Sometimes it feels like the construction industry is a moving puzzle. In 2023, you might not have control of the issues affecting you, but you can decide how you react to what you get. Different opportunities will fit into your business plans better than others, so it helps to know your goals, your strengths and what lies ahead. And when the pieces fall just right, your wins might even erase some of the losses.

For the pieces to fit into place, some situations must play out right at home and abroad. The Federal Reserve must tame inflation without tipping the economy into a recession. Interest rates can then begin a slow retreat. Other factors include less disruptive energy prices, de-escalation of the conflict between Ukraine and Russia, and a limited climb in unemployment. There are other requisites too, but economists wager strong fundamentals will win the day for a softer, shorter downturn with subdued growth

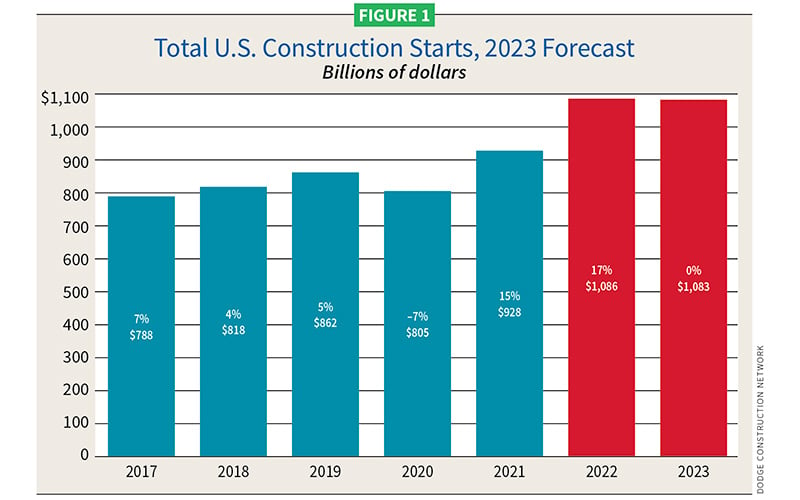

Last year was a very good year for construction in several sectors. Dodge Construction Network, Hamilton Township, N.J., estimated 2022 gains for total construction starts at 17% ($1.086 trillion). ConstructConnect, Cincinnati, Ohio, came in at 11.8% ($990 billion).

This year, expect a slowdown. Dodge sees flat growth (0%/$1 trillion) (see Figure 1). If a recession hits, perhaps a 9% loss. ConstructConnect forecasts a retraction at -4% (S861.1 billion). The firm also projected total construction put-in-place (PIP) spending (work in-progress). In 2022, PIP spending advanced 9.9% ($1.7 trillion), growing 1.4% over 2021. This year, PIP is forecast to gain another 3.2% ($1.8 trillion).

Forecasts were shared on Nov. 15, 2022. Dodge presented its webinar, “On the Razor’s Edge—Will the U.S. Economy Enter Recession and How Will Construction Starts Respond in 2023?” ConstructConnect, in collaboration with the American Institute of Architects (AIA), Washington, D.C., and the Associated General Contractors of America (AGC), Arlington, Va., presented its webinar, “Resources for a World of Economic Uncertainty.”

“Next year will not be a repeat of what the construction sector endured during the Great Recession when the financial system collapsed,” said Richard Branch, chief economist for Dodge Construction Network.

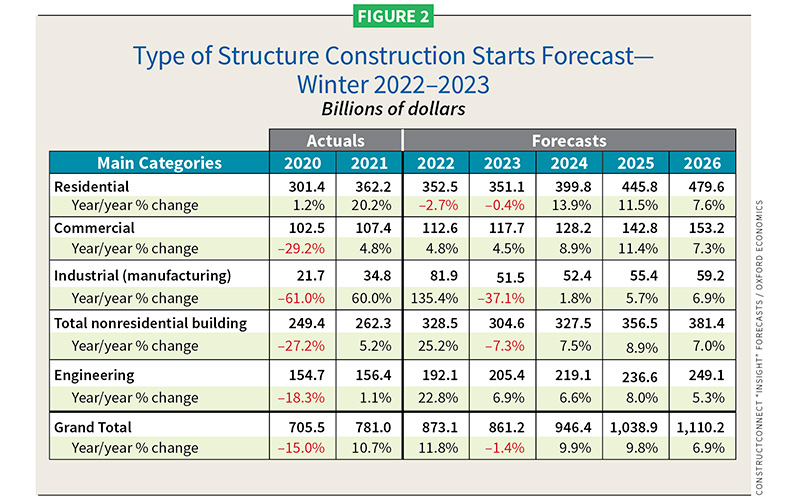

“Residential construction, already reeling from rising mortgage rates, will continue to contract and will be joined by nonresidential construction as the commercial sector retrenches (see Figure 2). The funds provided to the construction industry through the Infrastructure Investment and Jobs Act (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act (IRA) will counter the downturn, allowing the construction [industry] to tread water. During the Great Recession, there was no place to find solace in construction activity; 2023 will be quite different,” he said.

Economy should support construction

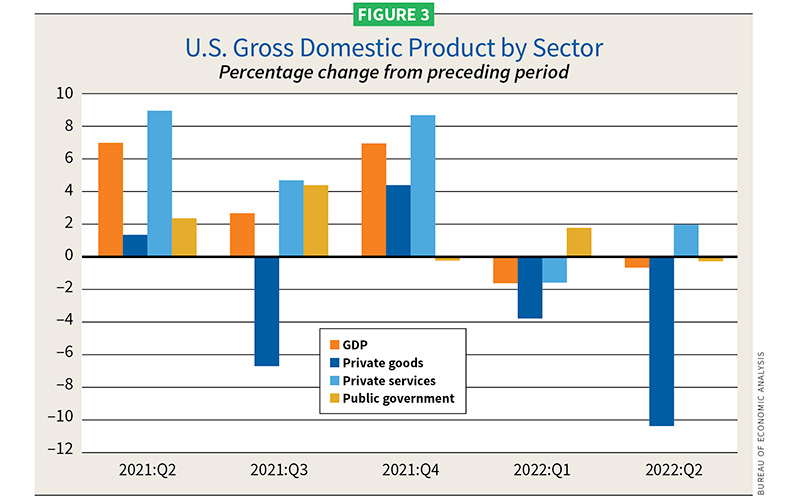

Cristian “Cris” deRitis is deputy chief economist for New York-based Moody’s Analytics. The global firm forecast 2022 gross domestic product (GDP) to settle at 1.7% ($19.9 trillion). The year-end GDP for 2023 will reflect a slowing at 0.7% (see Figure 3 from the Bureau of Economic Analysis). In December 2022, Moody's published its own 2023 economic forecast.

“Some growth, but much slower,” deRitis said. “If you break that out by quarter, we expect a small negative the first half of 2023 but picking up growth in the second half of the year.” That trajectory is similar among Dodge, ConstructConnect and others.

“This all assumes that the Fed script with its rate hikes goes according to plan and they’re enough to slow down the economy,” deRitis said. “The slowdown is reflected in our baseline. For 2023, we expect unemployment to remain healthy but rise closer to 4%. That is success in terms of the Fed’s plans.”

Wages should continue to rise in 2023, deRitis offered, with a labor market remaining tight (the economy showed full employment in 2022). “That is a reason the Fed stands a chance in terms of navigating this narrow path of slowing without a recession,” he said.

In other positives for the U.S. economy, deRitis pointed to strong balance sheets for households, businesses and banks, providing some resiliency.

“Household debt service ratios are near all-time lows. People have locked in very low interest rates on their mortgages and some on their auto loans [prior to the rapid rise in inflation]. So even though interest rates are rising, for most existing homeowners and debtors, their payments are not rising. That does open some room for their balance sheets and offers a cushion against economic shocks, whether that’s inflation or a weakness in the labor market. We are growing debts, but they are not excessive,” he said.

Even in a slower 2023, deRitis feels banks should be able to weather the storm and continue to supply credit, thereby helping favor growth. Government stimulus programs will also continue to steady a challenged economy.

“We are also seeing some manufacturing return—another tailwind,” deRitis added.

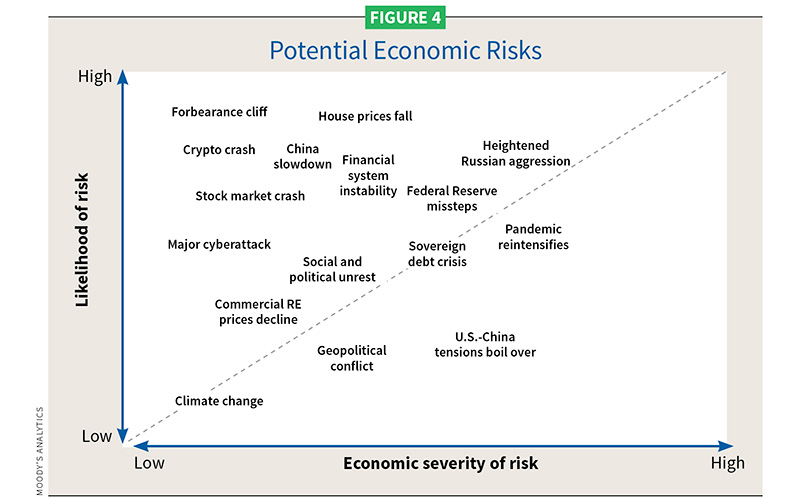

As for headwinds to 2023, deRitis said they are obvious. “There’s a plethora of uncertainty out there,” he said. “Inflation is the top headwind until we get at least the trend of inflation moving down at a sufficiently fast pace so the Fed can see light at the end of the tunnel. They will continue to hike interest rates and tighten monetary policy. If they [the Fed] go too far, how much damage does that cause to employment and demand? That’s clearly at the top of the list of our concerns.” (See Figure 4.)

Kermit Baker, AIA chief economist, added, “High inflation is pushing short-term rates by almost four percentage points since the beginning of the year [2022].“

In fact, in December 2022, the Federal Reserve did stick to its plan and raised rates another half-point to bring the total hike in 2022 to 4.4%. Inflation slowed in November after 18 months of relentless price rises (down from 7.7% to 7.1%).

“The popular scenario is that the Federal Reserve Board will stop raising interest rates around midyear 2023, maybe as early as the end of the first quarter,” Baker said. “They could even begin cutting interest rates by early 2024,” he said.

Another headwind is the war in Ukraine, which could further hurt energy markets, affecting households and businesses.

“Do we get another energy supply shock; does a hurricane come through and [take] out some refinery?” deRitis asked. “Other flare-ups in Europe and trade tensions with China could impact 2023, too. Issues can come up.”

Through the lens of economic cycles, 2022 was the year economists saw a possible recession. Inflation has added more pressure. Moody’s puts the odds of a recession in 2023 at 50%. Though it is expected this recession will be short-lived, deRitis added it will still hurt. Branch also stated that the downturn should be mild compared to past cycles (see Figure 5).

“Certain industries clearly are going to feel more pain. The housing industry is already feeling some hurt,” deRitis said, adding that, however, “The construction industry today is much more disciplined. Perhaps the experience of having gone through the Great Recession has educated it in terms of risks. During COVID, the industry did not stop building. I think we will effectively navigate this period.”

Optimism in a slowdown

“The economy is doing better than most people probably think, and in fact is reflected in the latest set of revisions to the GDP numbers,” said Alex Carrick, chief economist for ConstructConnect. “The pandemic decline was revised to –2.8%, which wasn’t much different from –2.6% for 2009. Also, it’s interesting that support in the third quarter [of 2022] came from trade, an unlikely source. The U.S. is now exporting oil and natural gas, a lot of it going to Europe. This has tremendous implications. for future large domestic LNG (liquefied natural gas) projects and petrochemical projects“ and related logistical support—new pipelines, ships and terminals.

Carrick pointed to the strength in megaprojects in 2022, which was a banner year for projects of a billion dollars or more.

“Projects included LNG plants using wind power to reduce the carbon footprint for LNG production, U.S.-based semiconductor manufacturing plants and battery plants. I keep waiting for this megaproject run to tail off,“ he said. “They keep on coming. They’re not necessarily influenced by commercial bank interest rates because they have other sources of funding.”

Megaprojects include the $5.5 billion electric Hyundai plant in Georgia, the $1 billion Gulf Coast Ammonia plant in Texas and the $2 billion Massachusetts General Hospital in Boston.

Carrick is expecting the move to net-zero emissions in buildings, the power grid and vehicles to become the next industrial revolution of sorts—driving growth in manufacturing, power and utilities, and industrial.

“There’s consensus that the world is going to have to move to zero-carbon emissions over the next couple of decades,“ he said. “And just think about what that will mean in terms of the need for expanded power generation and for commodity markets. This means some major investments right now. You see it with the investment by major auto companies in electric vehicles and batteries.”

Baker sees portions of the IRA and other federal programs providing some lift to construction in 2023 and beyond.

“It offers financing for renewable energy sources and uses those sources to make homes and buildings more energy-efficient,“ he said. “There are incentives for home retrofits for things like heat pumps, increased energy-efficiency retrofits and more efficient appliances. These should boost construction and renovation activity. Helping drive energy-efficiency on the commercial side is a greatly expanded energy-efficient commercial building deduction, commonly known as Section 179D. It offers a tax deduction on a sliding scale for new buildings that achieve at least a 25% reduction in annual energy cost.”

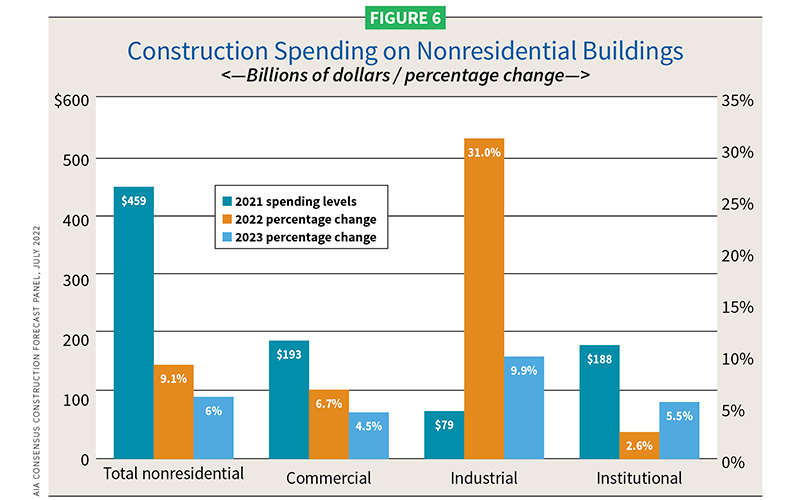

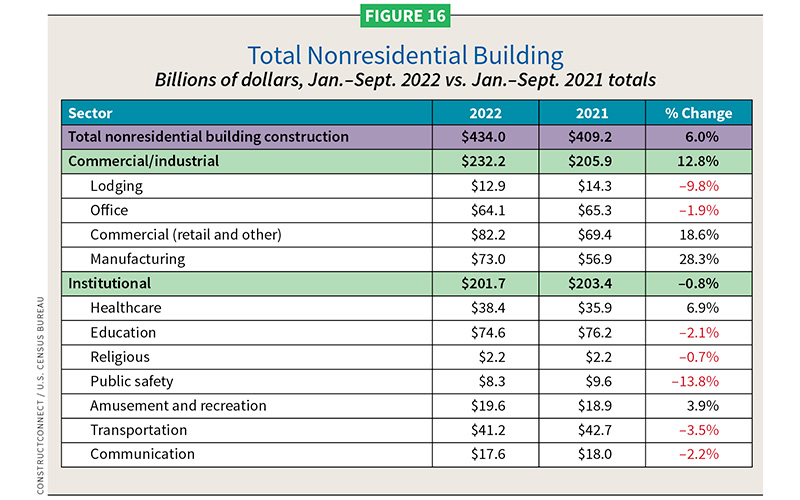

In nonresidential activity, Baker saw the beginning of a rebound in 2022. Spending was up overall 6% through the first nine months of 2022 (see Figure 6). “We saw strong growth on the retail and warehouse side of the commercial market, very strong growth on the manufacturing side and a healthy gain for healthcare facilities,” Baker said. “In 2022, construction employment has increased well over 3%, suggesting that there’s more than just higher costs pushing up construction spending in this sector.”

Estimating the project pipeline

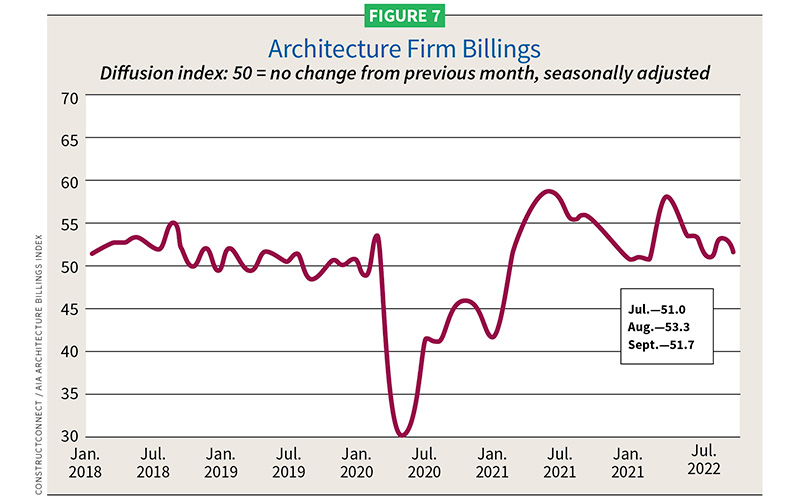

Another gauge for construction health is AIA’s Architecture Billings Index (ABI) (see Figure 7). This is an economic indicator for nonresidential construction activity (lead times of 9–12 months). For several consecutive months, architecture firms reported increased demand for design services. The run ended in October 2022, as the ABI score dropped to 47.7, the first decline in billings since January 2021. Any score below 50 indicates a decline in firm billings.

In some good news, inquiries into new projects continued to grow in October 2022, scoring 52.3, but the value of new design contracts declined to 48.6.

“While billings in the Northeast region and the institutional sector reached their highest pace of growth in several years (as of September 2022), there appears to be emerging weakness in the previously healthy multifamily residential and commercial/industrial sectors, both of which saw a decline in billings in September for the first time since the postpandemic recovery began,” Baker said. “Economic headwinds have been steadily mounting and finally led to weakening demand for new projects. Firm backlogs, however, are healthy and will hopefully provide healthy levels of design activity against fewer new projects entering the pipeline, should this weakness persist.”

Backlogs at firms remained at a robust seven months at the end of September, still near record-high levels since AIA began regularly collecting this data more than a decade ago.

November’s regional numbers broke down as follows: South (50.5), Midwest (47.6), West (45.8) and Northeast (42.4). Viewed by construction sector: mixed practice (51.5), institutional (47.7), multifamily residential (46.1) and commercial/industrial (44.2).

In fall 2022, AIA asked architects to look ahead to overall revenue in 2023. About a third of firms expected gains, a third generally expected flat revenue levels and another third expected declines. Firms concerned about revenue growth cited client concerns over inflation, rising interest rates, lack of staff and contractor availability. Baker added that AIA’s forecast panels projected about a 9% increase in spending for 2022 and an additional 6% increase this year. For 2022, the industrial sector was projected to be the strongest, followed by the commercial market. Healthier gains are expected in the institutional market this year.

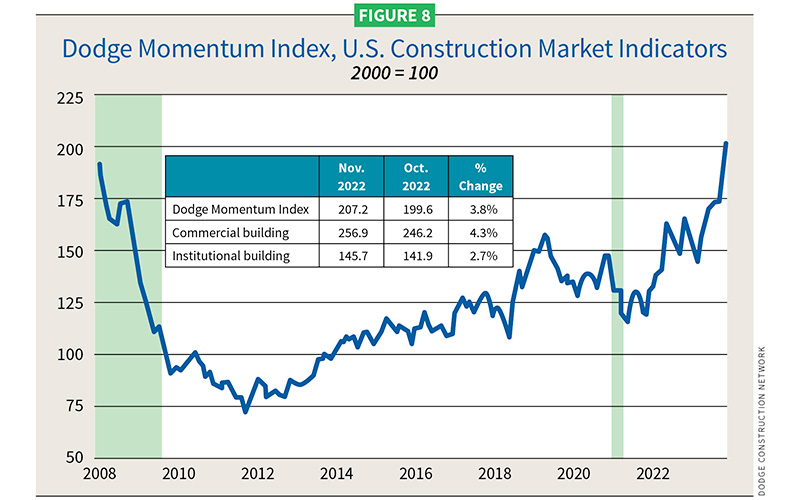

The Dodge Momentum Index (DMI) also gauges economic activity for construction. The DMI is a monthly measure of the initial reports for nonresidential building projects in planning. It leads construction spending for nonresidential buildings by a full year. The DMI in November 2022 rose to 207.2 from a revised October reading of 199.6. Commercial planning grew 4.3% with some healthy growth in hotel and data center projects, and modest growth in stores and office projects. Institutional planning grew 2.7%, featuring increases in government administrative building and religious facilities. Year-to-year, the November DMI was 25% higher (commercial 28% and institutional 21%) (see Figure 8).

“The sustained upward trajectory in the momentum index shows optimism from owners and developers that projects will continue to move forward, even with rising concerns of an economic recession,” said Sarah Martin, senior economist for Dodge. “Specific nonresidential segments, such as data centers and life science laboratories, have thrived in 2022 and continue to support strength in planning activity. As we move into next year, however, labor and supply shortages, high material costs and high interest rates will likely temper planning activity back to a more moderate pace.”

“There are a lot of projects sitting in the planning cycle waiting to break ground, near 14- to 15-year highs in the DMI,” Branch said. “It should provide some semblance of confidence and reassurance that developers and owners are continuing to put projects into the queue.

“What’s precipitating recession talk is that the Federal Reserve loses the battle here and must keep raising rates aggressively through 2023,” he said. “We think there’s a path here to avoiding that, but it is narrow. I think we are going to avoid a technical recession, but it is going to feel recessionary in some sectors here in the construction space.”

Economists at ConstructConnect and AGC feel the chances of avoiding recession in 2023 are good, but there are markets that will feel vulnerable, including multifamily, warehouse, retail, office and lodging.

Construction employment growth

Ken Simonson, chief economist for AGC, has found good news in construction employment, but there continues to be more work than there are workers.

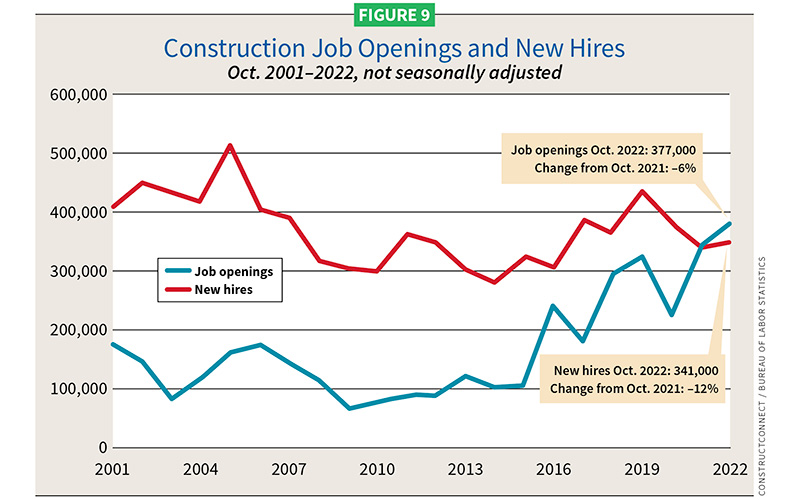

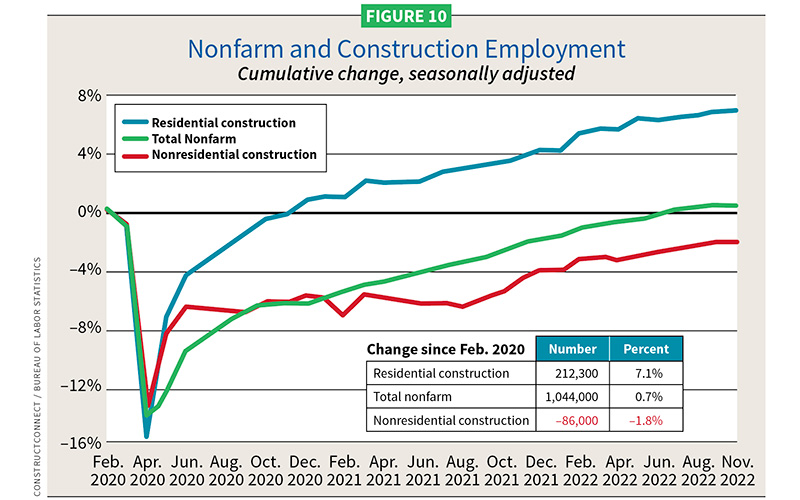

In an analysis of federal employment data by the Bureau of Labor Statistics, AGC found construction employment increased from October to November 2022 in 38 states (42 states added jobs since November 2021). But there was a paradox. Of the 341,000 jobs added, it still did not meet the 377,000 openings (see Figures 9 and 10).

“The shortfall in available workers is undermining job gains and causing delays and higher costs for many projects,” Simonson said.

Looking at the employment picture statistically in November 2022, Florida led in adding construction jobs over the month (5,400 jobs, 0.9%), followed by Ohio (4,800 jobs, 2.0%), Louisiana (3,400 jobs, 2.7%) and Michigan (3,300 jobs, 1.8%). The largest percentage gain occurred in Rhode Island (3.6%, 800 jobs), followed by Nebraska (3.3%, 2,000 jobs), Louisiana, Ohio and Vermont (2.0%, 300 jobs).

Carrick shared that 2022’s year-to-date monthly average gain in on-site employment was 18,000, nearly double 2021’s January–October pace of more than 10,000. And while pay gains have also followed, Simonson was concerned about a lag compared to other industries and the challenges in attracting workers to the profession. The wage concern may be reversing based on information shared by Carrick.

“Wage gains in construction are in the 5% to 6% year-over-year range and it’s partly because the leverage has shifted back to labor,” Carrick said. “Construction workers, including supervisory personnel, are reaping higher earnings rewards than most employees. In September [2022], their year-over-year hourly and weekly wage increases beat the 4.7% and 3.8% jumps for all jobs. Leaving out bosses, construction workers as an employee class were even further ahead than all workers on the compensation front. Year over year, they received 6.6% hourly and 7.1% increases to other workers’ 5.5% hourly and 4.8% gains.”

Retirements and other factors have led to labor being in extremely short supply, Carrick said. Simonson also expects continued challenges in filling construction jobs, though that will vary by state.

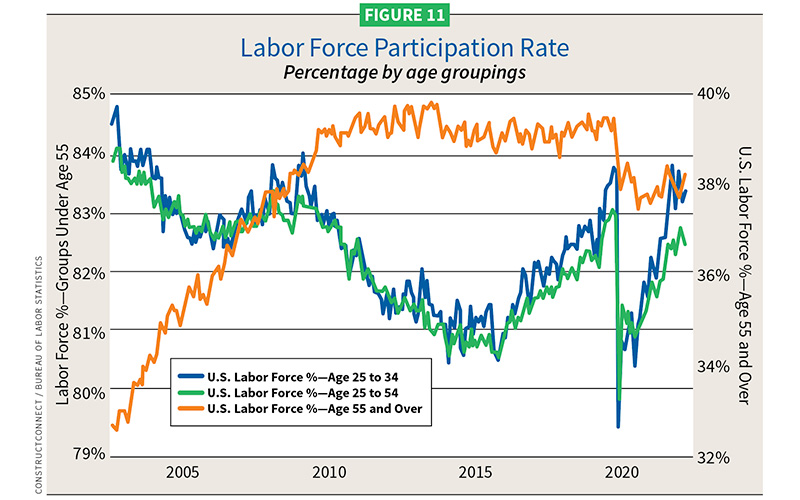

In another wrinkle, Michael Guckes, ConstructConnect senior economist, found implications to consider in construction employment gains, namely the loss of experienced workers (see Figure 11).

“What has replaced them is essentially a much younger and less experienced labor force,” he said. “So, as we’ve offset staffing losses since COVID, the composition of that labor force looks very different right now. Some of the more experienced workforce is now gone. That’s harmed our output by hour. It’s this issue of how we are going to train up the labor force we have—how do we educate them?”

Material costs may have peaked

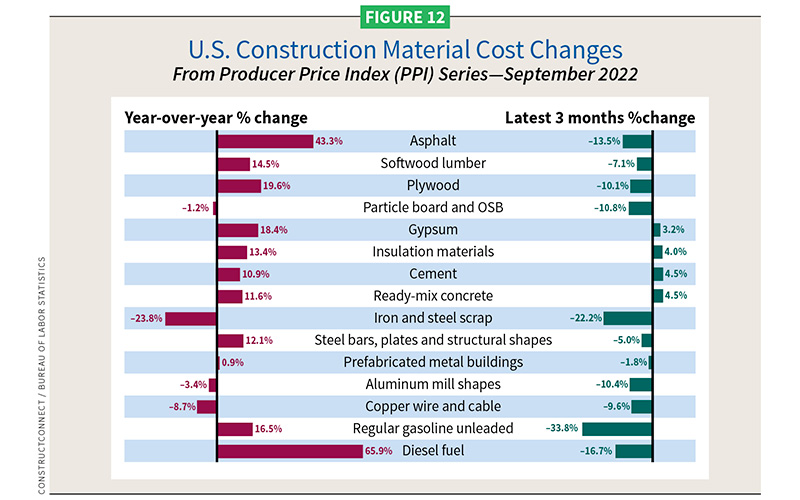

Based on recent Producer Price Index (PPI) data, Dodge’s Branch wondered if material price inflation may have peaked. In November 2022, the PPI’s composite index of construction materials showed a year-over-year average rise of around 3%, a considerable reduction.

“It’s kind of high-normal, but it is improving and that’s certainly a good sign. Regarding bid-price reduction, we think this will continue to go down, but pricing is going to remain challenging, especially the first half of 2023. I think we’ll start to see cooling of inflationary prices in the back half of the year,” Branch said.

As of October 2022, while going down, the PPI index stood at 41.9% above prepandemic levels (see Figure 12).

”There are still some stunningly high year/year cost advances apparent in the data set, but the latest three-month results show clear signs of moderation. Eleven of the 15 items are down since a quarter ago, and, as for the other four, none of them has a gain of more than 4.5%," Carrick said.

“Because average project cost is on the rise, it’s no surprise we’re seeing increases in the average award value for bid projects,” said Fonda Rosenfeldt, senior director of product strategy data for ConstructConnect.

Material prices vary

The National Association of Homebuilders (NAHB), Washington, D.C., reported that while lumber and steel prices have trended down in recent months, the prices of ready-mix concrete and gypsum building materials have continued their climb, which dates back to early 2021. Specifically, the PPI for softwood lumber (seasonally adjusted) declined 2.9% in September 2022, adding to a 5.2% drop in August.

Though softwood lumber prices are 14.5% higher than they were a year ago, they’ve fallen 39.6% since last March. Steel mill product prices decreased 6.7% in September, falling to a total of 16.1%, but these prices are still nearly double their prepandemic levels, on average. The PPI for ready-mix concrete increased 1.4% in September, its sixth consecutive increase, resulting in a rise of 11.6% in 2022. The PPI for gypsum building materials edged 0.2% lower last September, but prices increased 20.2% over 2022.

Commodity prices as shared by Market Insider showed the price of copper stood at $3.46 per pound in October but rose to $3.83 in November. Aluminum prices retreated in late October, but rebounded in November at $2,434 per ton, up $198. Electrical lighting fixtures dropped 1.1% in October/November 2022.

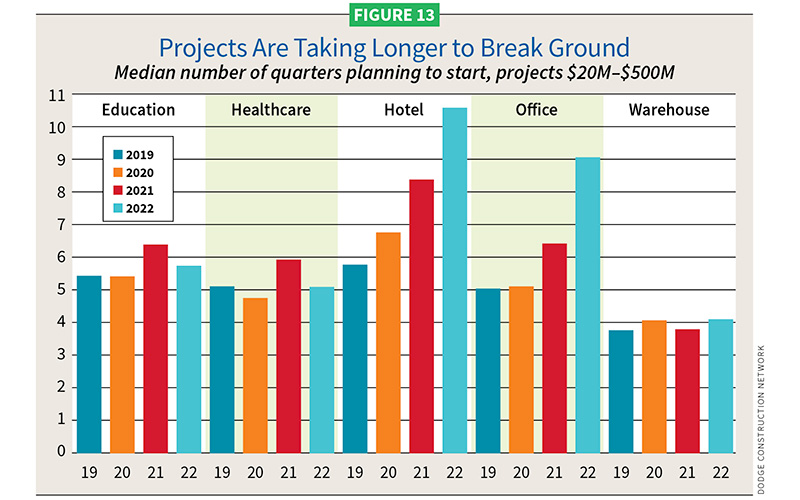

Costs have also influenced project start-to-completion timelines. Demand and market conditions might also play a role. Branch pointed to the office and hotel sectors as good examples.

“Projects are taking about a year longer to get through the planning cycle and into groundbreaking now,” he said (see Figure 13). “It would be easy to blame this on people and prices, and I’m sure that is a significant factor. There’s a demand element here, too. We know the hotel sector is recovering, but office continues to be weak.” Branch added that elongated construction cycles may at times be the result of developers waiting for market conditions to dictate project groundbreaking. In the nonresidential space, a slowing of the federal appropriations process for 2022 and 2023 has slowed federal funding for infrastructure projects. That delay trickles down to state and local communities.

“I do think federal infrastructure dollars are going to be skewed more towards funding larger projects,” he added.

Bond measures will support starts

Branch pointed to the strength of bond measures passed in November 2022 that will support construction moving forward. He named a few, including a $4.2 billion environmental bond measure for climate infrastructure in New York State, and $3.2 billion in the San Diego Unified School District for security and safety improvements. Other measures including a $1.2 billion bond in Harris County, Texas, will spread dollars toward infrastructure, safety and parks; and a $2.5 billion bond will help renovate 25 schools in Austin, Texas. Also in Texas, the $8.4 billion Transportation Road Improvement Program in Denton County is a go.

“There are a lot of bond measures here across a broad range of project types, from education to roads and bridges, to clean energy, to water and sewer,” Branch said. “This will certainly support the public side of the construction sector as we move forward into 2023.

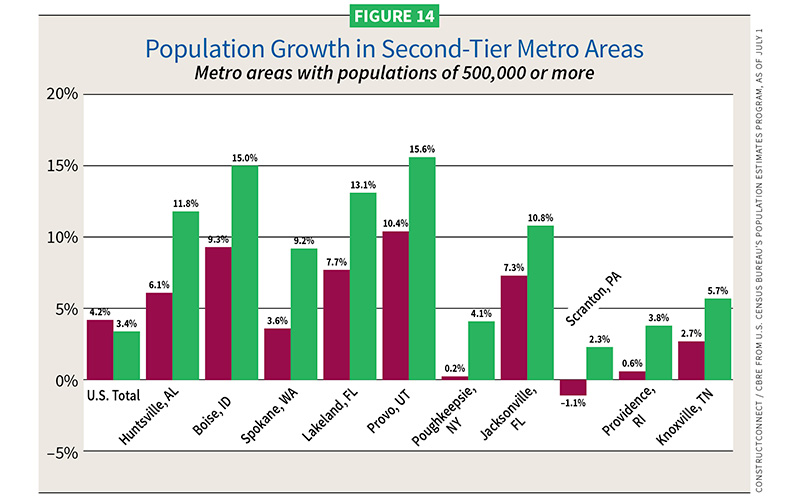

Regional population trends

Baker found little change in regional population trends, except for metropolitan-level. Comparing population changes from 2010–2015 with 2016–2021, the trends show people moving away from larger cities and into smaller, more affordable metro areas. These ”second-tier” metro areas, such as Huntsville, Ala.; Boise, Idaho; Provo, Utah; and Jacksonville, Fla., saw growth (see Figure 14). Conversely, larger cities with more expensive housing, including San Francisco and New York City, saw steep declines. Other big cities including Denver, Houston and Dallas went from strong to much more modest growth.

Regionally, Simonson found the highest population gains in the Intermountain region (between the Rockies and the Coast Mountains, Cascades and Sierra Nevadas). “We are also continuing to see growth broadly across the Southwest and Southeast. These population trends are likely to continue.”

The biggest declines in growth in less-affordable areas are in Denver; Washington, D.C.; Houston; Miami; and Dallas.

Let’s talk about residential

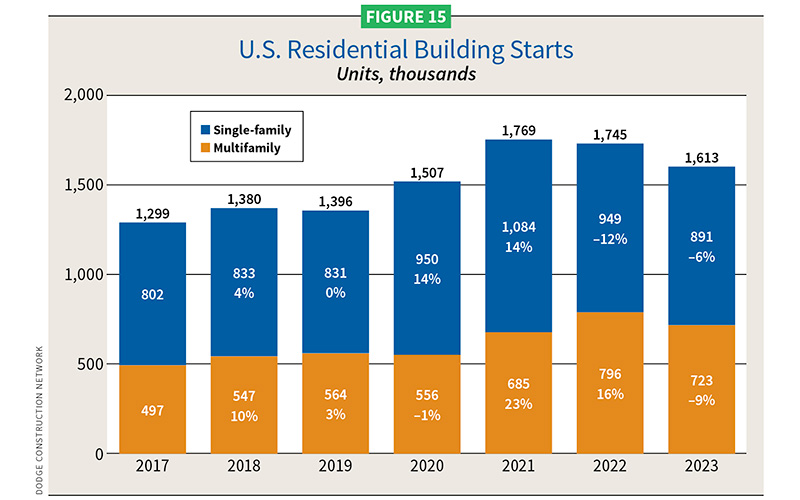

Robert Dietz, chief economist and senior vice president for economics and housing policy for NAHB, shared what most homebuilder contractors felt: “2022 is going to be the first year (since 2011) of a calendar-year decline in single-family housing starts. We are expecting to see at least a 10% decline for 2022, pushing us just below 1 million single-family starts.” He said 2021 showed a homebuilding pace of 1.1 million starts, enough to make a dent in the existing housing deficit that NAHB estimates at about a million houses nationwide (see Figure 15).

“If you look at total housing starts over the last two years, they have been about 1.5 million for each year,” Dietz said. “That was in combination with historically low interest rates to stimulate first-time buyers. We are seeing increased demand for rental investors, particularly in single-family housing to rent. Then, there was also an acceleration in household formations helped in part by the reopening of the U.S. economy.”

Dietz finds mortgage rates the biggest short-term risk for home purchasing.

“The biggest shock to the system was at the start of 2022,” Dietz said. “We quickly lifted off from a 30-year fixed rate mortgage around 3% to [end] around 7%. That’s the most rapid rise in quite a while. Our anticipated top rate as measured by Freddie Mac shows a maximum rate of about 7.5%. And then we expect interest rates to decline in the second half of 2023 and even lower in 2024. So, weakness in 2023 and then a housing rebound in 2024.”

In late November 2022, the national 30-year fixed mortgage rates stood at 6.27%; 15-year fixed was at 5.55%.

One of the bright spots for residential in 2022 was multifamily. Dietz and others had expected flat growth. Dietz forecast 2022 numbers to post around a 13% gain (about 540,000 units). “The highest in some time,” he said. “Add to that about 900,000 units currently under construction nationwide.”

What giveth, however, will be taken away this year, as Dietz expects a reversal and decline for multifamily housing due largely to an expected rise in unemployment and a slowing economy, denting demand for apartment housing and driving up vacancy rates. “That will leave a lot of inventory in the system, combined with a weakening housing demand in 2023,” he said.

In one upwind, Dietz expects continued strength in remodeling for single-family and multifamily due to an aging housing stock and people moving from their homes with less frequency while holding on to low interest rates they obtained before rates rose.

The health of residential construction correlates to the state of existing home sales.

“We expect existing home sales to be down this year (2022) and next,” Dietz said. “That makes it harder for the home seller to move up to new construction. Existing home inventory has been a key limiting factor in recent years. New construction has been about a third of single-family home inventory nationwide. Historically, new construction has only been about 13% of inventories. So, with less turnover, less resale of existing home stock, new home inventory becomes more important.”

As for material costs, Dietz sees some easing. “Lumber pricing is a key one. It peaked at $1,500 per 1,000 board feet in 2021. It has dropped to under $500. That helps. When we look broadly at residential material construction costs, a year ago those costs were rising 20%–25%. That has slowed to about a 12% year-over-year growth rate. The expectation in the coming months is a rapid decline to low, single-digit rates. There still are complaints for sure from builders about cost, but also availability of materials. An interesting shortage has emerged from our surveys. A third of builders are sharing a shortage of electrical transformers, which makes it hard to provide power to a subdivision.”

Finally, the weakening of the residential market needs to be put into some perspective, Dietz said.

“The rate of decline in 2006 through 2010 was a lot bigger,” Dietz said. “We had a severe economic recession combined with a financial crisis, and it was all centered on housing. We had over production and a supply glut, which led to deep price cuts and a huge amount of foreclosure activity. Today is more of a garden-variety cyclical downturn. If the Fed goes too far in raising rates, that will hurt.

But if we see interest rates drop to even 6%, we will see housing demand respond. Potential buyers are on the sidelines waiting for supply. I have been telling builders and land developers that from 2025 through 2030 we have a good five-year runway for building growth. So, we must wait for the Fed to complete its mission to tackle inflation.”

2023 sector forecasts

Starts information is supplied by Dodge (cited first), followed by ConstructConnect, unless otherwise noted. Due to some varying market categorization between the two companies, performance numbers can differ. We try to reconcile those differences or cite them when they occur. Also, this year square footage estimates were largely not shared. Dollars are not adjusted for inflation unless otherwise stated.

RESIDENTIAL

Holding on in a soft market

- 2022: 0%/$425B (Dodge)

–2.7%/$352.5B (ConstructConnect) - 2023: 1%/$427B (Dodge)

–0.4%/$351.1B (ConstructConnect)

Unfortunately, the residential sector is bearing the brunt of higher mortgage rates and affordability issues. Interest rates could still hover in the 6% range in 2023, but are expected to steadily decrease for a brighter 2024. It’s not a collapse, but it is an economic retrenching that feels recessionary. Single-family will feel more hurt than multifamily, which reaps better affordability, pushing demand up. Vacancy rates are at historic lows (around 5.8%).

Single-family

- 2022: –11%/949,000 units/$274B (Dodge)

–7.5%/$238.1B (ConstructConnect)

998,000 units (NAHB) - 2023: 0%/891,000 units/$274B (Dodge)

–1.5%/$234.5B (ConstructConnect)

838,000 units (NAHB)

Multifamily

- 2022: 27%/796,000 units/$151B (Dodge)

9.4%/$114.3B (ConstructConnect)

538,000 units (NAHB) - 2023: 1%/730,000 units/$153B (Dodge)

2.0%/$116.6B (ConstructConnect)

448,000 units (NAHB)

The year’s top three multifamily projects as of October 2022 are The Rise (mixed use), Cupertino, Calif. ($2.7B/3.9 million sq. feet/4 structures, 2,400 units); Bunker Hill Housing Redevelopment, Boston ($1.4B/2.8 million sq. feet/6 structures, 2,699 units/multiple units); and The Park Ward Village (mixed use), Honolulu ($620 million/2 million sq. feet/2 structures, 41 stories, 546 units).

COMMERCIAL

Winners and losers, some pullback

- 2022: 24%/$157B (Dodge)

4.8%/$112.5B (ConstructConnect) - 2023: –3%/$153B (Dodge)

4.5%/$117.7B (ConstructConnect)

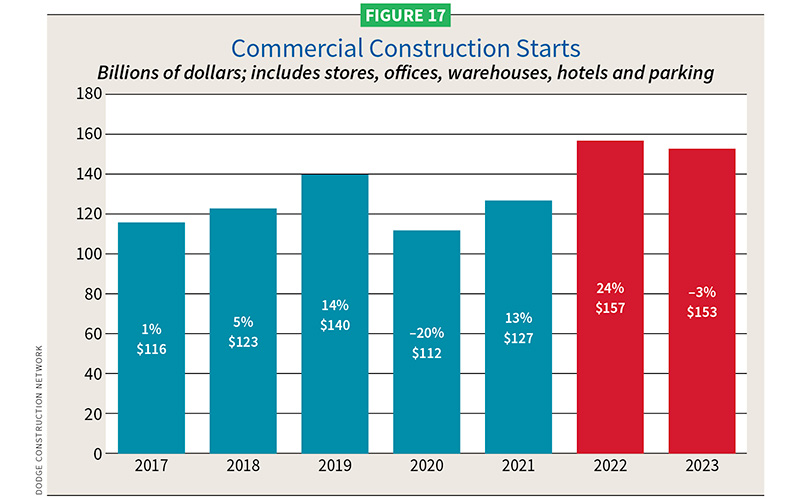

Dodge sees commercial starts dropping 3% in 2023 (–13% when adjusted for inflation) due to pullbacks in warehouse and office sectors (see Figures 16 and 17).

“Amazon is pulling out of the market, and it’s pushing the whole warehouse sector into decline,” Branch said. “There will, however, still be demand for warehouse over the next several years, particularly the high-end refrigerated warehouse buildings.” ConstructConnect also sees some decline in 2023, but smaller (–0.3%), with a gain for offices. Hotel and retail starts will offer some growth in nominal dollars (mostly luxury and upscale hotels), but will also slip when adjusted for inflation. Data center construction (part of office) will be a bright light in 2023; it is expected to stay strong for several years.

Retail

- 2022: 31%/$19.4B (Dodge)

11.7%/$14.3B (ConstructConnect) - 2023: 4%/$20.2B (Dodge)

3.8%/$14.9B (ConstructConnect)

Warehouses

- 2022: 19%/$57.1B (Dodge)

–5.9%/$26.4B (ConstructConnect) - 2023: –10%/$51.3B (Dodge)

–5.7%/$24.9B (ConstructConnect)

Hotels

- 2022: 53%/$11.9B (Dodge)

42.4%/$10.1B (ConstructConnect) - 2023: 3%/$12.2B (Dodge)

11.4%/$11.3B (ConstructConnect)

Office buildings

- 2022: 23%/$49.1B (Dodge)

–10.8%/$18.5B (ConstructConnect) - 2023: –1%/$48.8B (Dodge)

15.2%/$21.3B (ConstructConnect)

The top three commercial projects in 2022 (as of September 2022) are the Meta Hyperscale Data Center, Temple, Texas ($950 million/900,000 sq. feet); Digital Dulles Data Center 7 & 9r, Dulles, Va. ($940 million/1 million sq. feet); and Facebook Data Center Buildings 7 & 8, Los Lunas, N.M. ($800 million/1 million sq. feet).

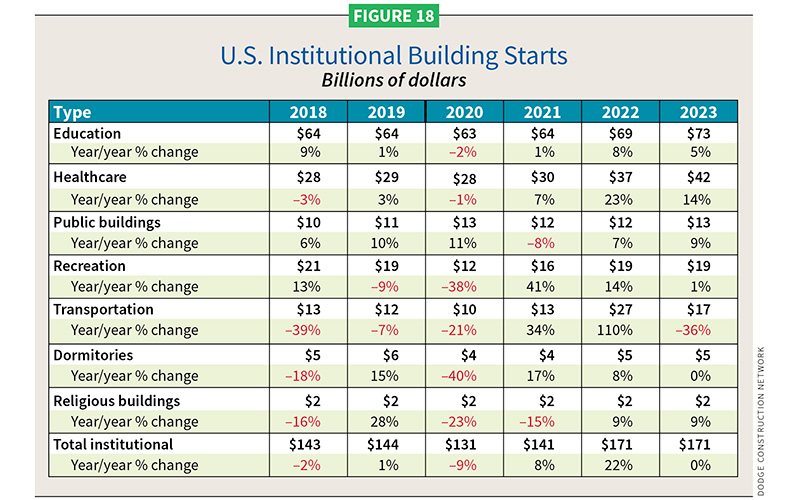

INSTITUTIONAL

Holding steady

- 2022: 22%/$171B (Dodge)

- 2023: 0%/$171B (Dodge)

ConstructConnect projections for this sector are harder to neatly quantify alongside Dodge. Its estimates are addressed below, largely within related Dodge subsectors.

Getting a boost from a strong healthcare market, Dodge sees institutional starts equaling 2022 performance, but no gains—so 0% (–1% inflation-adjusted) in 2023 (see Figure 18). Healthcare growth can be attributed to a demand for outpatient clinics and new hospitals. Starts in the educational sector (classrooms) languish as slow demographic growth weakens demand, though several bond measures for school districts passed in November are planting seeds for more growth. Life science buildings, however, have flourished and will continue to do so in the new year.

Education

- 2022: 8%/$69.0B (Dodge)

17.7%/$70.4B (ConstructConnect) - 2023: 5%/$72.7B (Dodge)

–1.2% /$69.6B (ConstructConnect)

Dodge did not break out starts figures by education markets.

Colleges and universities

- 2022 18.6%/$17.8B (ConstructConnect)

- 2023: 2.4%/$18.3B (ConstructConnect)

K-12

- 2022: 18.4%/$50.6B (ConstructConnect)

- 2023: –2.5%/$49.3B (ConstructConnect)

Healthcare

- 2022: 23%/$37.2B (Dodge)

4.7%/$33.6B (ConstructConnect) - 2023: 14%/$42.3B (Dodge)

4.5%/$35.2B (ConstructConnect)

Transportation

- 2022: 110%/$27B (Dodge)

6.0%/$10.5B (ConstructConnect) - 2023: –36%/$17B (Dodge)

3.9%/$10.9B (ConstructConnect)

Recreation

- 2022: 14%/$19B (Dodge)

0.2%/$6B (ConstructConnect) - 2023: 1%/$19B (Dodge)

43.1%/$8.6B (ConstructConnect)

Miscellaneous institutional

- 2022: 16%/$14B (Dodge)

–0.06%/$12.4B (ConstructConnect) - 2023: 18%/$18B (Dodge)

1.4%/$12.6B (ConstructConnect)

Miscellaneous institutional encompasses religious facilities; public buildings, including capitals, courthouses, police and fire buildings; detention; and other administrative facilities.

The top three commercial-related institutional projects as of September 2022 are all in New York: JFK Airport New Terminal 1, Jamaica ($9.5B/2.8 million sq. feet); JFK Airport New Terminal 4 Expansion, ($1.5B/150,000 sq. feet); and Metro-North Penn Station ($1.3B/1 million sq. feet).

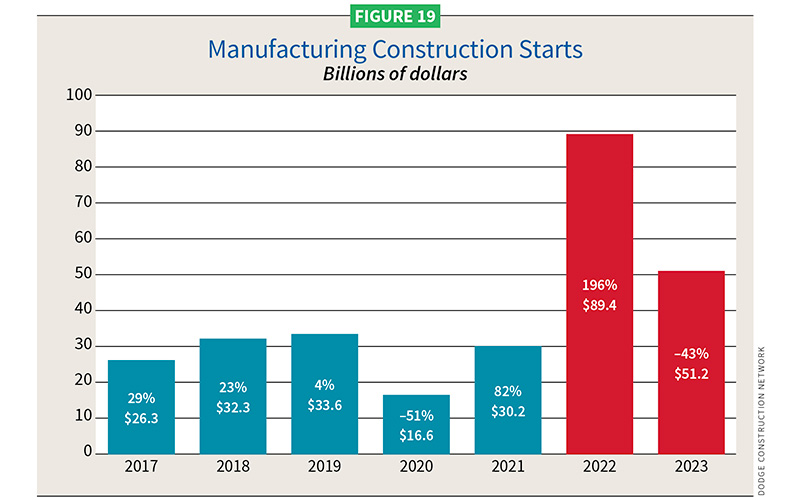

MANUFACTURING

- 2022: 196%/$89.4B (Dodge)

135.3%/$81.8B (ConstructConnect) - 2023: –43%/$51.2B (Dodge)

–37.1/$51.4B (ConstructConnect)

Manufacturing starts will decline by as much as 43% in 2023 (see Figure 19), which sounds like a miserable statistic. While it’s a decline, $51B represents a figure not seen by Dodge since 1967, that is, until last year’s $89.4B. You can attribute this robustness in manufacturing starts to reshoring efforts that have led to several chip fabrication plants, EV battery plants and other large facilities breaking ground. The CHIPS and Science Act and IRA will supercharge activity in this sector for several years.

Capacity utilization in the United States moved up 0.2 percentage points to 80.34% in September 2022, above market expectations of 80.0% and 0.7 percentage points above its long-run average. It is the highest rate in 14 years. It retreated a bit to 79.9% in October. Meanwhile, the capacity utilization rate for nondurable goods manufacturing increased to 82.1%, the highest since 1998. Capacity utilization measures the rate at which potential output levels are being met or used.

A few noteworthy starts in 2022 included the Texas Instruments Semiconductor Wafer Fabrication Plants in Sherman, Texas (470,000 sq. feet/$15B); General Motors Lansing (Mich.) Battery Cell Manufacturing Plant (259,000 sq. feet/$7B); and Ford Motor Co. Industrial BlueOvalSK Battery Park, Glendale, Ky. (5 million sq. feet/$5.8B).

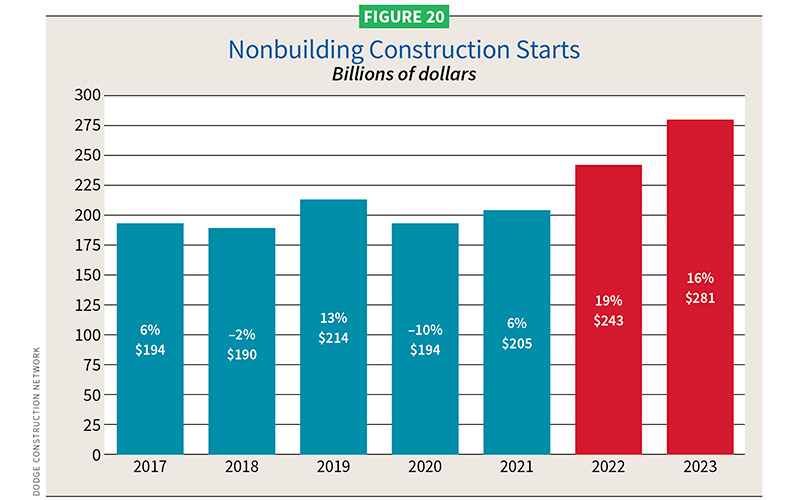

NONBUILDING

Stimulus supports robust growth

- 2022: 19%/$243.1B (Dodge)

22.7%/$192B (ConstructConnect) - 2023: 16%/$281.1B (Dodge)

6.9%/$205.4B (ConstructConnect)

Public dollars through IIJA will raise all boats in nonbuilding/infrastructure projects. Dodge expects starts in public works to gain 16% in 2023 (+12% adjusted for inflation) led by growth in streets and bridge work (see Figure 20). Power and utilities will advance 8% (+2% inflation-adjusted), benefiting from an extension of the IRA’s investment and production tax credits assisting utility-scale wind and solar projects. ConstructConnect projections are similar, though divergent in percentages and dollars, at times.

Streets/highways and bridges

- 2022, bridges: 25%/$22.2B (Dodge)

53.9%/$27.6B (ConstructConnect) - 2023, bridges: 20%/$26.6B (Dodge)

–3.4%/$26.7B (ConstructConnect) - 2022, streets and highways:

23%/$78.6B (Dodge)

27.3%/$85.8B (ConstructConnect) - 2023, streets and highways:

20%/$94.4B (Dodge)

2.9%/$88.3B (ConstructConnect)

See Figure 21.

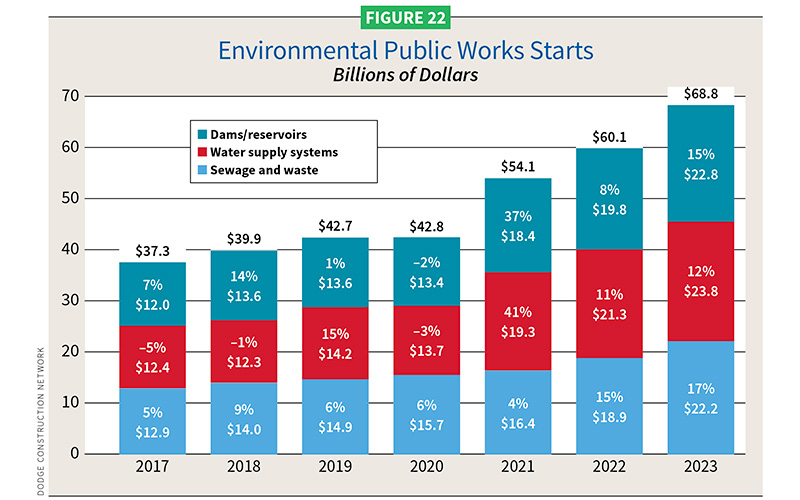

Environmental public works

- 2022, dams and reservoirs: 8%/$19.8B (Dodge);

5.1%/$8.9B (ConstructConnect) - 2023, dams and reservoirs:

15%/$22.8B (Dodge)

5.6%/$9.5B (ConstructConnect) - 2022, water supply systems:

11%/$21.3B (Dodge) - 2023, water supply systems:

12%/$23.8B (Dodge) - 2022, sewage and waste:

15%/$18.9B (Dodge) - 2023, sewage and waste:

17%/$22.2B (Dodge)

See Figure 22.

ConstructConnect combines water and sewage treatment: 19.87%/$40.6B (2022); 0.9%/$40.2B (2023).

Power and utilities

2022: 27%/$52.5B (Dodge)

4.1%/$8.6B (ConstructConnect)

2023: 8%/$56.4B (Dodge)

81.9%/$15.7B (ConstructConnect)

The year’s top three nonbuilding projects as of September 2022 are South Fork Wind Farm, East Hampton, N.Y. ($2B); the Texas Department of Transportation’s I-35 NEX Central Project, San Antonio ($3B); and the New York State Department of Transportation’s Van Wyk Expressway Capacity and Access Improvements, JFK Airport Project—Contract 3, New York ($804 million).

SUMMARY

Inflation and world affairs will play an outsized role on the economy this year. And while economists can only say the chances for a recession in 2023 have increased, even without a formal recession, some construction sectors will certainly feel “recessionary.” Some sectors with strong enough starts will help balance out weaknesses, such as residential. That sector will take it on the chin with higher mortgage rates and single-family affordability issues. Manufacturing should be another bright spot in 2023, even with a decline. The commercial sector will have winners and losers, but will see some continued growth in hotels and brick-and-mortar retail against a backdrop of strong but weakening warehouse demand. Data centers will help a challenged office sector. Institutional should hold its own. Nonbuilding construction will remain very strong, helped by various government stimulus programs.

In 2023, if every puzzle piece falls into place to the advantage of the U.S. economy, inflation will slow. Averaging out all construction, starts will be sluggish this year, but we can look forward to a stronger foundation for 2024.

Header image source: Bonotom Studio Inc. / Shutterstock / Kseniya Sazonova

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].