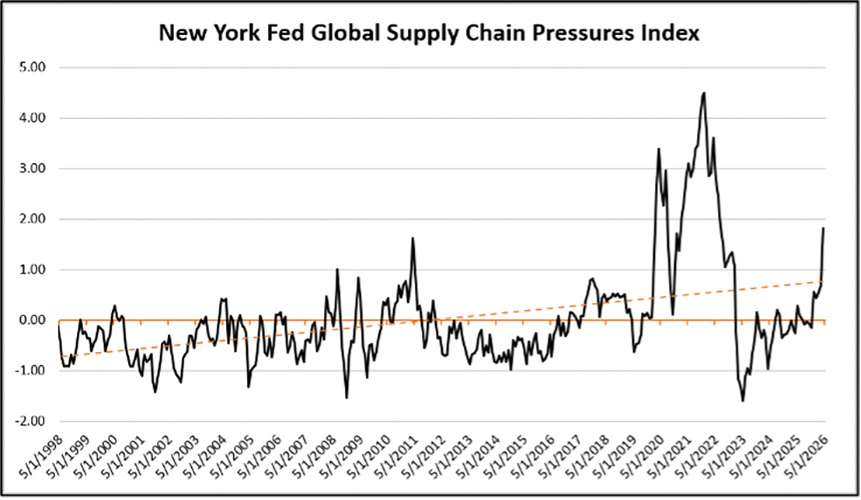

If your leadership teams are not having weekly meetings and updates about the global supply chain situation, you might want to consider starting. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index (see Figure 1) has surged at its fastest rate since April 2022 at the start of the war in Ukraine. Based on data and New York Fed models, the current situation is the third most difficult supply chain period in history.

Figure 1

The looming emergency is petrochemical shortages. We are already hearing of food shortages on grocery store shelves in Malaysia (far upstream in the supply chain) because of packaging shortages. Mexican manufacturers warned in April that some of their reductions in output were coming at the hands of inbound input shortages. They just couldn’t keep their supply chain continuous and replenished to keep their assembly lines operating. That was the canary in the coal mine.

Supply chain woes continue

At one point, a high-ranking general was commenting on supply chain vulnerabilities during the pandemic. He mentioned that the Department of Defense didn’t realize how exposed its supply chain was at the time because they had not mapped it far enough “upstream.” They had visibility into their primary suppliers and perhaps even into their tier two suppliers, but they couldn’t see further upstream into tier three and four suppliers. Many have fixed that, but most corporations have no visibility further upstream. That’s where surprises come from.

Electrical contractors are notoriously out of control. By that, I mean they are at the mercy of what they can’t affect. They are often several levels removed from the end-user and have no real control over suppliers, and even less over their suppliers’ suppliers. That forces a lot of speculation regarding supply, which heightens the risk of inventory imbalances.

I know that the general economy is doing well at this time. The Atlanta Fed GDPNow estimate is still showing a Q2 growth rate of 4.0%. But that is largely due to a surge in consumer spending activity driven by tax refunds, inventory building activity and nonresidential fixed investment. Models of the next 18 months, taking into account higher energy prices and other factors, are now showing some changes.

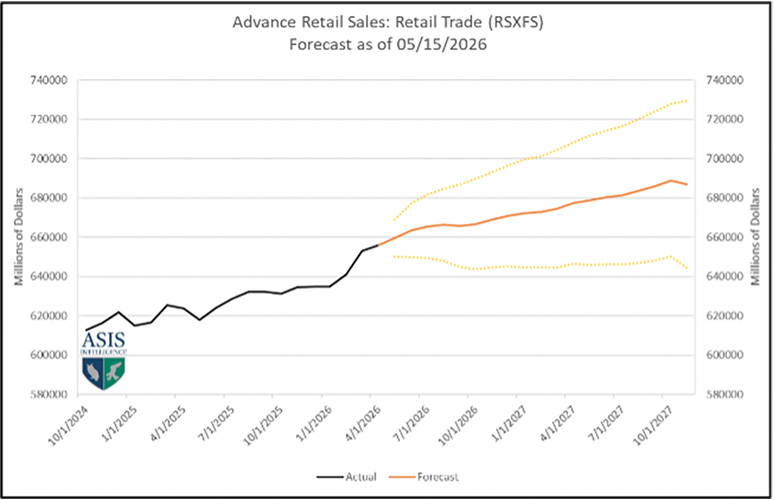

Retail accounts for the majority of U.S. GDP activity (consumer spending in the broad sense is 60%–70% of GDP). This sector is still poised for strong growth. The forecast shows it growing at 5.7% year-over-year.

One thing to note is the bottom dotted line in Figure 2. These dotted lines are generated with a thousand simulations of the data and paint a best-case scenario (upper bound) and worst-case scenario (lower bound). The lower-bound risk still shows little risk in the forecast. Despite a lot of headline noise in the press, the consumer risk is fairly light. Steady wage growth and a reasonably steady labor market is still driving consumer spending.

Figure 2

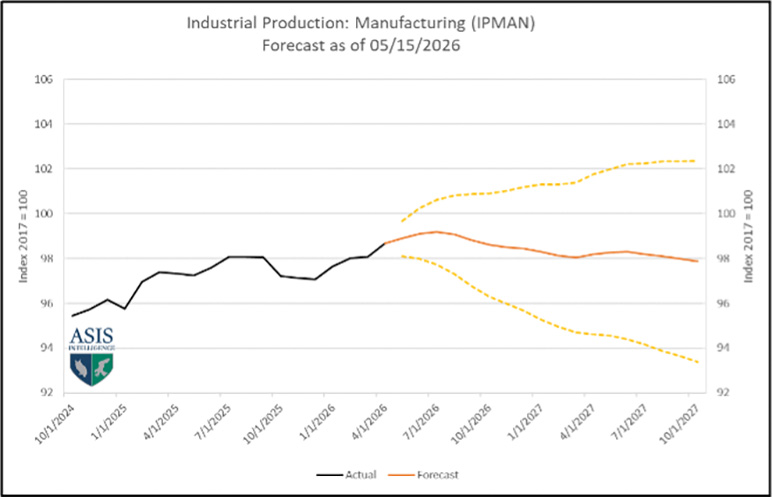

Manufacturing outlook

The manufacturing outlook, on the other hand, took a sharp turn downward and the lower bound risk went recessionary. The model is seeing downside risk generated primarily by supply chain pressures.

Most models are also seeing some strong headwinds from rising bond yield rates. They have hit concerning levels. If this forecast holds and there is no lasting breakthrough in the Middle East, manufacturing production would come in at 1.4% for the full year, which means that some sectors would dip sharply into contraction while a few staunch growth engines in manufacturing would continue to drive overall output higher.

The forecast likely sugarcoats how rough it could get for many firms if these conditions continue. It all hinges on whether the Strait of Hormuz is open or closed. (See Figure 3.)

Figure 3

If the retail forecast holds, manufacturing likely can’t. It will have to improve over time because retailers will need to replenish their inventories. And with global output pressures higher, a larger percentage of those products will need to get sourced within the USMCA markets. That would drive this manufacturing production forecast higher.

The bottom line is that we have yet to feel the true impact of the Iran war. This comes as no shock since these conflicts take a while to unfold. The oil world faced a glut just a few months ago, and it has taken time for the crisis to reverse and introduce a shortage. Inflation unfolds quickly, but reactions are slow as consumers try to keep holding on to their patterns as long as possible. The reactions will become apparent in the next month or so.

armada ci / Federal Reserve Bank of New York

About The Author

KUEHL is managing director of Armada Corporate Intelligence. He provides forecasts and strategic guidance for a wide variety of clients around the world. He is the co-author of two Armada publications, The Flagship and The Watch. Reach him at [email protected].