Working in this economy is a balancing act. Like walking across a tightrope or balance beam, it takes skills and deliberate choices to keep walking straight, no matter what the economy has in store.

The economic performance of construction is on a steadier track than the U.S. economy, which remains unpredictable. Growth is threatened, yet unemployment has hovered at its lowest in 55 years. Predictions of a recession over the past 18 months remain conjecture. The year-end gross domestic product will be smaller than 2022, but is forecast in the positive at about 0.8%. For every drag on the construction industry, such as a weakened residential market, there’s plenty of good news in other sectors like nonresidential and nonbuilding.

The U.S. economy is expected to slow in the second half of this year, but construction will battle through as 2023 progresses. Sector strengths will help balance construction activity. In looking at 2023 figures up through May year-over-year (y/y), Dodge Construction Network, Hamilton, N.J., reported total construction starts were 9% higher than 2022, a slight decline from a 11% gain in April y/y. May y/y nonbuilding starts gained 30%, nonresidential grew 26%, but residential declined 15%.

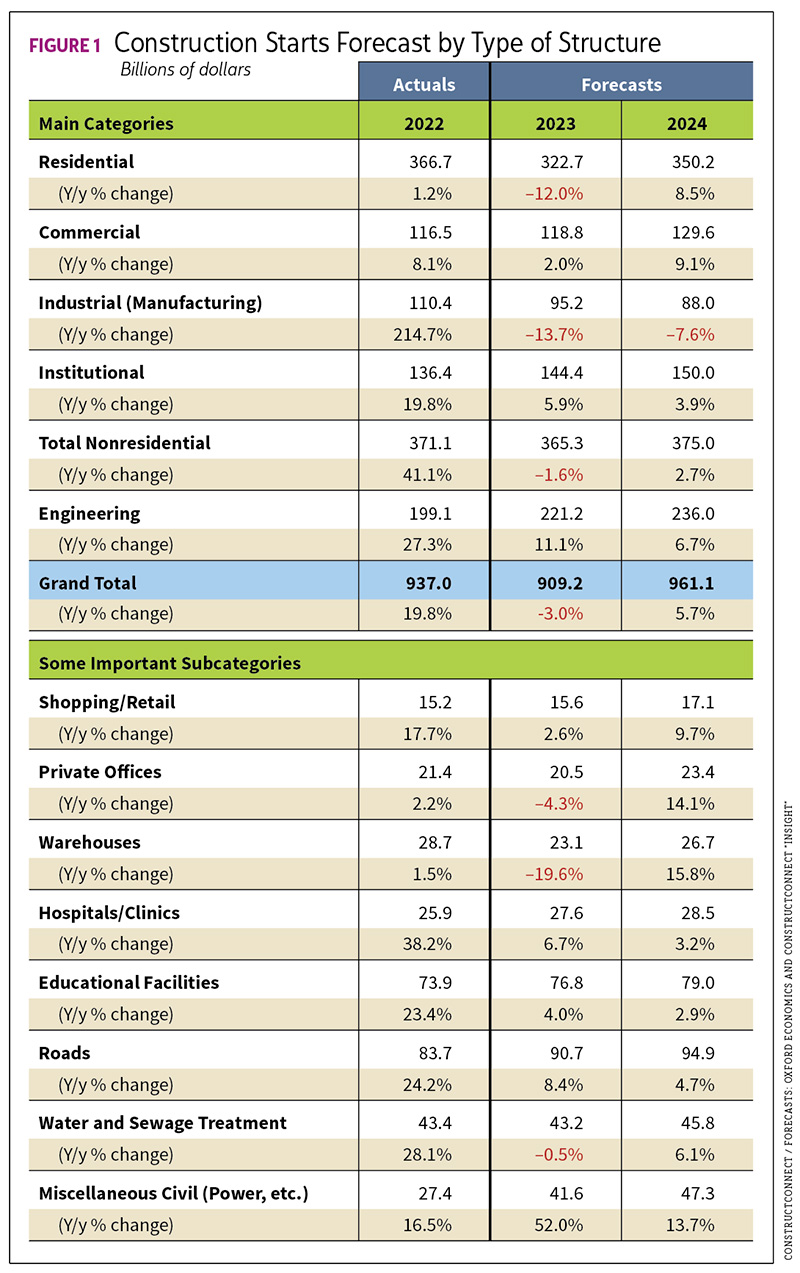

Looking at performance in the first five months of the year (year-to-date/YTD), Dodge showed total construction starts shrinking 6%. Residential starts fell 25%, nonresidential starts fell 1%, and nonbuilding starts up 25%. ConstructConnect, Cincinnati, numbers diverge. They show total construction starts through May declined 30.1% which is attributed to fewer mega project starts. Remove mega project activity and the total starts comes in at –11.3%. (See Figure 1.)

In its Summer 2023 U.S. Put-in-Place (PIP) Construction Forecasts, ConstructConnect projected PIP dollars gaining 2.8%, or roughly $1.8 trillion (current dollars), by year’s end. Stripping out inflation, PIP retracts by 2.3% (roughly $1.2 trillion) in constant dollars.

“The construction sector continues to sweep its economic worries under the rug,” said Richard Branch, chief economist for Dodge Construction Network. “While the presence of, or lack thereof, large manufacturing projects each month has made the data more volatile, the underlying trends point to a very healthy sector. However, this is likely transitory. The Dodge Momentum Index, which tracks [nonresidential] projects entering the earliest stages of planning, is falling, which should lead to weaker starts in the second half of the year—especially for the private sector.”

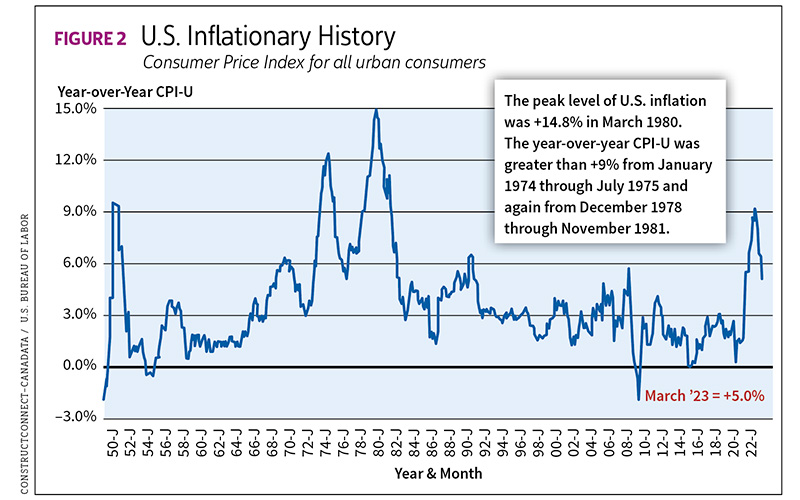

Alex Carrick, chief economist for ConstructConnect, said in May, “The unemployment rate, not seasonally adjusted at 3.1%, is about as low as it could possibly go [the May rate rose to 3.7% with a contradiction—more jobs created in May/339,000, versus April/294,000]. Our forecasting partner, Oxford Economics, doesn’t have very strong growth numbers for GDP. They’re saying 0.9% this year and 0.4% next year. And they do expect a couple of quarters of probably negative performance in Q3 or Q4, maybe Q1 2024. So, a slowdown is expected. But the stock market doesn’t seem to be terribly worried. At the end of April, NASDAQ and Dow Jones and the S&P index were off by about 20% versus their 52-week lows. And inflation has improved considerably. It’s gone down to 5% year-over-year. I’m particularly encouraged by that. In June of last year, it was 9%.” (See Figure 2.)

Construction planning weakens

Branch reported the Dodge Momentum Index (DMI) has slipped. The index fell in May to 180.5 (2000 = 100) from the revised April reading of 184.1, itself a fall from March’s 190.6. The DMI’s commercial component dropped 6.1% in May, but institutional improved 5.6%. Activity is stronger May 2023 y/y as commercial and institutional components showed planning growth of 7% and 18%, respectively, and the overall index is up 11% for the year. The DMI has been shown to lead construction spending for nonresidential buildings by a full year.

“Weaker commercial planning is driving the DMI’s decline, as it is more exposed to real-time economic changes than the largely publicly funded institutional segment,” said Sarah Martin, associate director of forecasting for Dodge Construction Network.

She cited other influences including uncertainty brought on by the recent failures of three banks.

On the flip side, “Institutional planning steadily improved over the month as research and development laboratories and hospital projects steadily entered planning,” Martin said, noting that the index remains above its historical average. “This paints an optimistic landscape for nonresidential construction in mid-2024, as the economy recovers, and the Fed begins to pull back rates.”

There was also steady growth in education and amusement projects. Dodge attributed the hit to commercial planning and sluggish office, hotel and retail activity.

The American Institute of Architects (AIA)/Deltek Architecture Billings Index (ABI) is another indicator for nonresidential construction activity, with a lead time of approximately 9–12 months. May saw a rebound in billings for architecture firms. The May ABI stood at 51.0 (April 48.5), Any score above 50 indicates an increase in firm billings.

“The modest improvement in overall demand for architectural services that we saw last month (May) is encouraging news”, said AIA chief economist Kermit Baker.

“However, there continues to be variation in the performance of firms by regional location and building specialization. This suggests that overall business conditions for the profession likely will continue to be variable,” he said. “High construction costs, extended project schedules, elevated interest rates and growing difficulty in obtaining financing are all weighing on the construction market.”

AIA did find firms are cautiously optimistic for the remainder of the year.

“As the construction market cools, construction costs and schedules are expected to ease, which may make some projects more feasible,” Baker said.

Key ABI highlights for May include regional averages: South (52.3), Midwest (49.6), Northeast (47.5) and West (47.7). A sector index breakdown showed institutional (53.4), mixed practice (52.7), commercial/industrial (47.5) and multifamily residential (43.0). Project inquiries stood at 57.2, and design contracts at 52.3, both up from April.

Sector performance y/y

Nonresidential

Dodge reported that between May 2022 and May 2023, total nonresidential starts were 26% higher. April’s y/y were even stronger at 34%. In May 2023 y/y, manufacturing starts rose 72%, institutional starts improved 22%, and commercial starts gained 12%.

ConstructConnect showed a contraction of 30.1% in total nonresidential building starts y/y (including civil engineering). Within that total were declines in industrial work at 68.9%, a slowing in commercial of 37.0%, an institutional loss of –15.5%.

Chris Kuehl is managing partner at Armada CI, a corporate intelligence firm based in Kansas City, Kan., serving many markets including construction. Kuehl is also the firm’s co-founder and chief economist.

According to Kuehl, the fastest growing sector has been manufacturing, with a 35% increase in activity compared to 2022. This has been driven by a couple of factors, including updates needed as manufacturers expand their use of robotics and automation.

The other driver has been reshoring. 2022 saw a trillion dollars of reshoring activity, and that number is expected to double this year. There will be an expansion in the middle of the country due to access to transportation corridors and a better labor market than in other regions.

Retail and office building development remains in a slump. Many banks are now selling their construction loans at a loss as they want these off their books. Even when the projects are current, they are being sold off as the banks want to sell while there is still some demand. The rapid pace of logistics and warehouse development has slowed, but still remains strong in key areas.

Residential

Year-to-year May 2022-2023, Dodge reported residential starts were 15% lower. Single family was down 26%, while multifamily rose 9% on a rolling 12-month basis. (634,000 annual rate).

Nonbuilding

Dodge reported May 2023 y/y total nonbuilding starts were 25% higher, with strong gains across sectors. Utility/gas plants grew 76%, miscellaneous nonbuilding starts were up 27%. Highway and bridge starts gained 20%, and environmental public works were up 17% on a year-to-date basis.

ConstructConnect’s civil category for May y/y showed a retraction of 2.6%, Within that, power infrastructure fell 22.2%, bridges were down 14.5% but roads grew 3.3%, water and sewage treatment rose 1.9%, and dams/marine work fell 18.9%. Water/sewage was up 1.9%.

Megaprojects ($1 billion or more), though fewer, continued to buoy construction. ConstructConnect reported two April 2023 megaprojects that included an electric vehicle battery plant joint venture in Kokomo, Ind., for Stellantis and Samsung, and a new marine lock in Sault Sainte Marie, Mich., built by the Army Corps of Engineers.

Construction employment gains

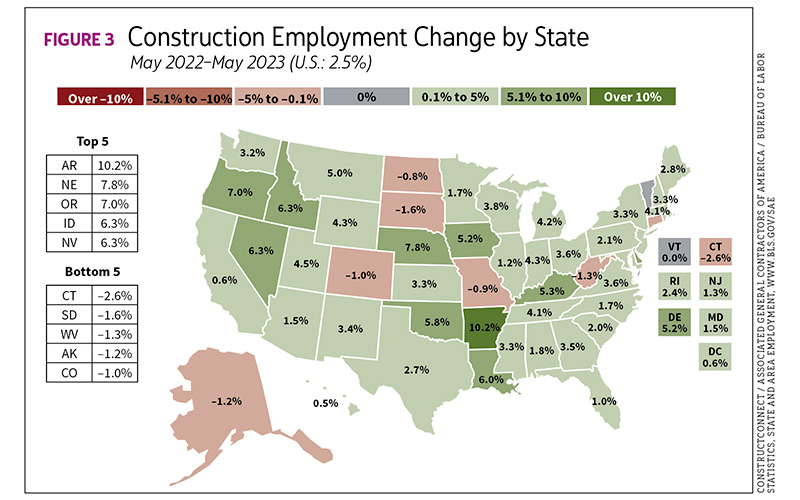

Construction employment increased in 42 states in May from a year earlier, though only 24 states added construction jobs from April to May this year, as reported by the Associated General Contractors of America (AGC), Arlington, Va. In May, another 25,000 jobs were added (May total of construction employment 7.93 million), dropping the unemployment rate to 3.5%. AGC also found firms in nonresidential construction are paying workers a premium 19% more compared to the private-sector production employees.

“Contractors continue to report strong demand for projects and have added employees in all but a handful of states over the past year,” said Ken Simonson, AGC’s chief economist. “The fact that employment dipped in April in half the states may reflect an inability to find qualified workers at a time of record-low construction unemployment not a slowdown in demand.”

Between May 2022 and May 2023, Texas added the most jobs (21,100 jobs/2.7%), followed by New York (12,900 jobs/3.3%), Ohio (8,400 jobs/3.6%), and Oregon (8,000 jobs, 7.0%). Arkansas had the largest percentage increase (5,800 jobs/10.2%), followed by Nebraska (4,400 jobs/7.8%), Oregon and Nevada (6,600 jobs/6.3%), and Idaho (4,100 jobs/6.3%).

In job losses, Colorado led (–1,800/(–1.0%), followed by Connecticut (–1,600/ (–2.6 %) and Missouri ((–1,200 jobs/(–0.9%). (See Figure 3.)

Materials costs still high

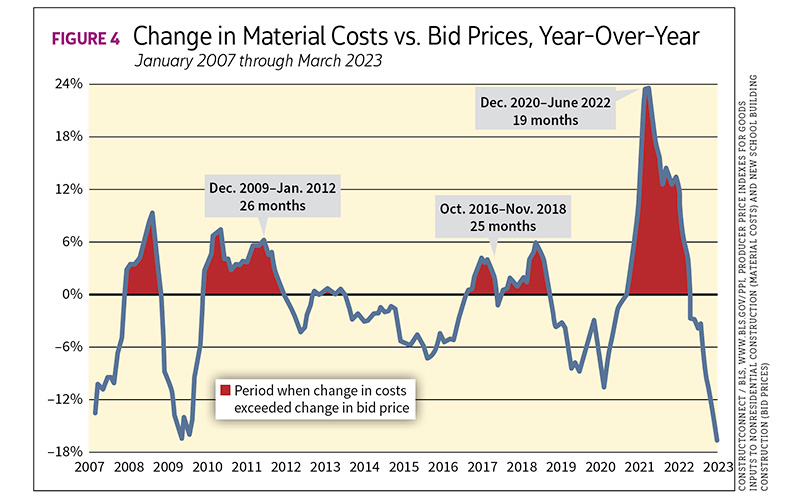

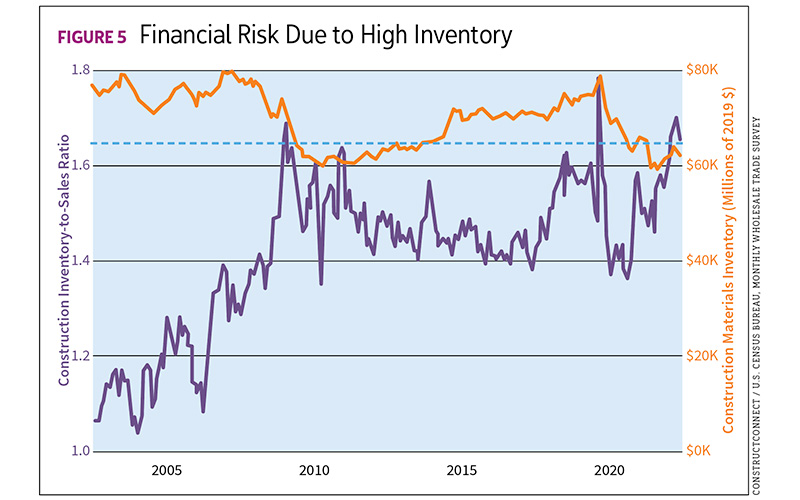

AGC shared in May that the price of materials and services used in nonresidential construction increased 0.5% from March to April, while an index that measures contractors’ bid prices declined 0.3%, an uncomfortable mismatch. In June, however, AGC reported an improvement as the price of materials and services decreased 0.6% from April to May, while an index that measures contractors’ bid prices inched up by 0.1%. (See figures 4 and 5.)

“Prices remain volatile for many key construction materials, making it difficult for contractors to bid on projects that may take years to complete,” Simonson said. “Even some materials that have dropped in price recently have still posted year-over-year increases exceeding 10%.”

Prices jumped 13.7% y/y for cement, 13.3% for electrical switchgear, 13.2% for concrete products and 12.1% for gypsum building products. The construction industry will continue to feel material price pressures.

“As we navigate these uncertain times, construction firms must remain vigilant and adapt to evolving market conditions by closely monitoring their costs and adjusting their pricing strategies to stay competitive,” Simonson said. “Contractors’ bid prices have been virtually flat since January as supply and price shocks from Russia’s attack on Ukraine and the pandemic have faded. But there are still exceptionally long lead times for electrical equipment and renewed or persistent price increases for steel and concrete.”

Encouraging news for residential

The National Association of Homebuilders (NAHB) reported overall housing starts in May increased 21.7% to a seasonally adjusted annual rate of 1.63 million units. Within that number, single-family starts increased 18.5% (997,00 seasonally adjusted annual rate) but remains 6.6% lower than a year ago. Multifamily (apartment buildings and condos) increased 27.1%.

“Mirroring rising builder sentiment, single-family permits and starts increased in May as builders boosted production to meet unmet demand,” said Alicia Huey, NAHB chairman and a custom home builder and developer in Birmingham, Ala.

“Despite elevated interest rates that make the cost of housing more expensive, the lack of existing home inventory in most markets is leading to increased demand for new construction.”

NAHB chief economist Robert Dietz was pleased to see new construction increase in a market where builders struggle to keep up with demand due to a shortage of distribution transformers and labor, but he tempered the positive gains that began in April.

“The May housing starts data and our latest builder confidence survey both point to a bottom forming for single-family residential construction earlier this year. There have been some improvements to the supply-chain. However, due to weakness at the start of the year, single-family housing starts are still down 24% on a year-to-date basis.”.

“There are some major differentiations in residential between regions due to population shifts out of the West Coast, Northeast and upper Midwest,” Kuehl said. “Growth areas have been along the I-35 corridor in the middle of the country and in the upper regions of the Southeast. These are more robust markets for both single- and multifamily housing. Overall, the growth of single-family has been reduced by high home prices and more expensive mortgages. The decline in starts as compared to last year is over 22%. At the same time, there has been a surge in starts for multifamily compared to last year (up 23%). The dominant home buyer is now the millennial, as they have finally started to have families. Gen-Z is still oriented toward rental.”

Some questions for this economy

Kuehl raised three critical questions for the economy as a whole:

- What happens with inflation?

- What happens with interest rates as a result of these inflation expectations?

- What are the prospects for growth the rest of the year (do we continue to avoid a recession)?

“For the last several quarters, there has been an expectation of recession. There was a prediction of 0.04% growth in Q3 of 2022, but we got 2.6%. In the fourth quarter, the prediction was 0.05% and we actually got 2.9%. The first quarter of 2023 was supposed to fall into recession and we got 1.1%—not great, but not recessionary. GDPNow from the Atlanta Fed is predicting 2.1% growth in Q2,” Kuehl said.

“We keep dodging a recession but for how much longer? There is no consensus on what to expect. Weighing on many minds is whether a soft landing of the economy still looks doable. It depends on which economist you ask,” Kuehl surmised. “Recently, the World Economic Forum asked over a hundred economists whether they anticipated a recession in 2023. Forty-five percent said one was near certain and that it would likely last the year, and 45% asserted that there would be no more than a mild slowdown that would likely dissipate by the fourth quarter. Apparently, the remaining 10% didn’t understand the question.

“It all seems to come down to Fed policy, unemployment numbers and consumer confidence. If the Fed decides to resume hiking rates, the odds of a recession increase, but only if these moves start to impact employment—and so far, they have not. The latest data on retail shows continued consumer activity even as the confidence surveys suggest people are more worried than they were six months ago. The longer the economy continues to exhibit growth, the less likely there is a stumble into recession in the next couple of quarters,” he said.

In response to bumps we could see in the rollout of the federal Infrastructure Investment and Jobs Act and CHIPS and Science Act, Kuehl said, “The money that has been promised and allocated could exceed the level of spending impact of the interstate highway activity in the 1950s. The challenge is getting it spent in an appropriate and timely manner. There are all the usual government hoops and studies required, and there is a further requirement as far as state and local engagement. There will be demands for matching funds and local permissions. Of course, the actual distribution of project money will depend on local political clout.”

Kuehl shared that the more conservative states are emphasizing traditional infrastructure, while the more liberal states are focusing on individual relief for those affected by inflation and other economic pressures. Conservative states have also moved away from alternative-energy projects in favor of more traditional power projects.

As to elevated materials costs, “producer price indices (PPI) are still high and rising, although there are some factors that have started to shift,” Kuehl said. “Logistics costs are down as the capacity issue in trucking has eased. Commodity prices have started to stabilize a little, but there is considerable political volatility in copper. Aluminum is settling a bit. The impact of a given PPI depends a lot on the contractor, their sources and projects. The supply chain is better, but not fully back to old patterns—especially material from China. There is an understanding [among clients and the building construction community] regarding higher bid prices, but the reality is that projects have become too expensive and are getting delayed and even canceled. The trend has been to delay rather than abandon.”

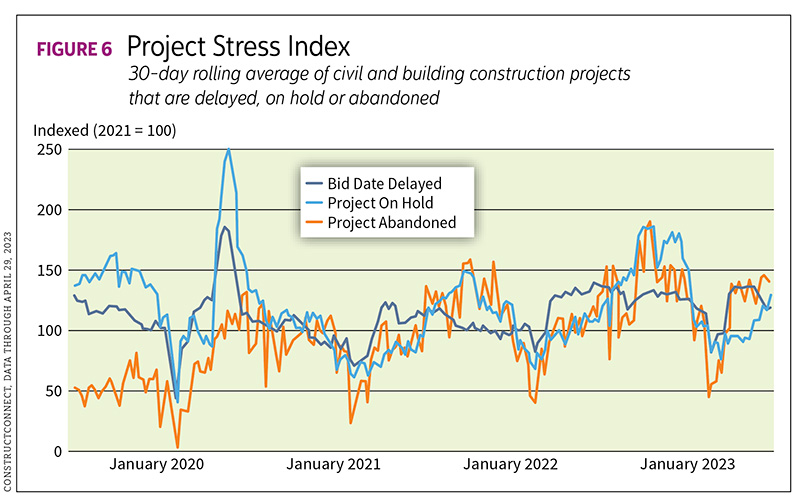

A resilient economy

ConstructConnect’s Project Stress Index tracks changes in the level of projects that are delayed, placed on hold or abandoned, based on weekly construction activity data. (See Figure 6.) In a mid-June report, project stress levels decreased 15.2% y/y. Within that was a sizable decline in abandoned projects of –21.0% y/y. Delayed projects fell 9.8% y/y. Projects on hold stood at –14.5%

The construction industry, while challenged, is holding its own in 2023. While it may require contractors to carefully balance multiple factors, this is a resilient economy that steams ahead no matter what’s thrown at it.

Header image: shutterstock / IMG_191

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].