What a difference six months makes. In January 2025, we reported on economists’ predictions for the year. The consensus was “some slowing in the economy but still significant growth.“ At midyear, economists are predicting the reverse—significant slowing, though some growth. To paraphrase the words of Forrest Gump, the construction economy right now is like a box of chocolates—“you never know what you’re gonna get.“

A look at spending

Tariffs, inflation and immigration policy play a role in the country’s economic performance moving forward this year. Construction starts forecasts for 2025 are now lower than January’s estimates. In the late months of 2024, Dodge Construction Network, Boston, projected starts growth at 9% ($1.277 trillion) for 2025. Now at midyear, they have lowered growth to 7.5% ($1.26 trillion).

Cincinnati-based ConstructConnect and its partner Oxford Economics, New York, predicted total starts growing 8.5% ($1.018 trillion). That number in midyear was revised to contract by 1.8% ($944.65 billion.).

It’s a strange time. This uncertain economy is filled with a hesitancy that infects investment, consumer spending and production. And yet, the fundamentals remain strong. In May 2025, unemployment stood at 4.2%, with inflation at 2.4%.

For many sectors, the work is there, including backlogs, but future work is stuck in neutral. Comparing April 2025 year-over-year (y/y), ConstructConnect’s Project Stress Index revealed a mild rise in delayed bids but a decrease in on-hold projects. Abandoned projects—a small percentage of all projects—were elevated in part due to “recent changes in trade policy.“

The first quarter of 2025 showed that gross domestic product (GDP) retracted to –0.2% from 2.4% in Q4 2024 (the first contraction since early 2022). Historically, first-quarter numbers are weaker as winter weather and other influences play a role. The Bureau of Economic Analysis attributed the GDP decline to an increase in imports (a subtraction in the calculation of GDP) and a decrease in government spending. GDP could have fallen further if not for increases in investment, consumer spending and exports.

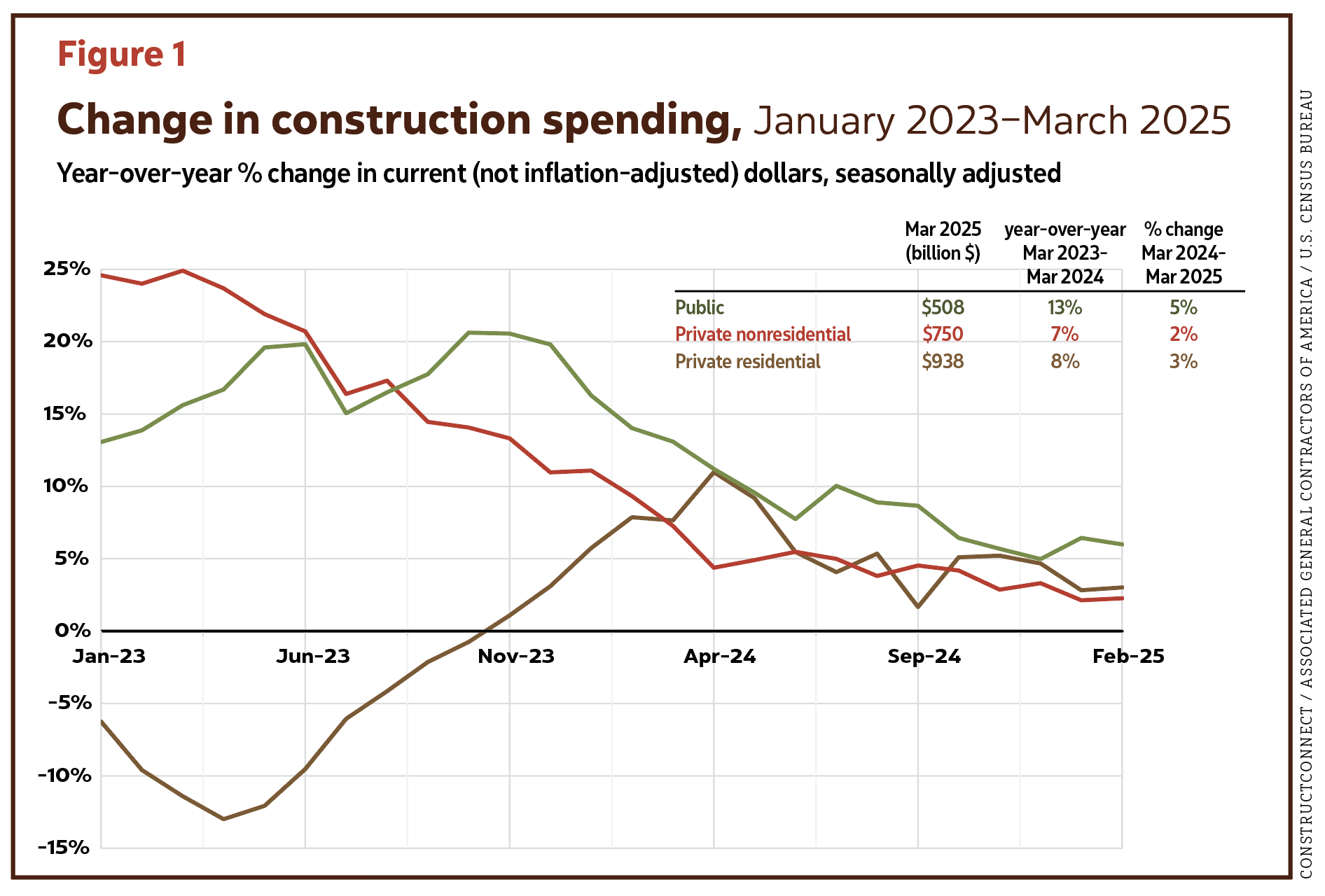

“For the construction industry, the GDP decline may cause confusion but doesn’t signal a pullback in actual activity,“ said Ralph Flores, economist for Dodge Construction Network. “Public construction and select nonresidential sectors like healthcare remain supported by steady investment and underlying demand. On the residential side, housing activity—the largest construction sector—showed resilience in the first quarter, with residential fixed investment contributing positively to GDP. Looking ahead, residential construction faces significant headwinds such as high interest rates, tighter credit conditions and consumer uncertainty threatening to dampen future demand.“ See Figure 1.

The Conference Board expects U.S. real GDP to grow by 1.6% in 2025, with the bulk of the effects of tariffs likely to hit the economy in Q3.

The University of Michigan’s Surveys of Consumers saw April 2025 y/y consumer sentiment drop by 26.5%. It went unchanged in May. The Consumer Price Index (CPI), however, increased only 0.2% in April. That was the smallest 12-month increase in the index since February 2021. The CPI increased 2.3% y/y in April. In other positive news, The Conference Board’s Consumer Confidence Index increased by 12.3 points in May to 98.0 (1985 = 100), up from 85.7 in April.

Federal Reserve Chair Jerome Powell has paused additional interest rate cuts, eyeing how federal policies may affect growth and inflation. However, the Fed expects two rate cuts later this year.

A closer look at construction

Though the economy is undergoing some “uncomfortable times,“ Dodge's chief economist Eric Gaus is not forecasting a recession.

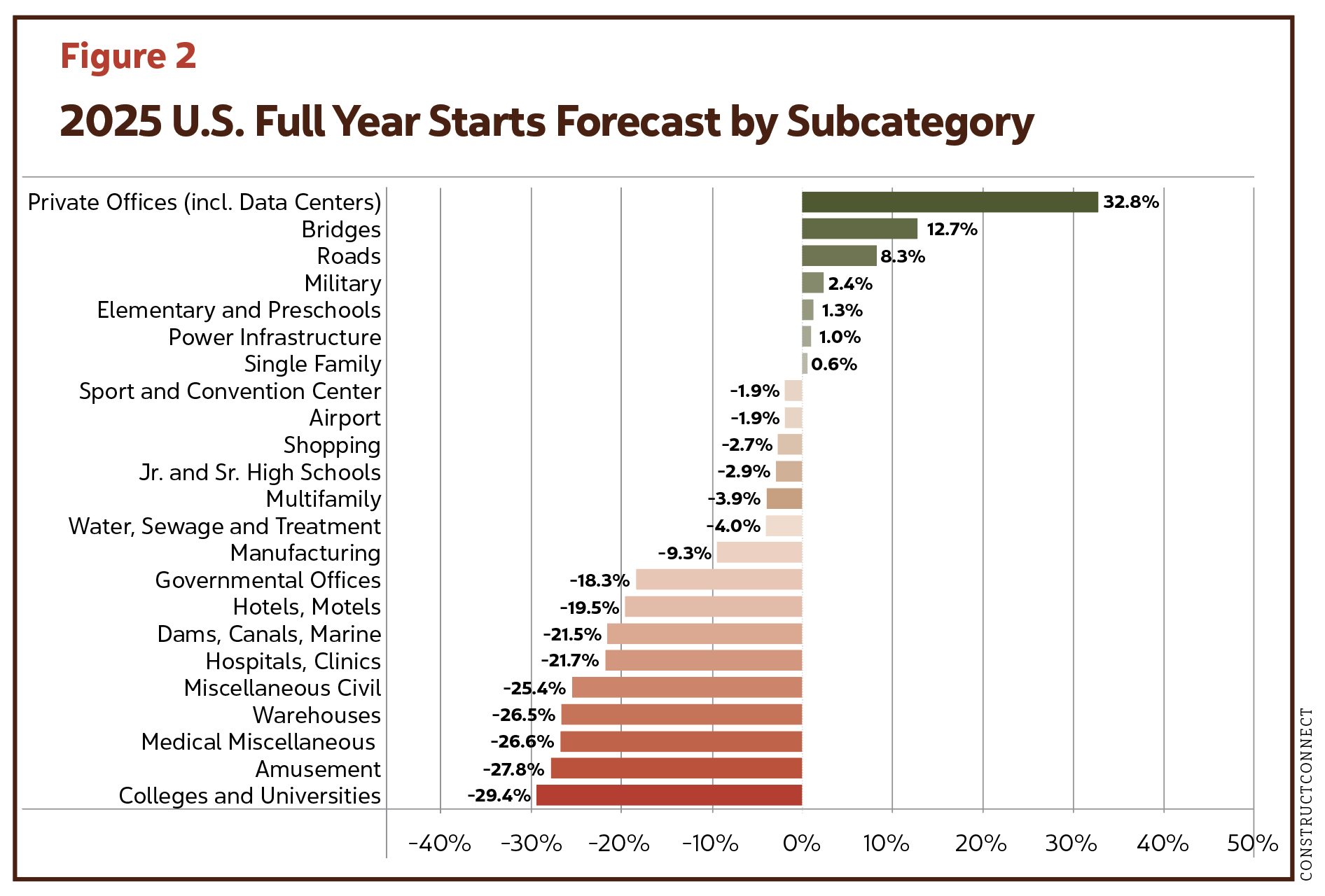

“Much of the nonbuilding is being funded by the Infrastructure Investment and Jobs Act [IIJA], with most of that funding still in the pipeline,“ he said. “So, roads and bridges, airports and so forth. The funds haven’t been clawed back. We don’t see that as a likelihood. Coming in second, institutional. The education sector is weaker, though K-12 is stronger. It’s healthcare that benefits from some large-scale projects, hospitals in particular. In commercial, manufacturing remains strong, even with starts dropping off some 50%. The drop, however, is from ridiculously high numbers. Today’s starts reflect what would be considered healthy pre-COVID numbers.“ See Figure 2.

ConstructConnect held its spring webcast, “The Construction Economy Outlook,“ on May 8. The firm brought its economists together with those from the American Institute of Architects (AIA), Washington, D.C., and the Associated General Contractors of America (AGC), Arlington, Va.

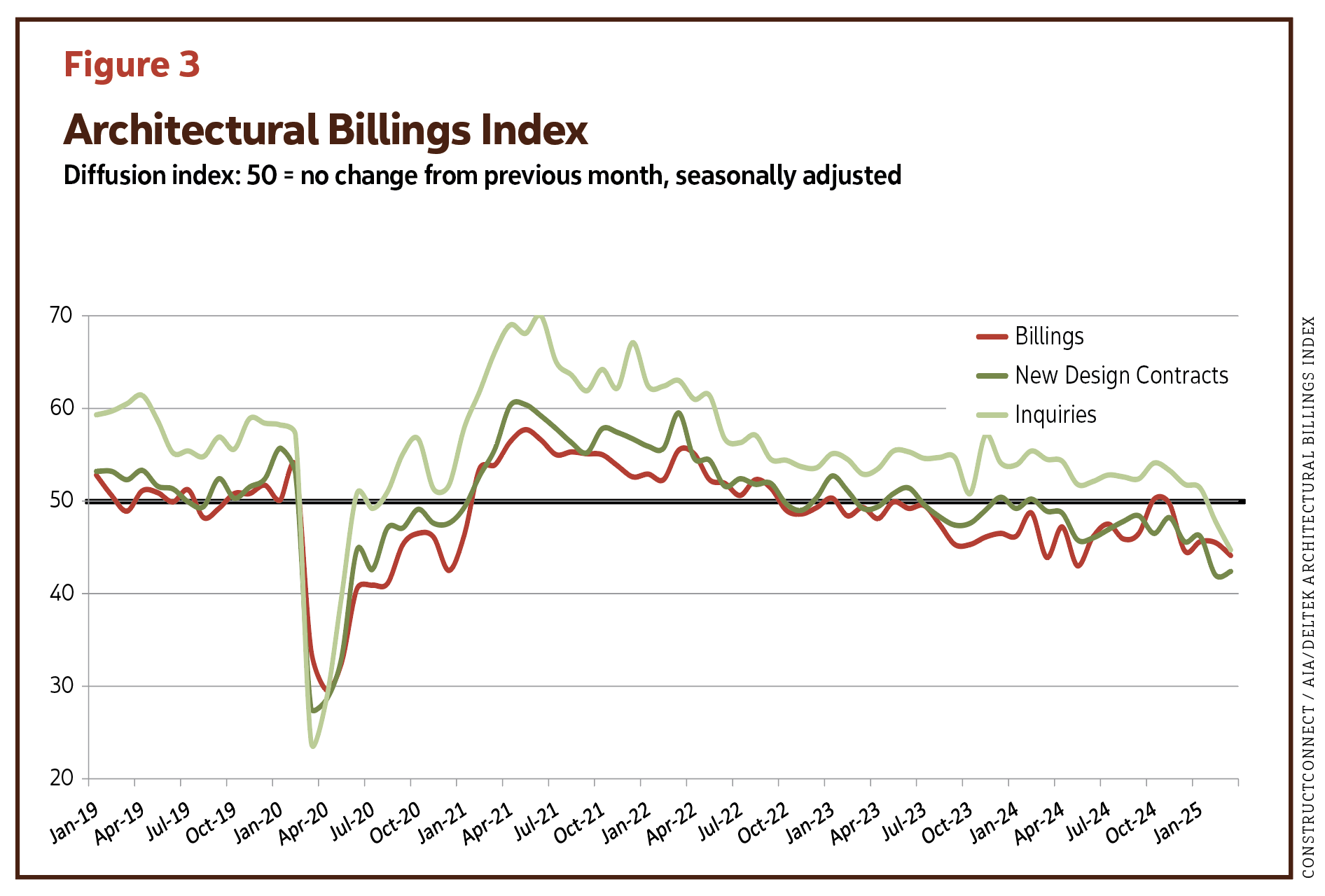

Kermit Baker, AIA’s chief economist, said, “Architecture project work has been soft since the fourth quarter of 2022. Projects move ahead in fits and starts, and that’s really what we have seen for the last year or so.“

The AIA/Deltek Architecture Billings Index (ABI) for April 2025 declined to 43.2. Billings declined for 28 of the last 31 months. See Figure 3.

According to AIA, “Although the U.S. economy is not officially in a recession at this time, many architecture firms are reporting recession-like business conditions.“

An ABI below 50 indicates a decline in activity. All regions reflect numbers under 50. The Northeast reflected the greatest softness for the last seven months (40.2). Firms in the West saw conditions retreat at the start of the year (42.1). The strongest region was the South (46.2), followed by the Midwest (44.4). By sector, architecture firms found institutional work to be the strongest.

In a different measure, the Dodge Momentum Index rose 1% in April 2025 and 3.7% in May. DMI measures nonresidential planning.

“Nonresidential planning continued to accelerate in May, primarily driven by strong project activity on the institutional side of the DMI,“ said Sarah Martin, associate director of forecasting, Dodge Construction Network. “Planning momentum moderately improved on the commercial side as well, following subdued growth in that sector over the last few months—outside of data centers. Increased economic and policy uncertainty will continue to contribute to heightened volatility in the project data—but in aggregate, planning activity is on steady footing.“ For some perspective, the DMI was up 24% y/y in May. The commercial segment was up 15%, institutional up 47%.

Data centers remained the fuel holding up commercial numbers and the DMI itself in April, although they returned to more typical levels in May.

“If you strip out data centers, the [April] DMI is largely flat,“ Gaus said. “That would still be the case if the others [verticals] were healthier. Data centers are just growing so rapidly.“

ConstructConnect's chief economist Michael Guckes is encouraged by megaproject activity.

“On average, we’re seeing about $10.2 billion of megaprojects per month,“ he said, adding that, “A megaproject is a project with a $1 billion or more start. And if we look forward to 2025 and beyond, we have hundreds of billions of dollars’ worth of megaprojects that we continue to track. Not all those projects will break ground in 2025. Others may be delayed into the future. But that pipeline of existing megaprojects that we see on the horizon is very, very encouraging.“

The employment picture

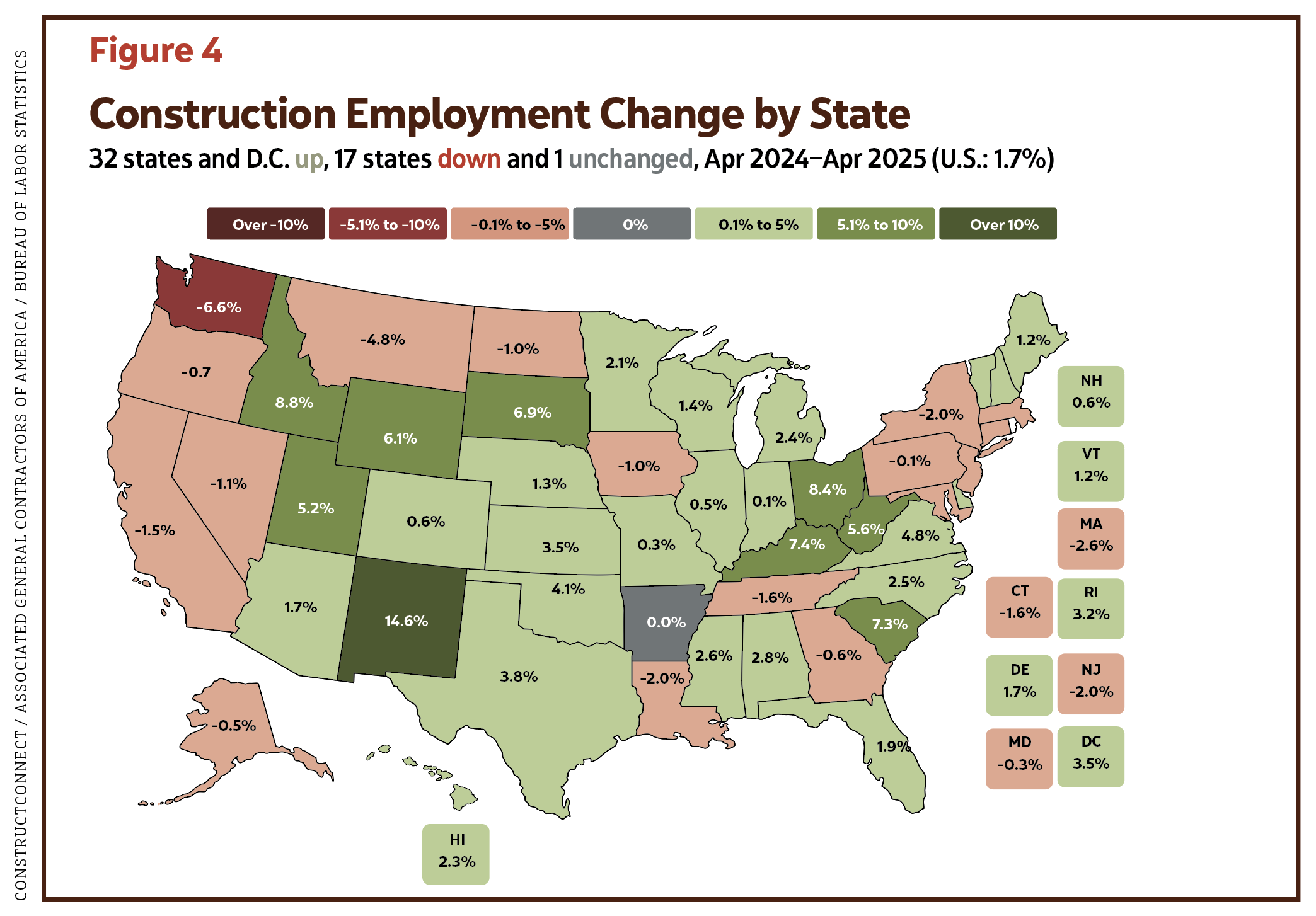

Ken Simonson, chief economist for AGC, shared that construction employment in April increased in 32 states and the District of Columbia from last year, but only 24 states added construction jobs between March and April. Within that, Texas added the largest number of construction employees (32,000 jobs or 3.8%), followed by Ohio (20,500 jobs, 8.4%) and Florida (12,400 jobs, 1.9%). See Figure 4. In May, construction employment seasonally adjusted, totaled 8,314,000, a gain of 4,000 from April and 126,000 (1.5%) y/y, with nonresidential construction employment rising 2.6% and residential seeing a small drop (–0.3%).

“Contractors tell us that finding workers is still their number one challenge,“ Simonson said. “Positions that don’t require prior training or industry experience have gotten easier, something consistent with the broader economy. People who shunned construction because they thought they could get an indoor job with flexible hours are now finding those hard to come by or not paying as well as construction. So, more people are showing up to apply for entry-level construction jobs. I expect wages in 2025, at least for craft workers, to rise in the 4.5%–5% range.“

Costs and bidding

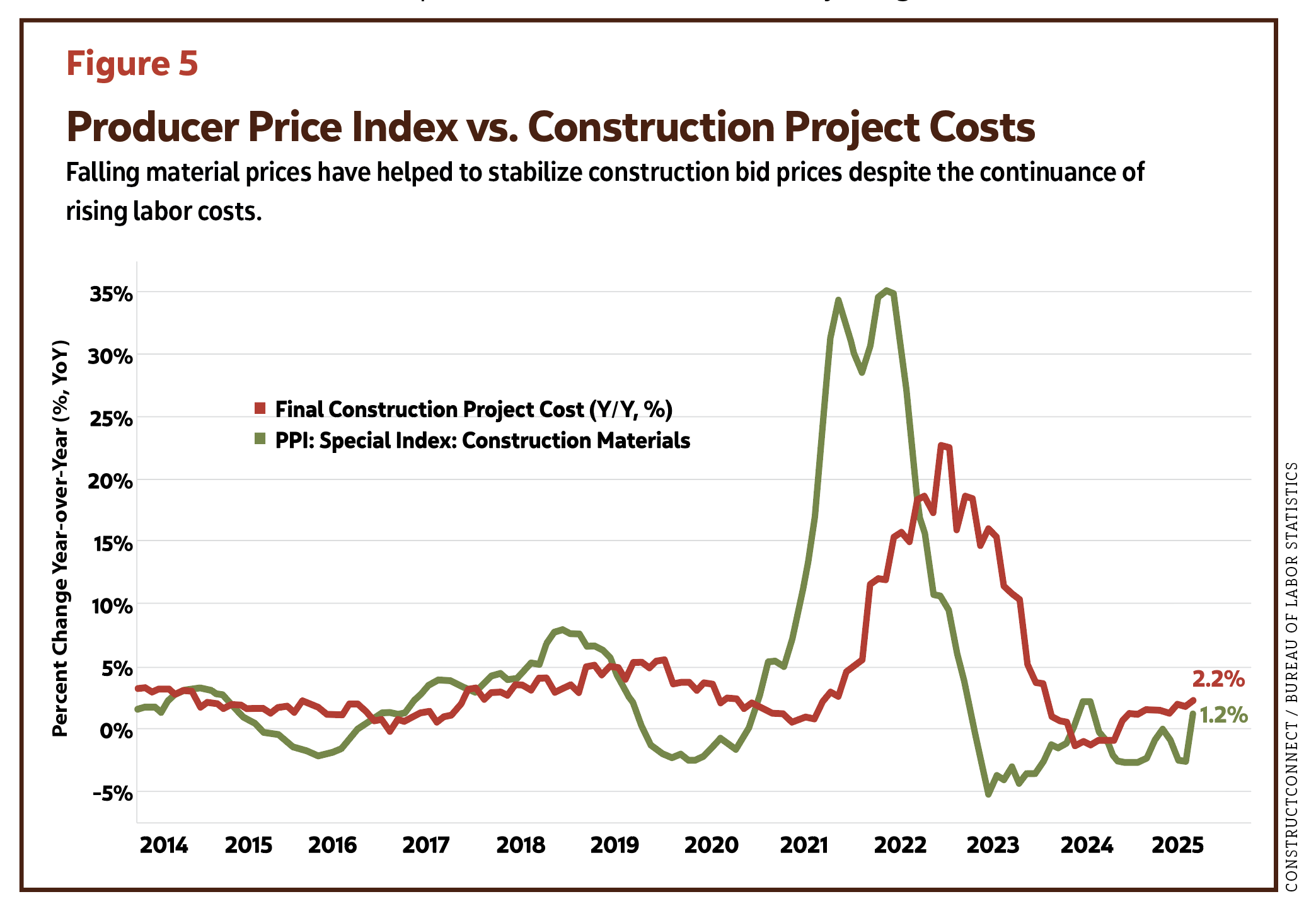

In terms of product costs, the AGC reported May 2025 y/y showed a 2.2% increase for nonresidential construction. The most volatile products were steel mill products (8.8% y/y), aluminum mill shapes (8.8%) and gypsum building materials (1.4%). These numbers were derived from the Producer Price Index (PPI). AGC added that tariffs threaten to drive up construction costs 2%–3%. See Figure 5. Stay tuned as the 25% steel and aluminum tariffs imposed on March 12 now jump to 50% (as of June 4).

Kristy O’Brien, ConstructConnect's director of private content acquisition, said, “We continue to witness growth in sectors like retail and restaurants, an upswing in activities such as new grocery stores and companies repurposing existing locations from one brand to another. Former office spaces are being converted into commercial use.

“Additionally, there has been a rise in construction for educational and medical facilities. Healthcare facilities could be prime candidates for repurposed spaces, which may contribute to the observed increase in medical building uses. And we continue to see a rise in planning for data centers. This shows us the growing demand for cloud services and advanced technologies like A.I.,“ she said.

O’Brien has seen slight declines in municipal projects. In addition, while there is plenty of work, warehouses and distribution centers may have peaked.

Trade and immigration

Guckes shared this point about tariff wars, using Canada and the United States as an example: “The U.S. remains Canada’s overwhelming trade partner, consuming almost 80% of Canadian exports. A stable exchange rate helps prices as goods move across the border.

"Trade is about one-quarter of all Canadian economic activity. So, seeing a trade war potentially ensue in the coming year or years would have a real impact on the construction economy, especially on the material side," he said.

He cited a 5% rise in lumber costs in May.

The construction workforce is very diversified, with workers from all over the world. Construction firms may struggle to find enough qualified people if there are significant changes to immigration policy.

A strong economy is facing a great deal of uncertainty. Will your box of chocolates be full of duds, or will you luck out with a truffle? Economists and the construction industry would bet on the truffle.

“Call me an optimist,“ Baker said. “I think we’re going to see some better times ahead, particularly by the second half of 2025.“

Clarity out of Washington will help.

Vecteezy | Stock.adobe.com / somchaisom

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].