Click here to read the 2022 topline report

Every two years, we reach out to you for our Profile of the Electrical Contractor. The 2022 edition occurs while the third year of supply-chain breakdowns instigated by the COVID-19 pandemic remains unresolved. Capturing a moment in your work life—like a sports trading card—our biennial survey asks you to tell us about your previous year’s business. So this profile covers 2021, a rollercoaster of vaccine-related hopefulness and slipping confidence in the economy compared to 2020, when ECs’ positivity reflected 2019’s boom. In the end, the story turns out to be relatively positive. You're doing OK and can, therefore, put this year’s trading card in your album.

This insight is based on information from 843 readers who responded to our comprehensive survey. Despite this rocky outlook, we found that most firms maintained staff rosters throughout the pandemic’s upheaval. However, there was a modest, yet statistically significant, decrease in the percentage of respondents who said their firms had increased in size over the previous two years, versus 2020. And there was an equally modest, yet statistically notable, increase in the percentage who said their firms had gotten smaller. Also, a trend we saw in 2020 toward larger firm sizes continued: while smaller firms—those with 1–9 employees—remain the majority, their proportion has decreased, while the number of larger firms continues to grow.

Another trend is the move away from standard power and wiring and toward higher-tech and more value-added areas, such as lighting and industrial systems and controls, with electric vehicle charging installations also on the rise. Maintaining and updating skills continues to be a priority for ECs, with about 80% of respondents noting that they or someone else in their firm has taken training in the previous 12 months or will be doing so in the next 12 months, a figure that has held steady since 2020.

But these observations are just highlights from all we learned about your views on the state of electrical construction in 2021. Keep reading for more details. And you can check out the full report online at ecmag.com/profile and ecmag.com/market-research, where we also maintain an archive of past results for easy, over-time comparisons.

Aging trends resume

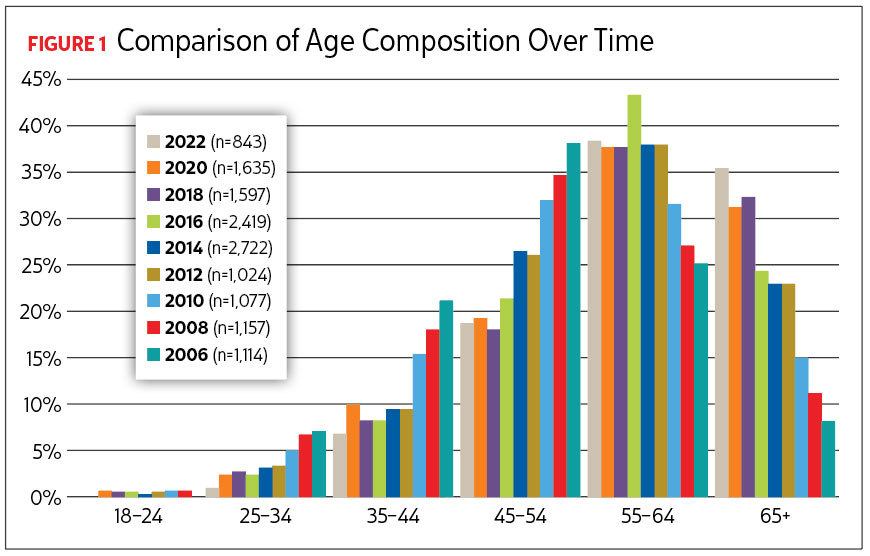

Two years ago, we posited that the trend toward an increasingly older EC workforce had, perhaps, slowed, as 2020’s average figure had remained virtually unchanged from 2018’s results at 57.9 years. Now it seems that result could have been just a pause, with the average of this year’s respondents climbing to 59.3. The shift back to an aging trend can be seen in Figure 1. Two years ago, we noted an increase in the combined 35–54 age ranges over the previous survey’s results. This year, that increase has reversed itself, primarily because of a drop in percentages of those aged 35–44 to 7.1% from 9.8%. And the rise in proportion of those aged 55 and older, to 73% from 68% in 2020, was driven almost entirely by growth in the 65–74 age range, to 29% from 25%. The finding that those working in smaller companies tend to be older held constant in this year’s survey, though average age climbed across all firm sizes.

The percentage of female respondents to the 2022 survey was 4%, statistically unchanged from 2020’s 3% figure. The female electrical contractors interviewed are less likely to work in very small firms (1-4 employees or with revenues of under $250K); they are more likely to be aged 35-54 and/or to be located in the West.

In terms of years of electrical contracting experience—a question we first asked in 2018—we found that respondents had been in the industry an average of 33.9 years, a statistically significant boost from 2020’s 32.4-year figure. And 7% have more than 50 years’ experience, up from 5% previously. Not surprisingly—as was the case in 2020—92% of those with that much experience are older than 65.

The proportion of respondents who are in ownership or top management was approximately 70% in this year’s survey. This is statistically unchanged from 2020’s findings. About 10% carry the master electrician title, or an equivalent, which is a significant drop from 2020’s 14% result. As expected, owners and top managers tend to be older than 65.

Firms continue to grow

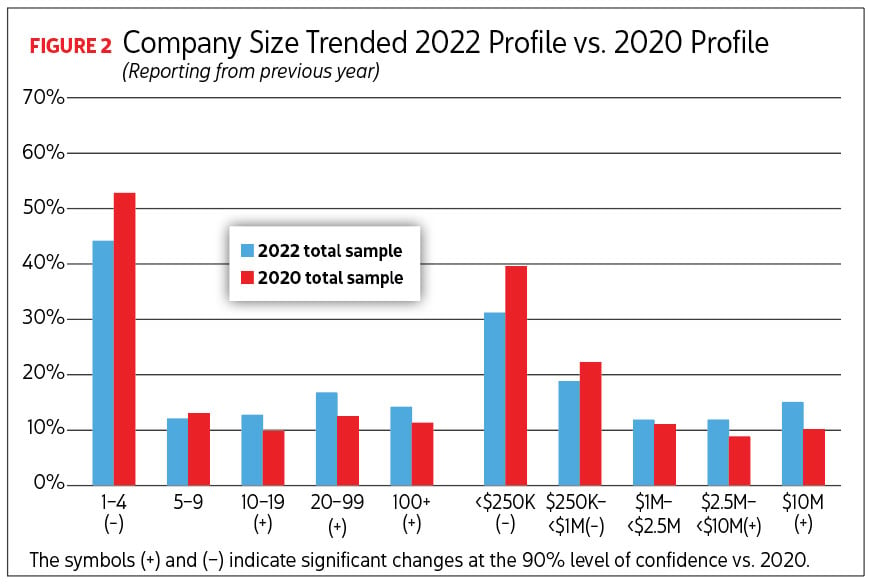

In 2020’s profile, we emphasized a steady decline in smaller firms and a corresponding rise in those with 10-plus employees. That shift has continued, with firm revenues rising along with headcount, as illustrated in Figure 2. Looking back at the state of their business in 2021, 56% of respondents reported 1–9 employees in their firms, down substantially and significantly from the 66% who fell into that category two years ago. And 50% reported revenues of less than $1 million, down from the 62% reported in 2020’s profile. At the other end of the size and revenue scales, 44% now have 10-plus employees, versus 34% two years ago, and 39% of firms now have annual revenue of more than $1 million, compared with 31% in 2020.

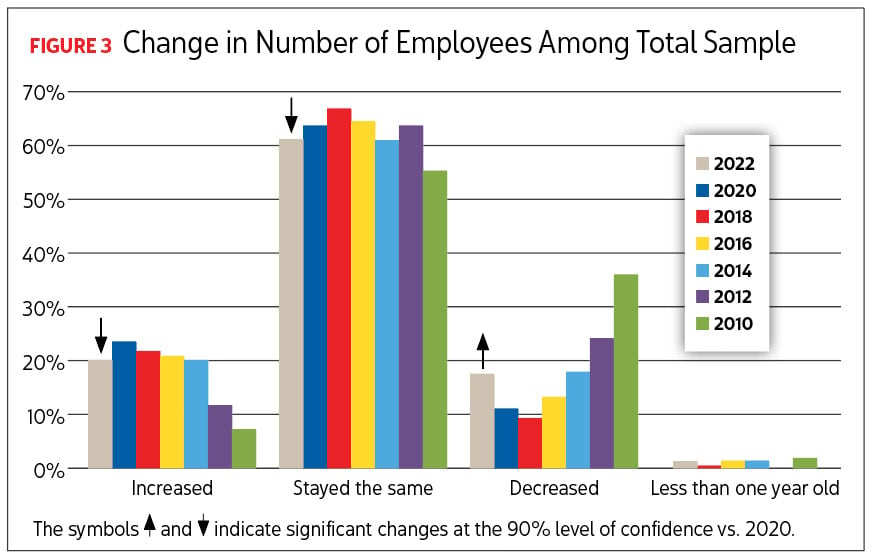

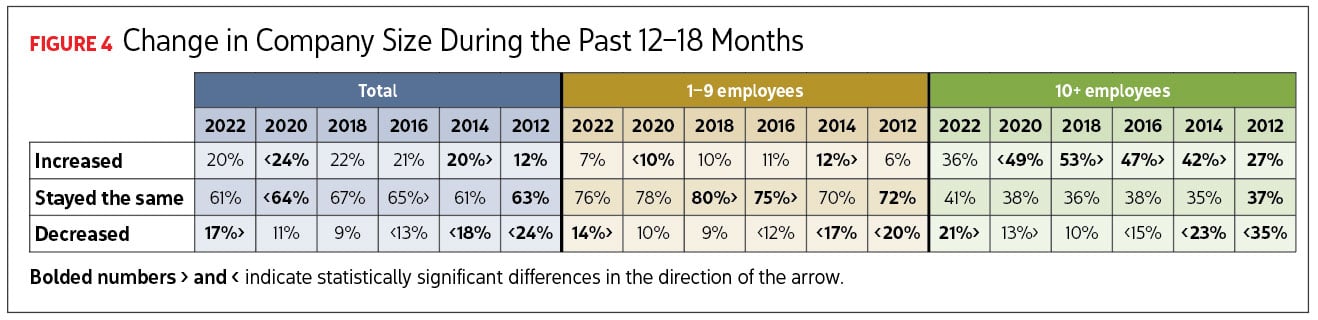

Of course, a big question is what effect COVID-19 might have had on firms’ employee numbers, and the answer seems to be, fortunately, not much. Most firms that participated in the 2022 survey reported their firms’ headcounts had remained stable. As Figure 3 shows, 61% of respondents said their firms’ sizes had stayed the same, with statistically equivalent numbers saying their companies had added or lost employees, at about 20% each.

Diving in deeper to look at how firms of different sizes might have been affected (see Figure 4), there’s a bit of a mixed bag. Fewer firms with 1–9 employees lost people than their larger counterparts, at 14% versus 21%. But larger firms were more likely to continue to grow, with 36% of firms with 10-plus employees gaining staff, compared to 7% of smaller companies.

Staff hiring and retention challenges remain statistically unchanged from two years ago. We asked ECs to consider the job market as it was when they were completing the survey, January through April 15, 2022, and 68% said they were having difficulty finding trained workers. Additionally, 27% said that they had difficulty retaining trained workers. These figures fall in line with those reported in the 2020 survey, over the comparable time frame.

Company income trends also showed a limited COVID-19 impact, as bottom-line figures continued to move upward, with fewer firms reporting revenues under $1 million (50%, versus 62% in 2020) and more reporting $1 million or more (39%, versus 31% in 2020). Of course, these numbers are broad generalizations across the spectrum of EC firms covered in this profile. For context, 67% of firms with 1–4 employees reported less than $250,000 in income, while 57% of companies with more than 100 workers had revenues of more than $25 million.

Confidence concerns

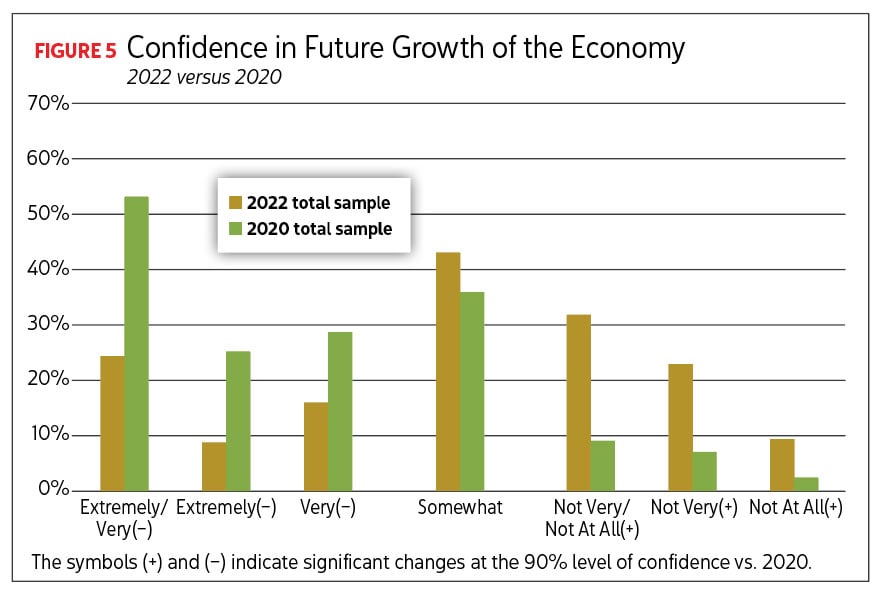

The chaos of the last two years has had a significant impact on the confidence of ECs regarding possible economic growth over the next few years, as you can see in Figure 5. Two years ago, a slight majority (53%) said that they were extremely or very confident. This year’s figure is less than half that, at 25%, and the proportion saying they are “not very or not at all” confident jumped to 32% from 9% in 2020. However, the largest group, 43%, remain “somewhat” confident, a figure that remains statistically unchanged from 2020.

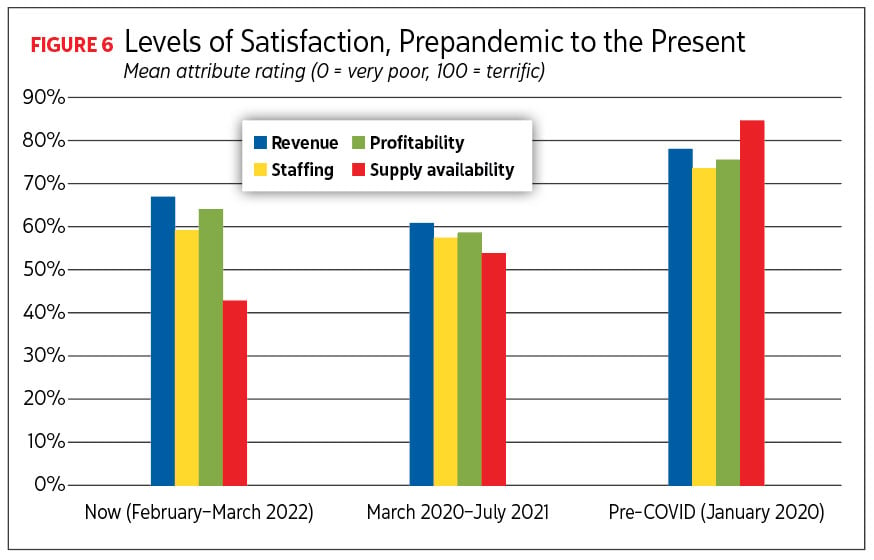

To dig into the impact the pandemic might have had on confidence levels, we asked respondents to report on their levels of satisfaction regarding four specific aspects of their business—revenue, staffing, profitability and supply availability—during three specific periods of time. These included their current state (February to March 2022), during the pandemic’s first year (March 2020 to July 2021) and just before COVID-19’s onset (January 2020). The bar charts in Figure 6 illustrate how those levels shifted. None returned to pre-COVID levels, but revenue and profitability are showing signs of recovering.

Economic constants

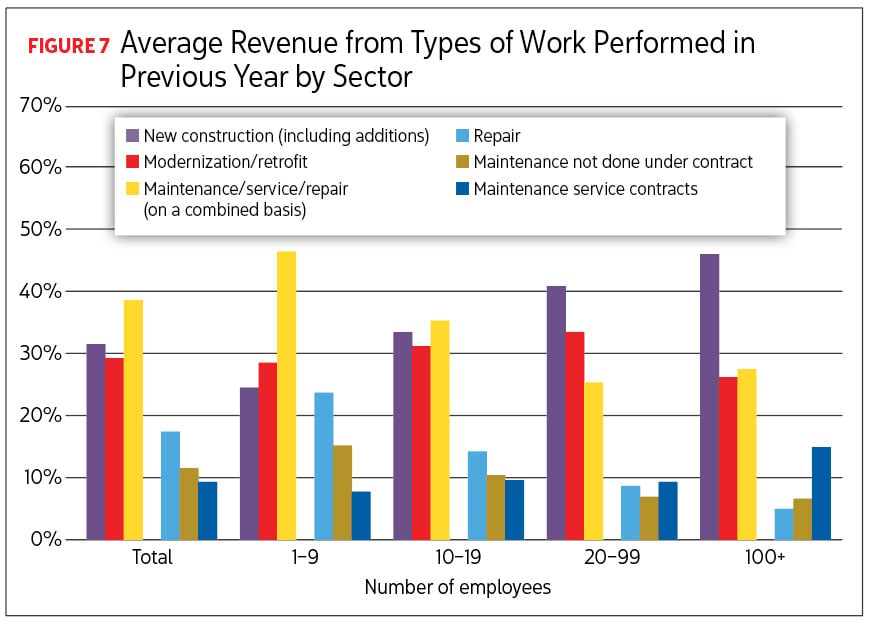

How ECs make their money remained statistically unchanged in this year’s survey, as we asked participants to look back at their 2021 earnings, versus the 2020 Profile’s review of 2019 business (see Figure 7). On average, 39% of their revenue came from maintenance/service or repair, 32% from new construction and 30% from modernization/retrofit. New construction remained low, compared to pre-2008 levels, though it plays a larger role for firms with 10-plus employees, at 40.5%, versus 24.8% for smaller companies. The combined maintenance/service/repair category was proportionally more important for smaller firms, at 46.6%, versus 28.9% for their larger counterparts. Maintenance done on a contract basis, however, was more important to larger companies.

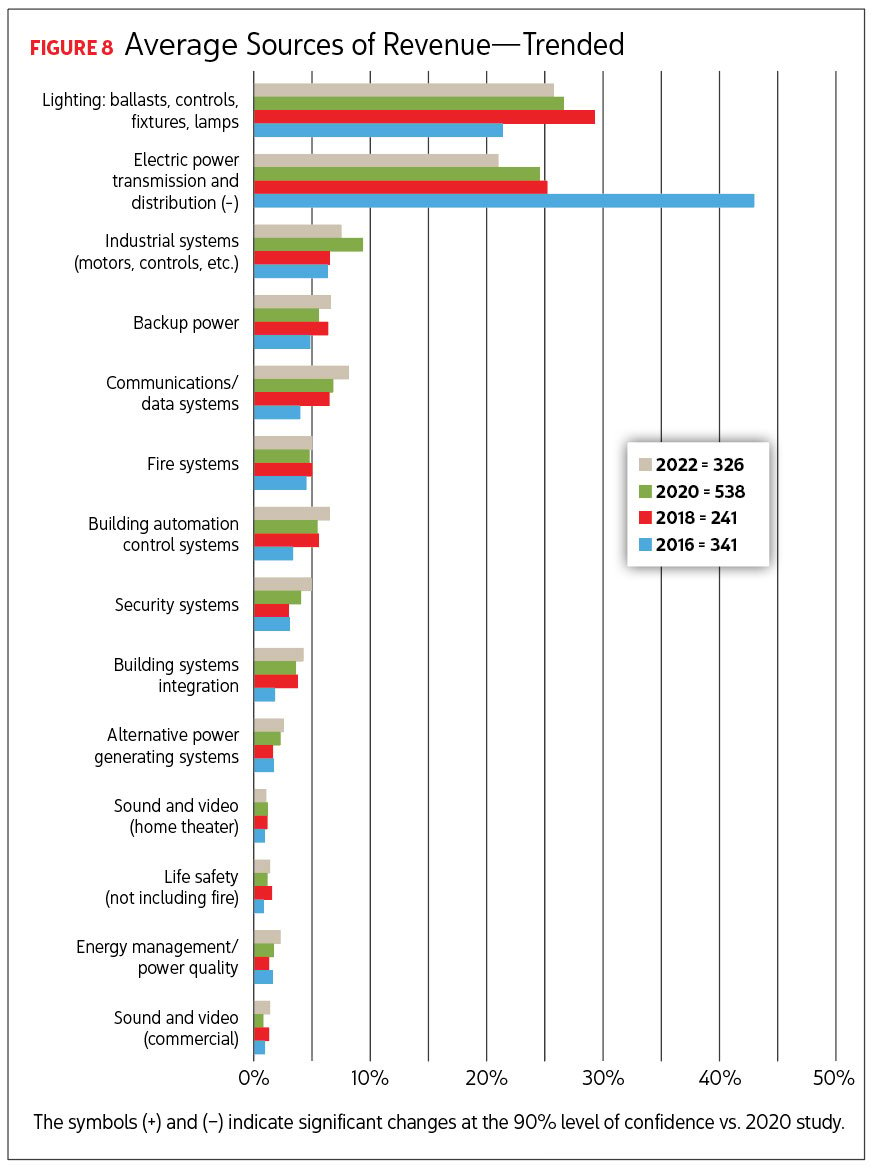

In terms of the various types of projects ECs perform, electric power transmission and distribution continued to shift downward, continuing a trend first noted in our 2018 Profile. As illustrated in Figure 8, this source now accounts for an average of 21.2% of EC firm revenue, down from 24.8% in 2020—and almost 45% in 2016. Lighting remains the top money maker, at a statistically similar level to 2020’s survey.

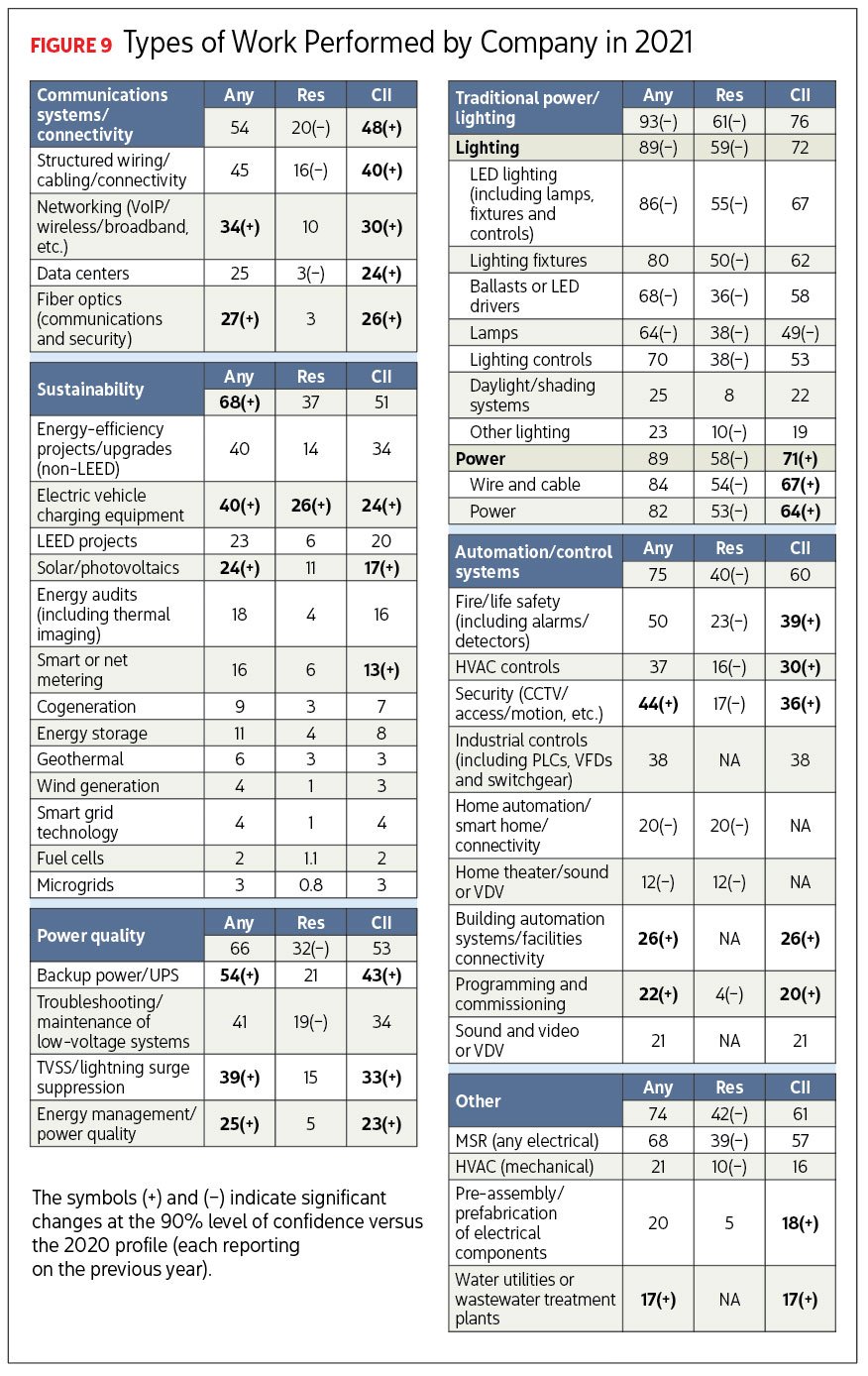

To get more detailed information, we also asked ECs to tell us about their work during 2021 in each of a list of more than 40 different project types in residential and commercial/institutional/industrial (CII) settings. Their responses are shown in Figure 9.

Comparing the combination of residential and CII project types to 2020’s survey results, the traditional power and lighting category fell slightly but not insignificantly, to 93% from 95%, largely due to a drop in lighting work, to 89% from 92%. However, the broad range of sustainability work rose over the last two years, to 68% from 64%. This increase is thanks to more ECs working on EV charging equipment and solar-power projects.

Other notable findings regarding combined residential and CII work completed in 2021, versus 2019, include:

Power quality remains statistically unchanged at a high level, but the subcategories of backup power/uninterruptible power supply systems, TVSS/lightning surge suppression and/or energy management/power quality have grown.

More ECs reported working on network/VoIP/broadband and/or fiber optics than two years ago.

More ECs reported work on water utilities or water treatment plants than two years ago.

In terms of automation and control systems, security, building automation and programing/commissioning were all up, while home automation, home theater/sound and voice/data/video are all down. The latter shift could reflect consumers’ move toward easier wireless offerings coming to market that they can install themselves.

Looking at CII work specifically, only the lamps category showed declines over work completed in 2019. This shift could reflect a combination of the move away from fluorescent lighting, which offered the possibility of regular lamp-replacement contracts, and the possibility that much of the low-hanging fruit of replacing those fluorescent lamps with long-lasting LEDs has been picked. Categories that showed gains included:

Power and its component parts

Communications systems and connectivity, overall and in related subcategories

Sustainability, including solar, EV charging equipment and smart or net metering

Many aspects of automation control and systems

Water utility or treatment plants

Prefabrication of electrical systems

In contrast, almost all the changes in residential construction reflect lower levels of business. This is particularly true in the areas of traditional power and lighting. Residential communications systems, connectivity and automation controls also took a hit—again, this could reflect a move away from residential structured wiring approaches and toward wireless systems homeowners can install themselves.

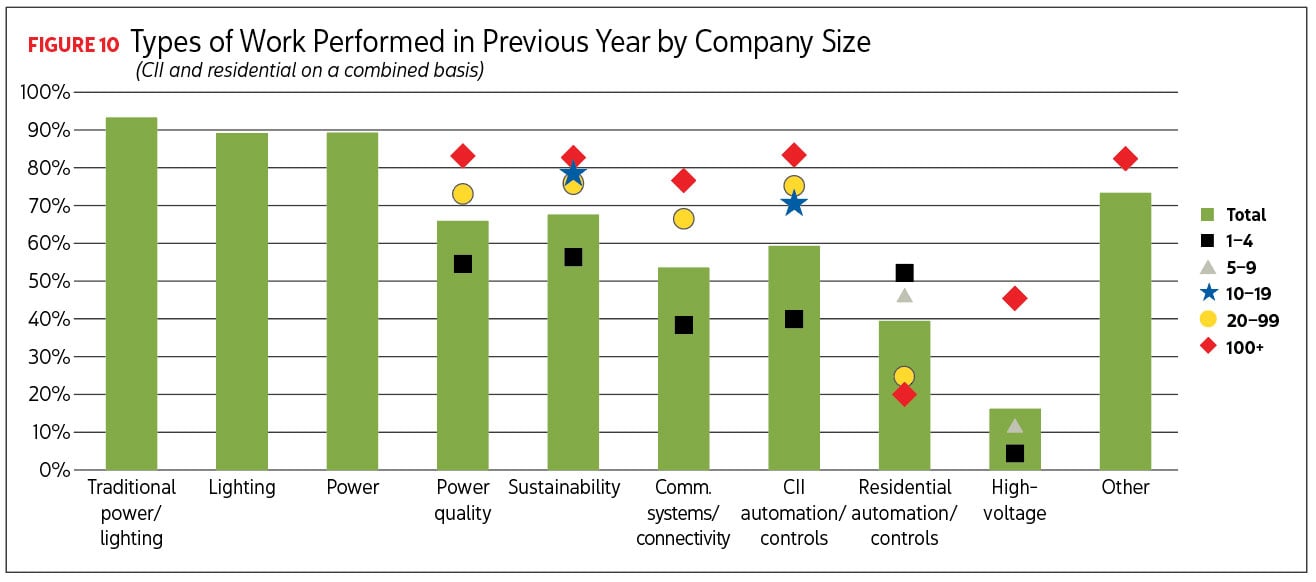

Looking at the types of work done by firms of varying sizes, there are two notable differences from our 2020 Profile. First, there are fewer differences at all by subgroup, and, second, firms with 5–9 employees are no longer more likely to work on the highest number of project types. In the 2020 survey, companies of that size, rather than larger operations, were more likely than average to participate in more of the categories. See Figure 10.

Additionally, high-voltage was added to our list of category types this year. Not surprisingly, firms with 100-plus employees were much more likely than average to participate in these labor-intensive projects, while those at the smallest end of the scale were less likely than average to work on these jobs. However, as has been the case in the past, the smallest firms were more likely than average to work in only one of the categories, residential automation and controls.

As to where ECs work, 40% of firms had projects in more than one state in 2021, up from 36% in 2020’s survey of 2019 work, and continues a trend we’ve observed over the last several surveys. Additionally, the proportions of companies working in 3-plus, 4-plus and 5-plus states also have risen significantly over the last two years.

Little change in low-voltage

Across our total sample, 94% of respondents said their firms did low-voltage work, with 22% noting their firms had a separate low-voltage division, which was unchanged from our 2020 results. As was the case two and four years ago, firms with 10-plus employees were more likely to have a separate division—the 38% figure also was statistically similar to what we heard two years ago. However, as was also the case in 2020, larger firms are no longer more likely to plan to add a low-voltage division in the next 1–2 years, although that was the case in 2016 and 2018. It is possible that the larger firms have already added the divisions they were planning on during the earlier surveys.

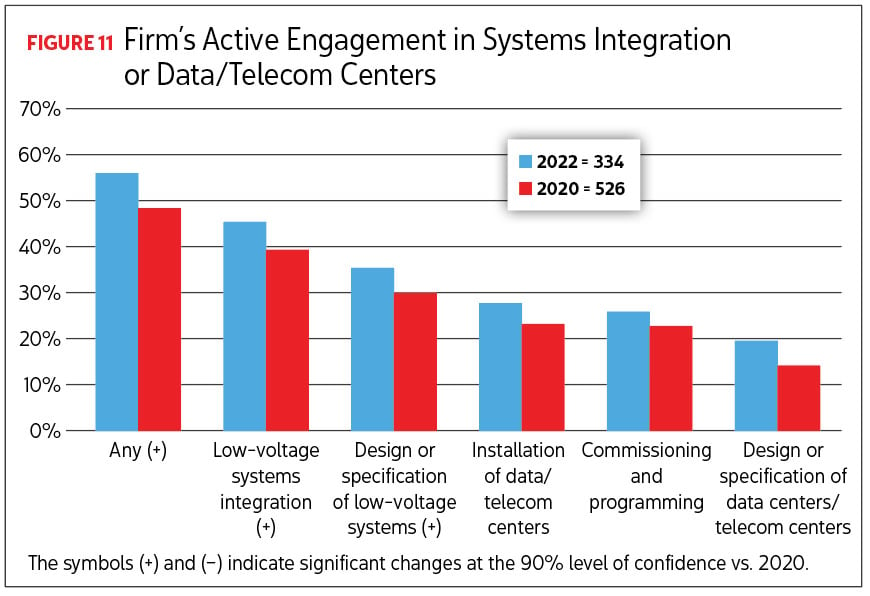

Systems integration and data centers are big targets for companies seeking to boost their low-voltage business, and more than half the ECs we surveyed are actively involved in any such efforts. This is a significant jump from 2020, as you can see in Figure 11. Specific increases were also noted in low-voltage systems integration, up to 46% from 40% in 2020, and design or specification of low-voltage systems, up to 36% from 29%.

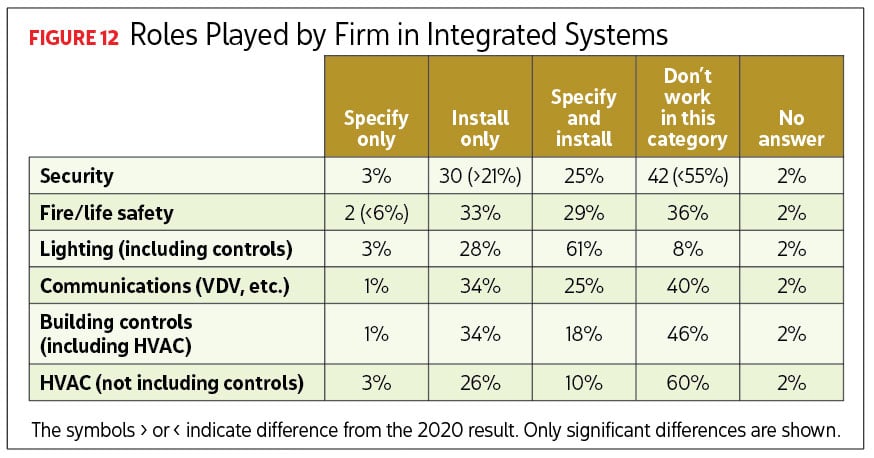

In terms of integrated systems projects, 61% of ECs said they specify and install lighting, about double the percentage of those reporting they only did installation work. As we noted in the 2020 Profile, this makes sense, given lighting’s overall role in ECs’ businesses. Figure 12 also illustrates a couple of statistically significant changes from 2020’s responses: more EC firms now perform security installation work, and fewer firms only specify fire/life safety systems. For most other integrated systems, about 20%–25% of respondents said their firms specified and installed related products. The exception remains HVAC (not including controls), where that figure falls to 10%.

What projects pay the bills?

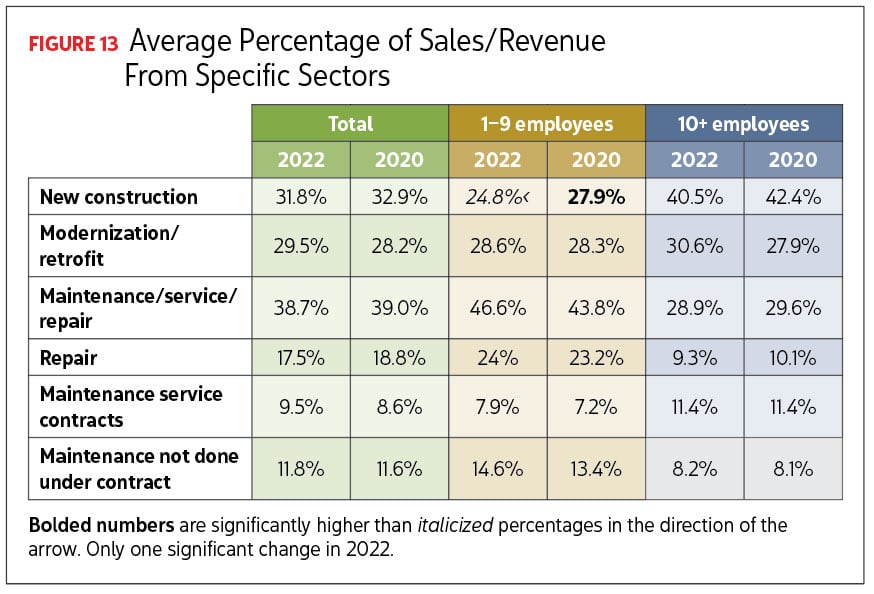

On average across all firm sizes, 39% of ECs’ 2021 revenue came from maintenance/service or repair, which is statistically unchanged from the 2019 results we covered in the 2020 Profile. Revenues from new construction (32%) and modernization/retrofit (30%) also remained statistically similar. See Figure 13.

Of course, average figures can differ substantially when broken down by company size. As has been the case in previous Profiles, we found new construction plays a proportionally larger role for firms with 20-plus employees than for smaller organizations, as do maintenance/service contracts. Headcount relates to business concentrations. These results remained statistically unchanged from 2020’s Profile, with one exception: the average percentage of revenue from new construction declined among firms with 1–9 employees.

Taking a different cut at revenue data, this time by building type, we found that CII and nonbuilding projects rose significantly in 2021 compared to 2019—at 55.1%, versus 50.9% two years earlier. Also, residential construction posted a significant decline, falling to 36.1%, versus 41.8% in 2019. Industrial-related revenues increased across all firm sizes, to 16.7% from 13.6%, as well as among firms with 5–9 employees and those with 100-plus employees. Nonbuilding work also rose for companies with 5–9 employees to 9.5% from 6.1%, and utility work jumped up to 6.7% from 3.2% (not shown).

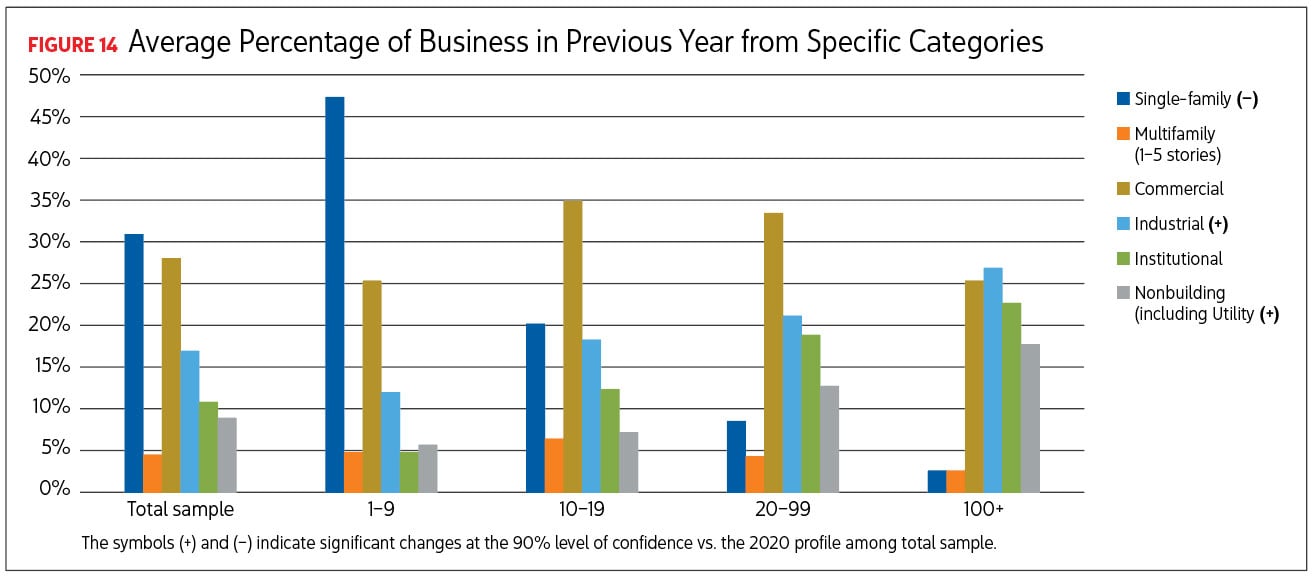

Looking at the major building types by categories of work in Figure 14, we see that single-family housing remained responsible for a high percentage of revenue across the total sample at just over 30% in 2021. But this figure rises to almost 50% for those firms with 1–9 employees. Other observations include:

Companies with 10–99 employees derived the largest percentage of their revenue from commercial projects.

Firms with 10-plus employees derived a disproportionate percentage of their revenue from industrial work (this was even more the case in companies with 20-plus employees) or institutional work (this was highest for firms with 100-plus employees).

Firms with 20-plus employees also received a disproportionate percentage of revenue from utility/nonbuilding work, and that percentage rose even higher for 100-plus employee companies.

Bidding requirements

For the second time, we polled ECs about whether they might have faced requirements to have a prequalified standards and safety program in place to bid on a project, and 48% of all respondents said they had faced this need. However, as was the case in 2020, this burden becomes more pronounced as firm size increases. So, for example, only 24% of those in firms with 1–4 employees had encountered this requirement, compared to around 51%–57% of firms with 5–9 or 10–19 employees and 76% of those with 20-plus employees. Regardless, 63% of respondents say their companies have such a program in place or plan on instituting one this year, up from 59% in 2020.

Man-hour requirements for women, minorities and veterans are another standard firms can face in their bidding efforts and, across the entire sample, about one in five say they’ve seen this need. Again, this falls more heavily on larger firms and increases significantly and steadily from 8% among firms with 1–4 employees to about 50% for firms with 100-plus employees.

However, there appears to be a shortfall between the percentage of companies required to meet man-hour minimums and those reporting such designations, with 83% not claiming or qualifying as minority-, women- or disabled veteran-owned businesses, or as being in a HUBZone location. Interestingly, two company sizes—those with 5–9 and 20–99 employees—are significantly more likely to report their qualification under one or more of these designations, at 25% versus firms with 1–4 employees and 22% versus firms with 100-plus employees, respectively.

Getting a good education

Keeping current on electrical and business practices remains important to the ECs we surveyed, with about 80% noting that they or someone in their firm has taken training in the previous 12 months or plans to do so in the next 12 months, either to broaden skills or for certification. The training could be through online, correspondence or in-person classroom approaches. These figures remained statistically unchanged from our 2020 Profile.

Because of the way the pandemic reshaped training programs, we asked about the role a hybrid combination of online and in-person structures might play in training they’ve taken or plan to take. About half said they have taken or will take hybrid classes, and 70% said such an approach would continue into the future.

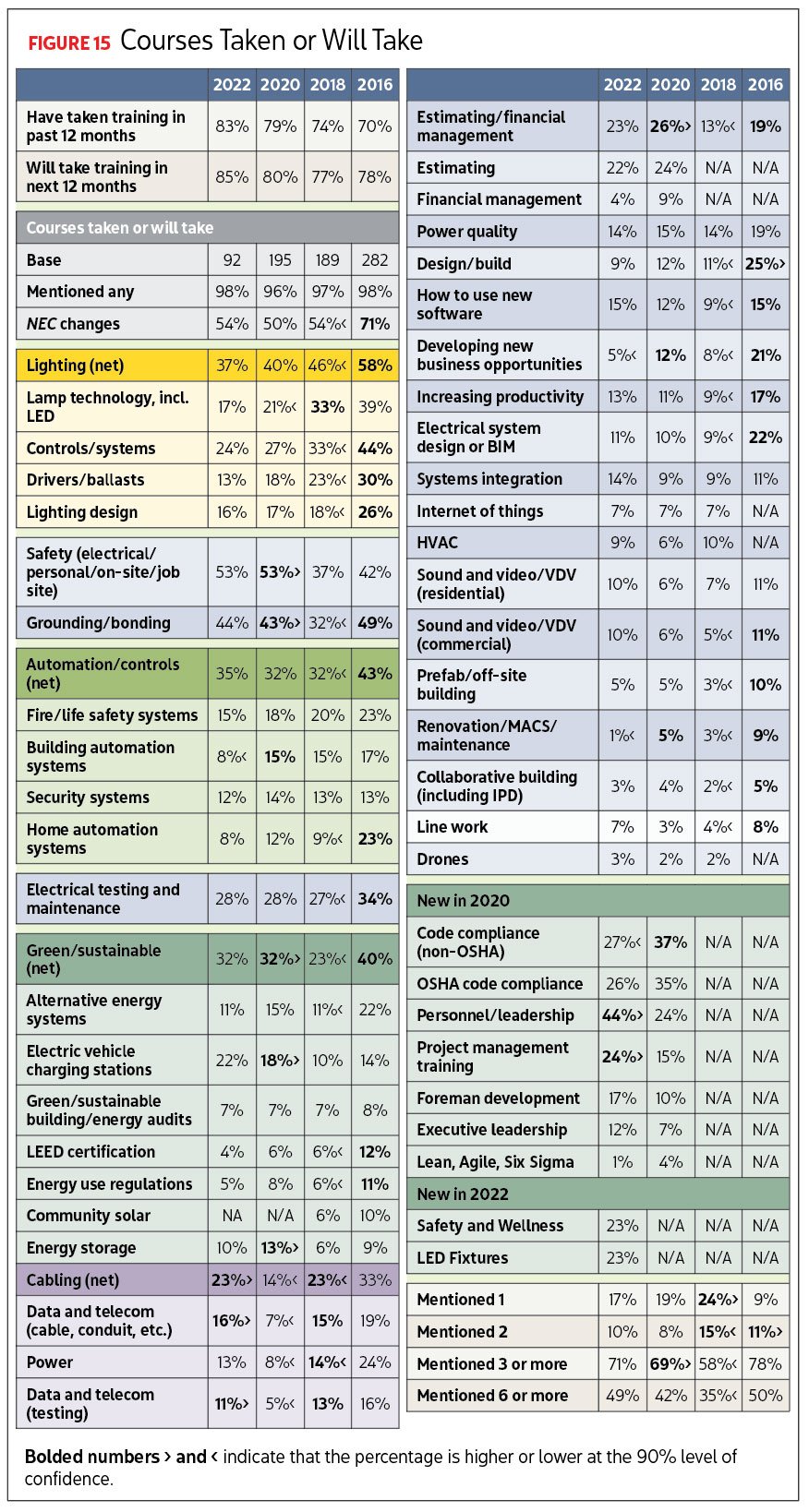

Interest in most of the individual training topics we asked about remained statistically unchanged compared to two years ago—you can see the details in Figure 15. National Electrical Code changes and safety basically tied at the top of the list. However significantly more ECs said they were interested in personnel/leadership (44%), project management (24%) and cabling (23%) courses.

Interestingly, when asked about their highest level of education, substantially more respondents have at least attended college compared with two years ago (60.1% versus 56.5%) and correspondingly fewer have not attended college (37.5% versus 43.3%). Within this, the percentage that have attended trade or vocational school declined (27% compared with 31% two years ago).

Leisure pursuits

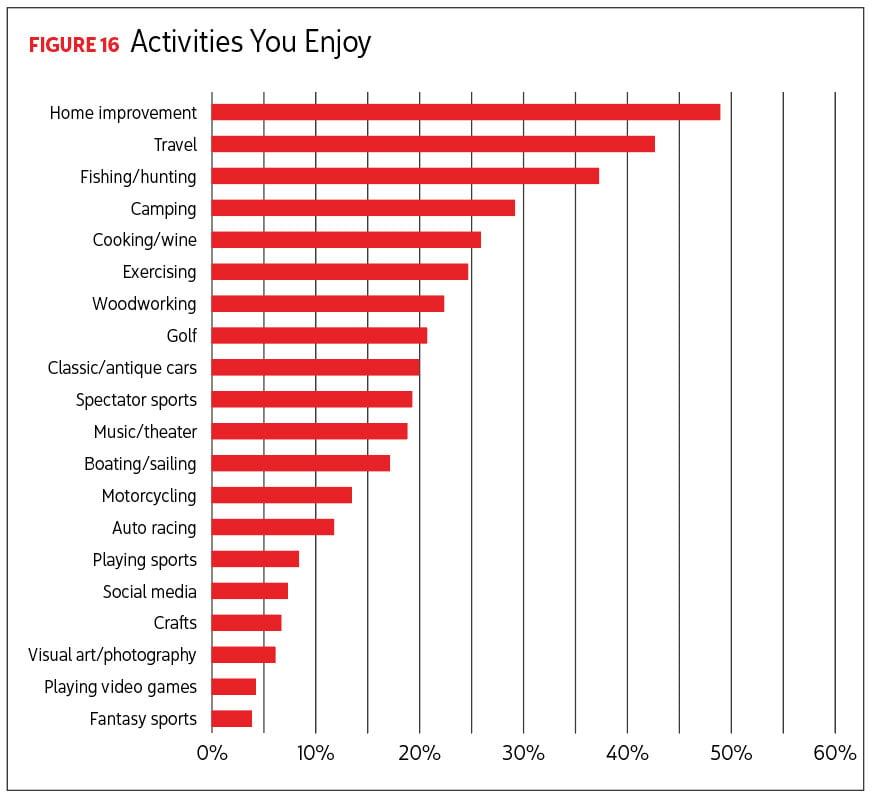

Returning to this year’s survey, we decided we wanted to learn a little more about what ECs enjoyed doing when they weren’t working or in training. One surprise: it appears that many of you just can’t get enough of working with your hands, as home improvement took the top spot at 49% among the list of activities we inquired about. Travel (43%) and outdoorsy pursuits such as hunting and fishing (37%) and camping (28%) were also among the more-popular activities. See Figure 16.

Summing things up

Like the 2020 Profile, this 2022 edition comes at an unusual time for the larger construction industry. During the last survey, many activities were going into lockdown, with a lot of insecurity regarding what the immediate future would bring. We’re releasing this 2022 Profile as life is beginning to look a bit more normal. With what the world has been through in the last few years, it’s interesting to note how similar responses have been between these two most recent survey efforts.

Still to come

But wait, there’s more! We couldn’t fit all our findings regarding ECs and their work into a single article, so we’ll continue next month. Part 2 will cover ECs’ business operations, including collaborative versus more traditional bidding formats. We’ll also take a look at the role ECs play in specifying and substituting the products they install.

Methodology

The survey was conducted exclusively online among subscribers to ELECTRICAL CONTRACTOR magazine. In addition, in 2022, as in 2020 and 2018, 136 members of the ELECTRICAL CONTRACTOR Subscriber Research Panel also participated in the survey.

The field period for the survey began on Jan. 26, 2022, and ran through April 15, 2022. A total of 843 participants completed the survey in that time.

As postal mail participation dwindled (also called the “print” sample, since subscribers received their printed survey by postal mail), the survey was only offered on the internet for the first time in 2022. The online option was introduced in 2004.

Because we were not able to invite those on the “print” list through emails, we attempted to attract them to participate through a magazine cover tip, which is essentially a second cover to draw special attention to an advertisement or other information. All subscribers received cover tips in January.

Since there was no print sample, the data was not weighted, same as 2020. The proportion of the total attributable to the print list was so low, weighting would distort the total statistics.

Each respondent who received the survey through the internet was sent up to seven follow-up emails. An incentive was offered for participation in the survey: For each completed survey, ELECTRICAL CONTRACTOR would contribute $5 to charity, up to a total of $10,000. In addition, as was the case since 2018, the magazine also offered a sweepstakes drawing for a chance to win one of 10 $150 Amazon gift cards. In 2018 and 2020, the drawing was for one of five $150 Amazon gift cards.

As has been the case since 2004, the survey was produced in different versions. For the 2008 through 2016 Profile studies, there were four versions of the survey, which differed from each other on fewer than 10 questions. The first 30 questions were common to all versions. Since 2018, there have been seven versions.

This research was conducted by New York-based Renaissance Research & Consulting Inc. (www.renaiss.com), an independent marketing research firm that has, as one of its specialties, market research for the construction industry.

Statistics

The margin of error on the total sample of 843 is +/– 2.8% for percentages around 50%, (i.e., we are confident that a reported 50% will fall between 53% on the plus side and 47% on the minus side 90% of the time). Please note that different rules apply to testing of averages, which were also tested at the 90% level of confidence and are noted in the report.

A significant difference in the total sample between 2022 with a sample size of 843, and 2020, where the sample size was 1,635, is at least 1.7% at the 90% confidence level.

Bold text and an arrow in the charts indicate significant difference and the direction of the difference. A (+) or (-) next to the title indicates a significant difference compared to its pair.

Header image by Shutterstock / iadams / primopiano / stock.adobe.com / Fand / koson_thamai.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].