You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

Electrical contractors generally use net profit levels as the primary measurement of their success, but cash is the lifeblood of daily operations. Even profitable companies can fail without a healthy cash flow. Working capital management (WCM) ensures a steady supply of cash to keep your company functioning and profiting.

Working capital is a primary measurement of your company’s liquidity, efficiency and general financial health. It is simple to calculate from your balance sheet: “current assets” minus “current liabilities” equals “working capital.” This is based on the assumption that your company would be able to quickly liquidate current assets at any time to pay its current liabilities.

Current assets include cash, plus accounts receivable and inventory, which can be liquidated (converted into cash) within a year. Current liabilities include accounts payable and any debt payments due within a year. For a cash business, there is no lag time between the sale and the payment. For the electrical contractor, the timing differences can be critical in managing your working capital and maintaining the cash flow needed to stay financially healthy. WCM includes ongoing, diligent oversight of purchases, collections and inventory levels.

Is it necessary to maintain positive working capital? Not always, and a negative working capital model has been used successfully by companies in industries such as telecommunications. Although a decrease in working capital may be interpreted as a sign that the company is overleveraged (carries too much debt) or has failed to efficiently manage collections or pay its bills, not all investors automatically consider this to be the case. For example, you may choose to pay a vendor early to receive favorable terms or a cash discount, and you may effectively finance your portion of the work on a new project for several months before you are able to invoice and collect the first payment. These temporary fluctuations in working capital are expected and tolerable.

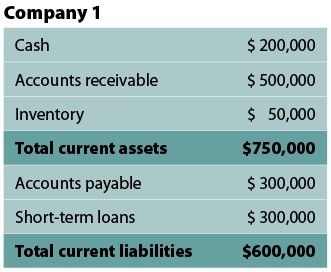

WCM is a long-term strategy to smooth out cash flow and create stability over time. The specific line items of current assets and current liabilities affect your ability to meet payment obligations. Here are two examples of how timing can complicate WCM.

This company has positive working capital of $150,000 ($750,000 – $600,000) but only $200,000 in cash. What if it doesn’t collect $200,000 of the receivables at all and the other $300,000 isn’t paid for another two months? It still has $200,000 in cash, but what if a $200,000 loan payment is due within 30 days and $200,000 of the payables are also due within the next month? That leaves a $200,000 shortfall, without even considering cash needed for payrolls or other small cash purchases.

Compare that situation with this one:

In this case, the company shows a company shows a negative working capital ($500,000 – $700,000 = –$200,000), so it might be unable to meet its short-term obligations. However, all the receivables are actually collected within the next 30 days, while only $100,000 of the payables and $50,000 in loan payments are due during that same month. The cash amount would rise to $400,000, the company would easily be able to pay the $150,000 due to vendors and lenders, and there would be no negative effect on cash flow.

The timing of receivables, payables and loan payments is critical, and so is the management of the individual line items. You must maintain enough cash to cover payroll and fund daily operations, and you must create a company-wide awareness of cash-flow management.

Accounts receivable management depends on accurate and current cost information from the field, prompt invoicing, and a consistent and effective collection process. Inventory levels will vary with individual project requirements, reliability of supplies and optimal levels of parts to support maintenance contracts and emergency work. Accounts payable management requires consolidating all purchasing to obtain the best pricing and terms, and it requires strong relationships that allow for occasional time extensions or vendor financing to cover cash-flow shortfalls.

Debt structuring also is important to ensure that assets are financed appropriately. Lines of credit fund short-term needs, while each fixed asset is funded by a loan with a term that closely matches its predicted useful life. Each year, a portion of multiyear loans and mortgages becomes part of current liabilities and becomes part of the working capital calculation.

Next month, we’ll look at other issues related to effective WCM.

About The Author

Denise Norberg-Johnson is a former subcontractor and past president of two national construction associations. She may be reached at [email protected].