You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

Contractors spend their adult life building businesses that usually hold more than 70 percent of their hard-earned wealth. Unlocking that trapped wealth without being clobbered by taxes will be a key to your retirement and not outliving your money.

Common misconceptions exist in successful business owners' understanding of the complex business exit. If you do not understand the following facts and myths, you are probably putting your business wealth at risk.

You don’t want to find yourself in the red zone of your business career only to fumble the ball before reaching the end zone. More than 70 percent of private businesses fail to transfer to the second generation or to an outside buyer. The odds do not improve as businesses enter the third, fourth and future generations.

“I will just sell my business and retire.”

This may sound like a good solution, but fewer than 20 percent of the businesses for sale actually close. Due to the characteristics of the construction industry, the closing rate when dealing with an outside seller becomes even more distant. And those that do sell to an outside party typically succeed when the company operates in a unique niche or location or when the economy is moving out of the periodical recessions and growing.

Most transactions in the construction industry are not outside sales; they are internal, and the majority of transfers are management buyouts with a small percentage of employee stock ownership programs (ESOPs) and some form of gifting. These internal exit paths require a long-term plan and a succession process to replace the owner with a strong management team.

“I will deal with my exit plan in five years.”

I will often talk to a business owner about when they intend to retire, and the answer is usually predictable: “In five years.” Three years later, the answer is still the same. In most cases, this means the owner has no plan and has not prepared for this complex process, and the procrastinating likely will continue.

The real problem is the lack of a written plan to direct the owner on a measured path that is in tune with their personal and business goals. Even though the actual exit may take an additional 5, 10 or 15 years to execute, having a strategy and direction is a critical component toward meeting an owner’s post-exit financial goals. Furthermore, it takes time and training to align, grow, stretch and replace the owner with a formal succession process.

The truth is most owners have not saved enough for retirement. They need time to aggressively save while they are in control of the company and have a 10–15 year window. The good news is there are attractive plans/strategies/packages that are very tax efficient and can be leveraged by the business owner. Some can even be deducted by the company and then tax deferred and withdrawn through capital gains instead of income.

“I can probably do this myself.”

It’s likely you know how to run your business, but have you ever exited a business? In a study, the Family Firm Institute found that 70 percent of businesses fail to transfer to the second generation, and 90 percent of businesses fail to transfer to the third generation. In other words, your grandson has about a 3 percent chance of running the business you hope to transfer to your son or daughter.

As a business owner, you have already had conversations with your accountant, lawyer, insurance agent and many other professionals. The information is probably scattered, meaning it is not comprehensive, cohesive or holistic. An exit plan pulls all of your personal, business and financial goals together and unlocks the trapped business wealth in the most efficient manner.

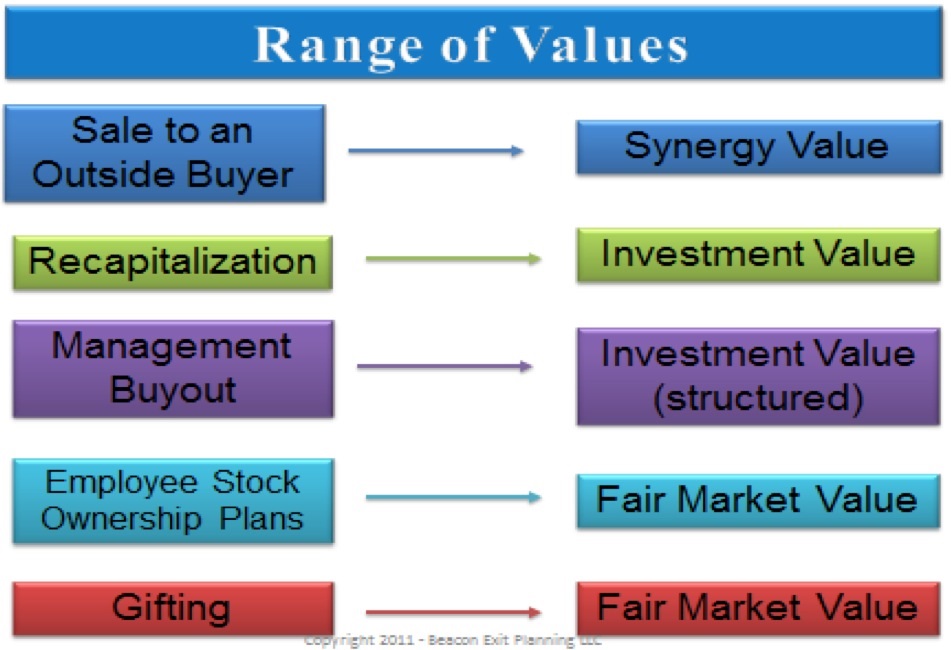

“My business is worth $7 million.”

Your business can have different values depending on whom you are selling to. This is called a “range of values" (see image) You should understand the value of your business based on the exit strategy you are trying to employ.

The reality is that most owners overvalue their business and have a false impression of its actual worth. Even though they have spent the last 30 years working 60 hours per week, they haven't created value.

It is critical to understand what makes your business most valuable to an acquiring party. Advisors accredited in business appraisals are trained in these situations and should be engaged to provide you with guidance on increasing business value. There may be instances where reducing value becomes more important as a tax strategy.

Here again, a comprehensive strategy is required to meet your needs. Remember that taxes, fees and a poor exit plan could reduce that harvest by 20–60 percent.

“But that will never happen to me.”

I get a call once a month regarding an owner’s untimely death or disability. In most cases, many of the buy/sell agreements are not aligned with the business owner’s motives or goals. Often, they are unfunded or established in a manner that makes taxable what should have been a non-taxable benefit. Many recent horror stories have seen the owner go to court for several years, costing both parties hundreds of thousands of dollars in legal fees with no clear end in sight.

Two months ago, a buy/sell was structured in a way that unintentionally created income tax for a business owner’s widow. In another case, a widow with no experience in the business was demanding her husband’s office, position and salary. In yet another situation, an agreement provided for a fixed amount to be paid out as a means of repurchasing the deceased owner’s interest. This agreement was created at the business’ inception, but several years later, the business' value had grown exponentially. Imagine the disputes that would have ensued. Clearly, these are unintended consequences of an outdated or poorly drafted agreement.

“If I could get $4 million, I would retire tomorrow.”

Even though you probably have more than 70 percent of your wealth trapped in your business, the real question is how much you will need to replace your income. You have to consider your money outside the business, including your savings, retirement funds, real estate income, investments, etc. The bottom line is you have to understand the process of how to replace your income so you don’t outlive your money.

Because so much is dependent on your exit, the process should coordinate three major areas of your life: business, personal and financial planning. When properly coordinated, the outcome should be a comprehensive plan that will not only satisfy your financial needs post-exit but will also support your other goals, such as legacy planning and wealth protection.

“But my accountant does exit planning.”

You probably have a good accountant and a book value for your company, but it takes a proactive approach and a significant amount of other information to successfully exit your business. The focus of your exit should be based on your business, personal and financial goals and not your advisor's goals.

My past company’s team of owners invested six years and more than $250,000 for fragmented advice as we wandered down the exit path with two offers from industry roll-ups and two offers from boutique private equity firms that wanted to invest in our company. Additionally, we investigated an ESOP and used a management buyout to transfer the stock of three existing owners to five new owners. We received reactive advice from our advisory team but were still lost and had no direction. The need to run a 200-employee company with three different owners and three different goals further complicated this issue.

Exit planners are trained as process consultants with the task of moving an owner’s goal into a matching path that meets the owner’s financial target, replaces the owner, and protects his or her wealth with a comprehensive result. Exit planners juggle the owner’s goal and scattered business, personal and financial information to arrive at one document that pieces the puzzle together and directs the owner and his advisors down a path that leads toward a desired outcome.

Exit planning is the orchestration of many disciplines coordinated in one comprehensive report. That report defines all the options, determines the best fit for your goals, and navigates a path out of the business. This combined information will give you the best overall result once the exit is complete.

After the exit plan is delivered, the next stage is a separate execution phase. An exit planner can also quarterback and coordinate different disciplines and professional advisers, including attorneys, accountants, estate planners, insurance advisers, financial planners, business consultants and others involved in the execution of the exit plan.

The good news of all this is there is a systematic, proven process that can guide you toward your ultimate exit goals. The process can take as little as three to six months or up to two years in some instances. The key is to start planning today.

For more information, visit www.BeaconExitPlanning.com.

About The Author

Kevin Kennedy is the founder and CEO of Beacon Exit Planning, LLC ("America's Exit Planner"), and a managing partner in Beacon Merger & Acquisitions Advisors, LLC. He is a nationally recognized speaker, author and a thought leader on exit planning and succession for private businesses. He personally walked the exit path and understands firsthand the challenges an owner faces from buying and selling a specialty contracting company and helping to implement succession planning to the fourth-generation owners. Beacon delivers owner-centric advice to business owners, once only available to the very affluent. For more information visit www.BeaconExitPlanning.com or email [email protected].