Delays are aggravating. The rescheduled flight or late train causes frustration. Rising to the top of the list—the unfinished economic recovery from COVID-19. In 2021, strong fiscal growth paused due to the rapid spread of the delta and omicron variants. Added to that was pandemic-related fallout from a hampered supply chain and unexpectedly high inflation. While such variables continue to loom, indicators are showing a full economic recovery later in 2022. The construction industry will bounce back more slowly, but recent outlooks show gains in every sector. If patience is a virtue, we should reap its rewards this year.

This article uses data forecasting from several companies. Included is material shared in two Nov. 3, 2021, presentations: Dodge Construction Network, Hamilton, N.J., in its 83rd annual Dodge Construction Industry Outlook, which also featured Moody’s Analytics, New York; and ConstructConnect, based in Cincinnati, which brought together its own chief economists and those from the American Institute of Architects (AIA), Washington, D.C., and the Associated General Contractors of America (AGC), Arlington, Va.

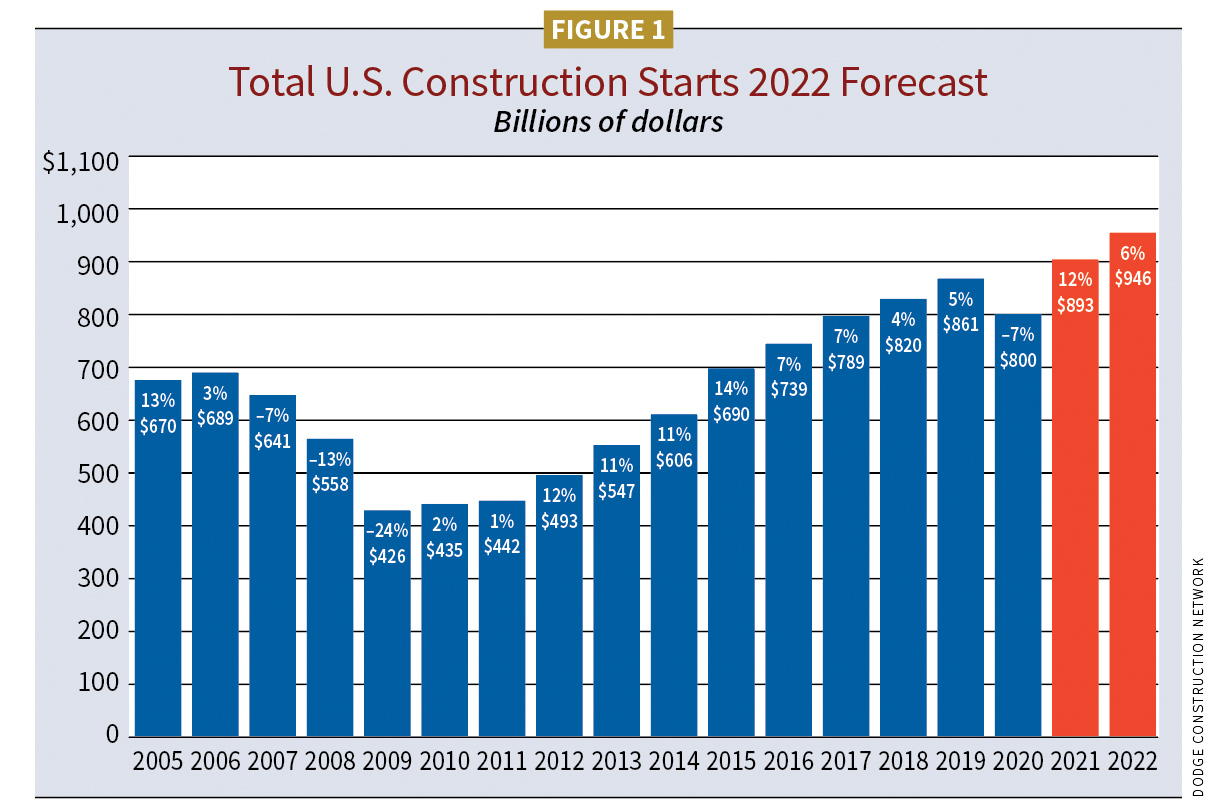

Dodge Construction Network found the dollar value of total construction starts in 2021 grew by 12% to $893 billion, a turnaround from –7% ($800B) in 2020. Much of this growth was due to the residential sector. ConstructConnect estimated 6.7% ($753B), a nice rebound from its 2020 estimate of –15%. This year, Dodge forecasts 6% ($946B), while ConstructConnect sees 12% ($842.5B) (see Figure 1).

Economists based their forecasts on some assumptions, including the successful passage of the Infrastructure Investment and Jobs Act, which was signed into law on Nov. 15, 2021; increased vaccination numbers and lower severe COVID-19 infection rates; and manageable inflation. Raising the federal debt limit (paying previous bills owed) and avoiding a December 2021 government shutdown were two others. So, projections are “this” if “that” doesn’t happen. One constant is labor shortages. Supply-chain constraints will dog the industry for at least half the year.

“I think it’s very clear, if not for the challenges including the shortages we are facing in labor and materials, that construction activity would be much stronger,” said Richard Branch, chief economist, Dodge Construction Network. Add COVID-19, and Paul Hart, vice president of product marketing for data innovation at ConstructConnect, said, “The near-term future is shaped by what we went through over the last 21 months.”

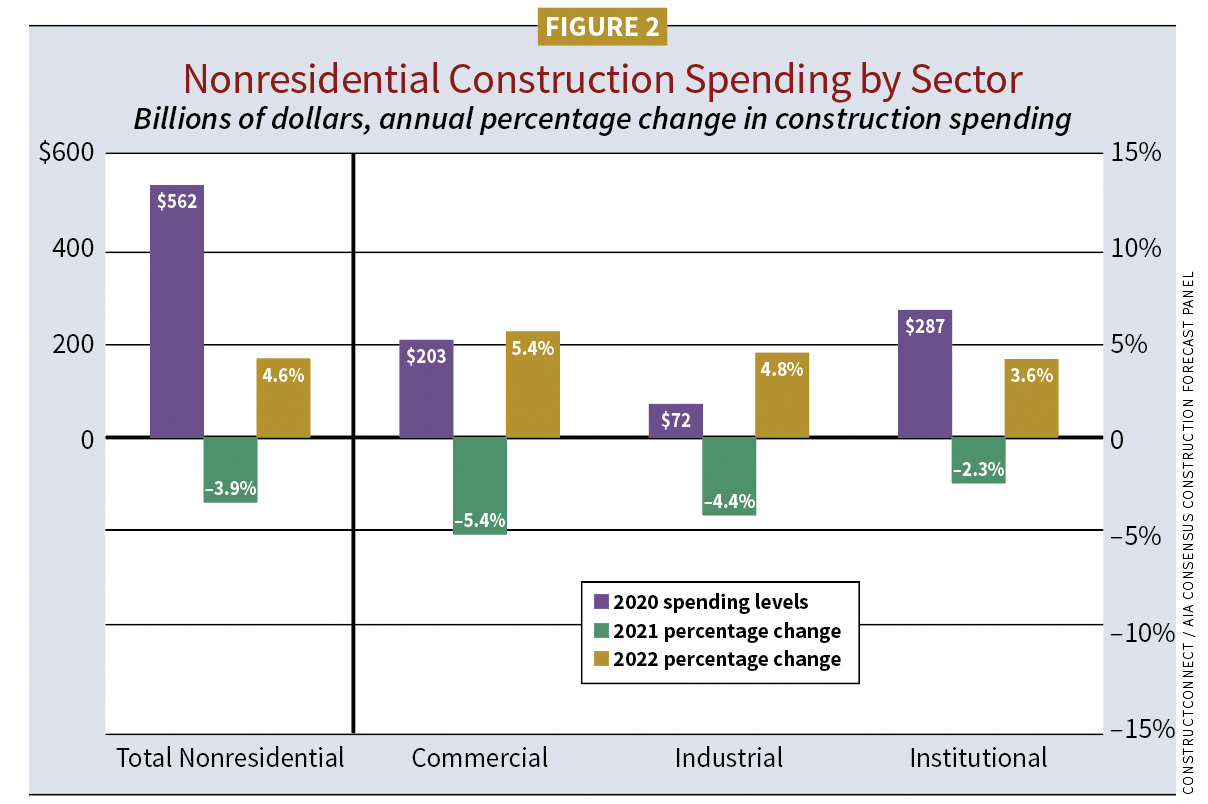

Put-in-place (PIP) spending (dollar spends during a construction project) is another lens through which to assess the state of construction. Based on AIA Consensus figures (an aggregate industry forecast), nonresidential PIP in 2021 was projected at –3.9%, reversing in 2022 with an estimated 4.6% (see Figure 2). Residential PIP in 2021 showed a hearty 20% gain ($767B) and is expected to advance 4% in 2022.

The economic underpinnings

Cristian “Cris” deRitis, deputy chief economist at Moody’s Analytics, was a featured presenter at the Dodge 2022 economic forecast

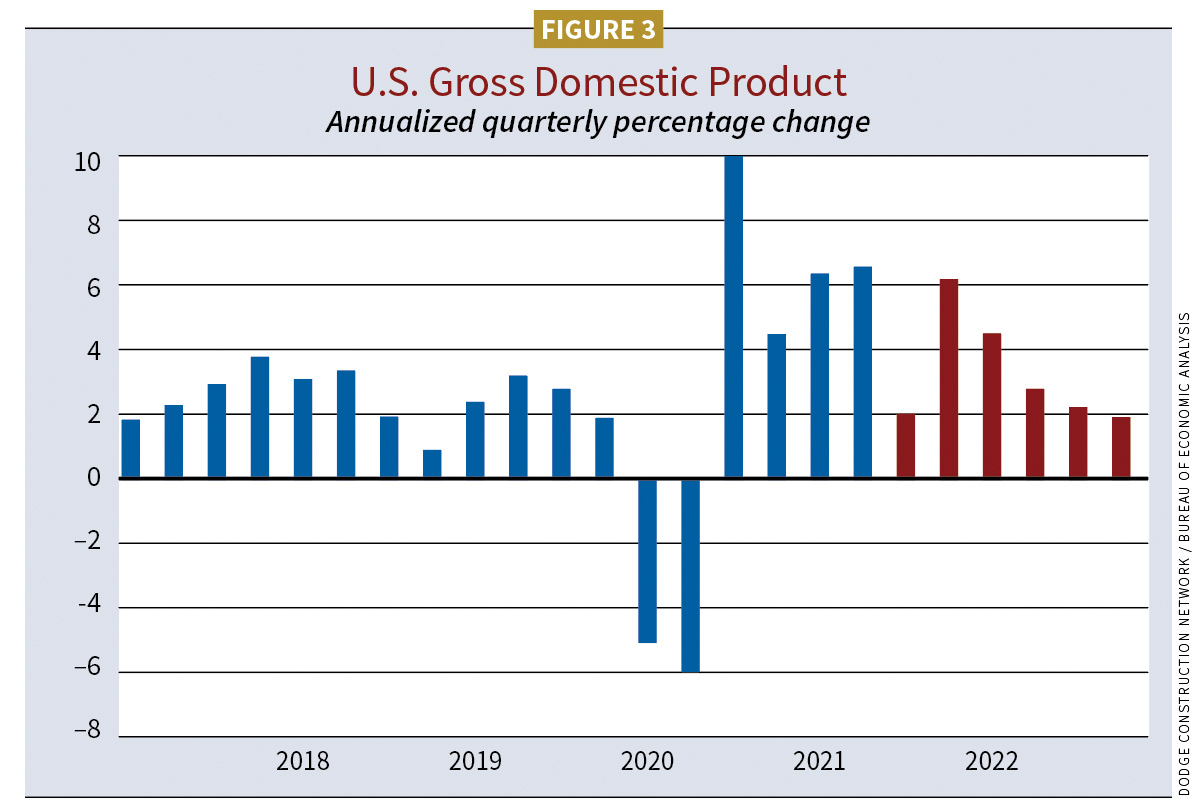

“Expecting just south of 6% (GDP), we knocked our 2021 estimate down to 5.8% year-over-year growth due to delta,” deRitis said (see Figure 3). This year, Moody’s anticipates a GDP around 4.25%.

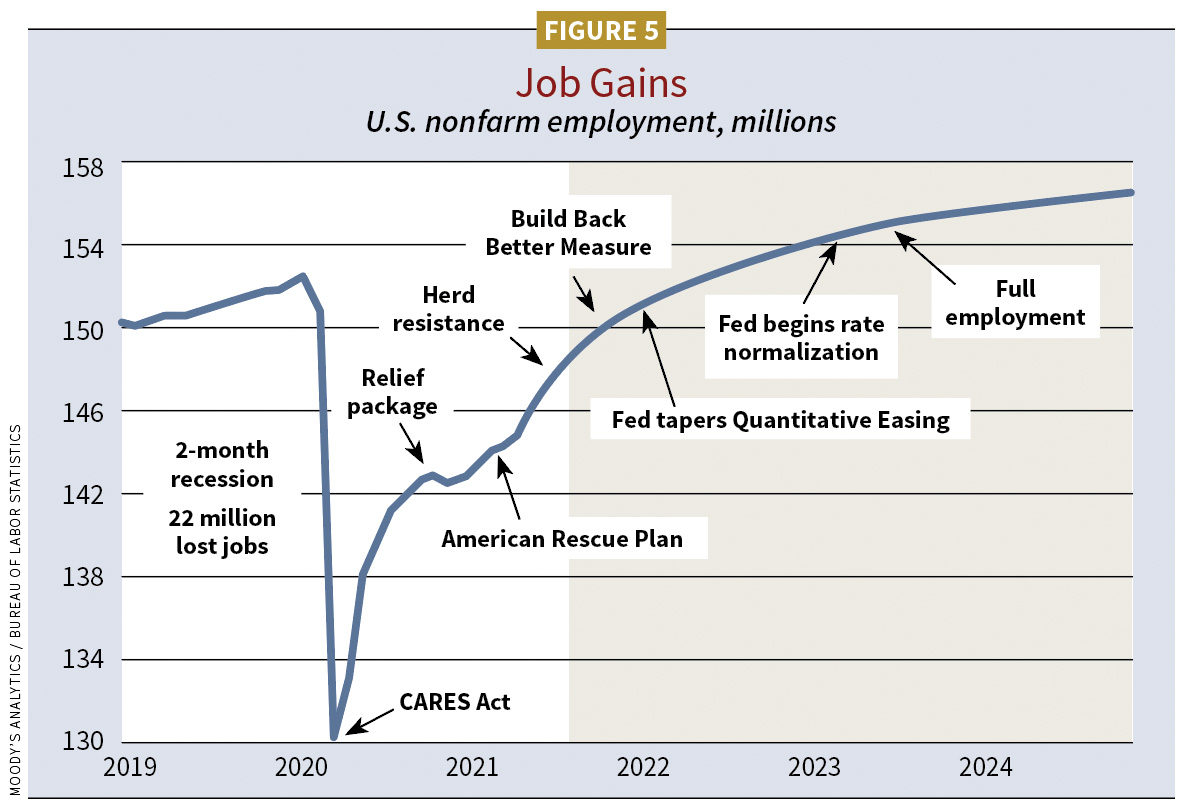

“Still very, very strong,” deRitis said. “About double what we normally have. Production we couldn’t get done [in 2021] will be shifted into [2022] because of delta. Supply chain issues should be resolved later in 2022. We anticipate job growth between 400,000 to 500,000 per month on average, so quite favorable. Our recovery outlook hasn’t really changed. We see delta as a speed bump and see very little risk of recession at this point.”

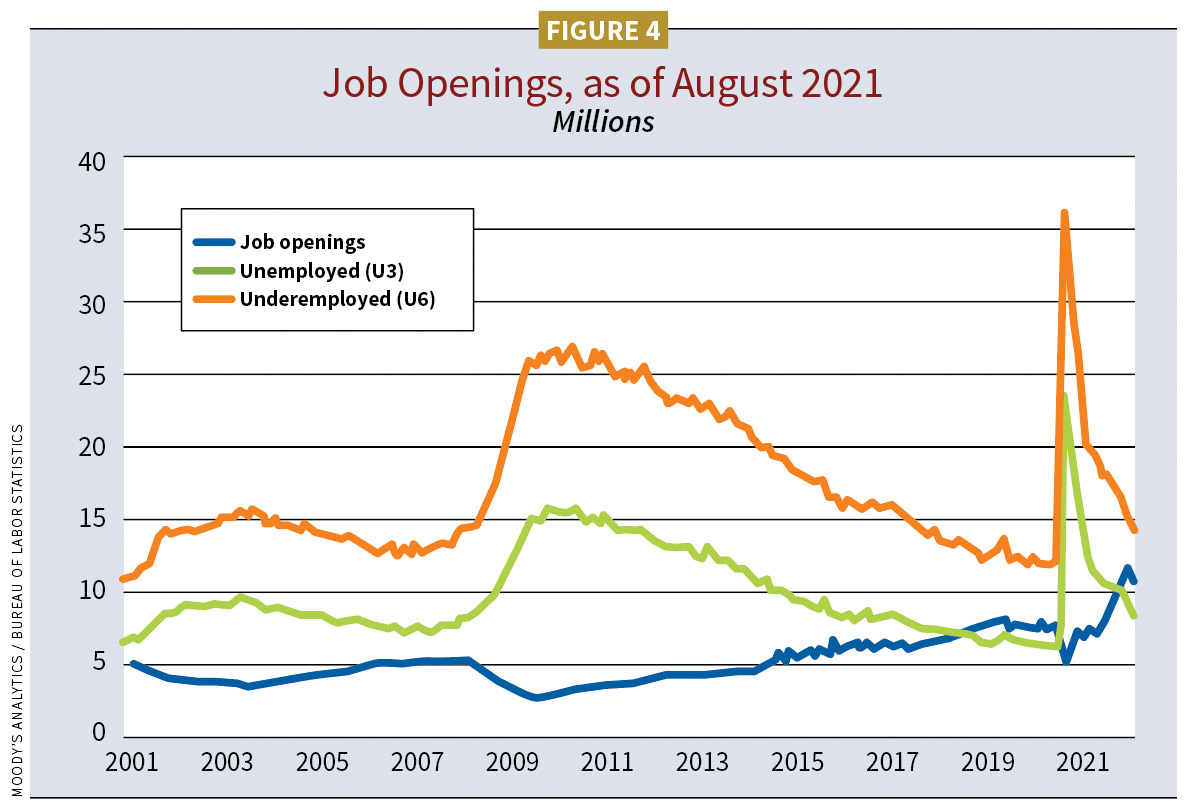

As shown in Figures 4 and 5, by the end of 2022, deRitis expects full employment—“Anyone that wants a job can get a job”—and continued payroll growth (higher wages 4%–5% on average). As of November 2021, the U.S. Bureau of Labor Statistics (BLS) reported unemployment at 4.2%. The Bureau of Economic Analysis reported in October 2021 that personal income increased $93.4 billion, or 0.5% at a monthly rate, largely due to wage increases, and payrolls are up, too. (See Figure 6.) Consumer spending increased $214.3 billion, or 1.3%. Women’s participation in the labor force is lagging, in large part due to the deficit of child care workers.

Other encouraging signs

“More people are coming back to their workplaces,” deRitis said. “Numbers are down maybe 20% compared to prepandemic levels. We may see 10% return as companies adopt a hybrid [home/office] work model.”

The TSA reported 2021 Thanksgiving holiday travel peaked at 2.3 million travelers, more than twice the number in 2020, which is good for infrastructure construction.

“The Federal Reserve will be concerned with overheating the economy and start to move short-term interest rates higher, a rates normalization,” deRitis said. “After that, [expect] a slowdown in the economy because of the higher rates. But we should be off and running at a more sustainable pace of growth. Some months will be stronger, some weaker. The wild card is the pandemic itself.”

The price of prices

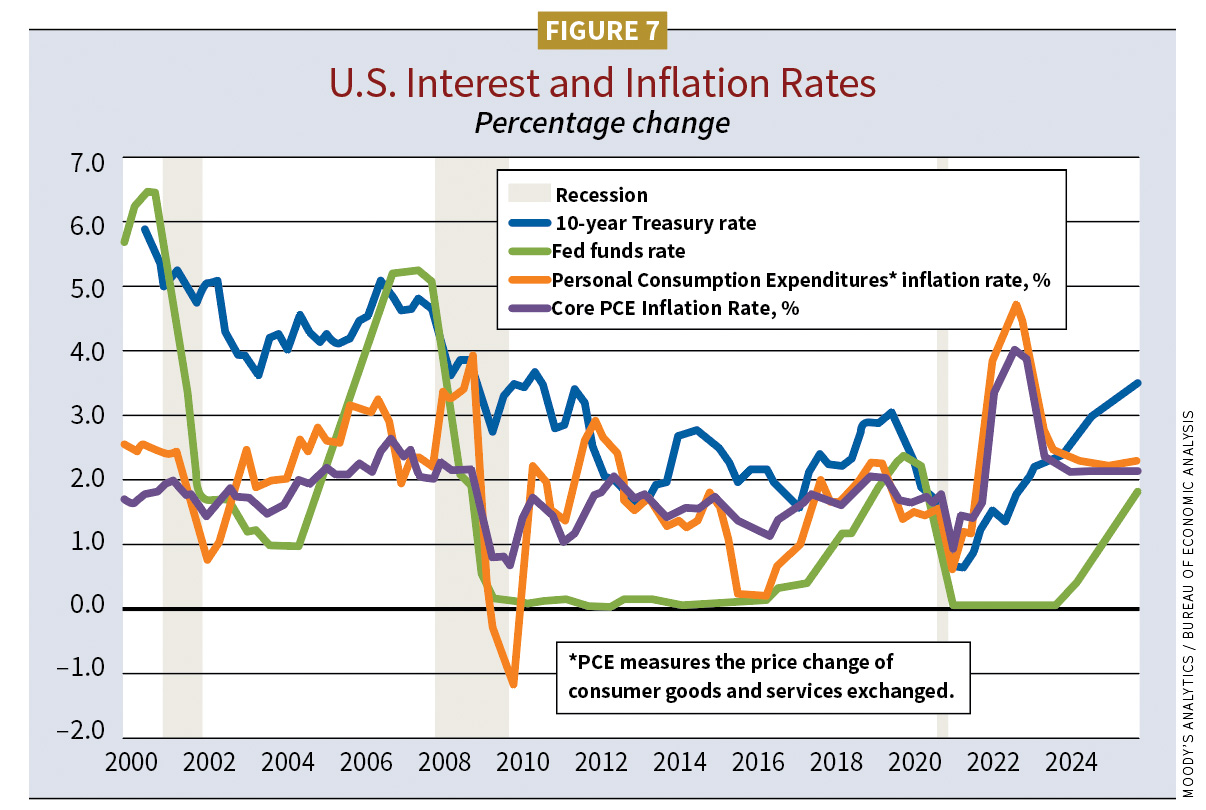

In November 2021, the Federal Reserve Economic Data reported the Consumer Price Index for services rose 3.6% year-over-year. That month also brought the year-to-date rise in durable goods costs to 6.8%, a profoundly larger share of consumer spending than prior to COVID-19.

“The rise in prices is something we haven’t seen in 30 years (since November 1990),” deRitis said. “With the reopening of the economy, everyone is trying to go through the door at the same time. Limited supply and lots of demand are sending prices upward. We anticipate another quarter or two of price acceleration, then some moderation by mid-2022. In December 2021, Fed officials surmised rates could be as high as 2.125%. There is a chance of uncontrollable inflation in the short term and consumer expectation of persistent inflation. Those could be a real risk to our outlook.” (See Figure 7.)

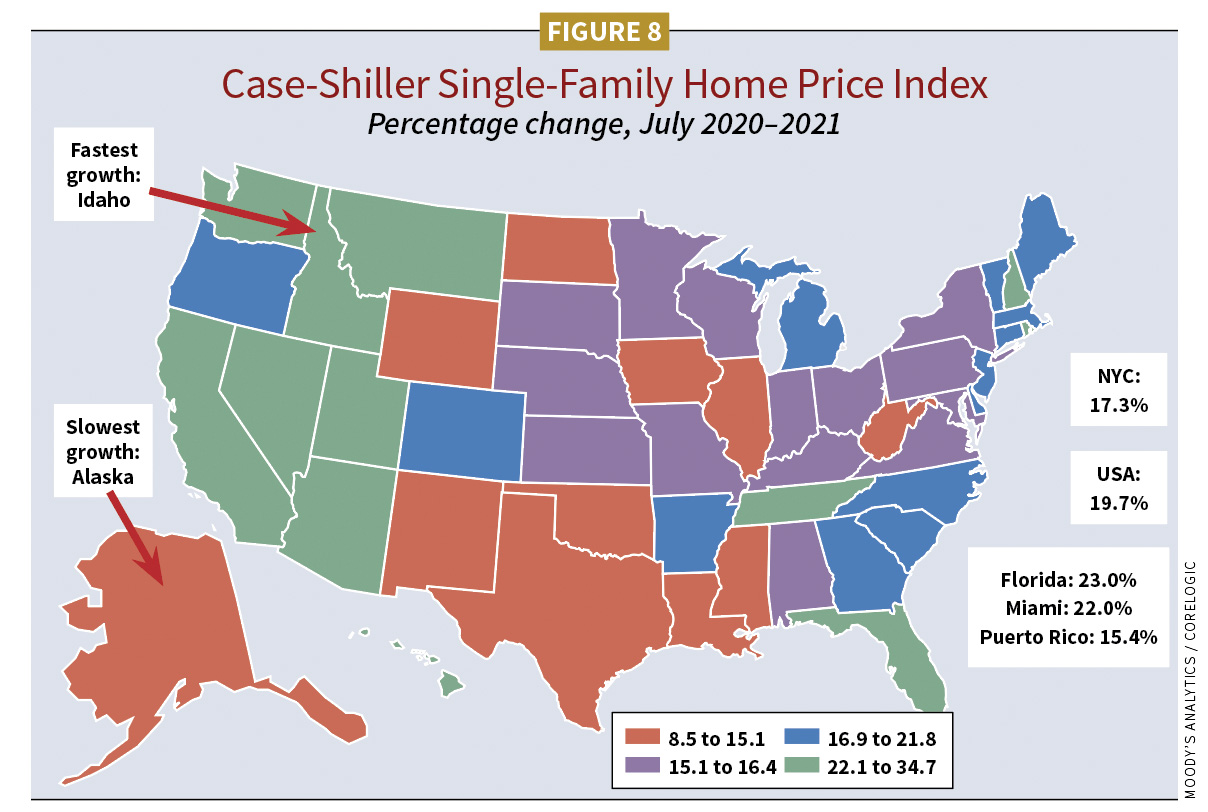

Another risk to the economy is the rise in asset prices, such as homes—a consequence of low interest rates, pent-up demand and the short-order reopening of the economy, deRitis said.

“Home prices grew very fast at 20% nationally, something not even seen in 2008–2009 during the housing boom and bust period,” deRitis said (see Figure 8).

He expects prices will slow and the market buoyed by favorable demographic trends.

“We are seeing peak numbers of 30-year-olds [as home buyers], more than we’ve seen in recent history,” deRitis said. “That provides a tailwind to home builders. I expect residential housing to remain very robust for the next five years. After that, [it’s] a different picture as the next generation is much smaller.”

Finally, deRitis sees a structural change in the construction industry, as workers over 55 are taking early retirement at increasing rates. “Whatever the reason, this segment has chosen early retirement,” he said. “It is a big loss when they exit the labor force early. Some are coming back, some maybe part time.”

The state of construction economy

Economists at Dodge Construction Network and ConstructConnect see construction turning around, but slowly.

“Economic growth has resumed following the [2021] third quarter’s delta-led slowdown. However, the construction sector’s grip on growth remains tenuous,” Branch said. “Pull residential out of 2021’s performance, and total construction is 3%–4% shy of 2019’s $853 billion on a nominal dollar basis. While healing from the pandemic continues, there is still a long road back to full recovery. The good news is all of construction is now moving in the right direction, fed by an increase of nonresidential building projects in planning and the recent passage of the infrastructure bill. Both will provide meaningful support and growth to construction in the year to come.”

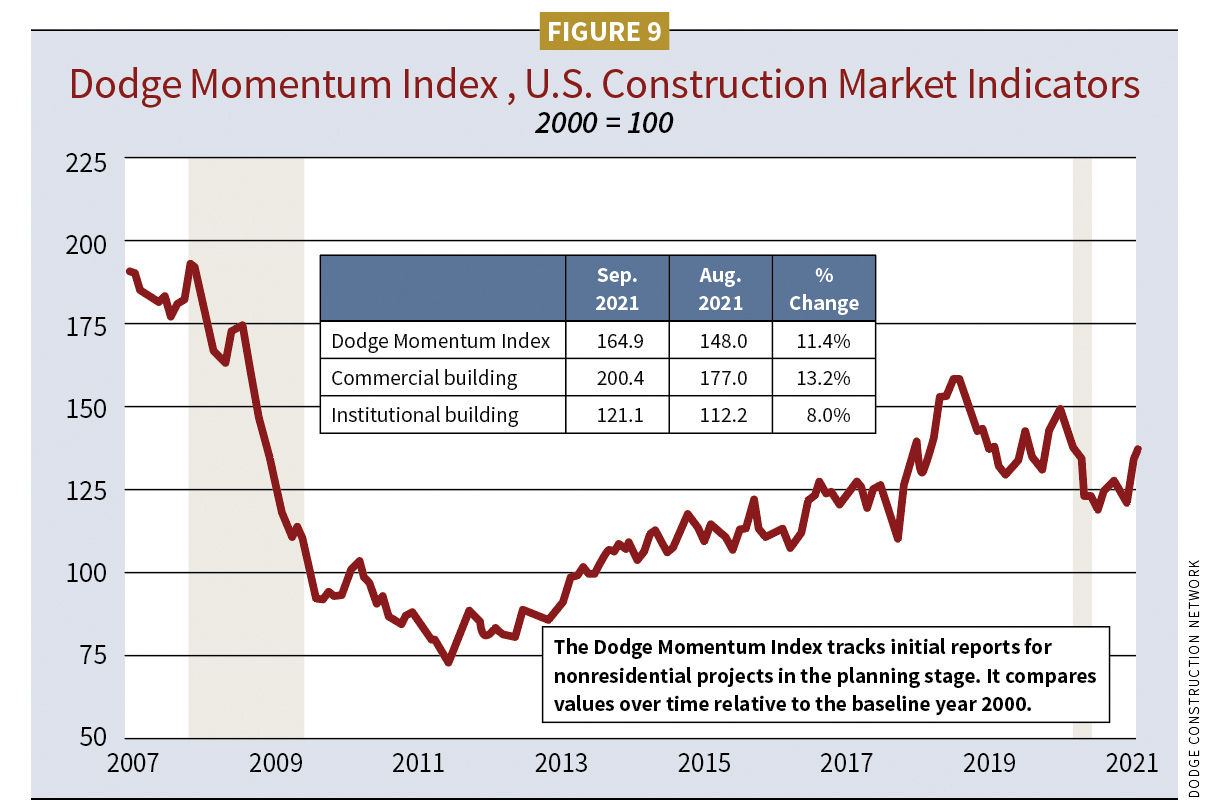

Branch finds the strength of data found within his firm’s Dodge Momentum Index (DMI) encouraging. The monthly DMI looks at what is ahead in nonresidential construction. It tracks projects in the initial stages of conceptual planning (see Figure 9).

“The DMI tilted up significantly since early in the year (2021) and has become much more well-balanced toward most types of private and public building projects,” Branch said. The dollar value of these projects is sitting at about a 14-year high.

The DMI increased 10% in October to 181.2 (2000=100), from a September reading of 164.6. In October 2021, commercial planning rose 14% and institutional gained 3%. In a see-saw year, the November 2021 DMI fell 4% to 171.7, but momentum remains strong. In a year-over-year comparison, the DMI was 44% higher. Commercial planning was 45% greater, and institutional 41% better.

Branch expected many of the 2021 projects tracked in the DMI to break ground in 2022, but added the time has lengthened during the pandemic.

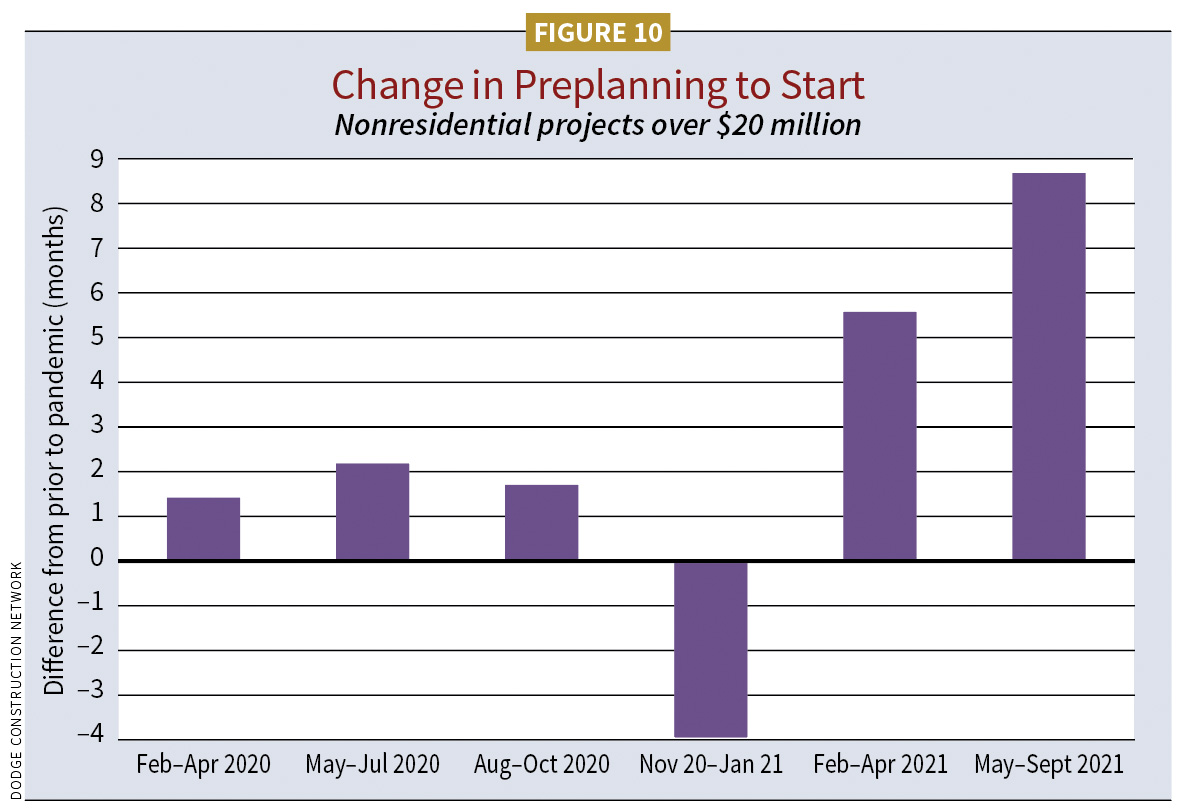

“It usually takes three months from bidding to groundbreaking, but that has extended since February 2020 to as long as nine months. The round of general bidding (as of November 2021) is ahead of 2020 and just a little behind 2019. We are generally very positive in looking at activity for 2022, but also cognizant of challenges.” (See Figure 10.)

Another revealing measure of construction is the AIA Architecture Billing Index (ABI). The ABI leads nonresidential construction movement by 9–12 months. Any score over 50 shows activity increasing. In 2021, the ABI stood at 56.6 (September), the highest score of the year was 54.3 in October and it was 51.0 in November. ABI scores through September rated the highest AIA had seen in immediate post-recessionary periods. Regional scores in November 2021 included Midwest (57.6), South (53.7), West (50.9) and Northeast (45.5). By sector, the ABI for commercial/industrial was 50.5, institutional 50.1, and though not technically nonresidential, AIA shared multifamily at 51.4.

Jennifer Riskus, director of market and economic research for AIA, said the level of inquiries and new design contracts were healthy. Another measure is backlogs.

“They were strong prior to the pandemic, helping architecture firms when new work wasn’t coming in. [As of November 2021,] backlogs are at their highest levels since we started gathering this data on a quarterly basis 11 years ago,” she said.

The power of remodeling

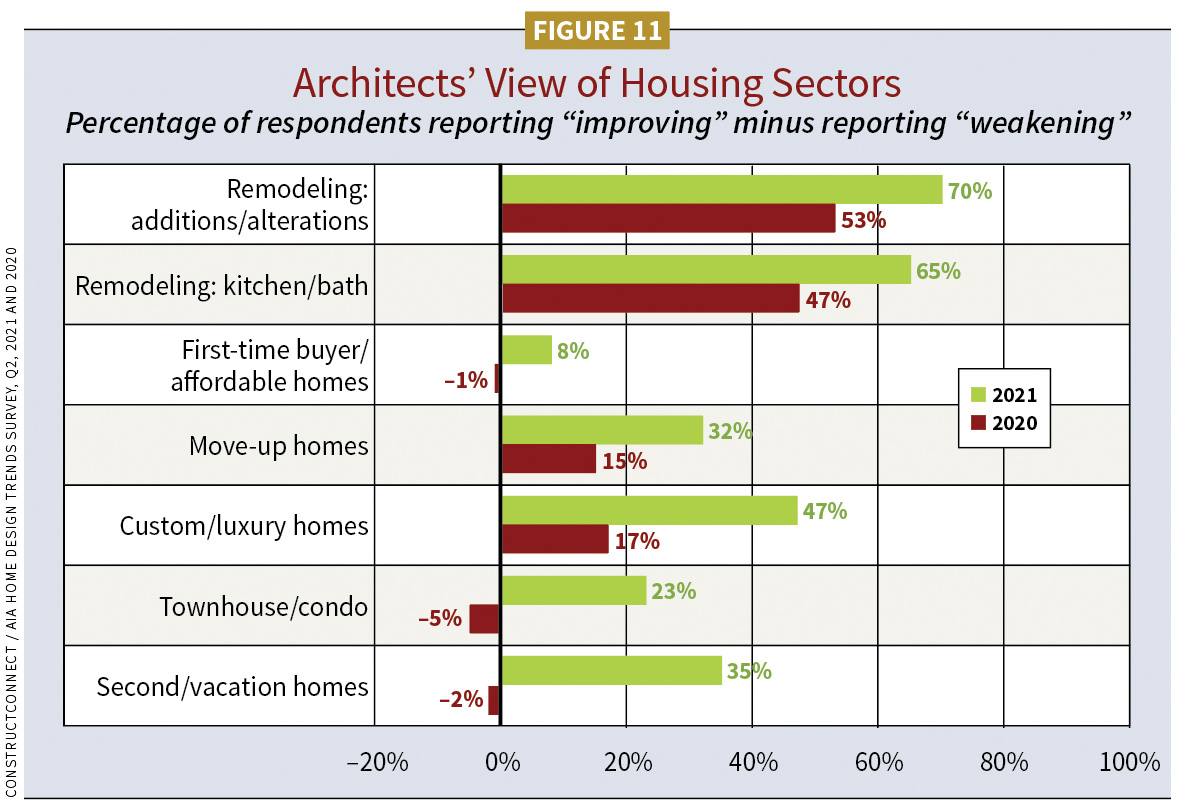

Along with residential new construction, remodeling in this market is strong. In October 2021, the National Association of Home Builders (NAHB), Washington, D.C., Royal Building Products Remodeling Market Index reached a vigorous score of 87. Any score above 50 indicates positive remodeling activity. Work was equally distributed by large remodeling projects above $50,000, $50,000–$20,000, and under $20,000. Remodeling is mostly up across the board (see Figure 11).

Statista, a data-gathering service with a U.S. office in New York, reported on renovation trends for nonresidential. These included office space remodels to accommodate tenant needs and related renovation of older buildings; redesign of restaurant interiors and technological customizations to attract customers; and renovations in e-commerce spaces. In 2019, 49.3% of AIA architects shared they were engaged in remodeling work. When asked in 2021, more than half indicated the same level of work, a quarter saw a small decrease and 8% saw a significant increase. AIA also found retrofit work to be solid in manufacturing, distribution facilities, multifamily and institutional markets.

The effects of inflation

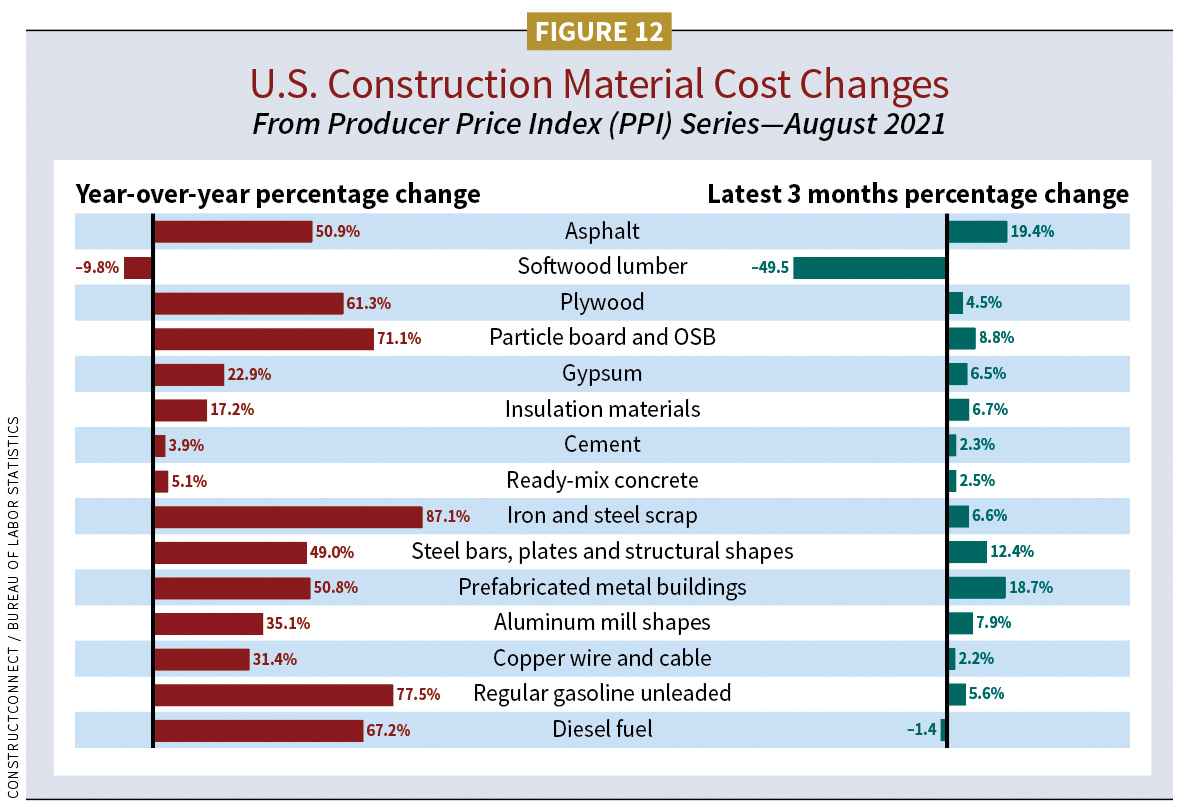

“In uncharted waters” was how Branch described building materials inflation (see Figure 12).

“I think construction inflation will probably last into mid-2022 before we see prices pull back,” he said. “In good news, plywood and soft lumber prices are easing back. In addition, the U.S. and European Union have agreed to lift some steel and aluminum tariffs in December 2021 (under a certain quota, less duties).”

Ken Simonson, AGC’s chief economist, added that, while bid prices rose between April to August 2021, the rise was hardly closing a historic gap in materials costs.

“The price of steel mill products (during this period) more than doubled,” he said. “Copper and brass mill shapes were up by two-thirds. Aluminum mill shapes and plastic construction products up by a third. Lumber and plywood have come down but are volatile. To deal with soaring material costs, we see contractors getting owners to accept price increase clauses, front money to buy materials sooner, pursue a variety of materials and/or find suppliers that can better meet a project schedule. Things to try, but no guaranteed solution right now.”

He indicated the cost squeeze on contractors could last two years or more.

Alex Carrick, chief economist for ConstructConnect, added this perspective: “While inflation will remain important, there is quite a difference between inflation and moving toward a more expensive economy,” he said. “I would postulate after the pandemic that it will be a more expensive world. Companies are having to set up cybersecurity, reduce carbon emissions and meet compliance. Taxes will go up and certainly interest rates.”

Carrick recently reported on the state of U.S. exports, with Texas in the lead.

“Its dollar volume of foreign sales to date in 2021 ($269B) has been double what second-place California has been able to achieve ($130B) and four times as great as third-place New York has managed ($63B).

“Texas and fourth-place Louisiana export a great deal of oil and gas in their various derivative forms,” Carrick said. “Louisiana’s trade story is not all about energy. In fact, the state’s major export product in 2021 has been soybeans. And the state’s chief customer is China.”

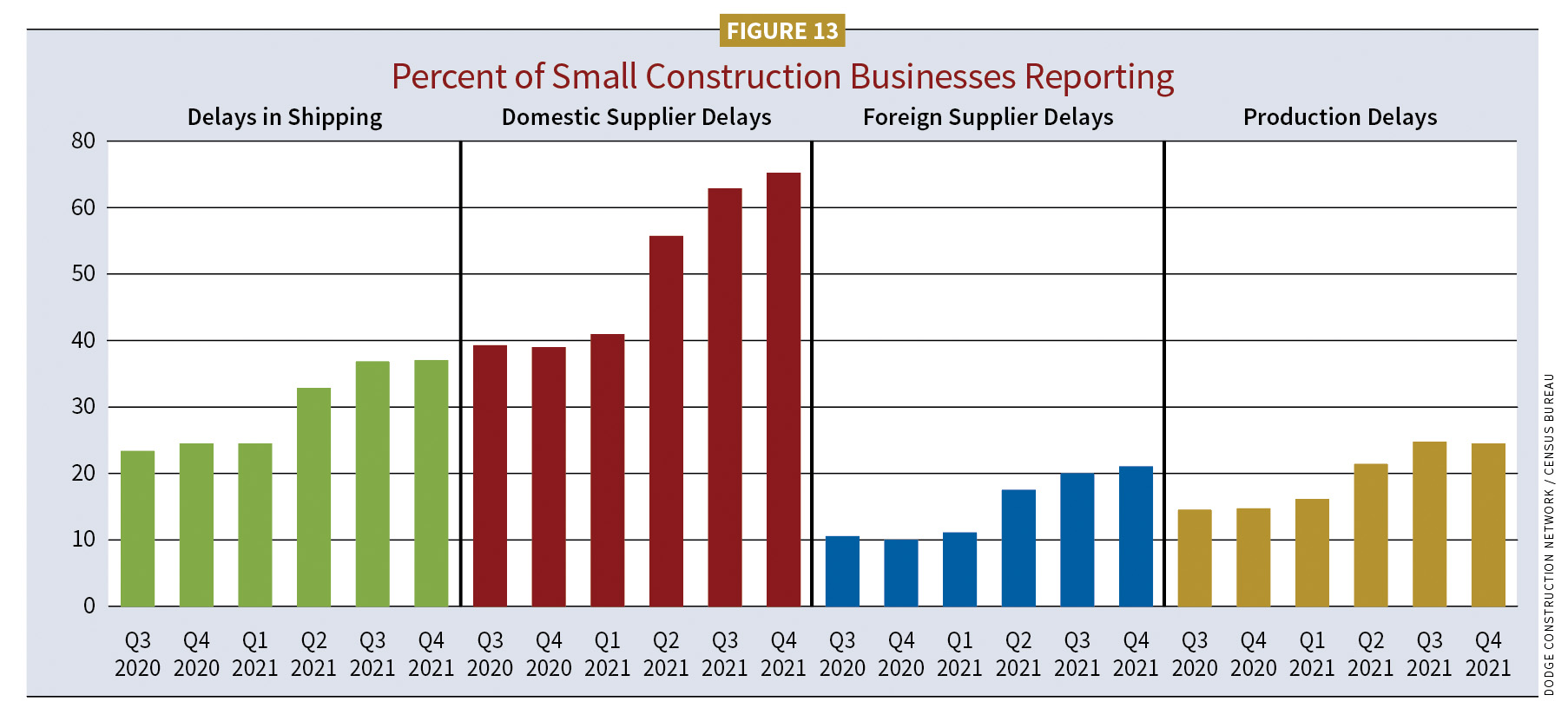

Adding to the problems with cost increases, many businesses are also reporting significant delays with shipping, suppliers and production (see Figure 13).

Construction employment

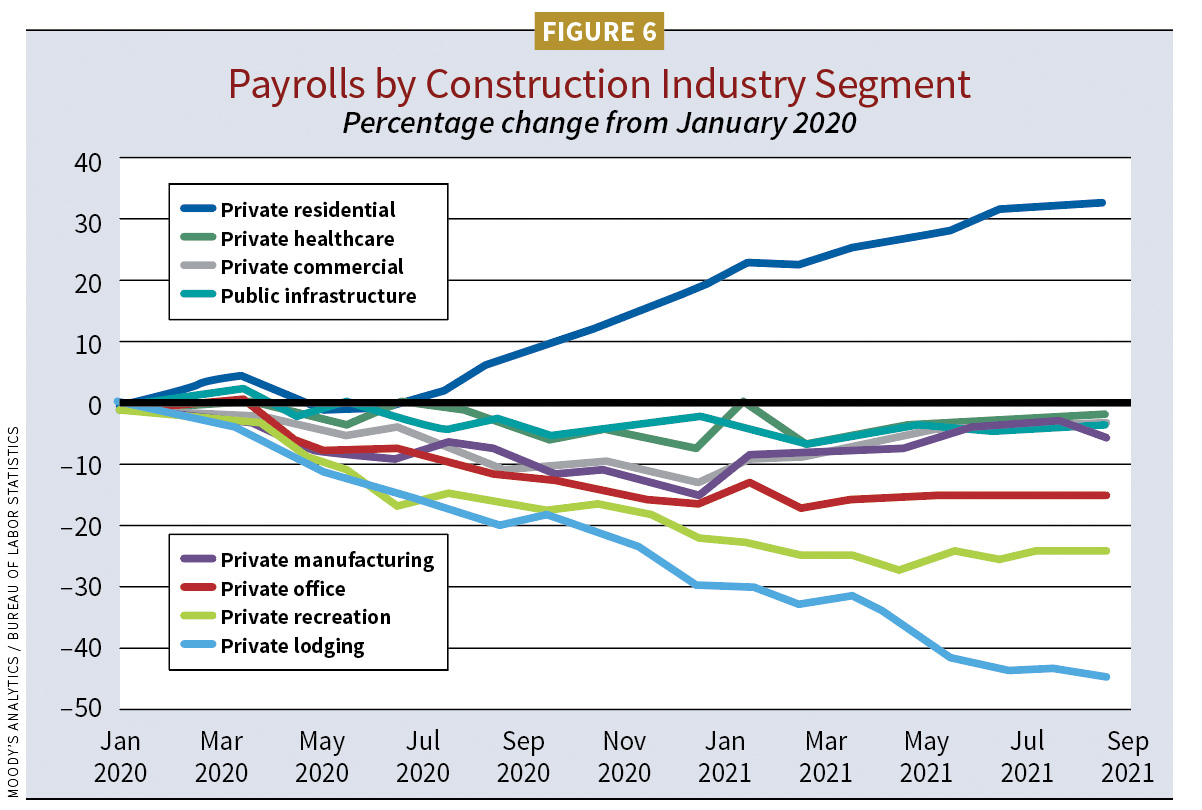

The pace of recovery for construction is in part made clear through employment. The BLS reported October’s construction employment added 44,000 workers, building on a September increase of 30,000. November saw 31,000 jobs added. These three months accounted for 109,000 jobs of the 130,000 added year-to-date. Another 100,000 new jobs would be needed before total construction employment returned to February 2020 pre-pandemic levels. Construction unemployment fell from 6.1% in July 2021 to 4.0% in October, but rose to 4.7% in November. Those 31,000 newly employed in November included specialty trade contractors (plus 13,000), construction of buildings (plus 10,000) and heavy and civil engineering construction (plus 8,000).

“It is harder to find qualified workers as work is coming in,” AIA’s Riskus said.

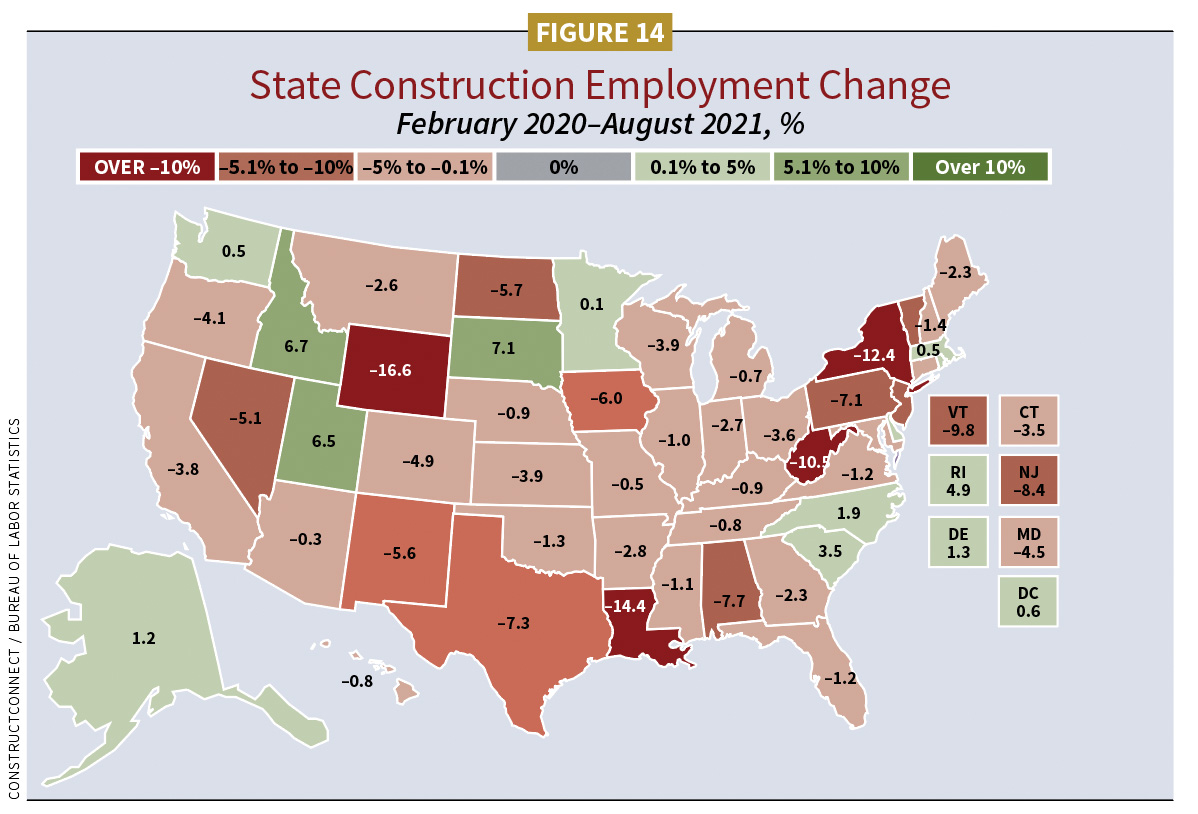

Simonson shared the top five gains in construction employment (September 2021) were South Dakota (7.1%), Idaho (6.7%), Utah (6.5%), Rhode Island (4.9%) and South Carolina (3.5%). The bottom five showed declines: Wyoming (–16.6%), Louisiana (–14.4%), New York (–12.4%), West Virginia (–10.5%) and Vermont (–9.8%) (see Figure 14).

“There are two big concerns regarding construction workers,” Simonson said. “They have a much lower vaccination rate by their own admission than most other occupations.”

Using research through surveying by the Delphi Group of Carnegie Mellon University, the Silver Spring, Md.-based Center for Construction Research and Training reported only 57% of people who identified their occupation as construction said they were vaccinated. Another 42% of construction workers were vaccine-hesitant, more than double of other occupations.

“The implication is construction firms may have trouble finding workers who are both healthy and eligible to get onto job sites as more and more owners insist on vaccination,” Simonson said.

The second concern Simonson shared was construction not keeping up with other industries in wage increases.

“Data suggests wages have barely moved up,” he said. “Historically, construction paid a premium of 9%–10% over other industries in hourly earnings. That has dropped to less than 8%. I fear that means entry-level workers may find other work attractive and pass up on construction. However, this also suggests the industry may raise wages and pass these costs on.”

2022 Sector Forecasts

Starts information is supplied by Dodge (cited first), followed by ConstructConnect, unless otherwise noted. Due to some varying market categorization between the two companies, performance numbers can differ. We try to reconcile those differences or cite them when they occur. Also, square footage estimates were largely not shared this year.

RESIDENTIAL

- Dodge 2021: 17% ($412.1B); 2022: 4% ($430.2B)

- ConstructConnect 2021: 16.7% ($351B); 2022: 10.5% ($388B)

This statement from Dodge’s Branch said it all regarding the strength of residential: “Understand, if you remove residential activity that has been absolutely on fire, the construction market today would look very, very different [in collective starts numbers].”

Through November 2021, residential starts were up 20% over the same period one year ago.

Single-family

- Dodge 2021: 16% ($301.4B); 2022: 4% ($313.8B)

- ConstructConnect 2021: 21.35% ($266.8B); 2022: 9.18% ($291.3B)

Though starts numbers eroded 10%–13% in the third quarter of last year, Dodge estimated an overall 16% pace of growth for single-family in 2021, on par with 2020. In 2022, a 4% gain is anticipated. ConstructConnect estimates for 2021 were 21.7% ($267B) and 9.18% ($388B) for 2022. Last year marked the first year since 2006 the single-family market exceeded 1 million units. The NAHB reported 1.111 million units in 2021 and anticipates a slight increase to 1.113 million in 2022.

“Mortgage purchase applications are mixed, not slipping but not gaining,” Branch said. “Issues of materials, labor costs are really affecting this market. Single-family is exposed to these higher building costs. The result are starts advancing at a more tepid but sustainable pace of 3% in 2022.”

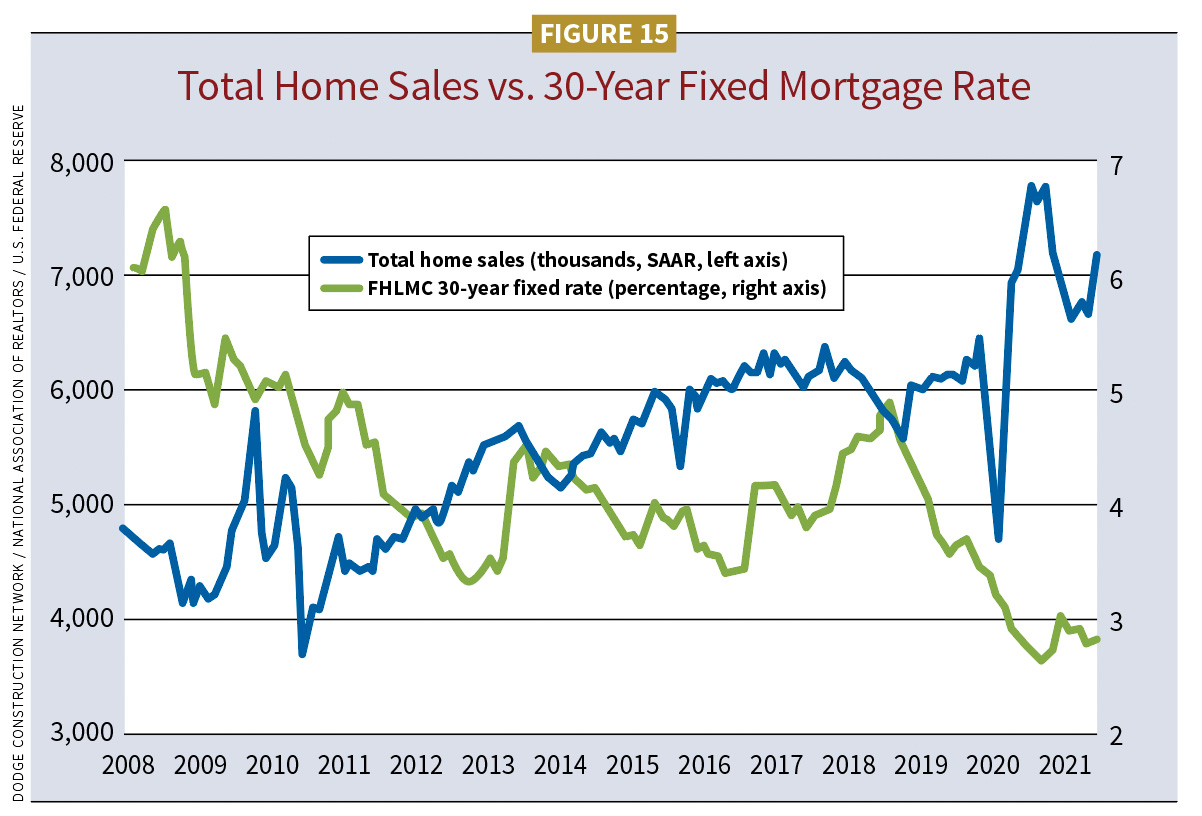

The National Association of Realtors (NAR), Chicago, predicts 30-year fixed-rate mortgages will rise slightly in 2022, averaging 3.6% for the year, according to Nadia Evangelou, senior economist and director of forecasting for NAR. That rate reflects an average among predictions from Fannie Mae, Freddie Mac and others. Fannie Mae is the most optimistic and predicts an average of 3.1% in 2022. NAHB estimated 2.96% for 2021 and an average of 3.57% in 2022. (See Figure 15.)

Home costs have also risen, dampening momentum. The S&P CoreLogic Case-Shiller’s U.S. National Home Price Index for single-family homes shows a price increase of 20% compared to a year ago.

The NAHB/Wells Fargo Housing Market Index (HMI) asks NAHB members to rate market conditions for current new homes sales and six-month estimates, including prospective buyers. In 2021, the HMI was extremely strong, hovering close to the top ranking of 90 for most of 2021.

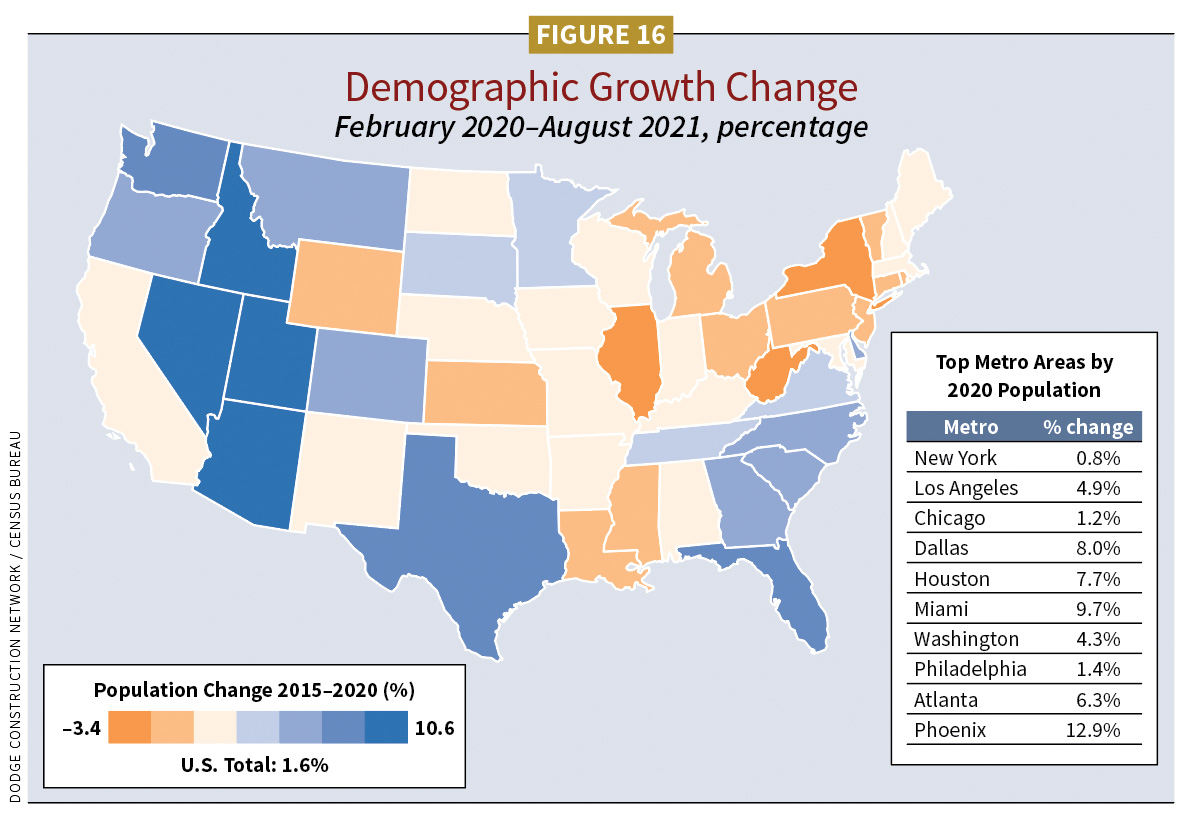

Growth in single-family construction is also broad-based, with Texas and Florida seeing the greatest starts through September 2021 (23% and 35% respectively). People are relocating, mostly to western and southern states. (See Figure 16). All the states were ahead in starts on a year-to-date basis.

“Residential permits tell a story,” Carrick said. “The top three housing starts, or permits, are in Texas cities—Dallas-Fort Worth, Houston and Austin. Texas is in a league of its own.”

He cited one specific draw: space tourism (Elon Musk’s SpaceX and Jeff Bezos’ Blue Origin). But other businesses such as battery storage plants in Austin and Houston, and the Tesla Gigafactory electric truck battery plant in Austin, could portend similar advances in other states.

Multifamily

- Dodge 2021: 19% ($110.7B); 2022: 5% ($116.4B)

- ConstructConnect 2021: 3.34% ($85.5B); 2022: 14.6% ($97B)

“Multifamily has taken off in a very aggressive fashion due to affordability challenges in single-family,” Branch said. “We haven’t seen this level of units breaking ground since the mid-80s.”

For 2021, Dodge expected a 19% gain ($110.7B) in multifamily starts, the best number since 1986. This comes after a 1% loss in 2020. This year, Dodge expects a 5% ($116.4B) gain. There has been some forward building due to fear of labor and supply shortages. In its count, ConstructConnect saw 2021 activity rise 3.34% ($84.5B). It estimates 14.6% ($97B) in 2022.

“We’re seeing less high-rise megatowers,” Branch said. “Instead, it’s $20–$25 million sized projects and buildings 4–6 stories. We are also seeing the most growth in buildings averaging 4–10 units. New York City still represented big projects, but we are seeing growth in nonmetropolitan areas, too. In fact, growth rates get stronger further and further away from big metro areas. The top three for multifamily activity are New York state followed by Florida and Georgia.”

Branch added that multifamily markets across the country are exceptionally tight, a huge incentive to build. Nonetheless, based on its planning database, Dodge expects activity to ease back to a more normal rate of growth in 2022, thus the smaller 5% gain.

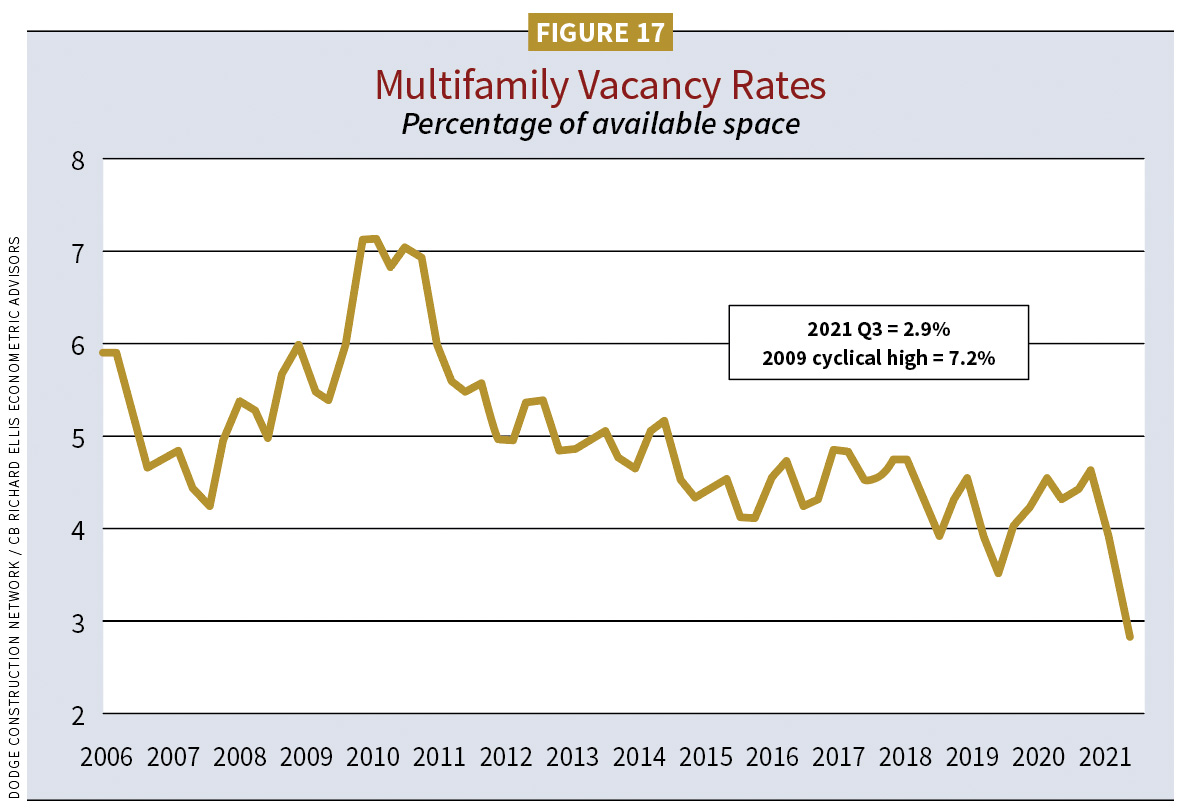

Fannie Mae anticipated 2021 multifamily rental vacancy rates to settle between 5.25% and 5.75% (see Figure 17).

The top three multifamily projects in 2021 (as of September) were 202-204 Arsenal St. (mixed use), Brooklyn, N.Y. ($492 million/910,000 sq. ft./1.046 units); Flamingo Crossing Apartments, Winter Garden, Fla. ($485 million/3 million sq. ft./2,091 units); and 1018 West Peachtree Apartments, Atlanta ($350 million/842,000 sq. ft./609 units).

COMMERCIAL

- Dodge 2021: 15% ($128B); 2022: 12% ($143B)

- ConstructConnect 2021: –21.0% ($23.6B); 2022: 19.3% ($28.2B)

In 2021, the commercial sector gained about half of what it lost in 2020. Warehouse starts helped. Construction activity should be broader-based in 2022.

In 2021, “Dollar values included new construction, additions, but also significant renovation,” Branch said.

Within the top 10 projects of this sector in 2021, data centers represented four of the top-10 projects through September 2021. Warehouses represented another four.

Retail

- Dodge 2021: 10% ($13.6B); 2022: 14% ($15.5B)

- ConstructConnect 2021: –8.6% ($25.8B); 2022: 22.3% ($31.6B)

Dodge estimated retail starts in 2021 stood at 10% ($13.6B), a stark departure from 2020’s dismal –26%. Encouragingly, 2021 will see additional growth of 14% ($15.5B). ConstructConnect gauged starts in 2021 at –8.6% ($25.8B), but gaining lost ground at 22.3% ($31.6B) in 2022.

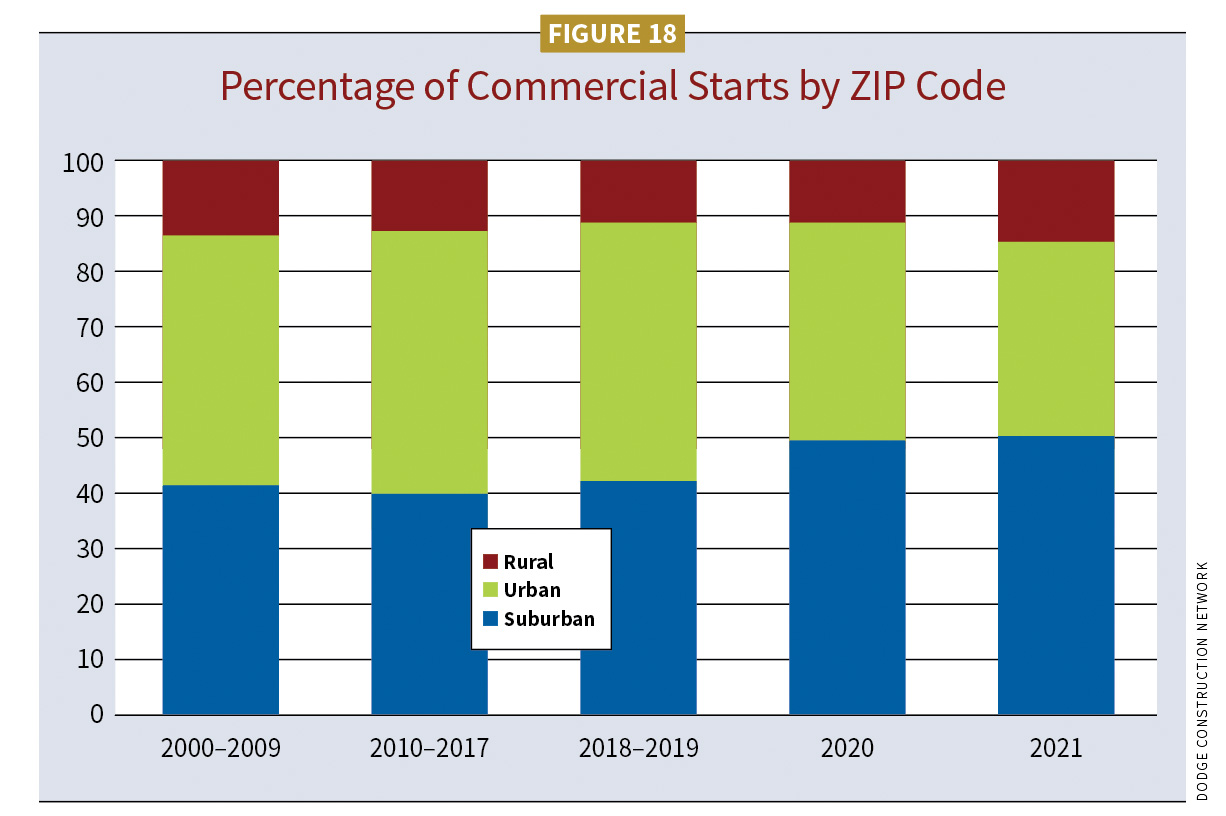

“Retail is benefiting from a shifting residential sector to the suburbs pulling some semblance of retail construction with it,” Branch said. (See Figure 18.) “We aren’t expecting a return to levels of 2015–16 (averaging $21B) and surely not those during the Great Recession (e.g., 2007/$29.4B). Mixed-use construction for multifamily (inclusion of retail and office) is a benefit.

“Interestingly, we’ve seen strength in DIY store construction, driven by the pandemic,” he said. “More people at home with maybe more time. Harbor Freight Tools was No. 3 in starts, AutoZone No. 9.”

Leading retail were Walmart ($1.19B), Publix Super Markets Inc. ($215 million) and Target ($192 million). Other top-10 included Aldi, H-E-B Grocery Co., Costco, Dollar General and Dollar Tree.

Warehouses

- Dodge 2021: 36% ($46.7B); 2022: 13% ($52.8B)

- ConstructConnect 2021: –8.09% ($24.1B); 2022: 9.64% ($26.4B)

“Warehouse starts continue to stagger the imagination,” Branch said. “I have run out of superlatives with activity going back to 2005. In 2021, we did decelerate a little bit in the third quarter, yet even that activity represented the third best quarter in our data set” (led respectively by 2021 Q1 and Q2).

In 2021, there was an impressive growth for this market at 36% ($46.7B). Dodge expects continued gains in 2022, but more subdued at 13% ($52.8B). ConstructConnect saw decline at –8% ($24B) in 2021, but estimates a rise to 9.64% ($26.4B) in 2022.

“Looking at our DMI showing the first nine months of 2021, there were $39 billion worth of warehouse construction projects entering early planning,” Branch said. “That is a full year in the pipeline for construction. We see growth for several more years. The lack of truck drivers both short-haul and long-haul might incentivize big developers to keep building larger distribution centers but closer to each other.”

Amazon dominated (better than half) as a warehouse builder over the last three years ($9.7B). Amazon-supported companies are major players, too. Walmart is investing ($1.2B).

Hotels

- Dodge 2021: –18% ($7.1B); 2022: 24% ($8.8B)

- ConstructConnect 2021: –33.7% ($6.8B); 2022: 41.0% ($9.6B)

Hotel starts activity was not great in 2021. The estimated value loss of –18% ($7.1B) was an improvement from –51% in 2020. Expect considerable hotel growth of 24% ($8.8B) in 2022, continuing into 2023. While hotel starts remained weak (down 30% year-over-year in the first nine months of 2021), the fourth quarter showed promise as large projects broke ground. They included the Loews Hotel in Arlington, Va., and renovation of the historic Cabana Hotel in Dallas.

Dodge expects business travel to make a return late in the second half of 2022, which feeds the hotel sector. Based on projects in planning, Dodge is seeing growth in midmarket hotels in addition to high-end.

Office buildings

- Dodge 2021: 4% ($45.3B); 2022: 10% ($49.7B)

- ConstructConnect 2021: –25.8% ($17.9B); 2022: 13.7% ($20.3B)

Office starts show a mixed future but are making progress. In 2021, Dodge expected office construction to gain 4% ($45.3B), a rebound from 2020’s –13.9% ($17.9B). ConstructConnect expected a negative contraction at –25.8% ($17.9B). This year both firms estimate growth, but the demand for space is uncertain in a COVID-19 world. How much of the workforce will remain hybrid?

“Kastle Systems Data, a key card company based in Falls Church, Va., reported in November 2021 that 37.8% of workers are back in the office full time,” Branch said. “We expected more with kids back on-site in school, but the delta variant threw us for a loop.”

He expects office occupancy to return more fully in the back half of 2022.

CBRE Group Inc., Dallas, reported office leasing increased by 3.3% quarter-over-quarter (October 2021) and 19.4% year-over-year to 49 million sq. ft.

Suburban office projects continue to gain strength as urban growth weakens. Dodge is seeing growth beginning to extend out to rural areas.

For the record, in 2021, data centers represented a 17% ($7.6B) share of all office construction, growing from 14% in 2020. Branch expects data center starts to gain 2% ($7.7B) in 2022.

The top three 2021 commercial projects as of September were New York’s JP Morgan Chase Office Tower ($1.5B/2.4 million sq. ft.) and Terminal Warehouse (addition/alteration) ($1.2B/180,000 sq. ft.); and Facebook Data Center Campus (phase 1), Mesa, Ariz. ($800 million/960,000 sq. ft.).

INSTITUTIONAL

- Dodge 2021: 5% ($136B); 2022: 6% ($145B)

Note: ConstructConnect projections for this sector are harder to neatly quantify alongside Dodge. Its estimates are addressed below, largely within related Dodge subsectors.

The institutional sector showed healthy progress in 2021. Some markets that were weak in 2020 gained strength in 2021, including recreation and transportation. This year, education and healthcare construction will advance, as will others.

The top three institutional (commercial-related) projects (as of September 2021) were Ohio State-Wexler Hospital, Columbus, Ohio ($1.2B/1.9 million sq. ft.); the Intuit Dome/NBA Los Angeles Clippers arena, Inglewood, Calif. ($1B/1.1 million sq. ft.); and Michigan Medicine Inpatient Tower, Ann Arbor, Mich. ($900 million/690,000 sq. ft.).

Education

- Dodge 2021: 0% ($62B); 2022: 9% ($67.5B)

- ConstructConnect 2021: –9.7% ($60.9B); 2022: 10.6% ($67.4B)

Note: Dodge did not offer specific starts figures by market.

Education represents half of all institutional. In 2021, the education market may not have grown in starts value, but neither did it suffer contraction. Budgets and demographics have held back this market. The real strength in 2021 came in lab space (research labs, private or college/university). This year, expect a good gain of 9% ($67.5B).

K-12

- ConstructConnect 2021: –8.43% ($43.82B); 2022: 8.06% ($47.3B)

In 2021, ConstructConnect found the K–12 market contracted 8.43% ($43.8B). Though students have returned to the classroom, a tentative cloud remains until vaccination numbers advance.

Through the American Rescue Plan, Congress allocated $200B for education construction and renovation. The School Superintendents Association, Alexandria, Va., surveyed superintendents about how they intended to spend this money.

“Only 16% said say would spend a half or quarter of those allocated dollars on construction,” Branch said. “Another 45% said they would spend less than 10% of those funds on renovation or construction. The big reasons were prices and people. Material prices are high, and they can’t find companies willing to take on the jobs in the time frame they want the projects done. I do think if we see prices start to moderate in the back half of 2022, dollars will start to flow back into new construction activity. We also have a veritable ton of money sitting on bond measures that hasn’t to date been spent.”

Branch cited $7 billion approved in November 2020 for K–12 construction in Los Angeles. Dallas approved $3.3 billion.

“Again, looking at the DMI in 2021 through September (2021), $8 billion entered planning. That is more than we saw in 2020 and just a little behind 2019. We expect these projects to break ground in 2022,” he said.

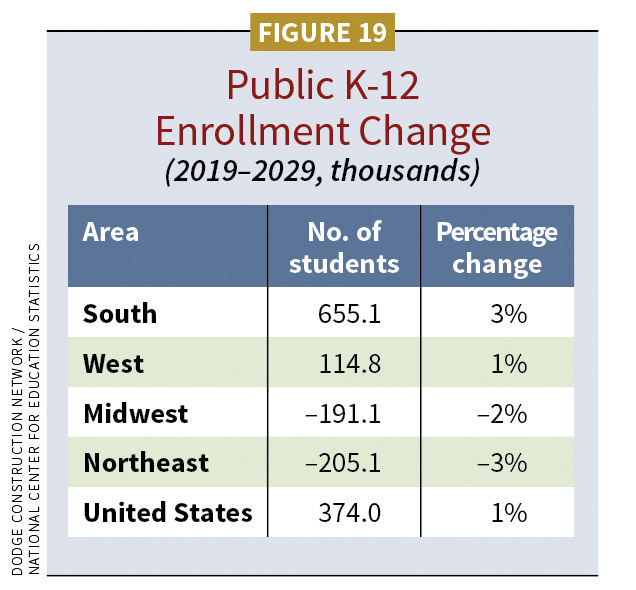

Regarding enrollment, the National Center for Education Statistics projects essentially flat growth until 2029. K–12 enrollment growth is strongest in the South and West (see Figure 19). College enrollments may edge up from 19 to 21 million by 2029.

While this doesn’t bode well for robust new construction, it doesn’t cancel it out either. For example, Branch cited the average age of a K-12 school building is 50 years old.

Lowell (Mass.) High School is a good example of renovating an existing school building while expanding it.

“Lowell is one of our top 10 institutional projects, and it belies a lack of demographic growth in that region,” Branch said.

If material prices ease and labor increases in 2022, Branch thinks construction dollars could flow to education.

Colleges and universities

- ConstructConnect 2021: –13.5% ($15.4B); 2022: 18.0% ($18.2B)

While ConstructConnect saw negative starts values in 2021 at –13.5%, the colleges and universities market is expected to gain 18% this year. Interesting variables are at play.

A 2021 survey by the National Association of College and University Business Officers, Washington, D.C., found declines in revenue in the academic year led to declines in construction and expenditure plans. There is reason for hope.

“Endowments are closely tied to stock market performance,” Branch said. “In the 2020 fiscal year, college endowments only grew by 2%. Since then, stock market growth performance has been extremely aggressive. College endowment growth should follow in kind with endowment dollars flowing back into the construction space.”

Healthcare buildings

- Dodge 2021: 8% ($30.1B); 2022: 9% ($32.9B)

- ConstructConnect 2021: 0.9% ($29.3B); 2022: 17.0% ($34.3B)

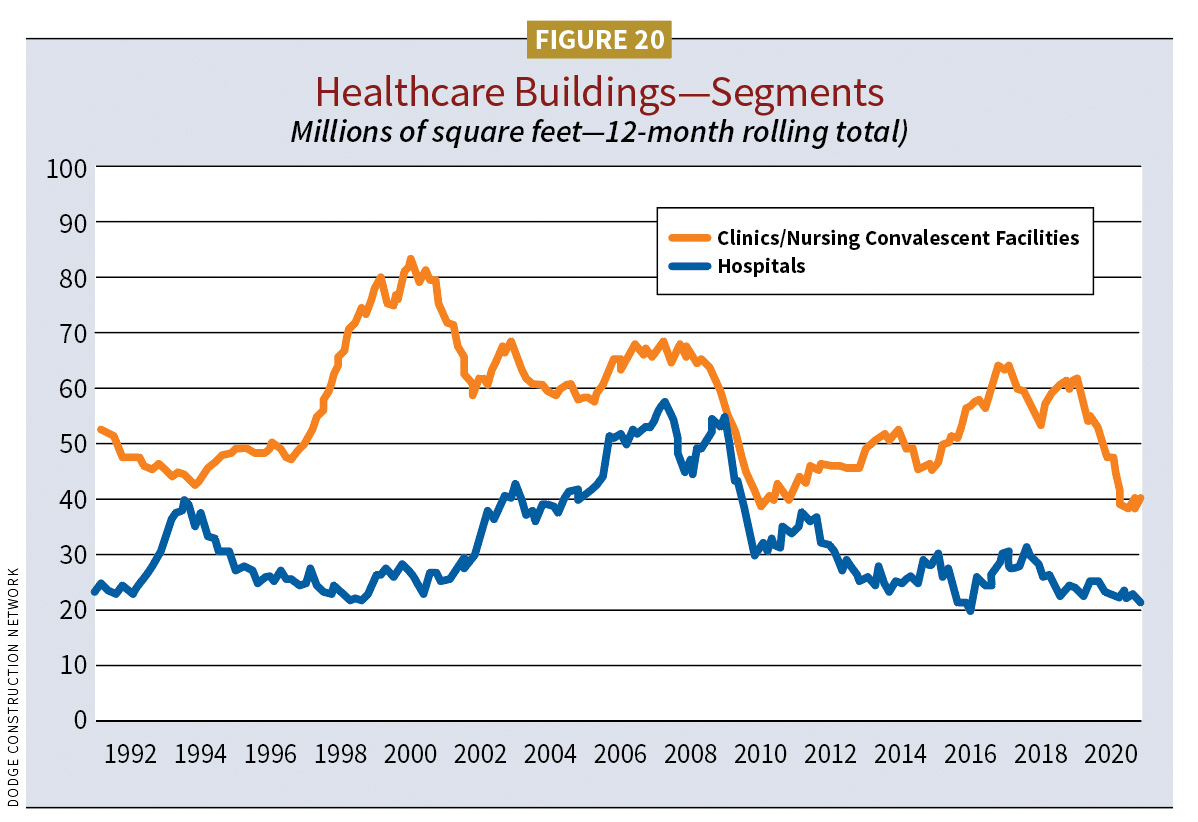

The healthcare construction is healthy. Healthcare has shown the strongest market strength outside of warehouses. Clinics and nursing homes are outperforming hospital construction. There was a shift toward private clinics in the 1990s, which narrowed during the recession. The gap has since widened, which Branch attributed to COVID-19 turmoil for nursing homes and a completed construction cycle of outpatient facilities over the past decade. (See Figure 20).

Transportation buildings

- Dodge 2021: 7% ($10B); 2022: 5% ($11B)

- ConstructConnect 2021: 42.3% ($4.1B); 2022: 41.3% ($5.78B)

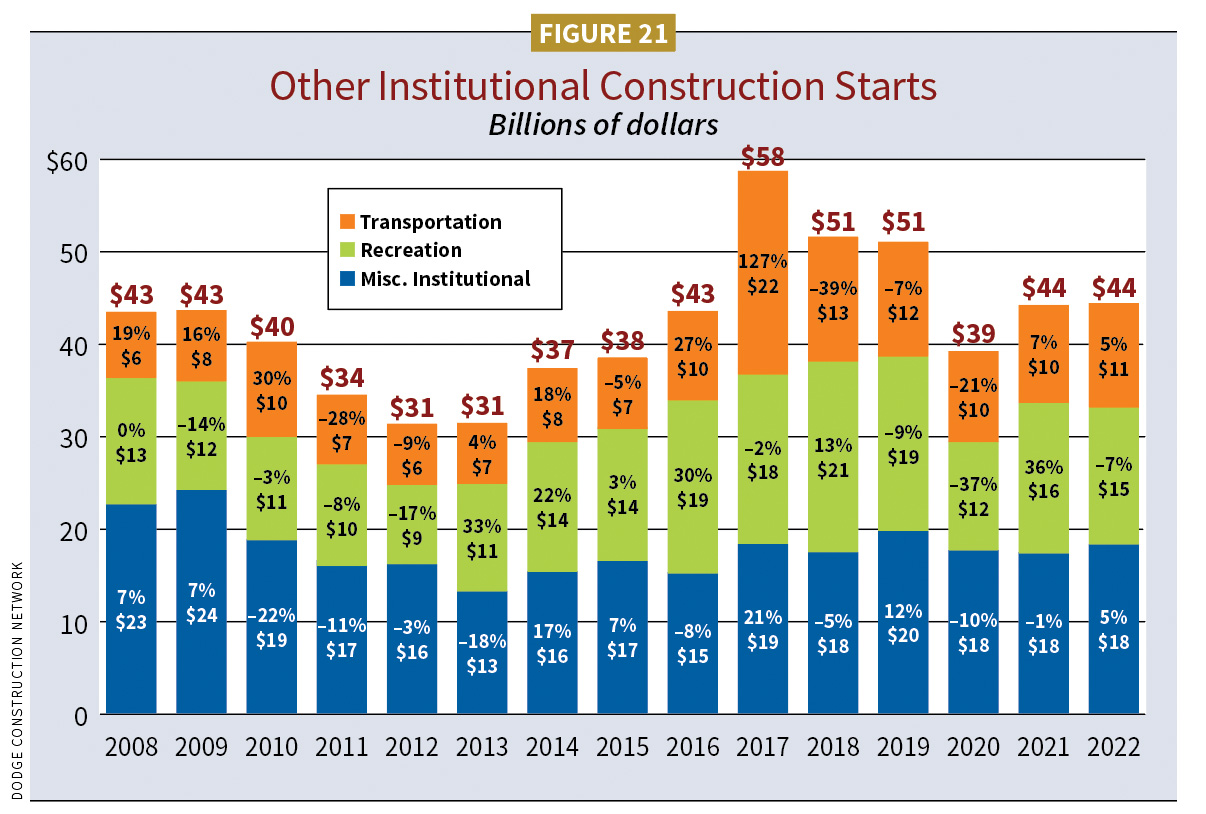

After dropping an estimated $22 billion in construction in 2020, the transportation market gained 7% ($10B) in 2021. This year, Dodge expects another 5% ($11B) advance. Some market category mismatch: ConstructConnect saw a 42.3% ($4.1B) gain in 2021 and expects 41.3% ($5.78B) in 2022. Money in the infrastructure act for airport terminals could also contribute to 2022 growth. (See Figure 21.)

Recreation buildings

- Dodge 2021: 36% ($16B); 2022: –7% ($15B)

- ConstructConnect 2021: –1.75% ($10.6B); 2022: 16% ($12.3B)

The recreational market was stronger in 2021 coming off a –37% decrease in 2020. Last year (2021) rebounded with a 36% ($16B) increase in starts value. That progress, however, will be short lived in 2022, with a projected –7% ($15B) due to a weakness in casinos and convention centers. Some market category mismatch: ConstructConnect saw a small contraction in 2021 of –1.75% ($10.6B). A 16% gain ($12.3B) is forecast for 2022.

Miscellaneous institutional

- Dodge 2021: –1% ($18B); 2022: 5% ($19B)

- ConstructConnect 2021: 4.6% ($19.6B); 2022: 5.9% ($20.7B)

The “miscellaneous” of this market encompasses public buildings, including capitols, courthouses, police and fire stations, detention and other administrative facilities. In 2021, this market was at –1% ($18B), a recovery from 2020’s –10%. In 2022, expect a projected return at 5% ($19B). ConstructConnect lists these markets as government. It estimated growth in 2021 at 4.6% ($19.6B) and in 2022 at 5.9% ($20.7B).

MANUFACTURING

- Dodge 2021: 46% ($22.7B); 2022: 0% ($22.6B)

- ConstructConnect 35.6% ($29.3B); 2022: -0.8% ($29B)

Manufacturing building starts in 2021 were stronger than expected, growing 46% ($22.7B) and exceeding all construction sectors. In 2022, Dodge expects flat growth. ConstructConnect measured 36.6% ($29.3B) for 2021 and –0.8% ($29B) for 2022. The starts of two large petrochemical plants—a $1.5B refinery in Port Arthur, Texas; and an $825 million biofuel plant in Louisiana—contributed to the sector’s success.

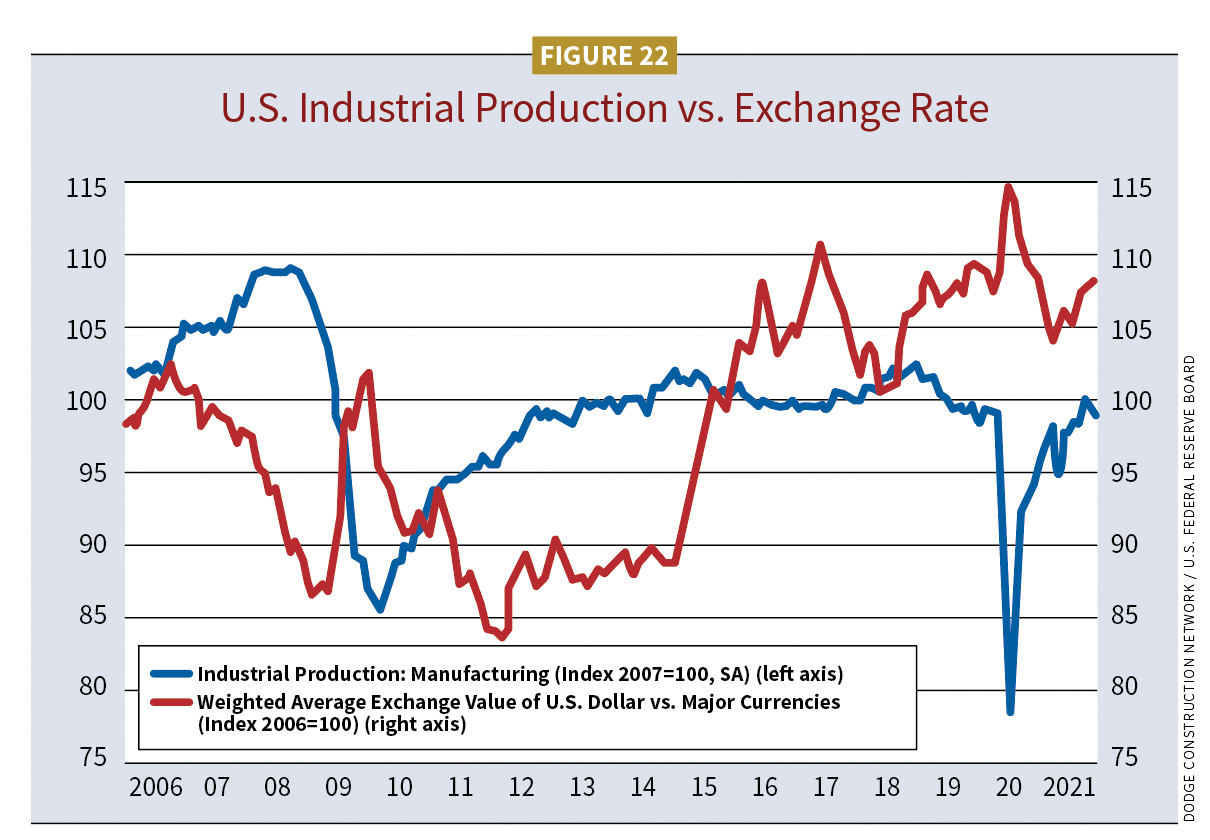

“Other” manufacturing—defined by Branch as motor vehicles and parts (e.g., EV battery plants), food production on the rise, and semiconductor chip manufacturing plants (possible future domestic growth in response to overseas supply chain issues)—was more uneven.

“Manufacturing output is recovering slowly prior to the pandemic, which is great news,” Branch said. “That trend of plants getting back to normal is certainly moving in the right direction.” (See Figure 22.)

NONBUILDING

- Dodge 2021: 1% ($194B); 2022: 6% ($205.8B)

- ConstructConnect 2021: 4.9% ($162B); 2022: 15.0% ($186B)

Better federal funding, better market. Nonbuilding starts in 2021 increased 1% ($194B). In 2022, starts rise 6% ($206B). ConstructConnect categorizes this work under “civil.” As such, it saw a 4.9% ($162B) gain in 2021 and expects a 15% ($186B) advance in 2022. Passage of the Infrastructure Investment and Jobs Act ($550B) was assumed in the 2022 forecasts. The bill’s dollars will start to enter this sector in 2022, but will mainly impact 2023–25. Dodge assumes 80% of the measure’s funding will be spent by 2026.

“In terms of influence, our models are suggesting total nonbuilding starts will increase by 33% by end of 2026,” Branch said.

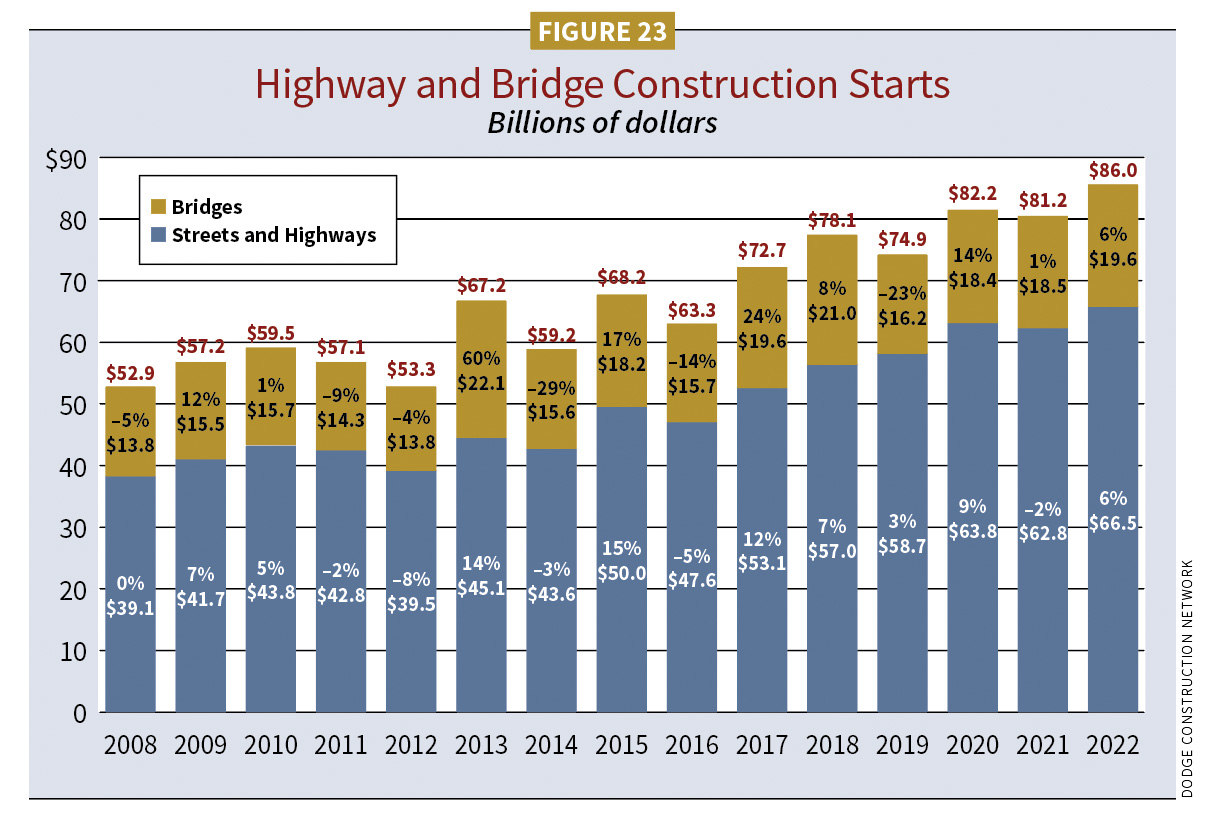

Streets/highways and bridges

- 2021 Bridges: 1%/$18.5B (Dodge); 17.43%/$18.8B (ConstructConnect)

- 2022 Bridges: 6%/$19.6B (Dodge); 19.2%/$22.4B (ConstructConnect)

- 2021 Streets & Highways: –2%/$62.8B (Dodge); 9.75%/$70B (ConstructConnect)

- 2022 Streets & Highways: 6%/$66.5B (Dodge); 9.73%/$76.8B (ConstructConnect)

Starts for streets/highways and bridges combined in 2021 represented a small –1.21% ($81.2B) decrease. This year, the market will represent a respectable 6% ($86B) advance. ConstructConnect anticipated a positive 27.18% ($88.8B) in 2021 and another 28.93% ($99.2B) gain this year. Supporting these markets was the Fixing America’s Surface Transportation Act, extended several times in 2021 at flat funding levels. The Infrastructure Investment and Jobs Act allocates $110B to streets and bridges, providing a positive effect for this sector. Branch estimates 10% of the law will be felt in 2022, which will help to provide the projected 6% gain (see Figure 23). The top state for 2021 street and bridge starts were Texas, California, Florida, Illinois and Indiana.

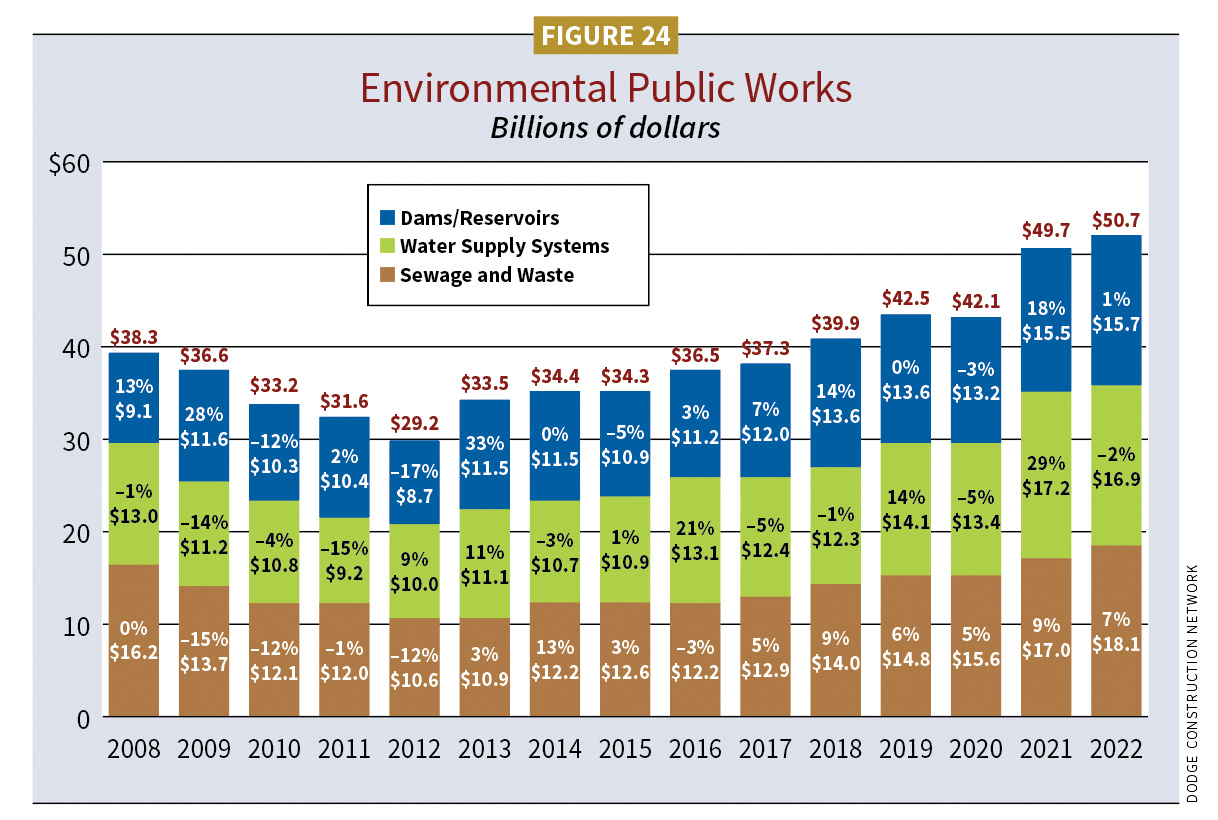

Environmental public works

- 2021 Dams and Reservoirs: 18%/$15.5B (Dodge); -6.4%/$7.0B (ConstructConnect)

- 2022 Dams and Reservoirs: 1%/$15.7B (Dodge); 7%/$7.9B (ConstructConnect)

- 2021 Water Supply Systems: 29%/$17.2B (Dodge); –2%/$16.9B (ConstructConnect)

- 2022 Water Supply Systems: –2%/$16.9B (Dodge); –2%/$16.9B (ConstructConnect)

- 2021 Sewage and Waste: 9%/$17.0B (Dodge);

- 2022 Sewage and Waste: 7%/$18.1B (Dodge)

Note: ConstructConnect combines Water and Sewage Treatment. 2021: 9.92% ($34.3B); 2022: 10.21% ($37.8B).

These markets performed strongly in 2021, advancing 18% ($49.7B). Dodge expects work to grow another 2% ($50.7B) this year, but water supply systems will contract. ConstructConnect saw the dams and reservoirs market lose -6.4% ($7B) in 2021, dropping its estimates of environmental public works to a 3.52% ($41.3B) gain in 2021. This year, it expects impressive overall growth of 17.21% ($45.70B), helped by the infrastructure act. Appropriations had not come through by November 2021, so funding is flat for now.

In 2021, emergency restoration funds for Hurricane Ida gave the Army Corps of Engineers about $6B. Notable large projects in 2021 lifted the fortunes of this sector. Branch cited North Dakota’s $1.2 billion Red River Valley Water Supply Project and a $528 million water reclamation project for Salt Lake City’s Department of Public Utilities. Like streets and bridges, large environmental public works projects that started in 2021 will feed into 2022 (see Figure 24).

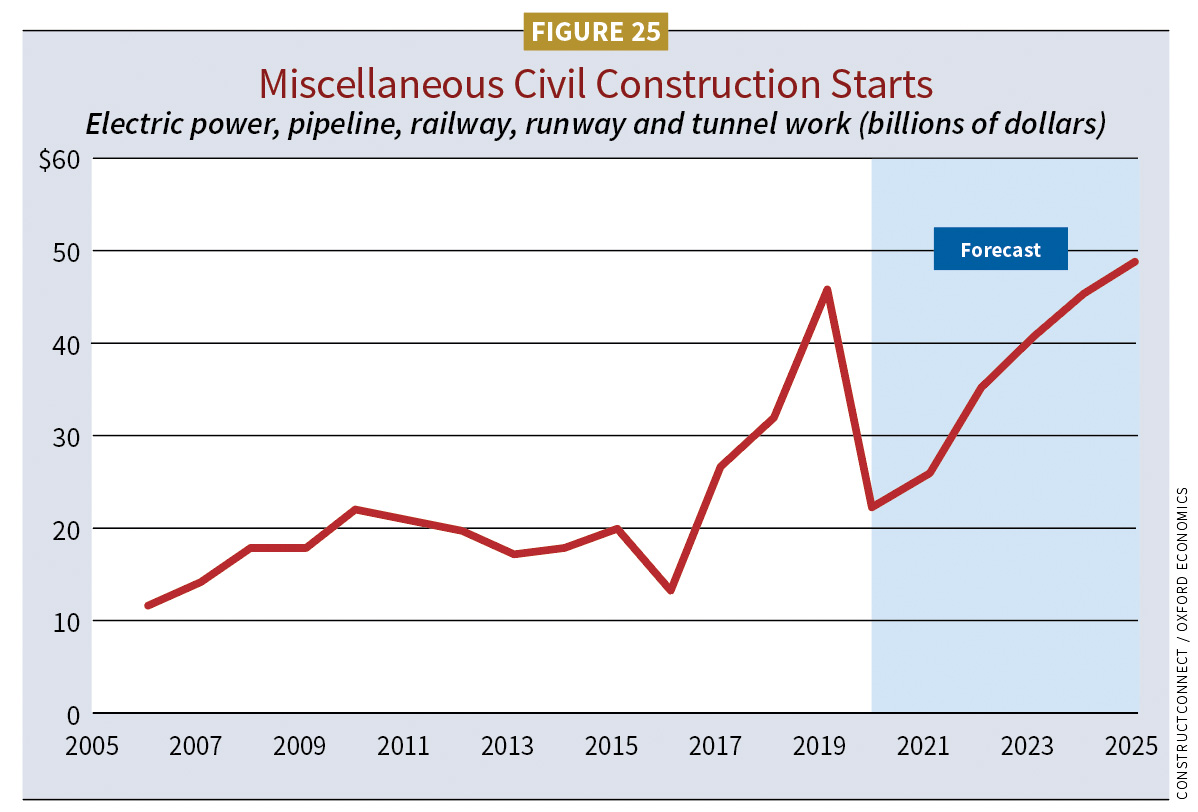

Power and utilities

- Dodge 2021: –3% ($35B); 2022: 10% ($38.5B)

- ConstructConnect 2021: 50% ($9.1B); 2022: 38.25% ($12.6B)

Here is another sector expected to turn a corner this year. In 2021, Dodge estimated a 3% contraction ($35B) for this market, which was an improvement over 2020’s –35% performance. Recognizing some market category mismatch, ConstructConnect saw a 50% gain ($9.1B) in 2021 and another 38.25% ($12.6B) this year. (See Figure 25.)

Lifting this market in 2022 are liquefied natural gas (LNG) plants that broke ground in 2021, including the $8.5B Venture Global LNG Export facility in Plaquemines Parish, La., and utility-grade solar and wind power projects helped by the extension of the investment and production tax credits. According to S&P Global Market Intelligence, in 2022, the United States is expected to add a record 44 gigawatts (GW) of solar, 27 GW of wind and more than 8 GW of battery storage.

Dodge also expects to see increased activity in the transmission and distribution line system as $73B, as the infrastructure act targets grid hardening (system resilience to storms, fire and climate) as well as building out transmission lines.

Summary

The construction industry and the economy as a whole need to maintain sustainable growth to stay on schedule for a full return. Electrical contractors will be interested in the money allotted in the infrastructure act for electrical grid enhancements ($73 billion) and broadband ($65 billion). The expected growth in residential, nonresidential and nonbuilding is a win, but a full construction recovery may take more time. Taming COVID-19, easing material prices, a working supply chain and Washington staying out of its way are all needed. While global factors could trip us up, too (see Figure 26), economists expect the stressors of 2021 to abate. That progress will be a good foundation for a recovering construction industry that should see growth in 2022 and beyond.

Header image: Bonotom Studio Inc. / Shutterstock / Mus Illustrations / Macrovector / Real Vector / Sensvector / BNP Design Studio

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].