The news of a reviving economy continues to gain currency. By year’s end, a gross domestic product (GDP) of 6% or more is expected. While recognizing we are climbing out from a –3.5% GDP low in 2020, the economy seems ready to run. An infrastructure bill could further fuel appreciable growth into 2022 and beyond.

In analyzing an improving 2021, economic forecasters have been offering updates. Though the 2021 recovery will remain uneven in the construction industry, we are strikingly close to a pre-pandemic economic return.

In its “2021 Construction Outlook,” presented in Nov. 2020, Dodge Data and Analytics, Hamilton, N.J., forecast total construction activity at $771 billion. Dodge’s chief economist Richard Branch has conservatively raised that forecast by nearly $1 billion (0.8%) based on the economic lift provided by the $1.9 trillion American Rescue Plan Act of 2021 enacted in March. For its part, ConstructConnect, Cincinnati, forecasts 2021 total construction starts at nearly $740 billion.

In terms of GDP, Dodge anticipates 6% by year’s end. ConstructConnect has estimated higher at 7.2%. Both forecasts expect growth to continue in 2022 as nonresidential building recovers. ConstructConnect has already estimated total construction gains of 12.2% ($829.8 billion) for next year.

“I don’t think our 2021 forecast change (4.8%) has materially affected our starts projections,” Branch said. “The initial forecast assumed the U.S. would be well on its way to vaccine deployment and herd immunity by midyear. In real dollar terms (adjusted for inflation), we have made real significant progress off the low of February 2020. In total construction, which includes residential, we have gained 21% off the low of fourth quarter 2020. We do remain 7% below 2019 year-over-year (y/y) but see pent-up spending in the second half of the year as the ‘horse leaves the barn’ and starts running.”

Branch expects vaccine distribution and additional stimulus will accelerate economic growth this year, pushing the economy, including a rebuilding of inventories and allowing businesses to invest in people and processes. Further, he estimates a pre-pandemic economy will return around mid-year.

“That does not mean every sector will recover along the same path,” he said. “It will take time for a construction industry recovery to dig in, take hold and gain traction.”

The economy to date

Stabilization is how Branch describes the economy to date. The late-2020 $900 billion COVID-19 relief stimulus steadied the economy through February 2021, he said. By the end of the first quarter of 2021, the U.S. economy grew at an annual rate of 6.4%. Though growth rates for the second quarter were not available as of this writing, analysts at brokerage firm Charles Schwab expected a jump to 9.4%, followed by third and fourth quarters at 6.8% and 4.8%, respectively. Spending on goods picked up and consumption of services has held steady. The $1.9 trillion American Rescue Plan Act of 2021, enacted in March, may do more.

Alex Carrick, chief economist for ConstructConnect, put it this way: “The March program injected more money into the economy and could really stimulate growth.”

The American Rescue Plan Act of 2021, in part, is being credited with stimulating consumer spending. The U.S. Bureau of Economic Analysis reported spending grew at an annualized 11.3% (upwardly revised) in the first quarter of this year.

Dodge reported, “Excluding last year’s third quarter (which saw an astounding bounce-back following the second quarter’s drop), this was the strongest quarterly growth rate for consumer spending since 1965.”

In March, employers added 916,000 jobs. April disappointed, adding only 266,000 to the workforce and raising unemployment slightly from 6.0% to 6.1%. In May, employment rose to 559,000 and dropped unemployment to 5.8%. The U.S. Bureau of Labor Statistics (BLS) reported May’s notable job gains involved leisure and hospitality, public and private education, and healthcare and social assistance. This back-and-forth of gains and losses speaks to this economic recovery’s fluidity.

In looking at April’s numbers, Carrick said, “Total U.S. employment in April was +10.9% [year-to-date]. In services, the y/y jobs jump was +14.0%; in manufacturing, +7.6%; and in construction, +14.0%.”

For May, Carrick reported on-site construction employment shrunk by 20,000 jobs, most of which was attributed to nonresidential subtrade contractors.

Dodge reported that total construction starts “dropped 1% in May to a seasonally adjusted annual rate of $902.8 billion.” Much of the decline was due to residential starts, but nonresidential and nonbuilding starts continued to recover.

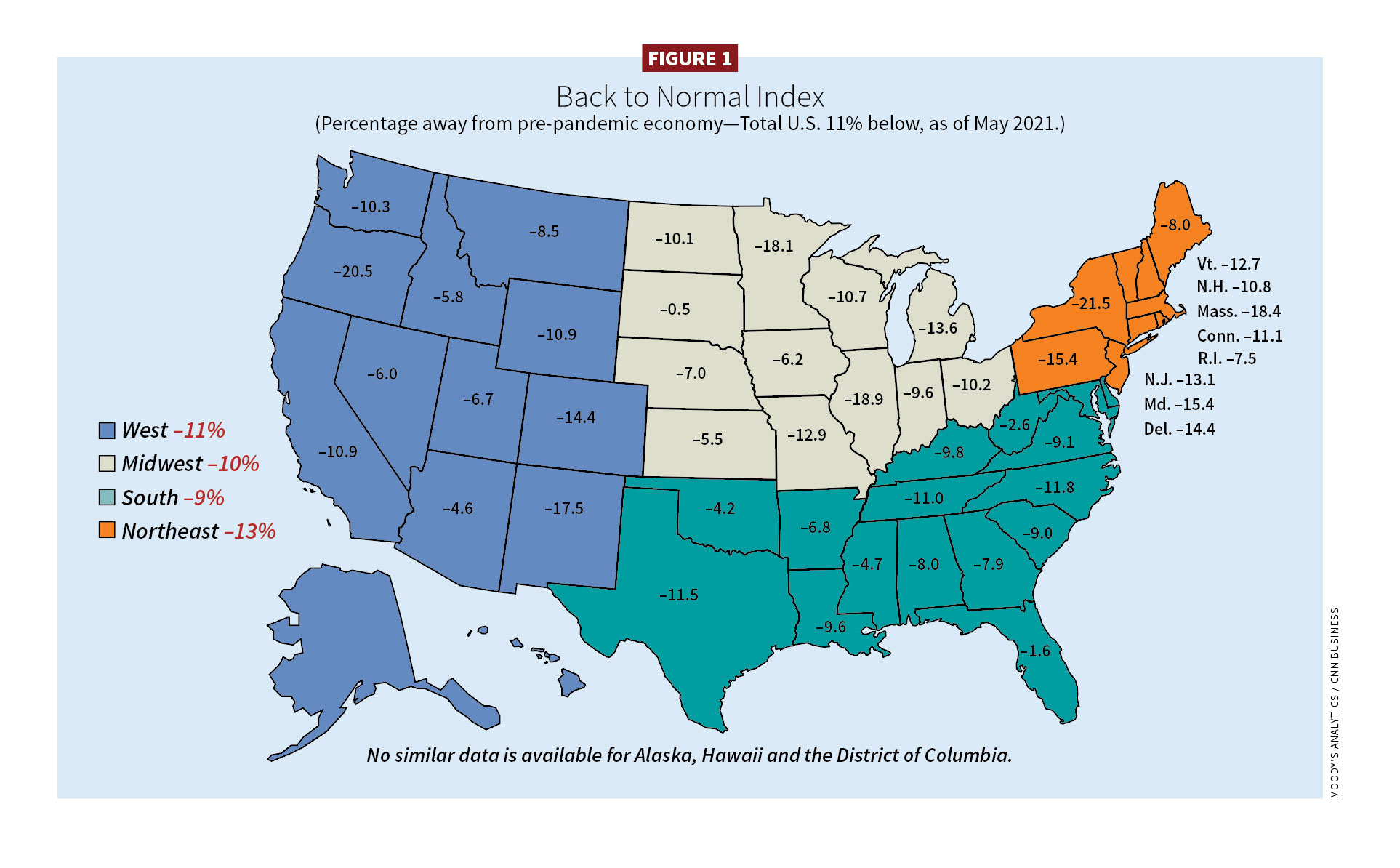

Regional disparity will also continue to be part of the story as the economy recovers (see Figure 1). Branch shared that the Pacific Southwest (California, Arizona and Utah), West North-Central (Minnesota, Kansas, Nebraska and the Dakotas) and East South-Central (Alabama, Tennessee and Mississippi) regions are closest to getting back to pre-pandemic levels. The Mid-Atlantic region (New York, New Jersey and Pennsylvania) is furthest out from recovery.

Sectors in general

In first quarter 2021 performance, ConstructConnect reported total U.S. construction starts fell 12.4% y/y. Nonresidential took the hardest hit by falling 27.5%. One bright spot was healthcare construction, growing 6.3%. Residential construction remained robust as it related to new single-family homes (7.7%) but contracted 1.2% overall based on weak multifamily residences. Total construction put-in-place spending grew 5.8% y/y (April).

In residential construction, the U.S. Department of Housing and Urban Development and the U.S. Census Bureau reported March sales of newly built, single-family homes rose 20.7%. That growth raised new construction y/y to 1.02 million units. By April, sales shrank 5.9% (863,000 units), though continued to reflect this construction mini-boom shown in a y/y gain of 48.3%.

Regionally, March numbers from the National Association of Home Builders (NAHB), Washington, D.C., showed new home sales y/y declined 3.3% in the West but rose 36.6% in the Northeast, 53.9% in the Midwest and 50.5% in the South. NAHB also reported the remodeling industry has fully recovered from the pandemic.

Looking to nonresidential, the Dodge Momentum Index in May stood at 178.0, a 9.1% increase from a revised April reading of 163.2 (the most recent numbers available as of this writing). April’s reading hit a 12-year high led by institutional planning, including healthcare and laboratory project planning (50% higher y/y). May’s jump was driven by a 15.5% advance in commercial planning, which posted its strongest month-over-month increase since October 2017. Institutional fell by less than one percentage point in May, remaining at strong levels not seen since 2009. On a year-over-year basis, commercial and institutional planning were up from May 2020 (38% and 47% respectively). The index overall was also 41% higher than in May 2020.

“If you removed warehouse activity, the momentum index would look very different,” Branch said. “So maybe a K-shaped recovery in nonresidential building where some sectors are performing well versus others.”

Warehouse construction is expected to break records. From $33 billion in 2020, it is projected to grow 14% to $37.5 billion in 2021 and an additional 7% to $40.1 billion in 2023. The top owner for warehouse construction for the last three years has been Amazon Inc., which spent $6.7 billion. Seefried Industrial Properties, an Atlanta-based industrial developer, spent $4 billion, and commercial real estate firm Northpoint Development, Savannah, Ga., spent $3.1 billion.

Branch shared that office projects are essentially flat, and planning for retail and hotel projects is down.

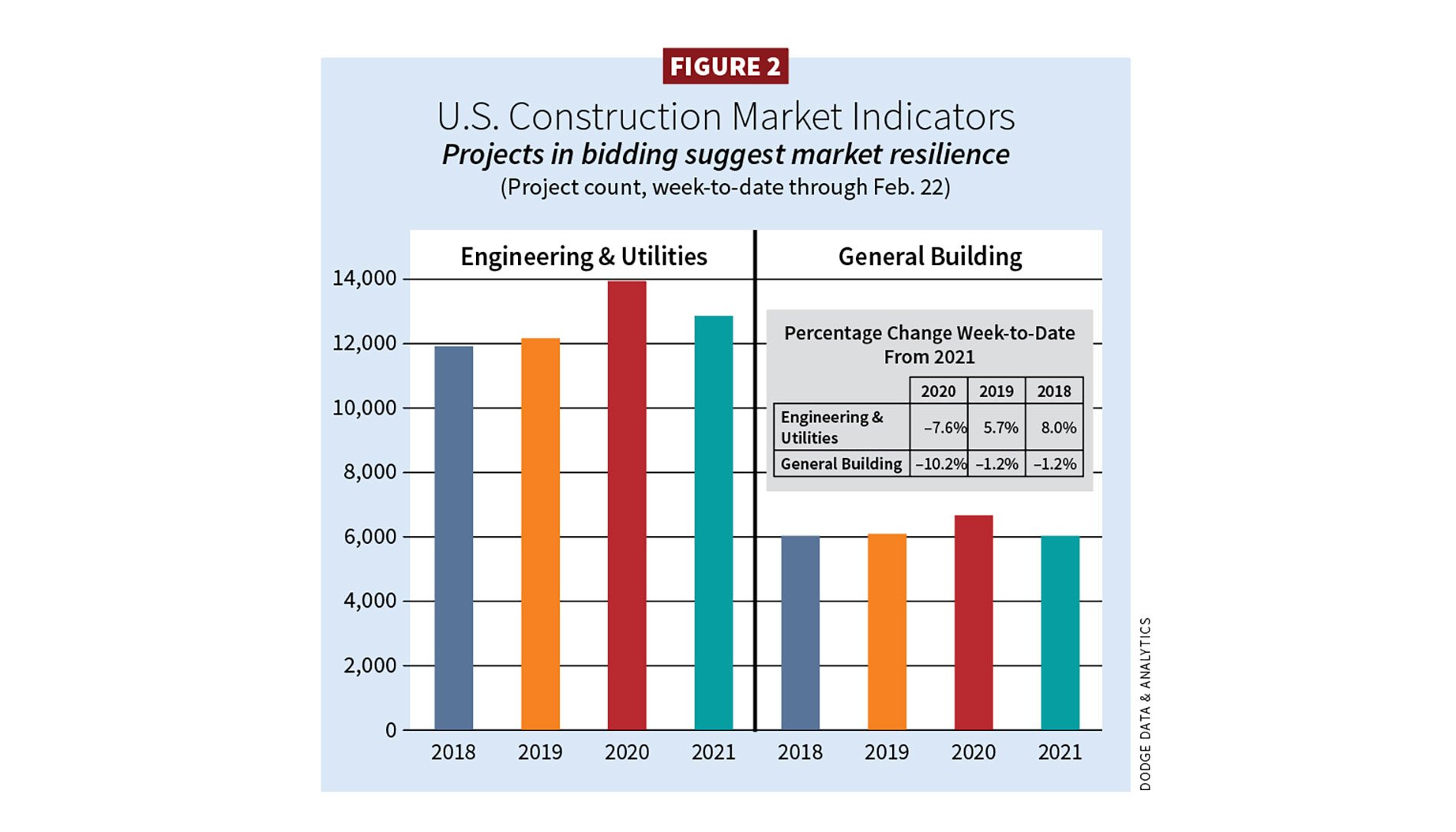

“The raw number of projects in bidding does, however, suggest market resilience,” Branch said. “Bidding numbers are on par from where we were in 2018 and 2019, which were strong for the construction sector. I think, going forward, 2021 recovery levels will be much more favorable.” (See Figure 2.)

In another encouraging measure, the American Institute of Architects’ (AIA) Architecture Billings Index score for April rose to 57.9 from 55.6 in March (any score above 50 indicates an increase in billings). March marked the first time in three years that all building sectors and regions posted positive scores. April scores for new project inquiries and new design contracts rose to 70.8 and 61.7, respectively. Sector scores included commercial/industrial (59.1), institutional (56.7) and residential (56.9). Regional averages were as follows: Midwest (60.6), South (58.3), West (52.4) and Northeast (55.0).

“The activity architecture firms are seeing is a positive bellwether not only for the construction outlook but also for the larger economy,” said Kermit Baker, AIA chief economist. “It does appear we turned the corner in design activity. Firms also showed a strong jump in backlogs, looking quite like 2017, 2018 and 2019.”

The challenge of rising costs and a tight job force

Branch added, aside from COVID, he sees one of the biggest speed bumps to recovery being rapidly rising material costs.

“The Producer Price Index for construction materials is currently 24% higher than it was in April 2020,” he said. “Lumber and metal prices continue to be the driving force behind this increase. We did see similar rates of inflation in 2017–18, but back then the U.S. economy was in much better shape. This price inflation is likely to remain elevated through 2021.”

In a May 2021 survey for the NAHB/Wells Fargo Housing Market Index, 28% of builders reported material costs increasing by 20%–30% over the past year. Another 15.9% indicated that costs increased by 30%–40%; 5.9% said costs rose by 40%–50%, and 15.2% indicated their costs increasing 50% or more. On average, the 12-month increase in material costs for the same house was 26.1%, which was by far the highest percentage cost increase ever recorded in an NAHB survey. The previous record was 6.1% in 2017.

“With building material pricing, the challenge for builders in 2021 will be to deal with higher input costs while making sure home prices remain within reach for American home buyers,” said Danushka Nanayakkara-Skillington, assistant vice president of forecasting and analysis, NAHB. The remodeling industry also faces the same stressors.

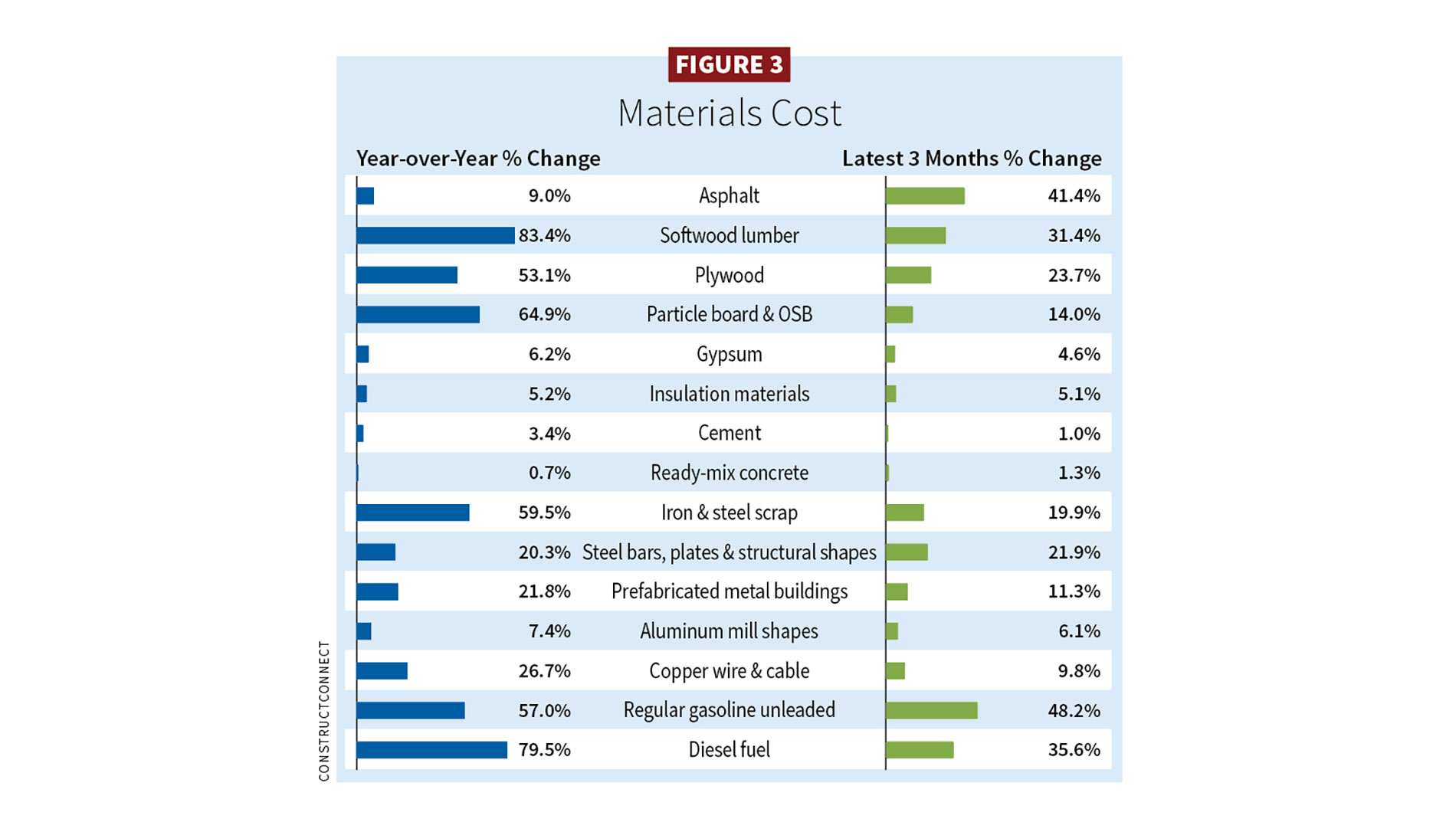

The Producer Price Index results for March vividly show material inflation. The cost of softwood lumber rose 83.4% y/y and 31.4% (January–March 2021). Following the same measures, plywood cost went up 53.1% and 23.7%; particleboard and OSB rose 64.9% and 14.0%; costs of iron and steel scrap used in steelmaking elevated 59.5% and 19.9%; steel bars, plates, and structural shapes went up 20.3% and 1.9%; and copper wire and cable cost climbed 26.7% and 9.8% (see Figure 3).

“These material cost increases, steep as they are, tell only part of the story,” said Ken Simonson, chief economist for Associated General Contractors of America (AGC). “They fail to capture the notices contractors are receiving daily about longer lead times, shipments held to a fraction of previous orders, and other challenges.”

Branch feels the construction sector will struggle to gain traction.

“Prices alter the calculus of a ‘go/no-go’ when projects are put out for bid, especially on the public building side,” he said. “This is a downward risk for our forecast [Dodge] and will be monitored very closely.”

In some promising news, on June 21, 2021, the New York Times reported a surge of production at an estimated 3,000 U.S. sawmills. In addition, futures for lumber prices, though high, did drop 45% in June. Materials inflation could be partly attributed to a mismatch between supply and demand.

Construction employment is another important factor to a construction recovery. In April, the BLS reported employment in the industry was 917,000 y/y, reducing employment from 16.6% to 7.7%. Adding in the May 2021 contraction of 20,000 jobs, BLS reported construction employment is still 225,000 lower than numbers from February 2020.

AGC reported residential construction firms (new housing, additions and remodeling) added a disappointing 3,000 employees in April but did add 46,000 workers (1.6%) over 14 months. However, the nonresidential sector lost 3,000 jobs in April, employing 242,000 fewer workers (5.2%) than in February 2020. Construction employment declined in 203 metro areas from March 2020 to March 2021.

“Employment has stalled,” Simonson said.

In terms of wages, there was some good news in April.

“The ‘all jobs’ wage hikes calculated by the BLS for the latest month were +0.3% hourly and +2.7% weekly,” Carrick said. “Construction workers did considerably better at +3.8% hourly and +7.1% weekly.”

“Despite strong demand for new homes, remodeling of all types, and selected categories of nonresidential projects, it suggests that contractors cannot get either the materials or the workers they need,” Simonson said.

He added that several firms reported key materials either backlogged or rationed, while others have reported a resistance from former workers to returning to work. Simonson feels such factors are contributing to rising costs for many contractors.

The impacts of an infrastructure plan

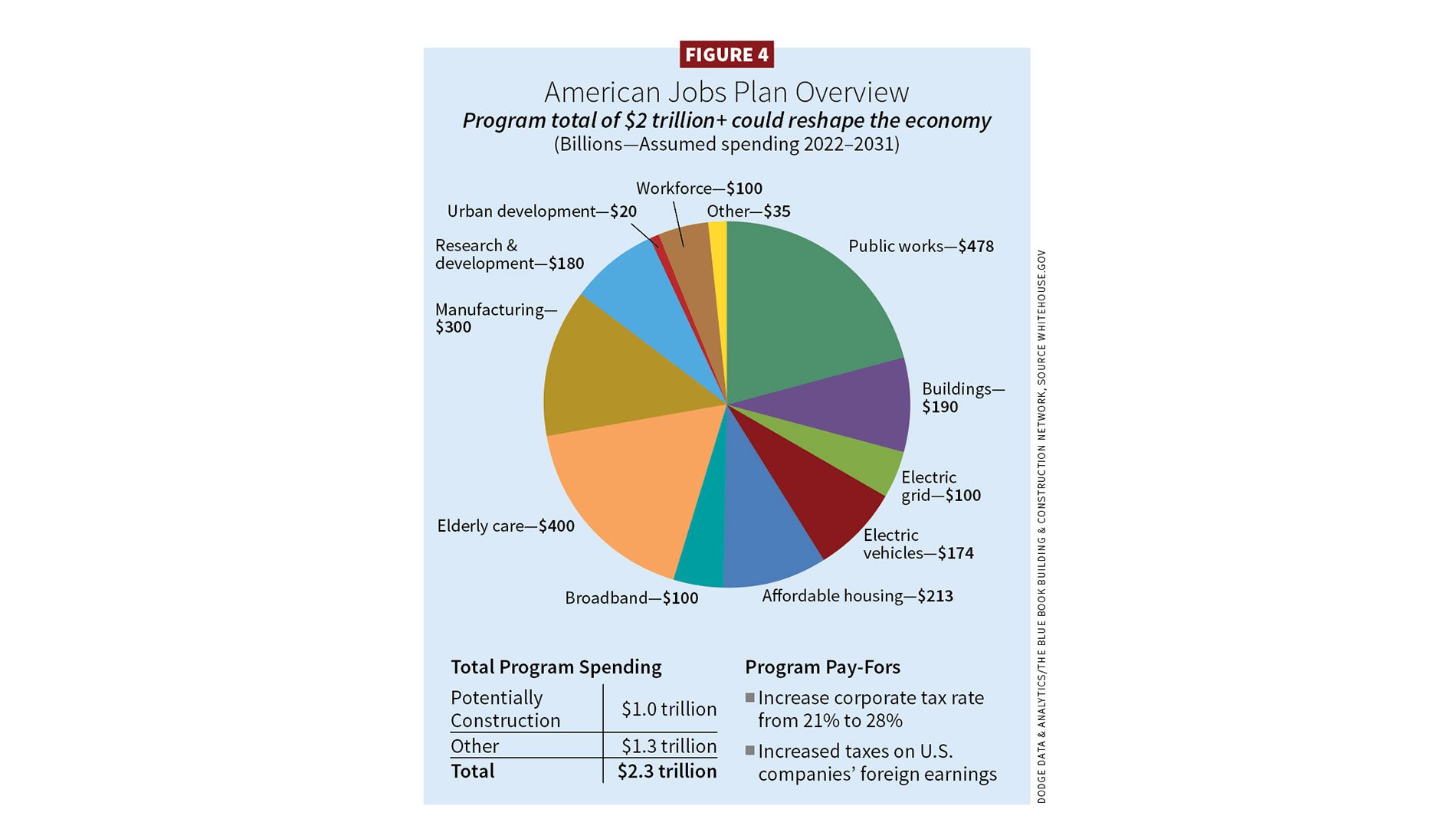

President Joe Biden’s original $2.3 trillion American Jobs Plan (AJP), a 15-year program, has sought to stimulate spending on traditional infrastructure, such as roads and bridges, as well as nontraditional forms of infrastructure. That includes spending on electric vehicle infrastructure ($174 billion), greening the power grid and adding resiliency ($100 billion), clean-energy manufacturing ($46 billion) and additional technology-driven research to address climate change ($35 billion). Tax credits to support renewable energy and storage were also part of the AJP (see Figure 4). In early June, Biden offered to cut more than $1 trillion from his initial $2.3 trillion proposal. Republicans offered $928 billion (a mix of new and existing spending), up from a narrower $568 billion offer, though still focused on roads, transit systems, airports and broadband internet over a five-year period. Biden rejected that counteroffer.

While the AJP could be scaled back from its original proposal, Branch felt the chances of nothing being passed as low (10%). He tackled the bill in a webcast, “Infrastructure Program Construction Starts Impact,” presented on April 27, 2021.

“If enacted in whole, it [the original AJP] would have a profound impact on the economy and the construction industry in particular,” Branch said.

Branch added that even a scaled-down AJP would positively affect construction starts, especially civil sectors. To better plug in impacts into its construction forecasts, Dodge input its best guess of a compromise bill set at $550 billion.

“Our proprietary econometric model suggests that public works starts would increase by nearly 50% from 2021 through the end of our forecast window in 2025, up from a 17% growth rate in the previous version of the forecast released in January,” Branch said. “This growth is equally shared across the public works sectors. Nonresidential buildings would also see some support through additional funds for education, healthcare and federal buildings, but the impact is more muted.”

Branch expects a plan to pass by fall 2021, with the first impacts felt in 2022.

The effects of COVID-19 remain front and center. Achieving higher vaccination rates and nearing herd immunity are central to economic projections and performance this second half of 2021. However, a return to normalcy does seem within reach, with continued growth in 2022.

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].