There’s much to be confident about in the construction industry. Spending is up, supply chain and inflationary effects are easing and employment is strong, among other good news. While there are areas to watch, “Keep calm and carry on” is an apt motto going forth. The future looks bright.

A look at spending

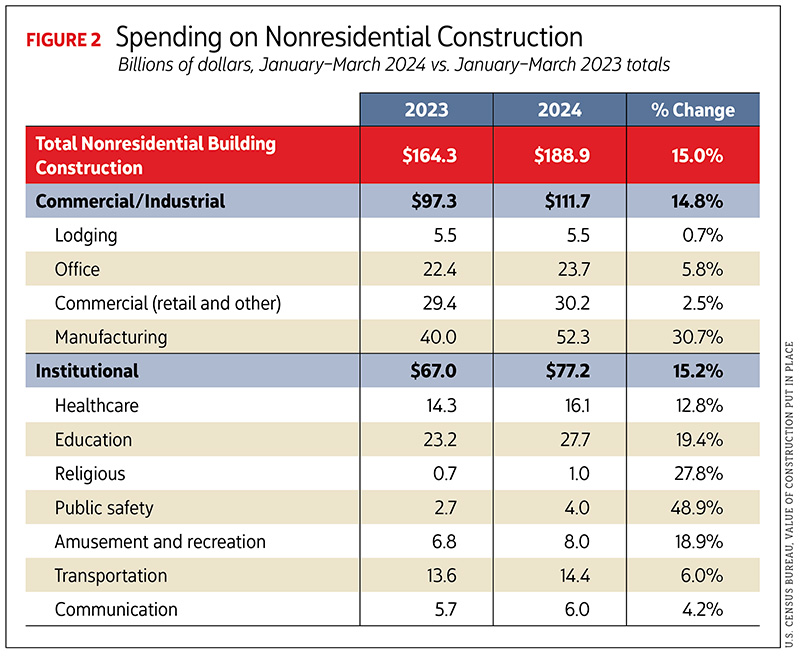

We’ve seen strong spending in the construction industry so far this year. In the first three months of 2024, total nonresidential building spending was up 15% over the same period in 2023.

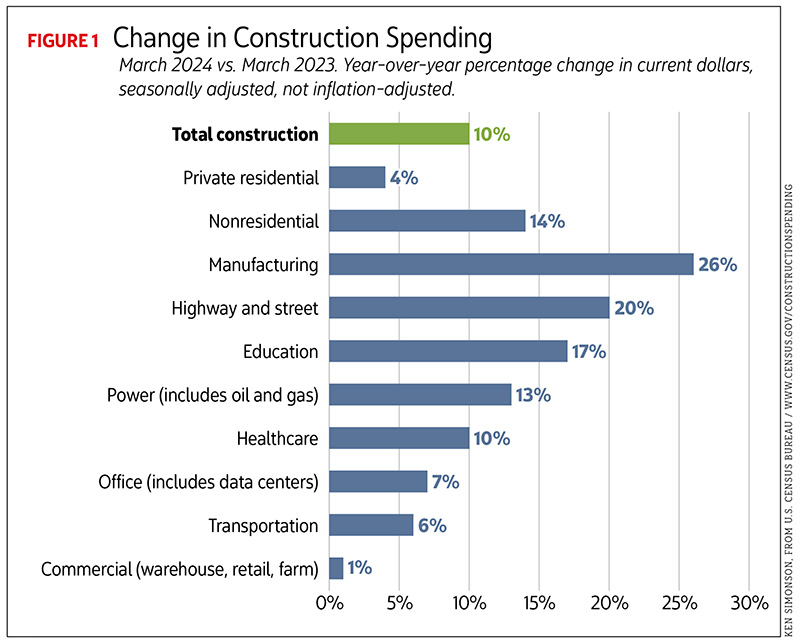

Kermit Baker is chief economist for the American Institute of Architects (AIA), Washington, D.C. In looking at the health of construction activity through put-in-place spending, Baker said strong activity in 2023 extended into the first three months of 2024. The numbers include an overall spending increase of 20% and almost 30% for commercial and industrial, with a few key verticals driving that growth. See Figure 1.

“The lodging number was very strong, almost 20% gains,” he said. “Manufacturing was off the charts with 70% growth. Institutional showed more uniform growth. Most sectors were in the high single-digit or low double-digit rates.”

Moving into the second quarter of 2024, Baker sees a pattern of reduced growth.

“Overall spending is still pretty healthy at 15%, though down from 20% last year. Commercial and industrial has lagged a little bit at 15%, being up to almost 30% last year. Institutional, on the other hand, is a little bit stronger, moving from 10% to 20% to 15%.

“Manufacturing is still a very healthy number but down to 30% growth. On the institutional side, education is strong, moving from 13% to almost 20%. Education is the largest institutional sector; its growth means a lot in terms of spending throughout the construction industry. Religious and public safety also showed strong growth, but much smaller numbers,” he said. See Figure 2.

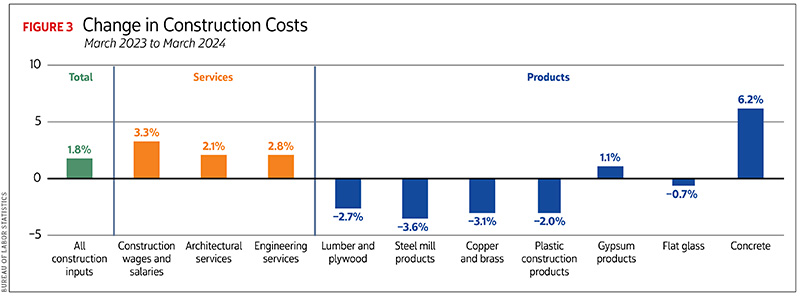

Costs for key construction inputs have largely stabilized. Before contractors start a job, they have to consider project costs, including wages and materials. See Figure 3.

The influence of interest rates

“If there is one subject that has dominated contractor planning this year, it would be the path of interest rates,” said Chris Kuehl, chief economist and co-founder of Armada Corporate Intelligence, Lawrence, Kan. “The rates are not the only factor in determining the fate of a given project, but [they are] the paramount motivator or demotivator.”

He said if rate cuts do appear, they are likely to be later this year.

“The sense is that there would be two- or three-quarter point reductions, taking rates from 5.5% to perhaps 4.75%.”

As to how that affects construction, Kuehl said, “Most big projects are currently on hold to some degree, as most assume that rates will come down, and financing these developments would become somewhat cheaper. The bottom line is that not much will be started until there is some confidence in a rate reduction.”

However, inflation remains a stubborn beast. Down considerably from last year, it is stuck at over 3%. The Federal Reserve wants it at 2%, so rate cuts will be fewer and later in the year. This holding pattern is keeping home prices high, interest rates elevated and developers uneasy. The prolonged effect is reflected in this construction outlook.

Sector strength

Sectors that reported growth will continue to grow, although less than they have been. Commercial is beginning to slow. While expansion in this sector will carry over into 2025, the amount will be determined by relaxing inflation, resulting in more rate decreases. Starts forecast numbers are down from what was projected in late 2023.

There are some encouraging signs. The May Consumer Price Index rose 3.3%, a small easing from April’s 3.4%. The Fed views this positively. The Labor Department’s “core” index (stripping out food and fuel prices) followed a similar trajectory at 3.4% in May from April’s 3.6%, which was the lowest annual increase in core inflation since early 2021.

Along with other economists and industry professionals, Michael Guckes, senior economist for ConstructConnect, Cincinnati, participated in “The Construction Economy Outlook Spring 2024: What Is Normal Anymore?” webinar on May 9, 2024. ConstructConnect collaborates with Oxford Economics for its starts forecast.

“2024 residential remains in the strong single digits from our prior outlook. So that’s good,” Guckes said. “But underlying this was a substantial reduction in our multifamily outlook. It was at 6.4% for 2024, and now it’s at 0.1%. So about flat. This will be partially offset by some improvement in our single-family outlook.”

Guckes sees strength in reshoring and national security, energy and electrification, and civil projects verticals. He said that government offices and laboratories may appear to be underperforming in 2024, but they are actually normalizing after a period of unprecedented growth.

Real estate firm CBRE, Dallas, conducted a survey of investor intentions that indicated multifamily properties are at the top of the investor preferred list for this year.

“For nonresidential building [construction], we are now at –4.8%,” Guckes said. “That is down further from the –2.4% outlook at the start of the year. Total nonresidential was [projected for 2024] at 3.3% at the beginning of the year. We have now reduced that to 2%. The U.S. grand total starts forecast has now been lowered from 4.5% to 3.3%.”

Guckes said commercial had been forecast at 9.9% for this year, but is now reduced to 2.3%.

Soft planning

AIA’s Architecture Billings Index (ABI) helps track construction conditions by showing architecture firm planning activity around 9–12 months. A score of 50 is considered healthy growth. The AIA/Deltek ABI for April 2024 was 48.3, up from 43.6 in March. Nonetheless, April’s score was the 15th consecutive month of declining billing attributed to inflation, supply chain and other issues.

By region, the numbers were 45.9 in the Northeast, 44.2 in the Midwest, 44.7 in the South and 47.8 in the West. Looking at sectors, commercial/industrial was 47.4, institutional at 46.1, mixed practice (firms that do not have at least half of their billings in any one other category) was 43.9 and multifamily residential stood at 45.6. Positively, project inquiries scored 54.8, but design contracts slipped from March’s 50 to 49.2 in April.

Baker sees some positives in commercial property values. Monthly numbers from Real Capital Analytics, Campbell, Calif., show that a downturn in property values is beginning to improve. He said negative numbers have been getting smaller in recent months in the apartment and retail categories. While large annual declines in office properties continue to accelerate, industrial property values are still increasing.

The Dodge Momentum Index (DMI), issued by the Dodge Construction Network, Bedford, Mass., measures nonresidential building projects in the planning process. It increased in May to 179.0 (2000=100), a 2.7% rise from April’s revised 174.3 and based largely on the strength of planned data centers.

Commercial planning rose 5.5%, but institutional planning fell 3.4%. For the 12 months ending in April 2024, Dodge found total construction starts up 2% from the 12 months ending in April 2023. In that month, nonresidential building starts retreated 8%, while residential starts rose 3%. Nonbuilding starts were up 16% on a 12-month rolling sum basis.

“Owners and developers are gaining confidence in 2025 market conditions, alongside more stable and predictable interest rates—spurring stronger commercial activity over the month,” said Sarah Martin, associate director of forecasting at Dodge Construction Network.

“Conversely, after last year’s growth, institutional planning is decelerating, as high material costs, labor shortages and elevated interest rates seep into planning decisions. The overall DMI remains 40% higher than May 2019 levels, indicating a steady pipeline of construction projects that will be ready to break ground through mid-2025,” she said.

If inflation continues, and in the absence of regular Fed rate cuts, forecasters predict a dramatic construction slowdown leading into 2025.

“Overall spending on nonresidential buildings is projected to increase a mere 4% this year and only 1% in 2025,” not adjusted for inflation, Baker said. “So real growth would be even lower. The commercial sector is expected to see no growth. Manufacturing will show healthy growth this year for projects currently in the pipeline [or] currently under construction, but spending would then stall next year to no growth. Institutional does better, but only modestly at mid-single-digit growth.”

Population changes

Kuehl said that demand and location help tell the tale of the current economy.

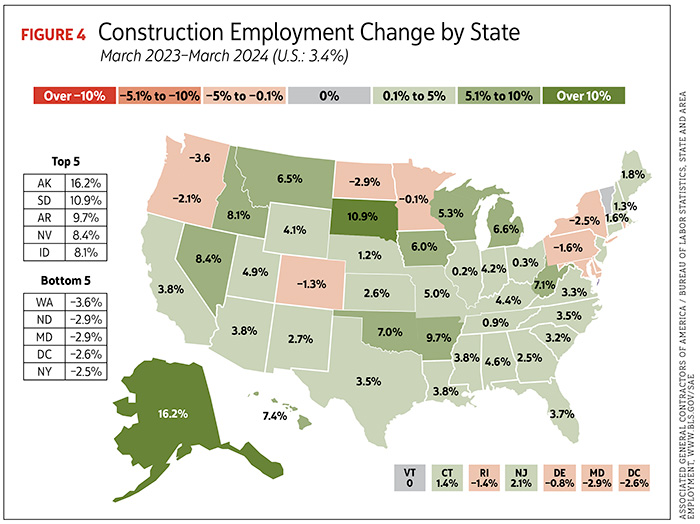

“There has been a substantial level of population movement over the last few years as people leave high-cost states to settle in lower-cost states,” he said. “This has meant a surge in demand for projects in Arizona, Texas, North Carolina, Tennessee, South Dakota, Montana and others. The demand creates enough profit potential for projects to proceed when interest rates are still high.” See Figure 4.

One headwind could hamper momentum and project development into 2025, even if interest rates fall.

“The United States and Europe started to engage a whole range of tariffs and regulations designed to pressure China, but most of the impact will be felt by those who are importing from China. Much of what the electrical contractors require comes from foreign sources, and China is still the dominant supplier. If tariffs escalate, so do the costs, unless and until there is an alternate source. Eventually there will be increased domestic production and more from other sources such as Mexico and India, but this will take time,” he said.

Employment: strong but not perfect

“Nonresidential construction employment has been growing very strongly for the past year and a half,” said Ken Simonson, chief economist for the Associated General Contractors of America, Arlington, Va. “Most recently, it is about twice as fast as total nonfarm payroll employment. Residential employment has also been positive year over year (y/y) and, though it slowed, it is still beating the total nonfarm payroll employment growth.”

According to the Bureau of Labor Statistics, the March 2023–March 2024 construction employment change was positive in 39 states. The South and Inland West have shown the strongest growth.

The need for labor hasn’t changed. Simonson thinks contractors wanted to hire twice as many people as they were able to. He highlighted contractors having trouble finishing multifamily projects.

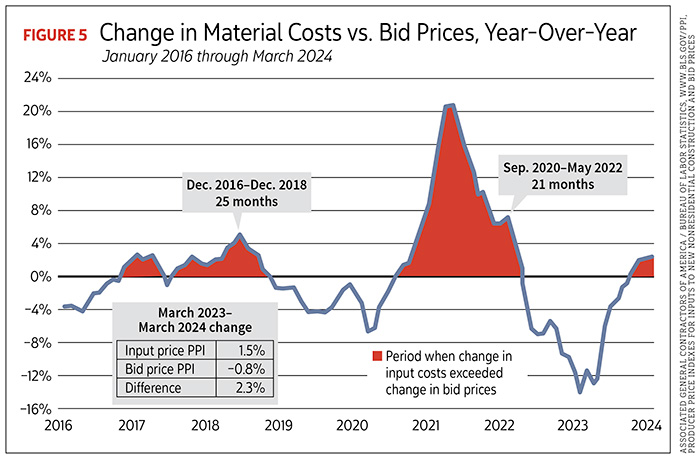

Nagging material prices

Simonson sees some moderation in material prices for the rest of 2024 that may give way to a gradual acceleration in costs. He doesn’t see such increases across the board and says they should hold to single digits.

“I expect input cost for materials to be rising from 3% to 5% this year,” he said.

Some supply chain issues will linger. “The biggest problem has been with electrical equipment,” he said. He referenced switchgear, transformers, electronics for elevators, HVAC and other products. See Figure 5.

Alex Carrick, chief economist for ConstructConnect, added, “Lumber is close to where it was before the pandemic. Still on the high end are paint and glass, lighting and plumbing fixtures, and heating and cooling equipment. Also, escalators, elevators and construction equipment in general.”

Unless there is a serious contraction, Carrick doesn’t see these prices moving down appreciably. In the long term, he sees steel and copper moving off their peak prices.

The shore and the horizon

Looking at construction activity in 2024 and beyond, Simonson expects the economic recovery to continue. At the same time, he sees higher interest rates “hanging around,” with the Fed beginning to cut rates in December or in 2025. Similarly, the 30-year fixed rate is likely to remain running at 7% or more, which will discourage many homebuyers. He does expect single-family home construction to pick up.

“But multifamily, warehouse and office construction are being hit hard by tightened lending standards and rising vacancy rates,” he said.

For Simonson, bright spots include strong construction growth in Las Vegas across multiple verticals and project formations resulting from money promised by the Infrastructure Investment and Jobs Act, the CHIPS and Science Act and the Inflation Reduction Act. However, money may be slow to turn into construction awards and spending.

Morgan Stinson is vice president of content acquisition for ConstructConnect. In bidding activity for commercial construction Q1 2024 through April, she said, “Over the last five years, we observed U.S. bids performing better than in 2019, 2020 and 2021. However, there is a noticeable decline compared to the surge we saw in 2022 [when many previously postponed bids resumed in 2023]. This stabilization and normalization of bids appears to have continued into 2024.”

Stinson said that the volume of newly created projects is “on par” with the planning and building stages in 2019 and 2021.

“Though slightly behind in 2022, there’s a notable 7% increase compared to last year. [Through April] 2024, we’ve observed an 11% increase in planning projects compared to last year,” she said.

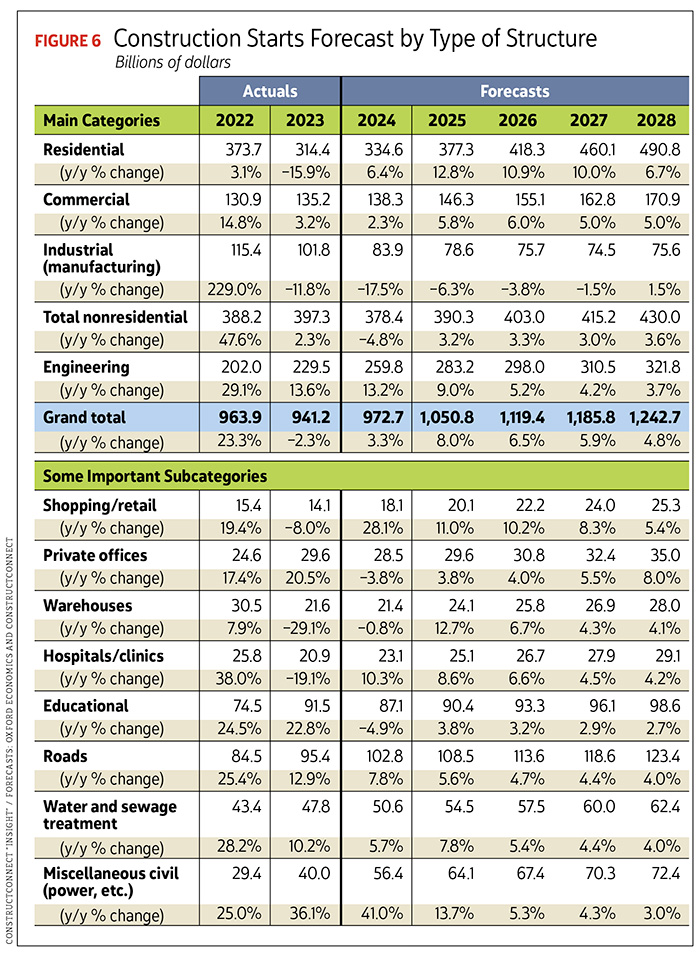

Stinson saw a marked uptick in civil building and a “noticeable resurgence” in sectors such as retail (up 27.5% from 2023) and restaurants (23%), grocery stores and a 4% rise in construction for educational and medical facilities. She said data center projects are up 18% and the initial surge in warehouse/distribution has tapered off. That sector is down 16.5%. Stinson sees a decline in municipal (–3.5% from 2023), multifamily residential (–4%) and office construction (–20%). See Figure 6.

A pipeline with surprises

In looking at the pipeline of construction projects, Carrick noted the strength of data centers and those in planning also caught his eye.

“Columbus, Ohio, is becoming somewhat of a high-tech city,” he said. “Railroads also caught my attention. While Brightline just completed that connection between Miami and Orlando in Florida, it has now started work on a high-speed rail link between Las Vegas and Rancho Cucamonga, Calif. In roadways, Texas has a huge road construction program underway.”

Carrick also noted entertainment and amusement verticals, including Universal Orlando, which is spending millions of dollars. Disney has nearly doubled its capital expenditures to roughly $60 billion on its theme parks in California and Florida over the course of some 10 years.

An ease in interest rates and lending will go a long way toward returning a measure of construction planning confidence. While growth is smaller right now, it is ready to return with a stronger hand. In the meantime, explore business activity in new verticals, maybe one related to your business. And embrace technology—your customers do.

“The fastest-growing sector for construction for the last three years has been manufacturing and a close second has been the medical community,” which are both technology-focused, Kuehl said.

Remember that “Keep calm and carry on” means maintaining confidence and a cool head amid adversity. Better days for everyone are within reach.

stock.adobe.com / Agor2012

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].