You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

The first two columns in this series provided an overview of occupational fraud and suggestions for tightening internal controls to protect your electrical contracting business. This final column examines factors that may cause an employee to commit fraud and some methods experts use to detect deception.

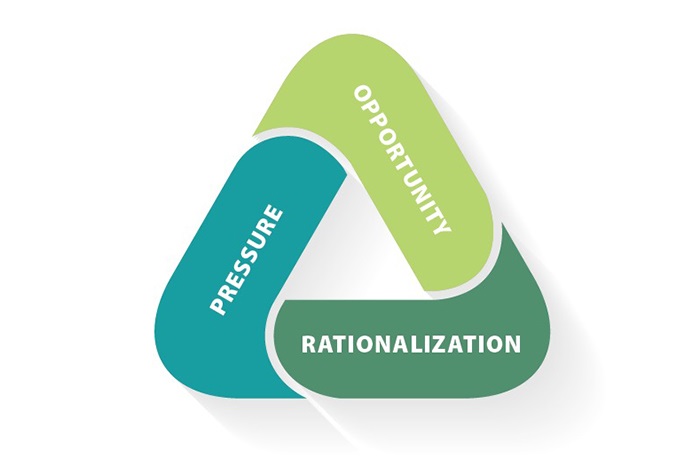

The fraud triangle

In his book, “Other People’s Money,” sociologist Donald R. Cressey hypothesizes that a “non-shareable” problem with no other solution triggers a person to violate a position of financial trust and then rationalize the fraud to maintain the illusion of trustworthiness. His “Fraud Triangle” (above) shows three components required for a trusted person to commit a fraudulent act.

Pressure, the first component, provides the motivation. It may be a personal financial debt, the imminent loss of a job or a business on the verge of failure. Believing there is no other solution, the person begins to consider criminal acts, such as stealing money or falsifying financial reports.

Opportunity, the second component, is the method for committing the crime. Believing there is a low risk of getting caught, the person finds a way to use his or her position of trust, while maintaining secrecy to protect his or her social status.

Rationalization is the final component. Usually a first-time offender, the person doesn’t see him or herself as a criminal—just an ordinary person in a tough situation. Justifications might include, “I was just borrowing the money,” or “I was underpaid,” or “My boss is cheating, too.”

Vigilance

You must be as vigilant in monitoring people as you are with financial records. Watch for employees who seem to be spending beyond their means or have problems in their personal lives, such as a costly divorce or an expensive medical issue. Pay attention to changes in mood or job performance. Notice any employee who is reluctant to take a vacation or refuses help. Consider this lesson from the bank that forced a reluctant teller to take her two-week vacation, allowing time to track the embezzlement of funds from dormant accounts.

Vendors may partner with employees to commit fraud, so watch for an employee who seems unusually close to a specific supplier or suddenly changes to another. Verify that each paycheck goes to an actual employee, check the endorsements on the backs of canceled checks, and be alert to an employee who is always the earliest to arrive and the last to leave the building. Investigate further if an employee resists changes in record-keeping procedures or frequently amends or corrects reports.

Detecting deception

A fraud examiner must build rapport with a stranger, determine that person’s state of mind, and detect deception while extracting the facts during an investigation. This requires training in observing body language, particularly reluctance to make eye contact, excessive blinking, and nervous tics or hand movements. The examiner also analyzes “paralinguistics”(not only what is said, but how it is said, including tone, pitch, pace, timber, word choice) and “dysfluencies” (speech that isn’t smooth or grammatical).

The FBI and fraud examiners use linguistic text analysis, based on controlled experiments from the 1970s, to analyze written and oral statements. Investigators determine typical factors of a truthful statement and look for deviations in written statements. Suspects and witnesses often reveal more than they intend to through specific word choices, grammar and syntax.

For example, liars may answer questions with questions of their own (“Why do you think I would do that?”), swear oaths (“cross my heart”), and use euphemisms (“borrowed” instead of “stolen”). They also may use more vague language (“sort of” or “I guess” or “maybe”) to allow some leeway in modifying a story.

Trustworthy people use the past tense to describe past events, while deceptive people may use present tense during part of the story. Truthful people tend to include more details, because experiences stored in long-term memory are highly detailed.

The deceiver minimizes self-reference, substituting “you” for “I,” fewer personal pronouns, and passive instead of active voice (“The job didn’t get done on time,” instead of “I didn’t finish the job on time”). The liar may also allude to actions without being definite (“I needed to lock up the financial records,” instead of “I locked up the financial records”).

Analysts look for balance between the three parts of a narrative: Prologue (background and early events) should be 20–25 percent; critical event should be 40–60 percent; and aftermath should be 25–35 percent. If the account is too short, the deceiver may have left out critical information. If it is too long, he or she may have given false information. The average sentence length is usually 10–15 words, and sentences that are too long or short may also indicate deception.

You want to trust your employees, but blind trust is risky. If you detect a potential problem early, you have the chance to help a struggling employee find a better solution than committing fraud.

About The Author

Denise Norberg-Johnson is a former subcontractor and past president of two national construction associations. She may be reached at [email protected].