You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

Part I: The Paradox

As the economic landscape of the electrical industry shifts from industrial to commercial/residential, the contractors demand more effective services from their supplier/distributors. Every day owners and operators of electrical distributors must face the question: Who are we? Are we our manufacturer’s distributors or our customer’s suppliers? Why is it so difficult to answer this question?

A contractor’s ordering behavior and communication have a major impact on its supplier/distributor and their role in the installation process.

Based on 15 years of research in various industries including distribution and electrical construction, we will answer the question and recommend a multifaceted strategy that allows electrical contractors and distributors to be able to operate profitably as both a distributor and a supplier in a more streamlined supply chain operation.

Electrical distribution is facing a shift across the entire industry. Manufacturers and contractors are circumnavigating distributors, buying and selling directly and in bulk, and acting in direct competition with their traditional distributors. Home Depot is emerging as a serious competitor. Material purchasing by the general contractors and owners do not help the situation from either the distributor’s or the contractor’s cost and profit perspective.

In this coming series of articles, we will shed light on the supply versus distribution paradox and cover these areas:

1. Distribution and suppliers have different needs—What are they?

2. Manufacturers and contractors also have different requirements—What are their requirements?

3. Underlying operations and cost drivers are different between distributors, manufacturers, contractors, owners, general contractors and architects.

a. What are their cost drivers? How are they different?

b. How do these differences impact the distributor’s operation?

4. How should distributors structure their companies? What strategies are needed to support the contradictory and opposing needs of their core stakeholders and constituencies? Is partnership a viable option? If so, with whom: manufacturers, contractors, or general contractors?

The beginning of the paradox

“The relationship in the electrical construction material procurement channel has an antagonistic nature.” This was the hypothesis that was used to open MCA Inc.’s research into “Procurement Chain Management for the Construction Industry” (P. Daneshgari and S. Harbin, 2004).

Our findings in that and subsequent research conducted by MCA Inc. for the National Association for Electrical Distributors’ (NAED) Education and Research Foundation showed this relationship, and the ensuing mistrust between the parties, was rooted far deeper than it initially appeared. The differences between the operational philosophies underlying this antagonistic relationship have deep historical roots.

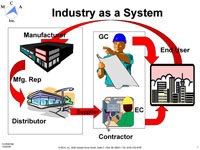

The material supply chain for the electrical construction is depicted in Figure 1. The distributor provides the connection between the manufacturers (upstream) and the owners, specialty contractors and general contractors (downstream).

In the role of distributor, an electrical distributor focuses on the upstream portion, distributing materials for a number of specific manufacturers. The historical role the distributor played was exactly that. Its alliance lay with its manufacturer; the distributor was a known provider of those materials that were available from its manufacturers.

In the role of a supplier, an electrical distributor shifts to a service-based function to address the needs of the downstream customers. As a supply house, the distributor is a partner or an ally of its customers, the contractors. It assists its customers not simply by distributing materials for a couple of manufacturers, but by supplying its customers with the right materials, in the correct packaging, at the right time, and in the right place. To provide these services may require sourcing, expediting, coordinating, special deliveries and many other material management functions.

Why does this distinction matter?

The historical distribution model worked well when the electrical contracting market was heavily industrial and OEM was a large component of the work. The end-users were known, as were the required materials. Manufacturers mass-produced materials, and electrical contractors used a highly skilled work force to install the materials in support of an expanding industrially based economy. The distributor only needed to provide the connection between the manufacturer and the contractor by delivering or arranging the delivery of materials.

Contractors often warehoused their materials either at their own location or on the job site itself. Large contractors would carry more inventory than the local distributors. In effect, the contractors were acting as their own suppliers. By maintaining control of the entire inventory needed for a project, the contractor could supply its own work force with the materials they needed at the right time and place.

In addition, contractors operated under a “cost plus profit” model: pricing their work by identifying the price of materials and labor and adding a profit margin. To make money, distributors simply had to line themselves up with the right manufacturer and distribute their products at a cost-plus-profit price for the contractors to resell.

The shift

In a shift almost undetected by either the contractors or the distributors, the electrical construction market entered a changing phase beginning in the 1970s. The electrical construction market expanded in size, as shown in Figure 2. Manufacturing gradually became a smaller and smaller contributor to the gross domestic product. Simultaneously, the electrical construction market was transforming from industrial work to commercial and residential construction to accommodate expanding electrical needs in the nonindustrial segments. Commercial and residential components now make up almost 60 percent of the electrical construction market.

The market has shifted but not the players. Distributors continue to align themselves with manufacturers, dictating the products. Manufacturers reward distributors who support their products by offering rebates to the distributors for large volumes of sales.

To compete in the residential and commercial markets, the contractors needs have changed. Technology has sped up everything from communication to transportation. In 1970, the nearest phone to the job site was on average five miles away; today, it is on the tool-belt. For the right price, materials from anywhere in the country can be on hand the next day, and almost as quickly from anywhere in the world. More than ever, contractors need suppliers instead of distributors.

A contractor’s agility is limited by its ability to respond to the changing job site, and this is affected in large part by its ability to have the correct materials in hand at the required time, even in the face of job site changes.

What is the impact of this shift on the distributor’s profits and operations?

We will look at this in the next article as we examine the needs and requirements this shift has placed on the key players in the supply chain. EC

DANESHGARI is president of MCA Inc. He is a consultant for various electrical and general contracting companies. WILSON, a professor at Franklin University, is the director of research for MCA Inc.