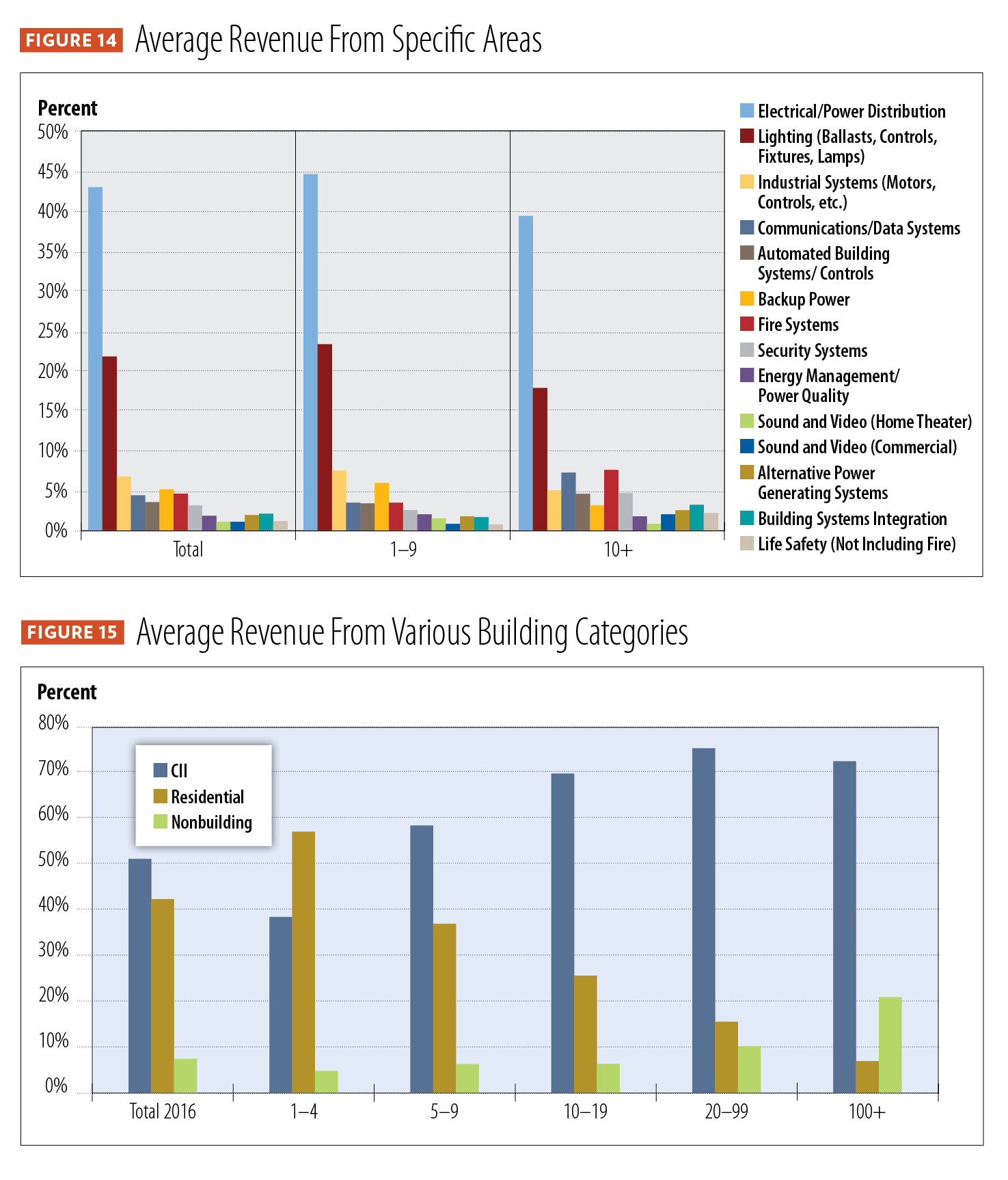

Looking at the types of work ECs are doing within these sectors, electrical/power distribution accounted for 43 percent of revenue in this year’s survey, and it is statistically unchanged from 2014. As a point of reference, in 2004, respondents indicated this category accounted for 69 percent of revenue, which serves as another indicator of how much ECs have expanded into other areas just over the last dozen years. Figure 14, Average Revenue From Specific Areas, shows that this trend holds true for the smallest firms—revenue from electrical/power distribution is no longer statistically higher for these companies than for their larger counterparts.

Looking at our total sample, CII projects represent a larger portion of total revenue than either residential or nonbuilding (including transportation/lighting and utility categories) projects, though residential is the top money-maker for firms with 1–4 employees. Continuing a switch seen in the 2014 survey, though, firms with 5–9 employees are no longer following that pattern; as in several other areas, these companies are more like larger organizations in this breakdown of revenue sources. See Figure 15, Average Revenue From Various Building Categories.

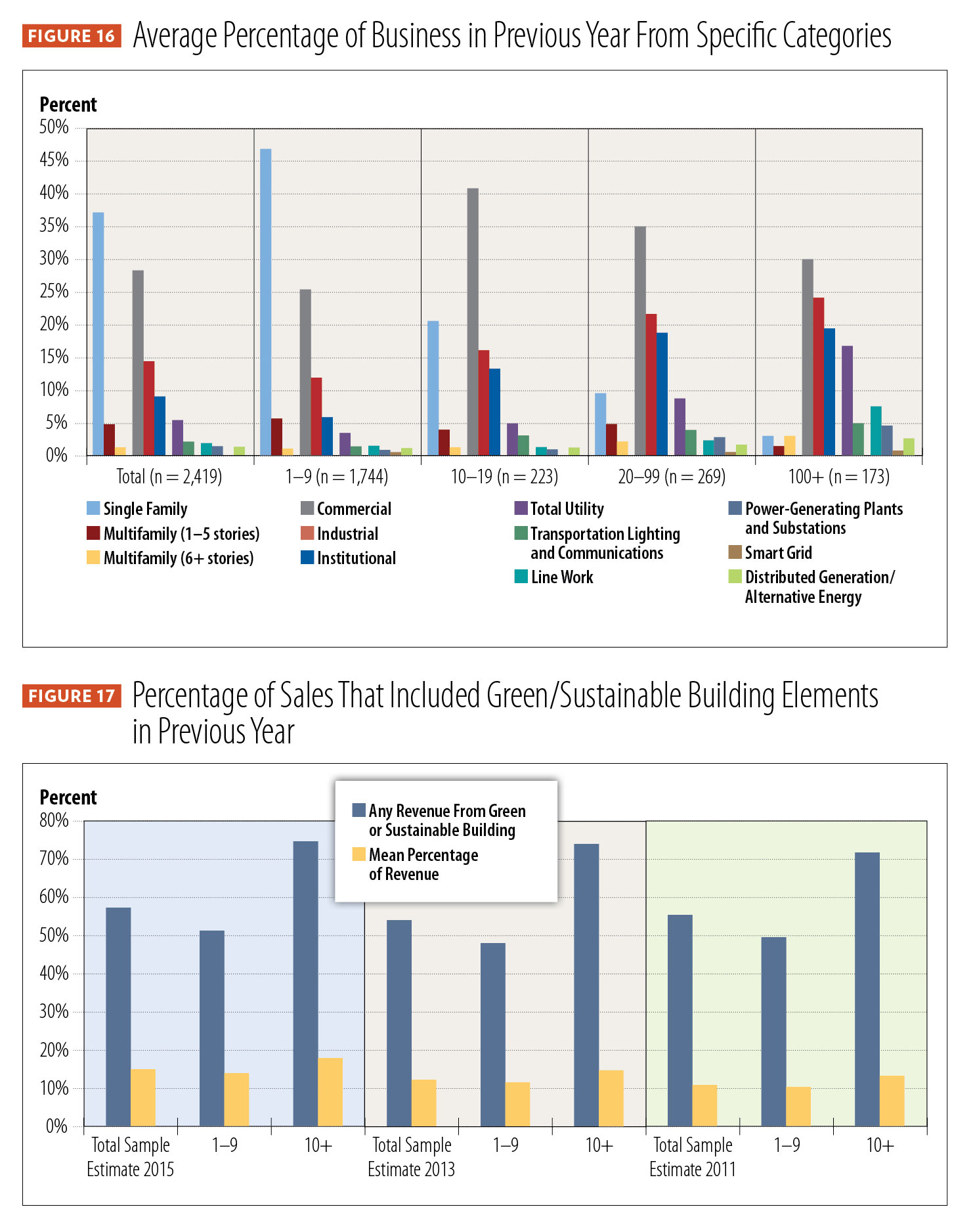

Despite the combined importance of CII work, single-family housing remains the single largest revenue source for ECs, at 36.7 percent of the total, across our entire sample, as shown in Figure 16, Average Percentage of Business in Previous Year From Specific Categories. Small firms derive almost half their revenue from single-family projects. Within the CII category, commercial construction is most important, contributing 28.1 percent of revenue, compared to 14.2 percent for industrial and 8.7 percent for institutional. Firms with 10–99 employees are most dependent on commercial construction, while those with 100 or more employees get a disproportionate percentage of their revenue from industrial and institutional projects and utility/nonbuilding work.

Seeing green in green

As energy codes continue to tighten performance requirements for everything from lamps to fan motors, it’s becoming a bit more difficult to separate out sustainability as a business driver. For example, is a client request for LED lighting intended to boost a facility’s “greenness,” or simply future-proofing, with recognition that LEDs are the direction toward which all lighting technology is heading?

With this caveat in mind, we do continue to ask about the importance of green/sustainable building elements in overall sales. In total, 56.4 percent of respondents reported that at least a portion of their sales fell into this category, accounting for an average of just under 15 percent of revenue. The impact of such products and services grows with firm size, as shown in Figure 17, Percent of Sales That Included Sustainable Building Elements in Previous Year. More than 80 percent of respondents from the largest firms reported at least some sustainability-related revenue.

Training plans

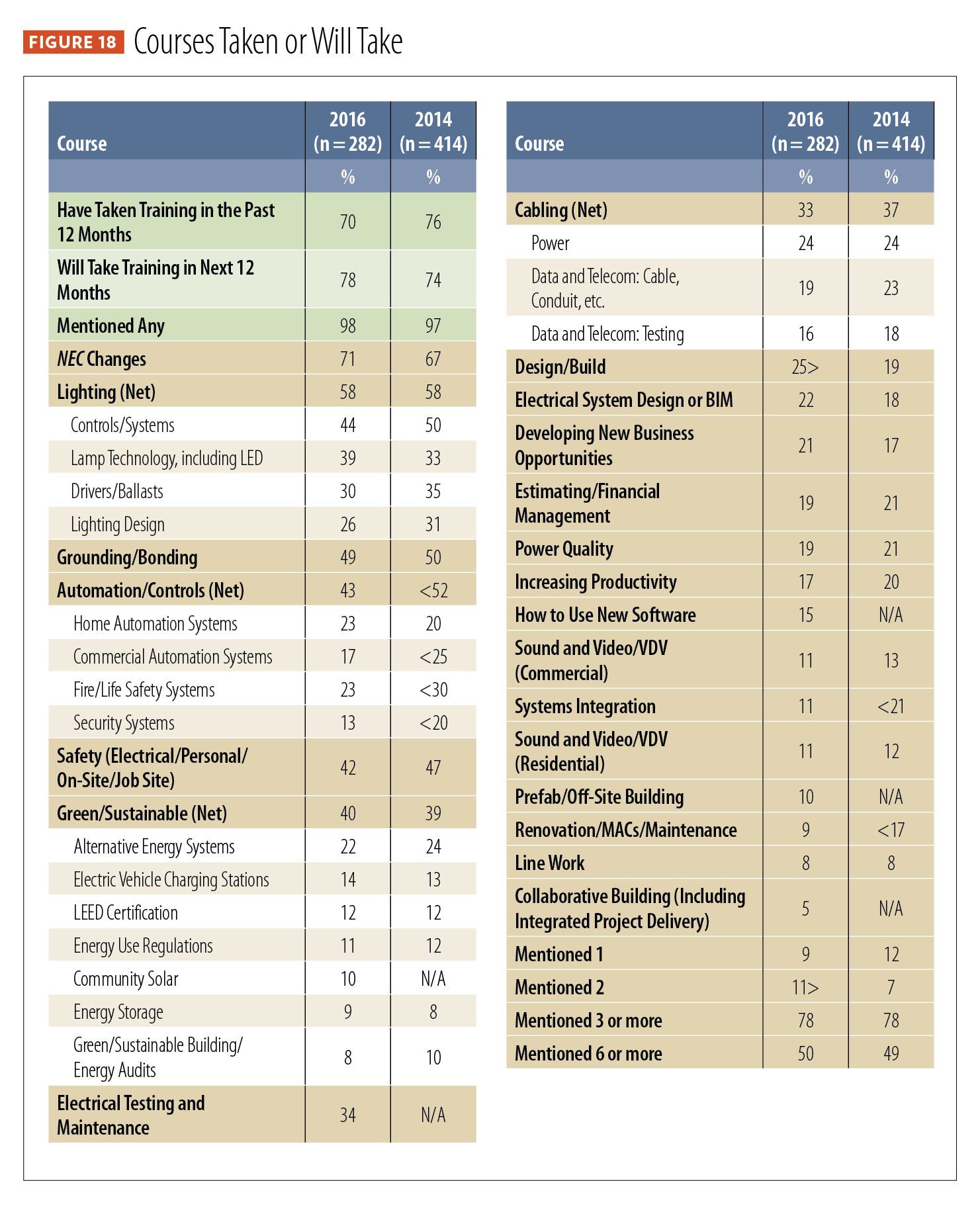

Our respondents recognize the need to keep up with new technologies, as more than 70 percent say they or someone in their firm has taken training in the past 12 months or plans to do so in the next 12 months, either to improve their skills or gain or maintain certification. This isn’t a new trend—the percentages remain statistically unchanged from the 2014 survey, as shown in Figure 18, Courses Taken or Will Take.

The leading reason for training isn’t surprising—with the National Fire Protection Association revising its National Electrical Code (NEC) every three years, those updates top the list of topics at 71 percent. Other subjects included:

- Lighting (58 percent), particularly controls and systems (44 percent)

- Grounding and bonding (49 percent)

- Safety (42 percent)

- Green/sustainable (40 percent), particularly alternative-energy systems (22 percent)

- Electrical testing and maintenance (34 percent)

- Cabling (33 percent)

Increased interest also was indicated in several project-delivery and business-development topics, including:

- Design/build, at 25.4 percent, versus 18.8 percent in 2014

Stay tuned for more

We learned much more about electrical contractors and their work than we could fit into a single article, so be sure to check out Part 2 of our findings in next month’s issue of ELECTRICAL CONTRACTOR. The topics we will be covering include the kinds of project arrangements ECs are seeing most frequently, such as design/build and more traditional bidding formats, along with the role ECs play in specifying and substituting products.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].