Want to see all of the data behind this article? Read the Topline Report for the 2024 Profile of the Electrical Contractor.

We are optimistic because—in the responses from 828 of you—we found electrical contracting firms are getting larger and growing their revenues. While firms with nine or fewer employees still make up the majority of our respondents, that lead is narrow, at only 51%, continuing a trend we noted in 2022.

Compared to two years ago, the proportion of firms with 1–4 employees showed a statistically significant decline, while the percentage of firms with 10 or more employees grew. We also found that nearly twice as many firms added employees (28%) as dropped them (15%). Two years ago, these figures were essentially equal.

Business revenues are also growing in parallel with employee numbers. That’s good news and, compared to 2022, there are significantly fewer firms with revenues under $1 million and more with revenues over $2.5 million, both in total and in each subsequent revenue break of $10 million and $25 million.

Where that revenue is coming from continues to shift. For example, electrical contractors are earning less from single-family projects, which accounted for 38.4% of revenue in 2018. This year’s respondents said such work only added up to 29% of revenue during 2023, about equal to commercial.

These are just a few of the data points revealed in our 2024 survey’s findings regarding the state of electrical construction in 2023. There is much more information to follow in this comprehensive two-part report. Visit ECmag.com/profile where we maintain an archive of past results for easy, over-time comparisons.

Aging slowdown

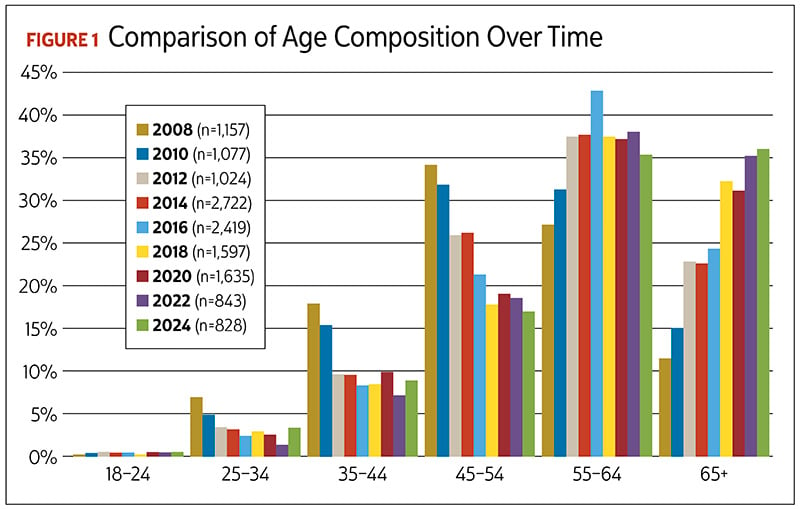

This year, the average age of electrical contractors has remained statistically unchanged at 58.6 years old (versus 59.3 years old in 2022). Two years ago, it seemed electrical contractors had resumed trending older (see Figure 1).

Now, we see some younger folks are getting into the industry, with the percentage of respondents aged 25–34 increasing to 3% from 1% two years ago. This is the only statistically significant age-group shift. The proportion for ages 35–54, 55–64 and 65+ remained unchanged from 2022’s figures.

The age numbers also remained flat across firm size. However, ECs working for larger companies continue to be younger, on average, at 56.6 years, than those in companies with nine or fewer employees, where 60.7 years is the average.

Female respondents made up 5% of the total, statistically unchanged from 2022. However, that figure jumps to 9% in the 35–54 age range. Like 2022’s survey, these female electrical contractors are less likely to work in very small firms. They make up only 3% of those from companies with 1–4 employees and only 1% of those from companies with revenue under $250,000.

We first asked our respondents about their years of electrical contracting experience in 2018, and the figure hasn’t moved a great deal since then, with this year’s participants averaging 33.2 years, statistically unchanged from 33.9 years in 2022. Also like our previous results, an impressive 7% have been in the industry more than 50 years.

Company owners and those in top management positions made up 72% of our survey respondents, and 12% are master electricians or hold similar titles, statistically unchanged from 10% in 2022. Owners and top managers are mostly in the 65-plus age group—not surprising, given the years of experience needed to reach that level.

Growing trends

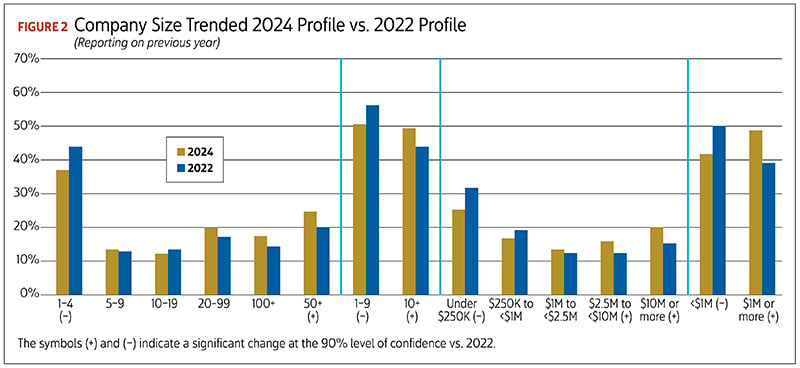

The last several Profile surveys have shown a steady decline in smaller firms, a rise in the proportion of companies with 10 or more employees and an increase in overall revenues. That trend continued this year as respondents described their companies’ 2023 operations. As shown in Figure 2, the proportion of firms with 1–9 employees dropped to 51%, down from 56% in 2022 and 66% in 2020.

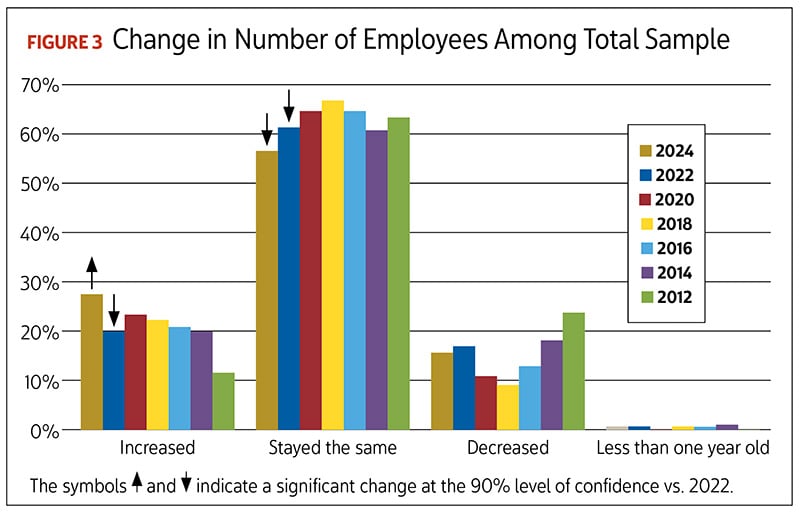

In our last survey, which looked at possible effects of COVID-19, we noted that staff rolls had remained stable, and that remains the case this year, with 56% reporting no change in company size. However, as Figure 3 shows, growth was more common than decline for those whose size did shift, which differed from our 2022 results.

More than a quarter of respondents said their companies added new employees in the previous 18 months, compared to 15% that said their size had decreased. In 2022, there was an even split of about 20% who said their firms had grown or gotten smaller.

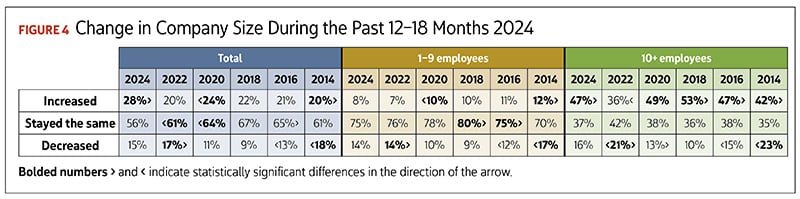

The likelihood of growth versus decline in our 2024 responses wasn’t the same across all firm sizes, as seen in Figure 4. For example, companies with fewer than 10 employees were more likely to have gotten smaller (14%) than to have grown (8%). The situation was significantly more positive for organizations with 10 or more employees, with 47% adding staff and only 16% decreasing in size.

Where is the skilled labor?

Finding qualified new employees continues to be a challenge, which has been the case at least back to our 2020 survey. Respondents were asked about the job market as they were completing the survey between January and March 2024.

Across all company sizes, 63% said they had difficulty finding trained workers and 33% had trouble retaining trained workers. These issues were substantially more pronounced for larger companies, with 80% finding and 46% retaining, respectively.

The postpandemic recovery trend noted in 2022 continued in this year’s survey, with significantly fewer firms with sub-$1 million revenue, 42% compared to 50% two years ago. More respondents reported company revenue of more than $2.5 million. Not surprisingly, though, income increases varied by company size, with 64% of those with 1–4 employees reporting revenue below $250,000, while 63% of those with 100-plus workers reported revenue above $25 million.

Economics by category

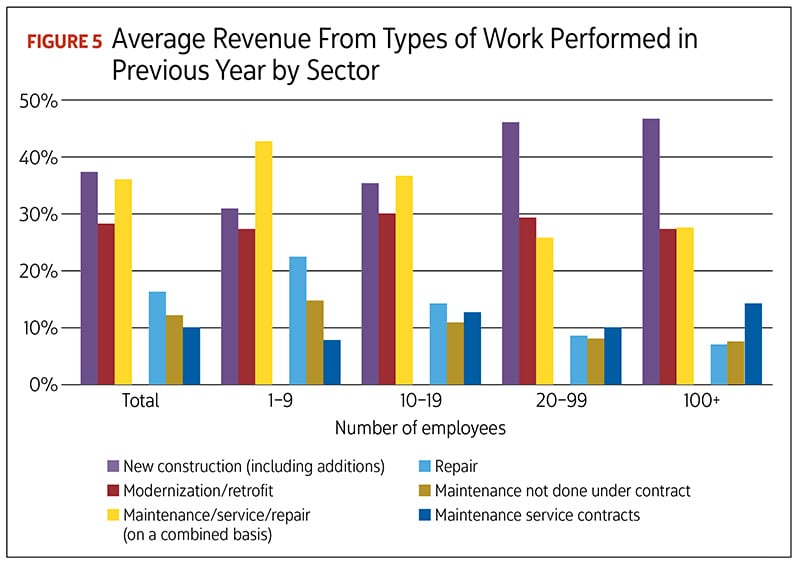

Categories shifted some with our 2024 survey, as we asked respondents to look back at their 2023 earnings and the larger sectors they represented (see Figure 5). For one thing, new construction grew to 36.6%, versus 31.8% in 2022, when we asked about 2021’s financials. Maintenance/service or repair dropped to 35.7% from 38.7% in 2022’s responses. This was due to a decrease in repair work, specifically, to 15% from 18% in 2022. The rise in new construction was especially notable in firms with 1–9 employees, rising to 30.3% of revenues, up from the 24.8% reported two years earlier.

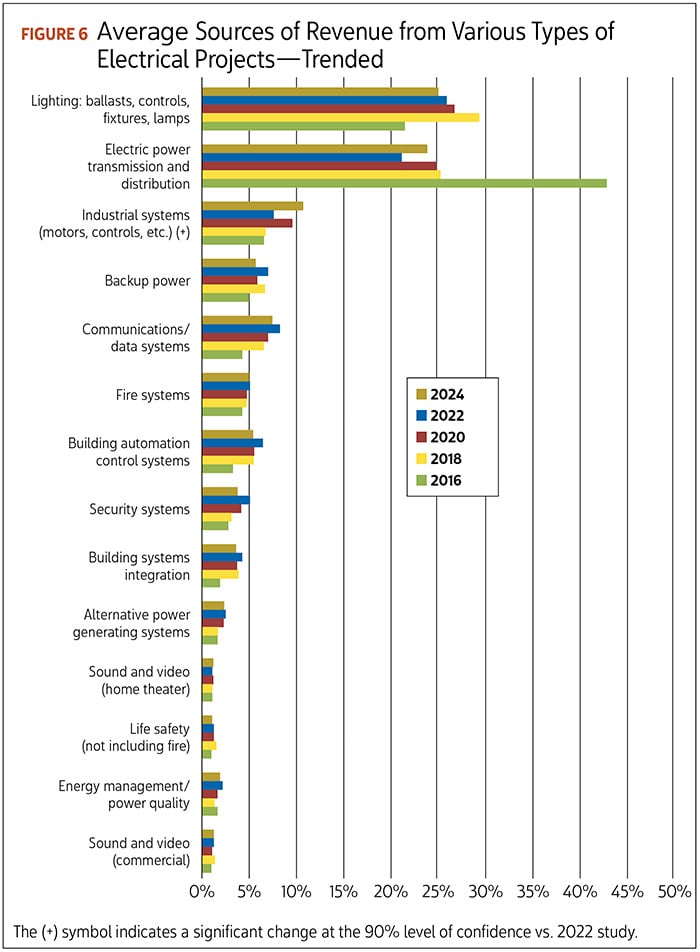

To drill down further, as in the past, we presented ECs with a list of 14 project types to rank by revenue, which you can see in Figure 6. Lighting, electric power transmission and distribution and industrial systems remained the top three revenue categories, as respondents looked back over their companies’ 2023 performance. However, in a bit of a twist, industrial systems took a significant jump up to 10.8%, compared to 7.8% in responses from 2022.

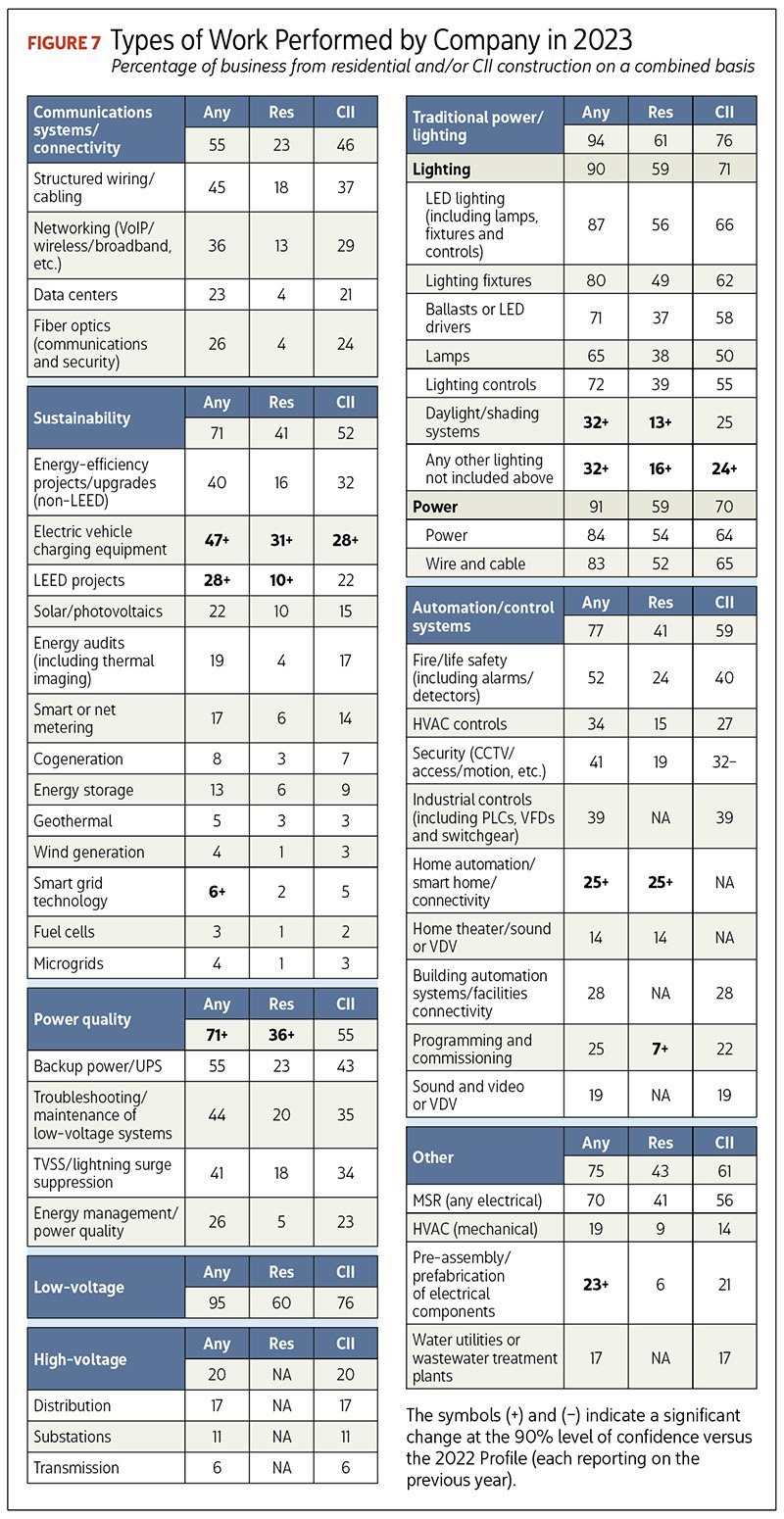

For a more detailed view of ECs’ businesses, we queried you about work you did in 2023 in a list of more than 40 different project types in residential and commercial/institutional/industrial (CII) settings. Responses are shown in Figure 7. Comparing this combination of residential and CII project types to responses from the 2022 survey, the results are relatively unchanged, and any differences are the result of business increasing in those categories. More of those increases occurred in residential construction. For example:

- More ECs said they are performing “other types of lighting” in residential and CII settings.

- Daylighting rose in residential construction and on a combined basis.

- Home automation/smart home connectivity and programming/commissioning both rose in residential construction.

- Electric vehicle charging equipment rose in both residential and CII settings.

- Both LEED projects and power quality as a broad category rose in residential projects and on a combined basis.

In terms of CII work on its own, percentages generally held steady across categories in comparison to our 2022 findings, with several notable exceptions. First, involvement in EV charging installation continues to grow, with 28% reporting work with this equipment, versus 24% two years earlier. However, security system work, including CCTV, access control and motion sensing decreased to 32% from 36%. Perhaps do-it-yourself wireless systems are having an effect in this area. Additionally, 17% worked on water utilities/wastewater treatment plant projects in 2023, statistically unchanged from what was reported for 2021.

For residential and CII combined, there’s evidence that electrical contractors continue to work in other nontraditional areas as well. For example, 38% worked on either HVAC controls and/or HVAC mechanical, with 15% working in both areas (this figure is a statistically significant drop from the 18% reported in 2022, regarding business in 2021).

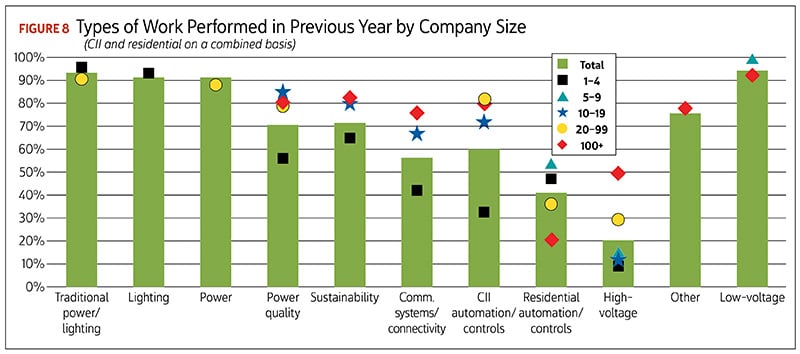

As previous surveys have shown, the largest firms—those with 100 or more employees—work in more categories than their smaller counterparts, and they’re above average in six of the queried categories. Smaller firms are more likely to be involved in two to four of those categories, but which categories also varies by size. See Figure 8.

- Firms with 1–4 employees are more likely than average to work in traditional power, lighting and residential automation/controls.

- Those with 5–9 employees are also more likely than average to be involved with residential automation/controls and low-voltage work.

- Those with 100-plus employees are more likely than average to be involved in more complex projects, including prefabrication, power quality, sustainability and high voltage.

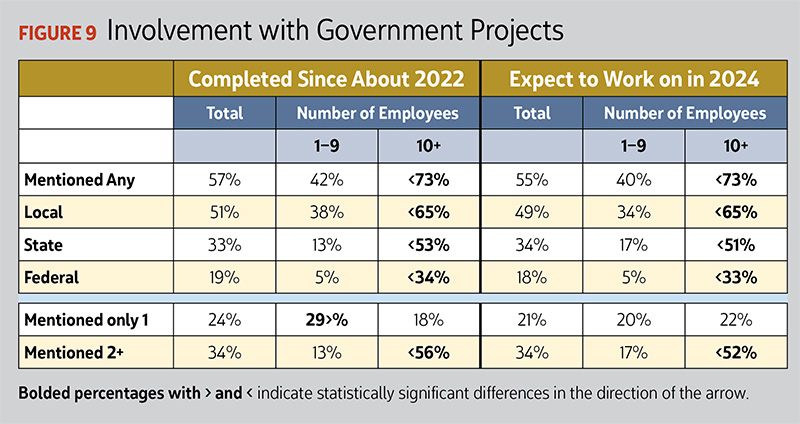

More than half of firms have worked on government projects since 2022 (57%), and 55% said that they expect to work on government projects in 2024. Regardless of the time frame of the work, more of the participation is close to home, i.e., more local government work than state or federal. Larger firms are far more likely to perform government work (some 73% among firms with 10+ employees compared to about 40%–42% among firms with 1–9 employees). Larger firms are about twice as likely to have done or plan to do local work, about four times more likely to have done or plan to do state work, and about six times more likely to have done federal work than smaller firms. See Figure 9.

In terms of where ECs do their work, the percentage of firms with projects in multiple states has held steady since the 2022 survey at 40%. As has been the case traditionally, larger firms are more likely to work in multiple states; 56% of those in firms with more than 10 employees reported their company worked in multiple states.

High interest in low-voltage

Low-voltage is a very broad project category, including fiber optic cable installation, networking, LED lighting controls, structured wiring and more. So, it’s not surprising that, across the entire sample, 95% of

respondents reported involvement

in low-voltage projects. As has been the case with the last several surveys, 26% of respondents said their firms currently have a separate low-voltage division, and this is more likely for those firms with 10 or more employees. In 2024, larger firms

are more likely to plan to add a

low-voltage division in the next one to two years

compared to smaller firms.

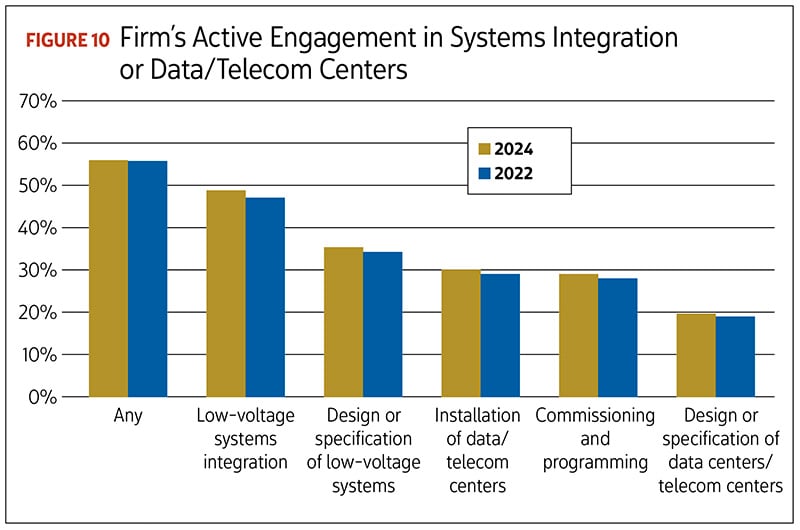

Data/telecom center work will likely be getting more attention over the next few years, as the effort to build more facilities to support artificial intelligence integration kicks in. As Figure 10 shows, more than half of respondents—56%—are already actively involved in systems integration or data centers, with low-voltage systems integration the most-mentioned task within this category, at 48%. This was followed by design or specification of low-voltage systems (36%), installation (29%), commissioning and programming (28%), and designing or specifying data/telecom centers (20%).

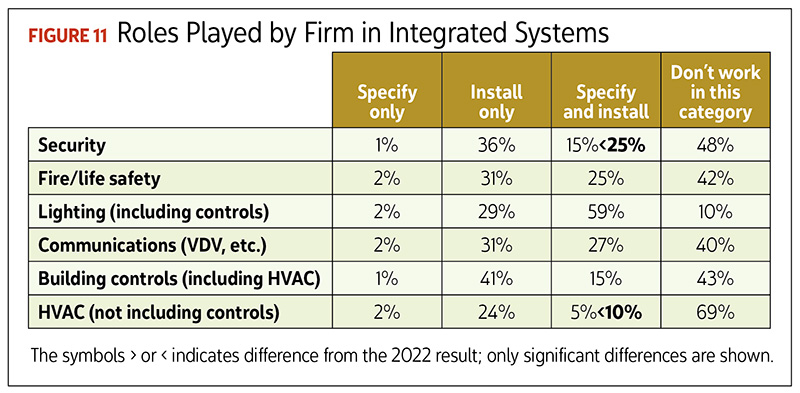

In terms of work with integrated systems, 59% of respondents said they specify and install lighting, which—as has been the case historically—is about double the percentage that only do installation. For most of the other integrated systems categories, between 15% and 27% of ECs specify and install equipment, except for HVAC (not including controls). Specify-and-install percentages dropped significantly for security and HVAC (not including controls) compared to the 2022 responses. See Figure 11.

Revenue leaders

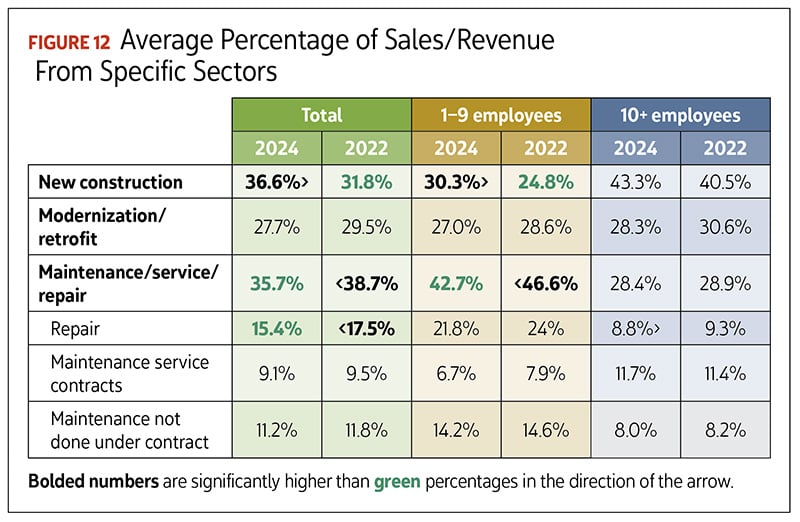

There was a bit of a shakeup at the top with this year’s survey when looking at what areas of work were most important to electrical contractors’ bottom lines. Looking at 2023’s business, 37% of revenues on average came from new construction (up from 32% for 2021) and 36% from maintenance/service/repair (down from 39% for 2021), with 28% credited to modernization/retrofit projects. See Figure 12.

While this does represent a boost in new construction, this sector still hasn’t recovered from the Great Recession. In our 2008 survey, which looked at business in 2007 just before the housing crash, new construction represented an average of 43% of revenue across all company sizes. This means there's room for upward movement.

These averages can shift when looking into performance by company size. Taking this view, new construction is even more important to firms with more than 20 employees than it is for smaller firms.

Maintenance/service/repair—which fell across

the entire sample thanks to a drop in repair work—is a bigger revenue contributor for smaller companies, topping 40% for those with 1–9 employees.

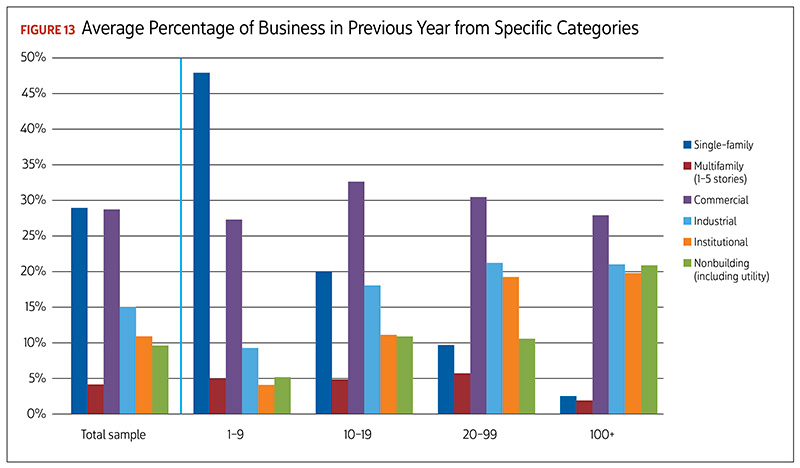

Earnings by building type

Looking at earnings by building type (Figure 13), the increase we noted in CII work for 2021 in the 2022 survey, along with a slip in residential work, has held steady. Respondents reported an average of 55% of revenue coming from CII projects, 35% from residential and 10% from nonbuilding efforts. CII and nonbuilding (which includes transportation lighting and utility) account for more average revenue for the largest firms than for other company sizes.

These figures have maintained a shift we noted in the 2022 survey, when industrial work (not broken out in this figure) jumped from 13.6% in 2020 to 16.7% across all firm sizes. Additionally, the figure indicates how quickly residential work’s importance drops as company size grows. Although it accounts for more than 50% for businesses with fewer than 10 employees, it falls by half with the 10–19 cohort and is just more than 9% for companies with 100-plus workers.

With this year’s survey, we found that commercial and single-family housing categories contributed equivalent percentages of revenue in 2023 across companies of all sizes, at 29%. This isn’t a big change from our 2022 survey, but it does continue a decrease in single-family housing’s importance since 2018, when it averaged 38.4% of all revenue.

Other findings of note:

- Commercial work quickly becomes the most important revenue category as firms expand beyond 10 employees, rising to more than 30% for those with

10–19 workers, while single-family jobs fall to 20%. - Industrial work jumps noticeably, to more than 20% of average revenue, as firms grow above 20 employees.

- For the largest firms, nonbuilding projects (including utility work) pulls even with industrial work in terms of revenue proportion.

Bidding requirements

Questions about bidding requirements have now become standard for these surveys, as this is the third round where we’ve queried electrical contractors on the topic. Across the whole sample, 48% say a prequalified standards and safety program is a necessity. But, as has been the case previously, this need increases with company size. So, only 18% of firms with 1–4 employees face this requirement, but that jumps to 39% for those with 5–9 employees, 57% for those with 10-19 workers, and up to 82% for those with more than 100 employees.

Project owners also often raise man-hour targets for women, minorities or veterans as prerequisites for bidding, and across the board, 25% say they face this requirement. Again, it’s a more common need for larger firms, increasing from 6% among firms with 1–4 employees, up to 56% for those with more than 100 workers.

As we noted in our 2022 report, there’s a disconnect between the percentage of companies that have encountered specialdesignation requirements and those that actually qualify under the requirements. The vast majority (82%) of companies don’t claim or qualify for any of these designations. Two company-size groups—those with 5–9 employees (versus those with 1–4 employees) and 20–99 employees (compared to those with 100+)—are more likely to report they do qualify under one of these designations.

Training priorities

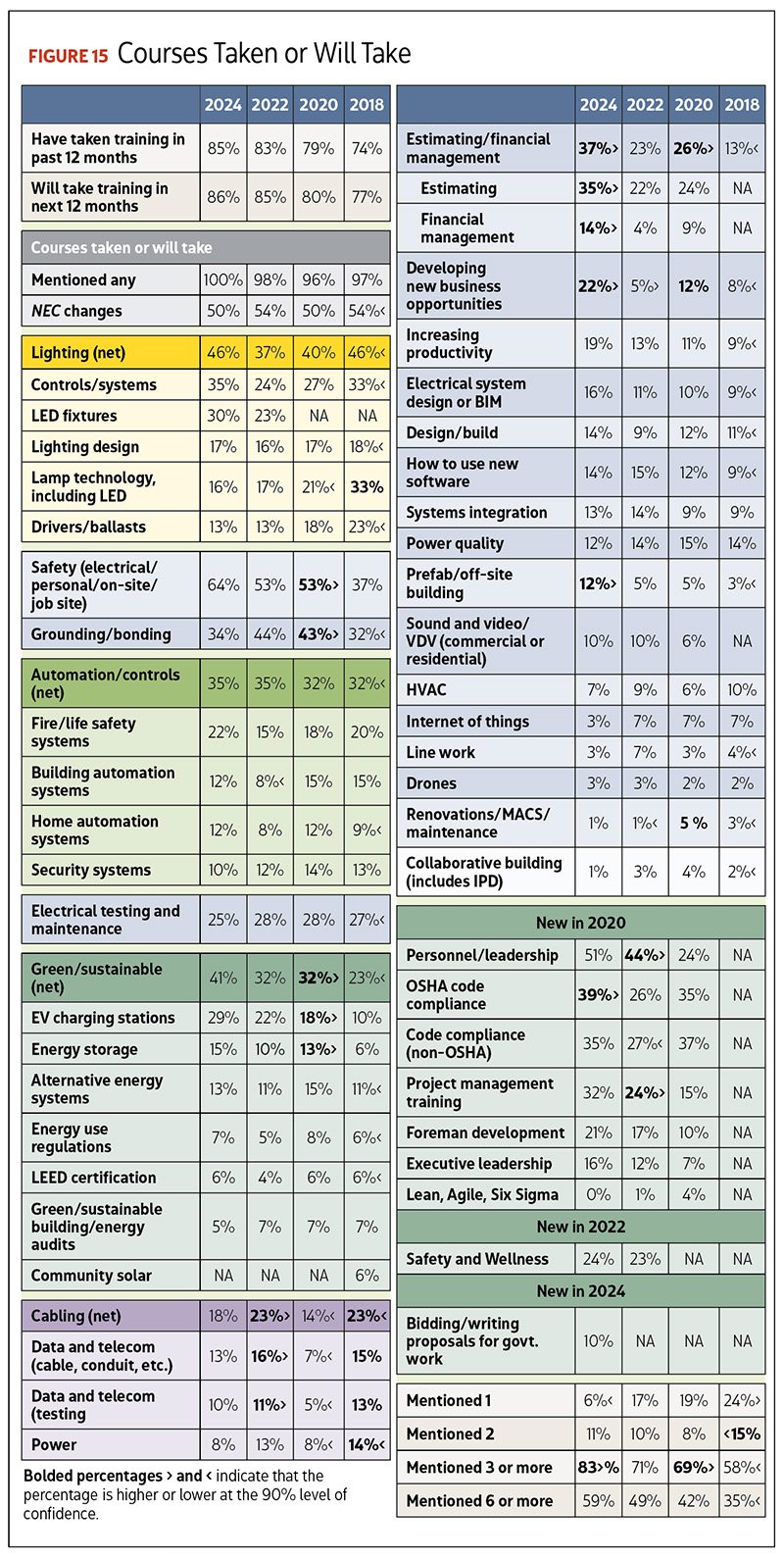

Electrical contracting isn’t a one-and-done profession when it comes to education and training, a fact our respondents know well. About 85% of them said they or someone in their firm had taken a training course in the past 12 months or had plans to take one in the next 12 months for certification or to improve or broaden skills. This training could be online, in classrooms or through correspondence.

In the last survey, with the pandemic era’s rise of video conferencing and online training, we started asking whether training might take a hybrid form, combining online and in-person classwork. As in 2022, about half reported they had already or would be taking hybrid training. And 72% said they think the hybrid approach will continue in the future. Both these figures are essentially unchanged from 2022’s responses.

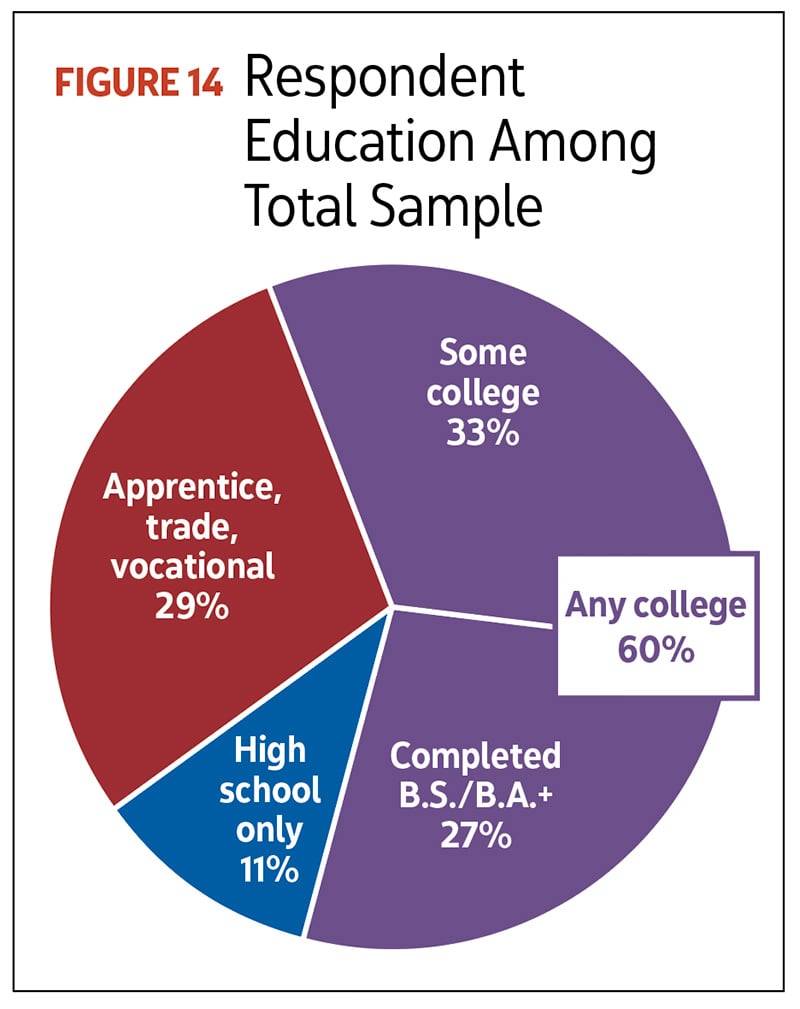

In our last survey, we noted a rise in respondents reporting they had attended college, which remained statistically unchanged this year at 60%. See Figure 14. However, respondents in firms with 10-plus employees are significantly more likely to hold a bachelor’s degree or higher, at 31%, than those in smaller companies, at 23%.

As Figure 15 illustrates, the most popular courses involve safety (electrical/personal/on-site/job site) at 64%, personnel/leadership at 51% and National Electrical Code use or changes at 50%. While interest in most of the individual course topics are statistically unchanged from the 2022 survey, there are some notable exceptions:

- Significantly more electrical contractors are interested in business management topics than technical skills, notably, OSHA compliance (39%), estimating (35%), developing a new business (22%) and financial management (14%).

- Interest in courses related to prefab/off-site building also posted a statistically significant increase to 12%.

Also, there was a strong uptick—to 83%—in ECs saying they had taken or will take three or more training courses, and an impressive 59% mentioned six or more courses (though this figure is statistically unchanged from 2022).

Putting it together

If our last survey showed an industry weathering the challenges presented by the COVID-19 pandemic, this edition sees electrical contractors growing their businesses in size and revenue. Companies are beginning to benefit from an increase in new construction opportunities. It will be interesting to see how these figures might continue to shift over the next two years, as the budding industrial construction boom really kicks into gear.

Still to come

There’s just too much information from our biennial survey to fit into one article, so next month's will cover firms’ business operations, including collaborative versus more traditional bidding formats. We’ll also look at the role ECs play in specifying and substituting the products they install.

Methodology

The survey was conducted exclusively online among subscribers to ELECTRICAL CONTRACTOR magazine. In addition, more than a hundred members of the ELECTRICAL CONTRACTOR Subscriber Research Panel also participated in the survey. The field period for the survey ran from Jan. 24 through March 31, 2024. A total of 828 participants completed the survey in that time.

As in 2022, the 2024 survey was only offered on the internet because of the dwindling participation in previous years through the mailed printed surveys. The online option was introduced in 2004.

We also attracted respondents through the weekly ELECTRICAL CONTRACTOR e-newsletter and with advertisements in the February and March print magazine that included a link to the survey using their subscriber number, which was then authenticated online.

As in 2020 and 2022, the proportion of the total respondents attributable to the print list was so low that weighting the data would distort the total statistics.

Each respondent who received the online survey was sent up to seven follow-up emails. For each completed survey, ELECTRICAL CONTRACTOR contributes $5 to charity, up to a total of $10,000. In addition, the magazine offered a sweepstakes drawing for a chance to win one of ten $150 Amazon gift cards. Panel members were also entitled to be entered into the monthly Panel sweepstakes for completing the Profile survey.

Since 2004, we have produced different versions of the survey. For the 2008 through 2016 Profile studies, there were four versions that had 30 common questions, differing on fewer than 10 questions. Since 2018, there have been seven versions.

This research was conducted by New York-based Renaissance Research & Consulting Inc. (www.renaiss.com), an independent market research firm that specializes in the construction industry.

Statistics

The margin of error on the total sample of 828 is +/- 2.9% for percentages around 50%, (i.e., we are confident that a reported 50% will fall between 53% on the plus side and 47% on the minus side 90% of the time). Please note that different rules apply to testing of averages, which were also tested at the 90% level of confidence and are noted in the report.

A significant difference in the total sample between 2024 with a sample size of 828 and 2022 with a sample size of 843 is at least 4% at the 90% confidence level. Bold text and an arrow in the charts indicate significant difference and the direction of the difference. A (+) or (-) next to the title indicates a significant difference compared to its pair.

stock.adobe.com / 22_monkeyzzz/ Elnur / bonotom studio, Inc.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].