You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

“The [act] is the legislative vehicle for provisions promoting advanced metering in the federal government; a greater focus at the Department of Energy on deployment of existing manufacturing technologies; improved energy efficiency within federal facilities; and a study on barriers to industrial deployment of electric motors, demand response, and combined heat and power technologies,” according to a release from the National Electrical Manufacturers Association (NEMA), which endorsed the bill.

“There are huge gains in industrial energy efficiency that we are leaving on the table by not addressing the inefficiencies in many manufacturing and industrial processes,” said Paul Hamilton, chair of the Industrial Energy Efficiency Coalition (IEEC). “Policies such as this are helping to understand and tackle these industrial energy-efficiency opportunities.”

Energy-intensive manufacturers have long been aware of the cost of inefficient energy use and have made major investments in sensors, controls and automation to reduce their energy costs.

The bill also compels certain federal facilities to publish energy and water consumption data on an individual facility basis and ensures certain technical corrections to lighting efficiency and electric motor provisions in the Energy Independence and Security Act of 2007.

“The challenge now is to drive awareness and deployment of these energy-efficiency opportunities across the entire manufacturing sector, especially into the less energy intensive sites, which represents some 150,000 facilities across the United States,” said Bruce Quinn, a founding member of the IEEC. “We also need to make sure future policies support the continued positive investment environment for industrial efficiency.”

Founding IEEC members ABB, Eaton Corp., GE, Rockwell Automation, Schneider Electric and Siemens are promoting policies that give proper attention to the efficiency gains that automation can contribute to any manufacturing facility or other industrial process.

North America Leads the World in New Smart EnergyOne recent study provides some reassurance that, in the global competition for the installation and use of renewable power, the United States and neighboring countries still hold the advantage in one very important measure.

According to Pike Research, North America leads the world in the addition of new smart energy capacity. The Boulder, Colo.-based company projects this trend to continue for the next three years.

The clean-tech market research firm’s study projects North America to add more than 400,000 megawatts (MW) of renewable capacity from 2012 through 2015, making it the leading region in the world for new renewable energy.

Pike’s measure of renewable power covers the standard wide net of sources, including hydro, biomass, waste, geothermal, wind and solar. Pike notes that renewable power makes up 10 percent of total electricity production in the United States.

The study also emphasizes that, while North America relies heavily on biofuel and biopower for its smart energy revenue and new installations, the potential for growth in other industries could lead to even stronger and more sustainable growth within the sector.

Pike also credits U.S. government policies for contributing to the trend. It points out that state governments are pushing utilities to purchase more renewable energy, through renewable portfolio standards and other similar policies, all of which stimulate the renewable market, albeit artificially.

—Rick Laezman

New Jersey Sandy Restoration Largest in U.S. HistoryPSE&G brought in 1,000 out-of-state line workers and tree trimmers in preparation for the storm. That number grew to more than 4,000. In the first three days, PSE&G restored service to more than 1 million customers.

This was an unprecedented storm that caused an unusually difficult restoration, mainly because of its enormous size and power: It was twice the size of 2011’s Hurricane Irene with widespread impact over 900 square miles and incredibly strong winds reaching up to 90 mph.

When the storm hit on Oct. 29, 2012, PSE&G lost more than one-third of its transmission circuits and half of its subtransmission circuits. More than three-quarters of its distribution circuits were interrupted. The nor’easter put temporary repairs at risk.

Sandy caused twice the number of outages as Irene, which until Sandy, had the distinction of being the worst storm in PSE&G history. Sandy also caused almost three times the number of outages than an October 2011 snowstorm.

Among all the record setting, 48,000 trees were removed or trimmed, compared to 22,500 after Irene. PSE&G replaced or repaired more than 2,400 utility poles, almost three times the number replaced after the last two storms. Thanks to prestorm preparation, PSE&G did not run out of equipment to restore service.

The storm surge affected a number of switching stations and substations located along the Hudson, Hackensack and Passaic rivers as well as two switching stations located along the Arthur Kill, a saltwater channel that separates New Jersey and Staten Island, N.Y. A 4-to-8-foot-high wall of water flooded these locations, damaging equipment. Some stations had never been inundated with water damage in the 50 to 75 years that they existed. Work to restore those stations required painstaking, labor-intensive drying and cleaning of equipment to get them back in service.

Sandy and storms like it have defined a new norm for PSE&G and other Mid-Atlantic utilities. They are now in the process of studying what happened and what they can do better to prepare and respond to future storms. A major issue for all New Jersey utilities was that they can only monitor outages down to the circuit level and not to the customer’s meter. This caused great confusion in detecting individual outages. PSE&G is currently looking into smart meter technology to help solve the problem.

Microsoft Test-Markets Sludge PowerPlenty of media stories cover companies, such as Google, that have gone from tech giant to renewable developer. As data centers become ubiquitous, the convergence of these two industries will continue, and now, Microsoft has taken the plunge, in an innovative, if not entirely odor-free approach.

Danbury, Conn.-based fuel cell developer, FuelCell Energy Inc. announced in November that it will partner with the software titan on a demonstration project in Wyoming. The project will feature a stationary fuel cell power plant that will support a Microsoft data center research project.

The power plant will use renewable biogas generated by a wastewater treatment facility as the fuel source to generate power for Microsoft’s Data Plant project in the city of Cheyenne. It will be a test project designed to evaluate the effectiveness of using fuel cell plants powered by on-site biogas for future data centers.

Microsoft announced in May 2012 that it had made a commitment to become carbon-neutral beginning in 2013. Reliable on-site power generation could be a key element of achieving that goal. The need to power data centers is a growing concern for companies such as Microsoft as the demand for cloud services expands. Microsoft claims its data centers support more than 1 billion customers and 20 million businesses worldwide.

The fuel cell plant will provide 200 kilowatts of power for the data center. It will be installed at the Dry Creek Water Reclamation Facility and is due for completion by spring 2013.

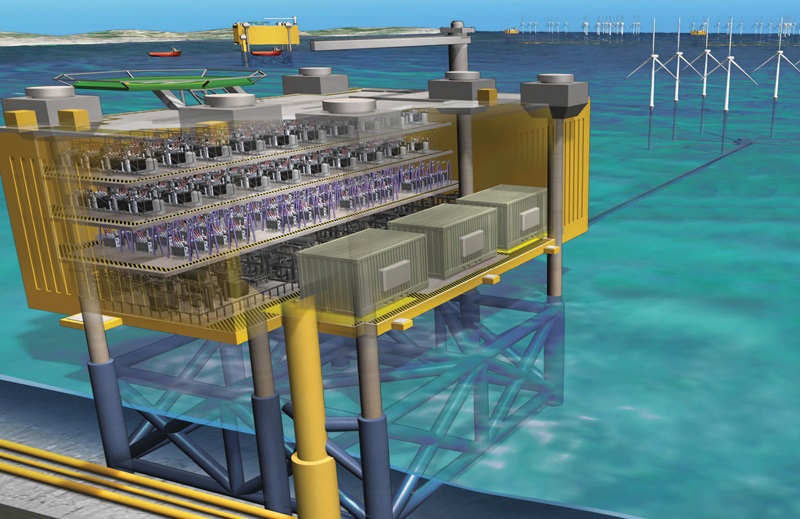

Massive Offshore Wind-Transmission Project Planned for Mid-Atlantic StatesThe project, appropriately named the Atlantic Wind Connection (AWC), is premised on the anticipation of a coming boom in offshore wind-power generation and the need to transmit that power back to land. The project’s backers feel strongly, and perhaps not unwisely, that if a backbone transmission project is installed first, it will both encourage and benefit from the subsequent development of the power it is designed to transmit.

The AWC’s self-fulfilling vision rests on some compelling figures for support. It is designed to service Virginia, Maryland, Delaware and New Jersey, representing a region that is said to offer more than 60,000 megawatts (MW) of offshore wind-development potential. The project itself, whose principal backers include Internet giant Google, will be able to connect up to 7,000 MW of that offshore wind, enough power to serve approximately 1.9 million households.

The project is moving its way through the regulatory process, receiving an important declaration of no competitive interest from the U.S. Department of the Interior in May. More recently, the project touted a new study that underscored its potential as a boon for jobs in the region.

The study, which was prepared by IHS Inc., a Colorado-based global information company, asserts that 7,700 MW of offshore wind in the Mid-Atlantic linked by the Atlantic Wind Connection would create more than 170,000 jobs. Of the total jobs created, 70,000 will be in the manufacturing sector, another 40,000 in the business supply chain, and an additional 50,000 in general by the effect of added economic activity.

Wind Power Hits Peak in the MidwestA recent measure made it clear that wind power has arrived. The Midwest Independent System Operator (MISO) announced that wind power had reached a peak by surpassing 10,000 megawatts (MW). Specifically, the output from wind reached a peak of 10,012 MW overnight on Nov. 23, 2012.

The peak represents a steady growth trend in wind power for the region, reflecting the region’s investment in the industry over a six-year period. MISO, the regional grid operator for 11 states and the Canadian province of Manitoba, first started integrating wind power into its market operations in 2006. The region enjoyed a little more than 1,000 MW of capacity at the end of that year. Wind power has expanded steadily since then, reaching a total generating capacity of nearly 12,500 MW as of September 2012. MISO reports that another 7,000 MW of projects are currently advancing through various stages of interconnection.

The 10,000 MW peak also represents a milestone for the region by various other measures. For example, MISO reports that the Nov. 23 output from wind accounted for more than 25 percent of the total generation output being used at the time. By comparison, that would exceed the total renewable-energy portfolio standard of many states.

At 12,500 MW, the total wind-generating capacity accounts for about 9.5 percent of MISO’s total market generating capacity of 132,313 MW. Wind is also by far the largest source of renewable power for the region. Generating capacity for all renewables is 14 percent for the region. By contrast, coal represents 48 percent of the region’s total generating capacity, while gas and oil represent a combined 32 percent.

Initiative to Bring New Energy-Efficient Technologies into New YorkThe Energy Efficiency Market Acceleration Program (EE-MAP) is spearheaded by the New York Power Authority (NYPA). The program will fund research, market-development activities and demonstration projects to help leverage investments and promote business-development opportunities for emerging energy-efficiency technologies. In July 2012, the NYPA Board of Trustees authorized $30 million for the EE-MAP initiative.

EE-MAP focuses on accelerating the market development of energy-efficiency technologies by doing the following:

• Helping to accelerate their deployment

• Attracting technology companies to New York

• Creating and facilitating market channels for energy-efficiency technology companies

• Assisting in the forming of strategic alliances and business-development opportunities for technology companies

• Training engineers, contractors and maintenance service providers in designing and installing energy-efficiency products

In addition, EE-MAP assists with developing energy-efficiency master planning programs and efforts to create new energy-efficiency markets in coordination with state agencies, authorities and electric utilities to improve industry access to investments made at public facilities.

To implement the initiative, NYPA issued a request for proposals (RFP). Once selected, the RFP awardee will identify commercial but-not-yet-widely deployed clean-energy products with significant promise for gaining market share and providing economic development benefits for New York. Each product will be evaluated according to a market readiness and risk profile.

Through EE-MAP, the RFP awardee will create market-development plans, including strategic alliances, business-development opportunities and training programs. This will provide a blueprint to enable engineers to design, install and maintain the new energy-efficiency products and provide technical support and performance evaluation.

“This public-private partnership will help bring innovative green technologies into the marketplace, helping spur economic investment in the clean-energy sector and protect our environment, while maintaining New York’s position as a leader in sustainability,” Cuomo said. “By supporting clean-energy research and production, the state is helping create green jobs in communities across New York, while ensuring that our environment is protected for generations to come.”

For more information and to download the RFP, visit www.nypa.gov.

Sun Setting on Sky-High Solar PricesAccording to a recent study released by the U.S. Department of Energy’s Lawrence Berkeley National Laboratory, the installed price of PV systems in the United States fell substantially in 2011 and through the first half of 2012.

The study, “Tracking the Sun V: An Historical Summary of the Installed Price of Photovoltaics in the United States from 1998 to 2011,” examines more than 150,000 residential, commercial and utility-sector PV systems installed between 1998 and 2011 across 27 states. That sample represents roughly 76 percent of all U.S. grid-connected PV capacity installed.

The study’s findings indicate that the median installed price of residential and commercial PV systems completed in 2011 fell by roughly 11 to 14 percent from the year before. The declines varied depending on the size of the system and its location. For example, the costs of systems installed in California fell by an additional 3 to 7 percent within the first six months of 2012.

The report also highlights the different trajectory of price declines for nonmodule costs, such as installation labor, marketing, overhead, inverters and the balance of systems, as compared to the decline in prices for the modules themselves. According to the report, nonmodule costs have declined by roughly 30 percent from 1998 to 2011. However, these figures are somewhat deceiving, as the decline for nonmodule costs has not been as great as it has been for module costs. Consequently, the price of nonmodule costs represents the portion of the total cost for solar where the greatest reductions can still be made.

According to the report, the median price of PV systems installed in 2011 ranged from $6.10 per watt for the smallest systems (residential and consumer systems smaller than 1 kilowatts) to $3.40 per watt for utility-sector PV systems larger than 2,000 kW.

The study suggests that the greatest potential for further cost reductions could be through large-scale deployment programs because solar represents significant economies of scale.

Study Finds Solar a Bargain for New Jersey and PennsylvaniaNew Jersey and Pennsylvania are major solar markets in terms of the amount of installed solar capacity. New Jersey, the nation’s second-largest solar market with 900 megawatts (MW) of solar capacity is the first state to generate more than 1 percent of its annual electricity from solar. Pennsylvania ranks eighth in installed capacity.

Utilities in both states are mandated to buy certain amounts of solar power every year. They pay a premium for that solar power in the form of Solar Renewable Energy Certificates (SRECs) and pass the cost on to ratepayers.

The study found that solar power delivers a total levelized value, ranging from $256 to $318 per megawatt-hour (MWh). However, this includes a premium value in the range of $150 to $200 per MWh above the levelized value of the solar electricity generated. The SRECs in New Jersey currently cost about $60 per MWh and in Pennsylvania about $20 per MWh.

“This indicates that electric ratepayers in the region are getting more than a two-to-one return on their investment in solar energy,” said Dennis Wilson, president of MSEIA. “Our analysis indicates that SRECs can increase in price, deliver net benefits and still support strong solar growth. This net-positive benefit will only increase as solar technology continues to drop in cost.”

“Add together the proven public health, security and environmental benefits, and it’s clear that aggressive solar power development is a win for these states and their residents,” said Lyle Rawlings, vice president of MSEIA, New Jersey division.

The study concluded that, by offsetting the need for conventional power, distributed solar power delivers measurable benefits, such as lower conventional electricity market prices due to reduced peak demand; a valuable price hedge by using a free, renewable fuel rather than variably priced fossil fuels; avoided costs of new transmission and distribution infrastructure to manage electricity delivery from centralized power plants; reduced need to build, operate and maintain natural gas generating plants; reduced outages due to a more reliable, distributed power system; and reduced future costs of mitigating the environmental impacts of coal, natural gas and nuclear generation.

Renewables in Europe Could Soon Displace Fossil FuelsIf futuristic thinking and undiminished optimism are the hallmarks of the industry, then the latest assertion from a European think tank devoted to green power and democracy should come as little to no surprise.

According to a report published by the German-based Heinrich-Boll Foundation, the European continent could be powered by 100 percent renewables by the middle of this century. The report, “A European Union for Renewable Energy—Policy Options for Better Grids and Support Schemes,” argues that with the right mix of policies and direction, the European Union can and should completely shed its dependence on fossil fuels by 2050.

While theoretically possible, the milestone of a 100 percent renewable-powered Europe is fraught with monumental challenges, both practical and political. For example, according to the report, nuclear power plays no part in the continent’s renewable future, a fact that will not be lost on member nations, such as France, where nuclear power is a huge slice of the power pie. The report also asserts that about two-thirds of the continent’s power plants will have to be replaced in the coming years. Last, the report recognizes that in their adoption of renewable power, European nations are anything but uniform, and leaders such as Germany will have to set the example for other nations.

The report breaks down the task into two distinct categories. The first set of policy imperatives concern the transition of the continent’s grid infrastructure. The second set of options concerns the development of support and remunerations schemes that will encourage this change.

The first set of imperatives includes such recommendations as binding targets of 45 percent renewable energy for the energy sector by 2030, redesigned markets to accommodate variable renewable energies, and a stable environment for investors. The second set of recommendations focuses on transparency and democracy to win public support. It includes such recommendations as demand management and decentralized power generation, the formation of stakeholder groups and public participation in the grid-planning process.

Global Renewable Demand, and Investment, on the RiseThe first study, “Global Wind Consumer Wind Study 2012,” surveyed consumer preferences for renewable power. Conducted by TNS Gallup, it found that 45 percent of consumers perceive climate change as one of the top three challenges facing the world today. An even greater percentage of consumers would be willing to tailor their choices based on the power that is used to manufacture the things they purchase. More specifically, 65 percent said they would be more willing to buy products from brands using wind energy. Nearly half, 49 percent, said they would pay more for these products. Purchasing choices notwithstanding, a whopping 85 percent said they want more renewable power.

The second study confirmed that companies are also getting on the bandwagon. “The Corporate Renewable Energy Index Report 2012,” prepared by Bloomberg, indexes companies that use renewable-power voluntarily. It identified a continued global increase in new renewable-energy capacity. Specifically, at $237 billion, net investment in renewable power capacity in 2011 far exceeded the $223 billion invested in fossil fuels in the same year.

The index also found that many companies made a significant commitment to renewable energy through direct investment in on-site generation, which accounted for 40 percent of renewable electricity purchases in 2011. The index includes 389 companies from 26 countries. —Rick Laezman

Scientists Tackling Cost, Charge-Life of EVsThrough research and innovation, all of these technologies have been able to overcome their initial obstacles to a greater or lesser degree on their paths to becoming more affordable and accessible to mainstream consumers.

The same may be said of the electric vehicle (EV). Despite its recent surge in popularity and the promise it holds for helping the nation to wean itself off of foreign oil, the technology still suffers from some major flaws, which make it less than a practical consideration for most drivers who are in the market to buy a car. Chief among these flaws are the high cost, long charge times and short driving range.

All of these flaws can be traced to the integral component of the EV: its battery. Lithium-ion batteries have been the blessing and the curse of electric and hybrid vehicles. A common element in rechargeable consumer electronics, they possess the desirable qualities of high energy density and slow loss of charge when not in use, which makes them an ideal candidate for EVs.

On the other hand, the high cost and the limited range of EVs also represent a great drawback. These vehicles typically have a range of only slightly more than 100 miles even in the most ideal conditions, which means drivers can’t go far before they have to plug in and wait for the battery to recharge.

Recently, scientists with the Toyota Research Institute of North America (TRINA) conducted research on alternative components that could spur the development of a less expensive, longer lasting EV battery. Results of their research were announced in the scientific journal Chemical Communications.

In the article, the scientists describe tests on a battery made of magnesium and a tin anode insert. Magnesium is the eighth most common element in the Earth’s crust, in contrast to lithium, which is far less common, and it has a higher positive charge of two compared to lithium’s one. All of this means that a magnesium battery would be less expensive to manufacture than a lithium battery, and it could store more power, which would increase the range of the car.

Don’t expect to see EVs powered by magnesium-ion batteries any time soon. Technical and scientific hurdles remain, and the typical time for a concept to travel from scientific breakthrough to mass commercialization can often be as long as 10 years. Until then, stay close to home.

Digger Derrick Exemption Granted for Subpart V Related WorkThe direct final rule will become effective in February 2013.

“OSHA has, through direct final rulemaking, expanded the digger derrick certification requirements to now exclude work meeting the scope of Subpart V work and utility type settings. Digger derricks fitting the description of this exemption are not required to meet certification requirements under subpart CC by 2014. Digger derricks used in construction related activities, such as installation of traffic signals, lighting and others not meeting the definition of Subpart V work or utility setting, fall outside the exemption of this rule. Contractors should be mindful that, while the certification requirements have been lifted, employers still have to ensure that digger derrick operators have been trained and are proficient in the safe operation of such equipment prior to use,” said Jerry Rivera, NECA’s director of safety.

When federal OSHA promulgates a new standard or a more stringent amendment to an existing standard, the 27 states that have state-run programs and U.S. territories with their own OSHA-approved occupational safety and health plans must amend their standards to reflect the change. The state standard must be at least as effective at protecting employees as the final federal rule. State Plan States must issue the standard within six months of the promulgation date of the final federal rule.