“Blurry” and “static” are good descriptors for 2019, when economic challenges were boisterously discussed. Trade tensions, Mother Nature’s wrath and turbulent politics tested growth and will continue to hover over the longest expansion in U.S. history—10 years now and counting.

Economic cycles end, but a recession isn’t expected this year. What you can anticipate in 2020 is a slowdown that will affect the construction industry. An accurate read of an economy shaded with nuance, ambiguity and contradiction will require 20/20 vision. Put on your glasses.

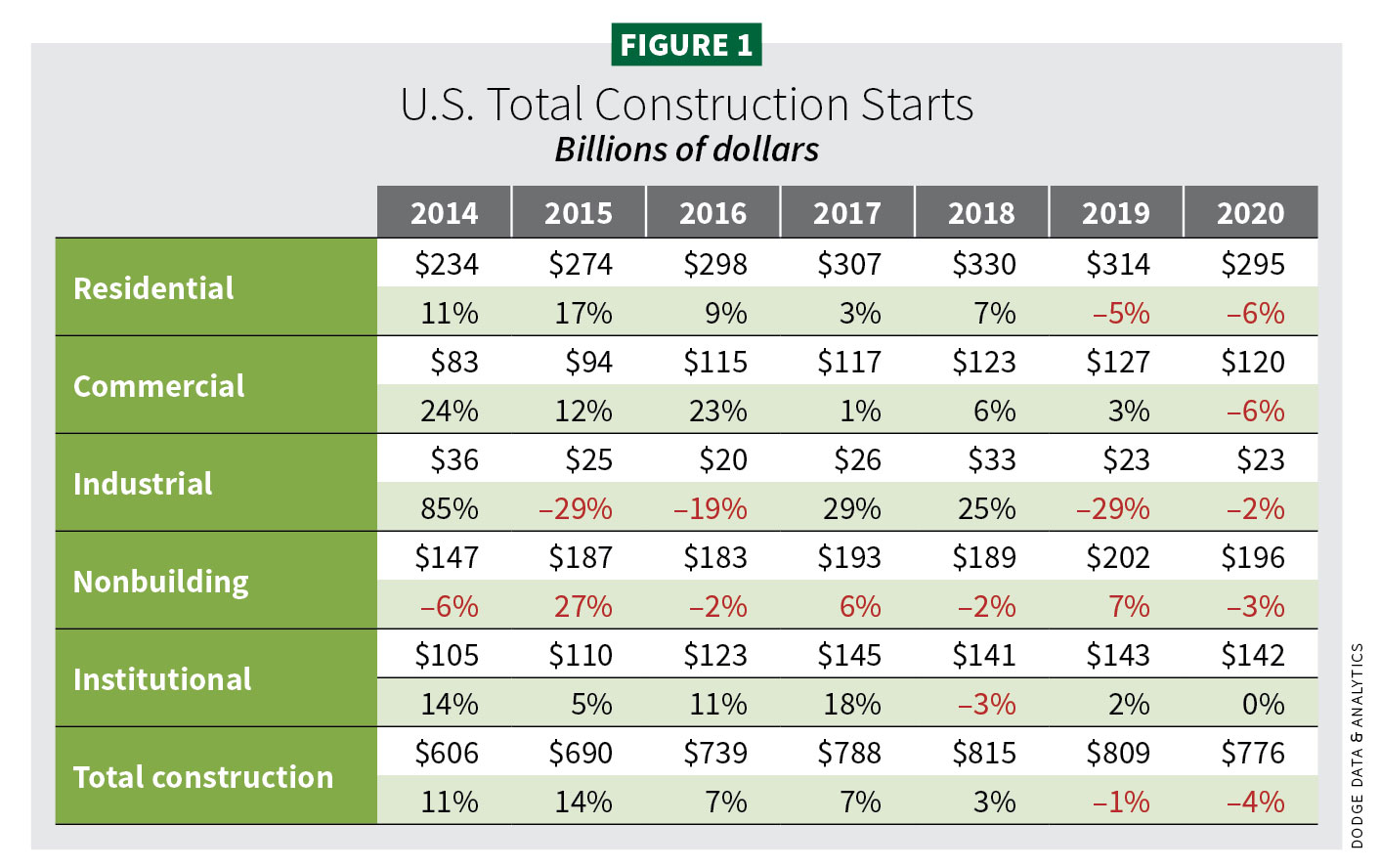

Dodge Data & Analytics reports that total construction activity in 2019 fell 1% ($809 billion), a marginally different result from the flat growth economists forecast last year. Projections for 2020 show a reduction of 4% ($776 billion) (see Figure 1).

Economists from ConstructConnect saw 2019 starts fall 1.6% but predict a small gain of 0.8% this year. For perspective, even Dodge’s pullback projections represent solid performance seen in recent years. The Associated General Contractors of America

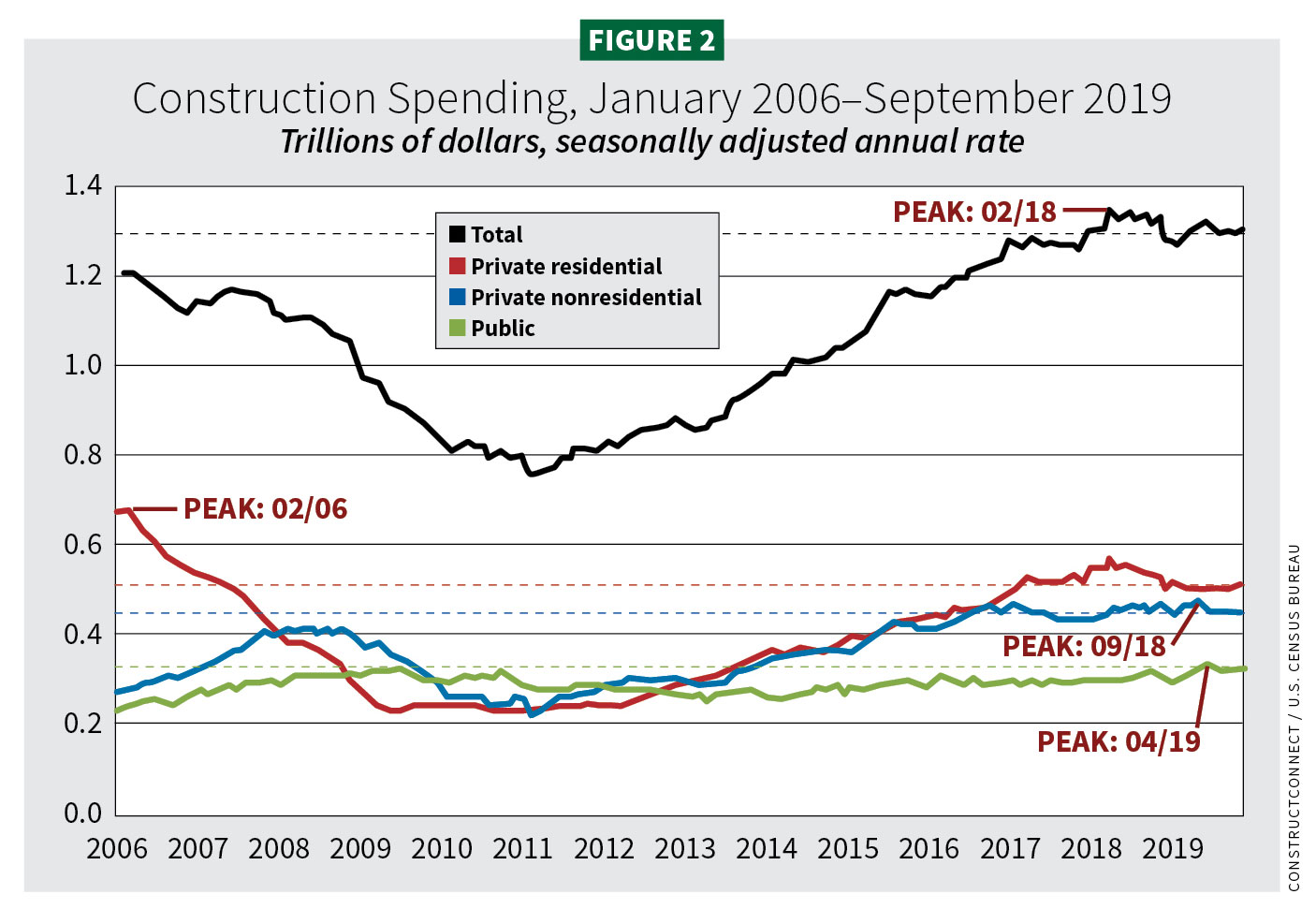

(AGC) projected 2020 put-in-place (PIP) capital spending from flat to 4–5% growth (AGC/U.S. Census Bureau). PIP numbers—a measure of the actual work being done—almost always come in higher than starts (see Figure 2).

Richard Branch, chief economist of Dodge Data & Analytics, said that, although the recovery in construction starts that began in 2010 is coming to an end, 2020 will not see a repeat what the industry experienced during the Great Recession (approximately December 2007 to June 2009).

“Economic growth is slowing but is not anticipated to contract [in 2020]. Construction starts, therefore, will decline, but the level of activity will remain close to recent highs. By major construction sector, the dollar value of starts for residential buildings will be down 6%, while starts for nonresidential buildings and nonbuilding construction will drop 3%” (see Figures 1 and 3).

The 2020 Dodge Construction Outlook was presented at the 81st annual Outlook Executive Conference held by Dodge Data & Analytics in Chicago on Oct. 31, 2019. ConstructConnect brought together its own chief economists along with others from the American Institute of Architects (AIA) and AGC in a webinar, “CAUTION: Uncertainty and Disruptors Ahead” on Nov. 8, 2019.

Looking broadly, 2019 brought some slowing in some sectors and levels of growth in others. We should be in for more of the same in 2020.

Construction in general

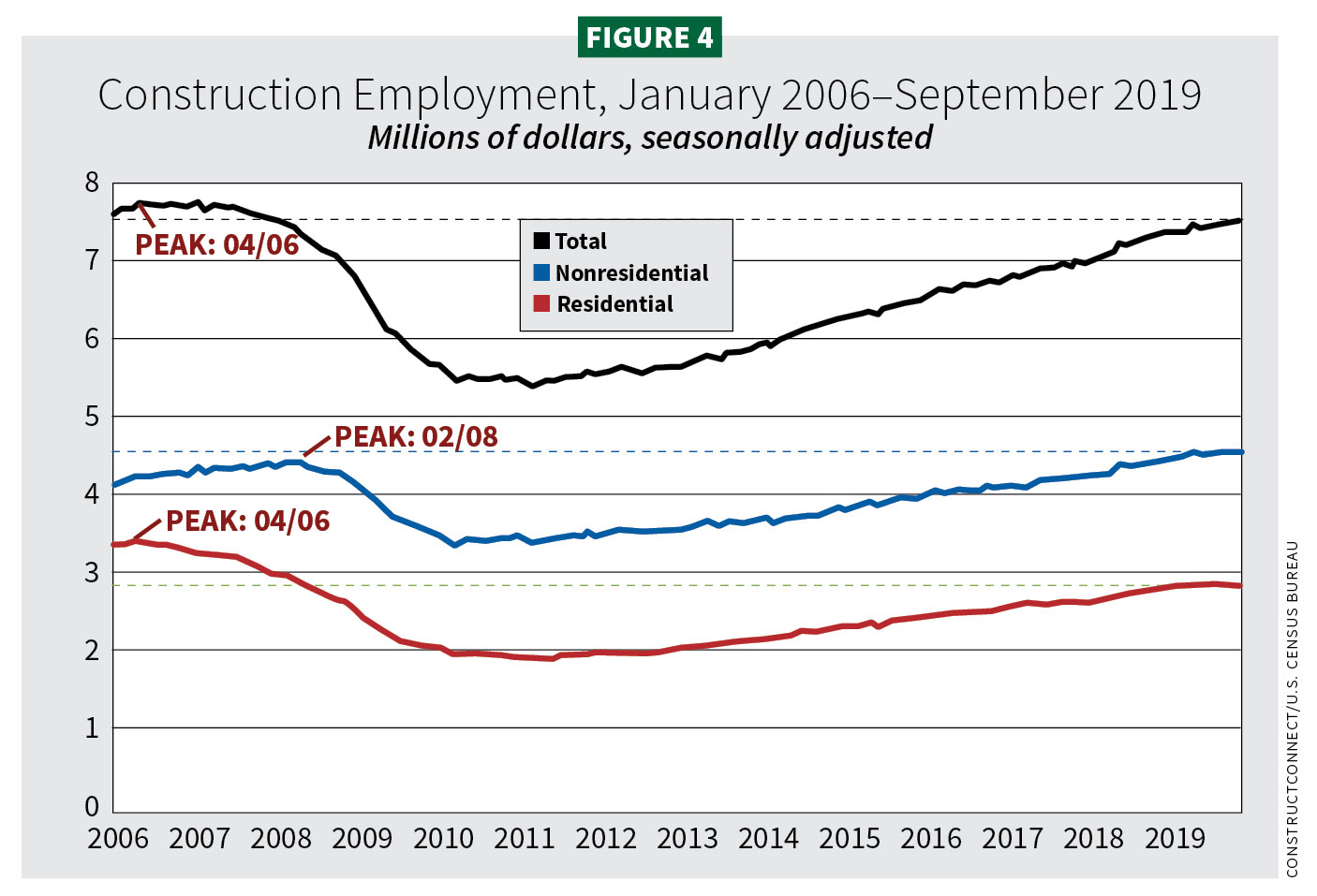

“I don’t think the economy is teetering on recession,” said Ken Simonson, AGC chief economist. “It may slow but construction is still quite positive and adding jobs at a higher rate than the rest of the economy. Job openings in construction are at record levels and have been for the past 16 months, though some slowing is starting to show. Overall, the market is still quite favorable for construction” (see Figure 4).

Simonson said PIP spending, the total dollar value of construction work, peaked in February 2018 (see Figure 2). Last year, numbers represented a 3% decline from that peak. Looking year over year (September 2018–2019), overall residential spending was down 4 to 6%. Single-family construction did enjoy -double-digit spending growth in the first half of 2019, followed by a midyear slump.

Builder confidence, however, remains high for newly built single-family homes, according to the National Association of Home Builders/Wells Fargo Housing Market Index. Interestingly, Zillow, the popular online aggregator of real estate pricing and market, sees a recessionary period for housing this year based on a poll of 100 real estate experts and economists. Dodge and ConstructConnect starts, however, are not poised at recessionary levels.

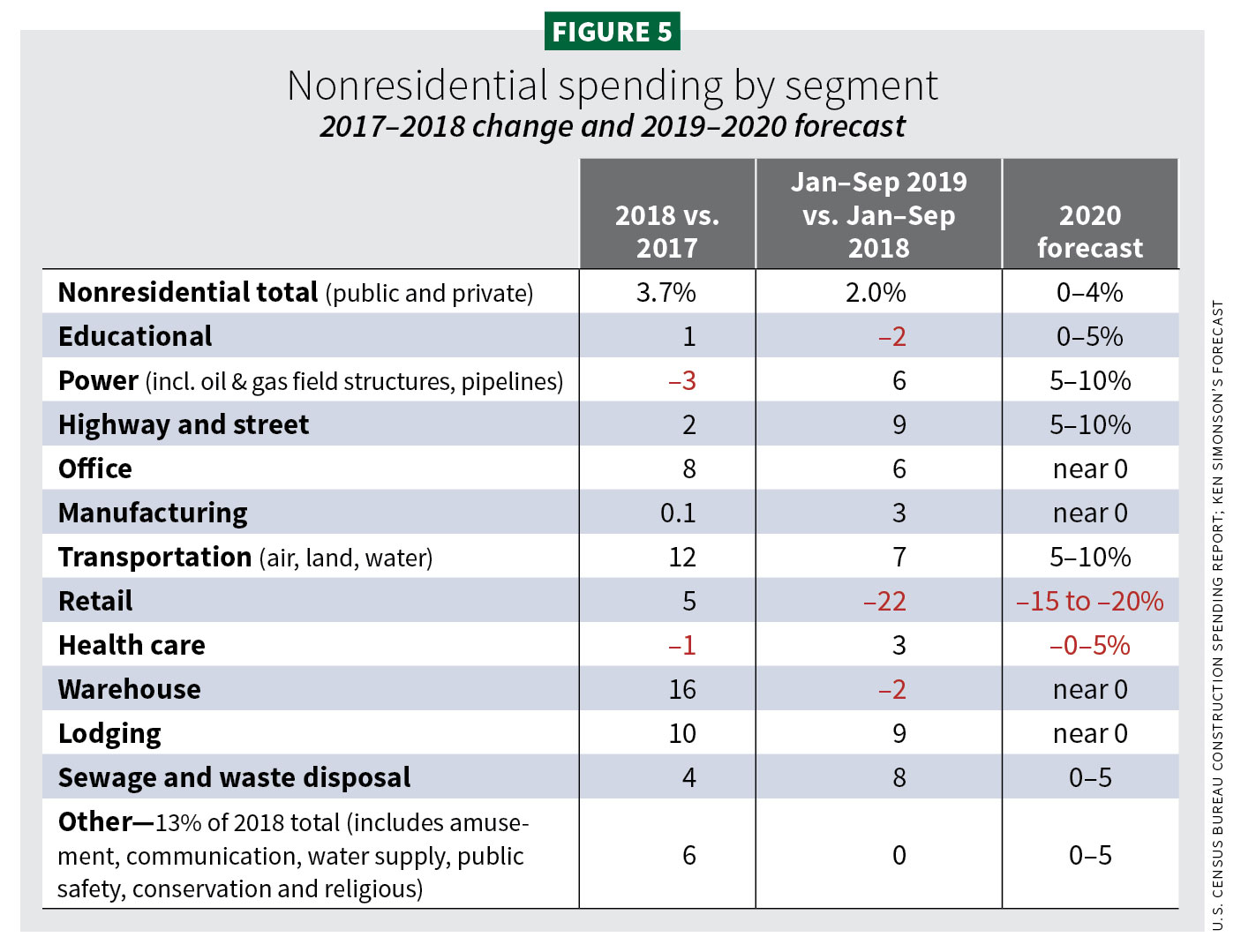

Addressing other sectors, Simonson reported nonresidential PIP spending was off 5.7%, landing at 2% growth. Within that, public construction performed strongly, gaining 6.6%.

Looking to this year, Simonson expects a breakthrough for single-family PIP spending, achieving a possible 5–10% gain, thanks to lower interest rates, continuing job growth and record stock market performance giving confidence to homebuyers. Multifamily could maintain between 0–5% PIP growth, partly through rental and condo construction .

Simonson projects overall 0–4% PIP spending growth for nonresidential: public construction (0–5%) due to activity in pipeline construction and on- and offshore wind energy construction; street and highway construction (5–10%); and supportive work from transit projects, including commuter/high-speed rail (particularly airport projects) and some port activity (see Figure 5).

Kermit Baker, chief economist, AIA, shared 2019 Architecture Billing Index (ABI) statistics showing what construction (nonresidential) might look like this year. Late last year, architecture firms reported a 6.5-month project backlog.

“Firms in general found 2019 to be disappointing (flat or some growth). We are seeing a slowdown in design activity,” he said.

The ABI score in September 2019 was 49.7. Any score below 50 indicates a decrease in billings. In December, the ABI rose to 51.9%.

“All major sectors are slowing. Multifamily saw slight declines in 2019, pretty much the same in commercial/residential activity. Institutional showed a bit of a decline, too. Over half of firms reported uncertain construction costs or concern about the economy affecting current projects in 2019,” Baker said.

ABI scores regionally showed the South with the highest ABI of 51.1 (compared to 53.5 in 2018), followed by the West at 50.2 (51.5), the Midwest at 49.0 (53.1), and the Northeast at 47.3 (49.9).

The U.S. economic picture

Cristian deRitis, Moody’s Analytics deputy chief economist, presented at the 2020 Dodge Outlook Executive Conference. His view of 2020 is “cautiously optimistic.”

“We’re coming off a historic expansion,” he said. “A lot of things are going right but there are an awful lot of risks.”

Pointing to things “going right,” deRitis highlighted overall healthy household wealth, citing Federal Reserve stats that show $16.4 trillion (+4.7%) in disposable income year over year, $107 trillion net worth and a lower outstanding debt ($15.2 trillion). Consumer sales grew 4%.

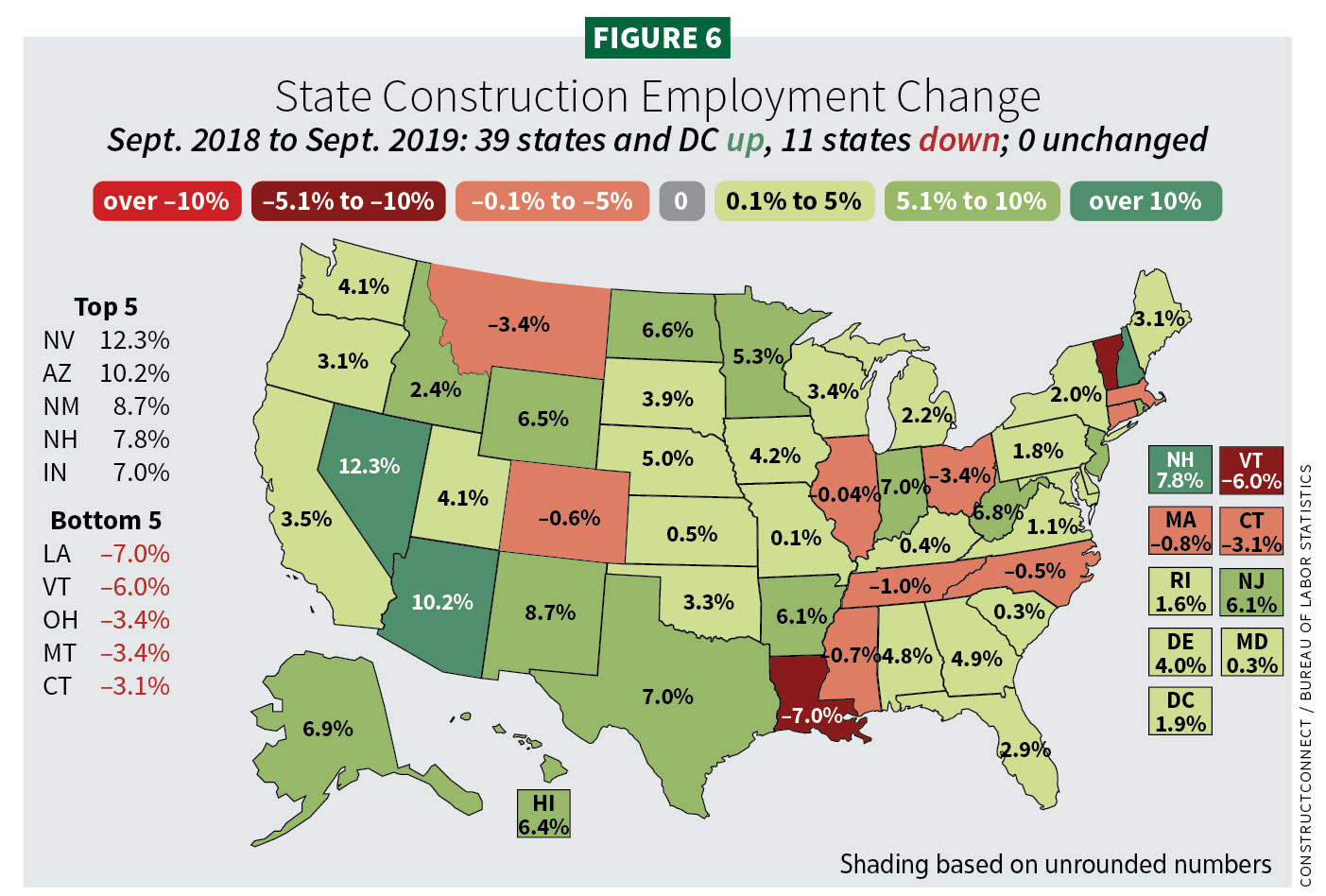

DeRitis viewed the job market as “pretty good” but slowing. Unemployment as of November 2019 stood at 3.5%, according to the U.S. Bureau of Labor Statistics. For construction-specific data, see Figure 6.

Wages and salaries rose 2.9% year over year. Jobs added in October 2019 stood at 128,000, surpassing an expected 85,000.

Meanwhile, gross domestic product (GDP) reached 3.1% in the first quarter but was expected to settle close to 2.1% by the fourth quarter. Dodge attributed much of the first quarter performance to “a boost from inventory accumulation as firms ordered more goods to use in the future, possibly fueled by fears of imminent tariffs.”

“The GDP target nowadays is 3% or higher, it seems,” added Alex Carrick, chief economist, ConstructConnect. “In the past 19 years, we hit 2.9% and higher on seven occasions. Consumer spending is now 70% of GDP. So, it is imperative that consumers be happy and confident.”

Last summer, a temporary inverted yield curve made a lot of noise in economic circles. When short-term rates shoot up over longer terms, the curve inverts. An inversion is considered a signifier of a coming recession.

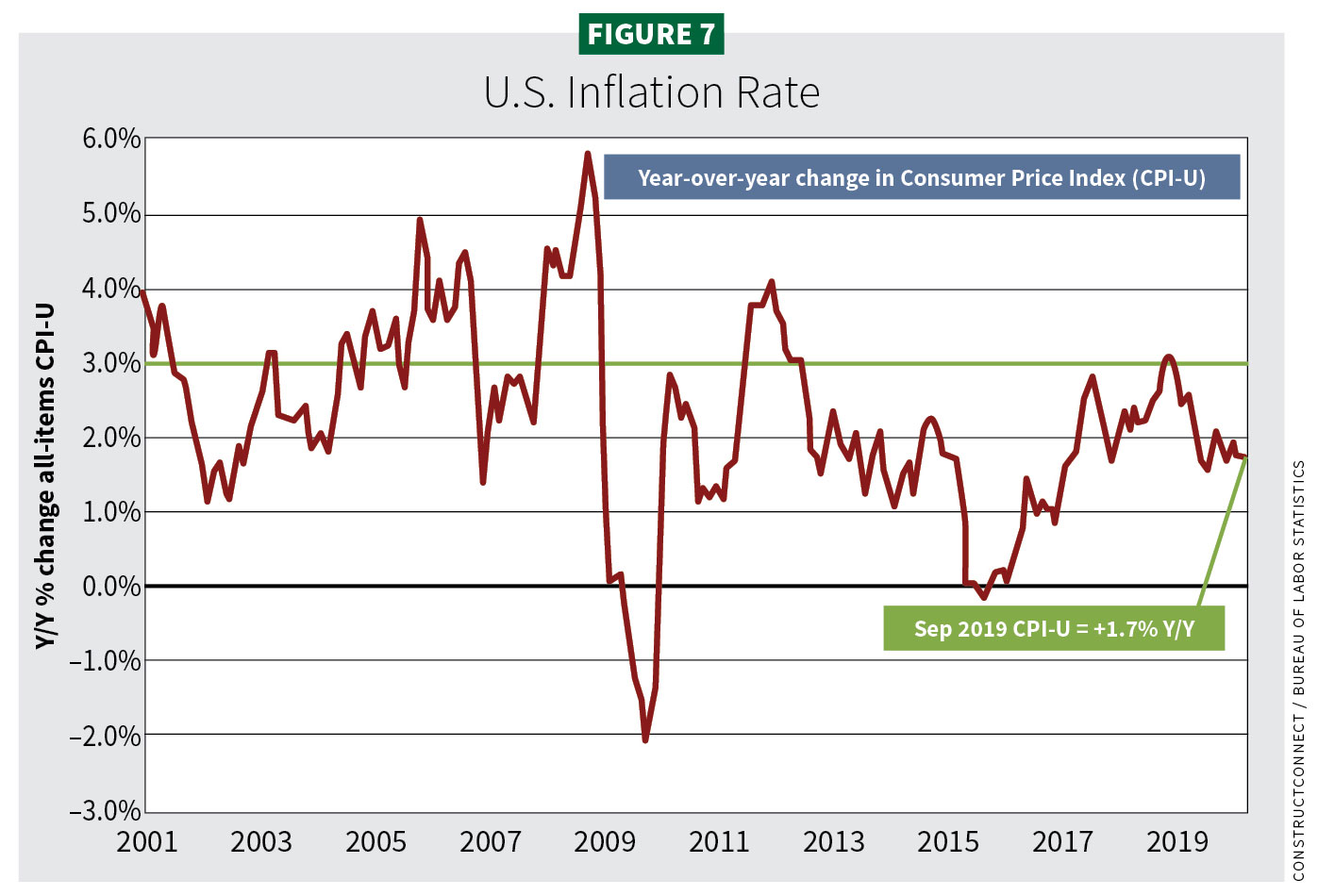

“It freaked out a lot of people, so the Fed lowered interest rates,” Carrick said. “The inversion was short-lived, and I think somewhat inadvertent. Inflation has not been a problem, but the rates lowered anyway. Inflation is low due to commodity prices being low [metals, gas, agriculture products and oil and gas]. They are the building blocks of everything” (see Figure 7).

In other positives, interest rates remained low. The Fed lowered its rate by 0.25 basis points in July 2019 and again in September, after raising interest rates nine times between 2015–2018. Arguments have arisen over whether the Fed should have employed this action during the relative health of the economy. DeRitis said time will tell.

The Fed held rates in December and predicted no lowering would occur in 2020.

Federal funding also played a role in feeding the economy. Congress agreed to $19.1 billion disaster relief in July 2019. The debt ceiling was increased through July 2021. A two-year budget deal increased defense and nondefense spending by $320 billion. Though appropriation bills (unfunded at this writing) will determine dollar allocations, the Department of Transportation, the Army Corps of Engineers and others could see slightly higher funding for 2020.

In November 2019, Transportation Secretary Elaine Chao announced BUILD (Better Utilizing Investments to Leverage Development) grants for infrastructure projects. Totaling $900 million, the grants were awarded to 55 urban and rural projects in 35 states that included bridges, highways, ports and other transportation.

Finally, deRitis shared a perplexing phenomenon: Consumer confidence dropped in the early half of 2019, then rebounded the rest of the year, while real spending softened. Nonetheless, “Consumers are telling us they are enthusiastic about the economy,” he said.

Risks to the economy

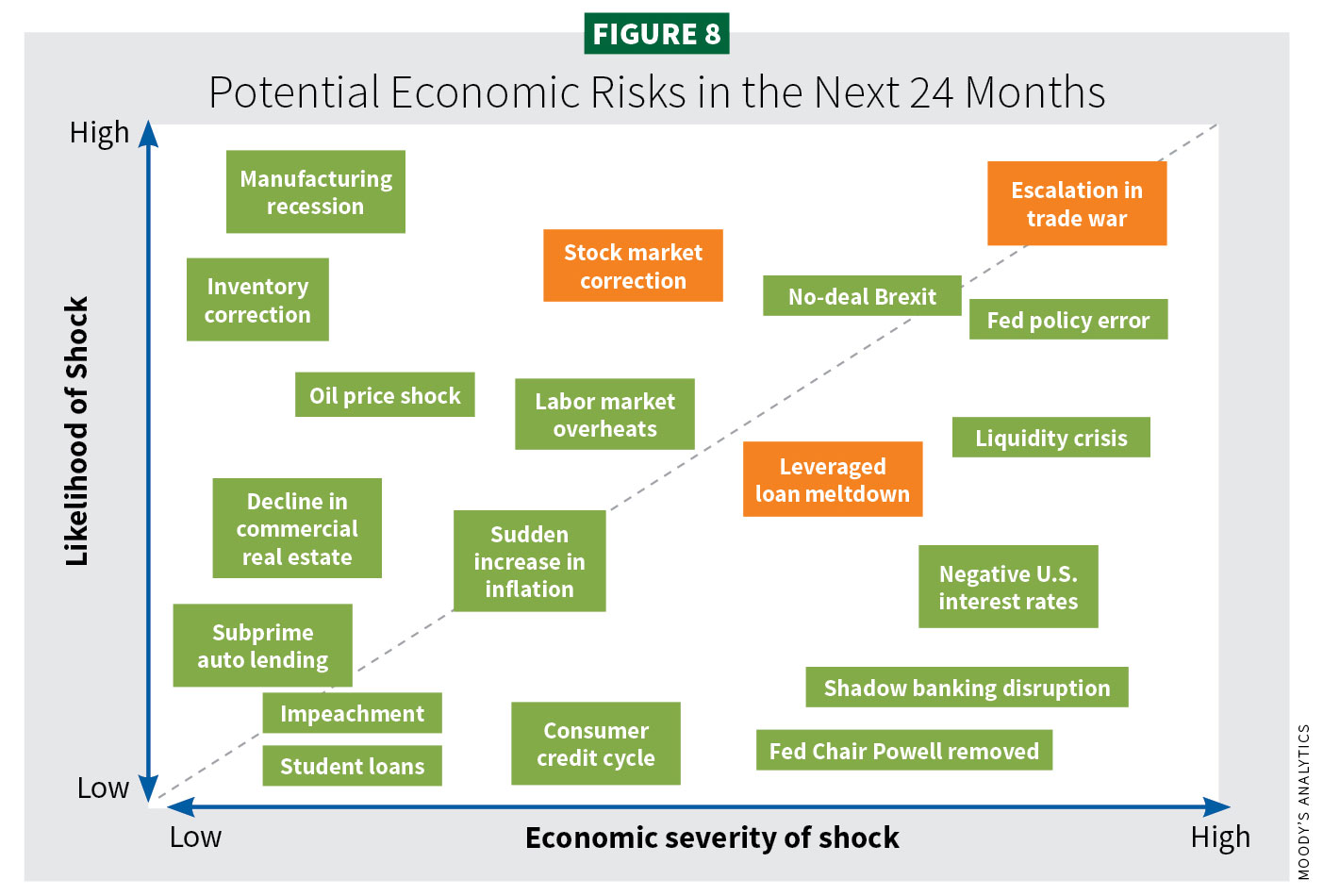

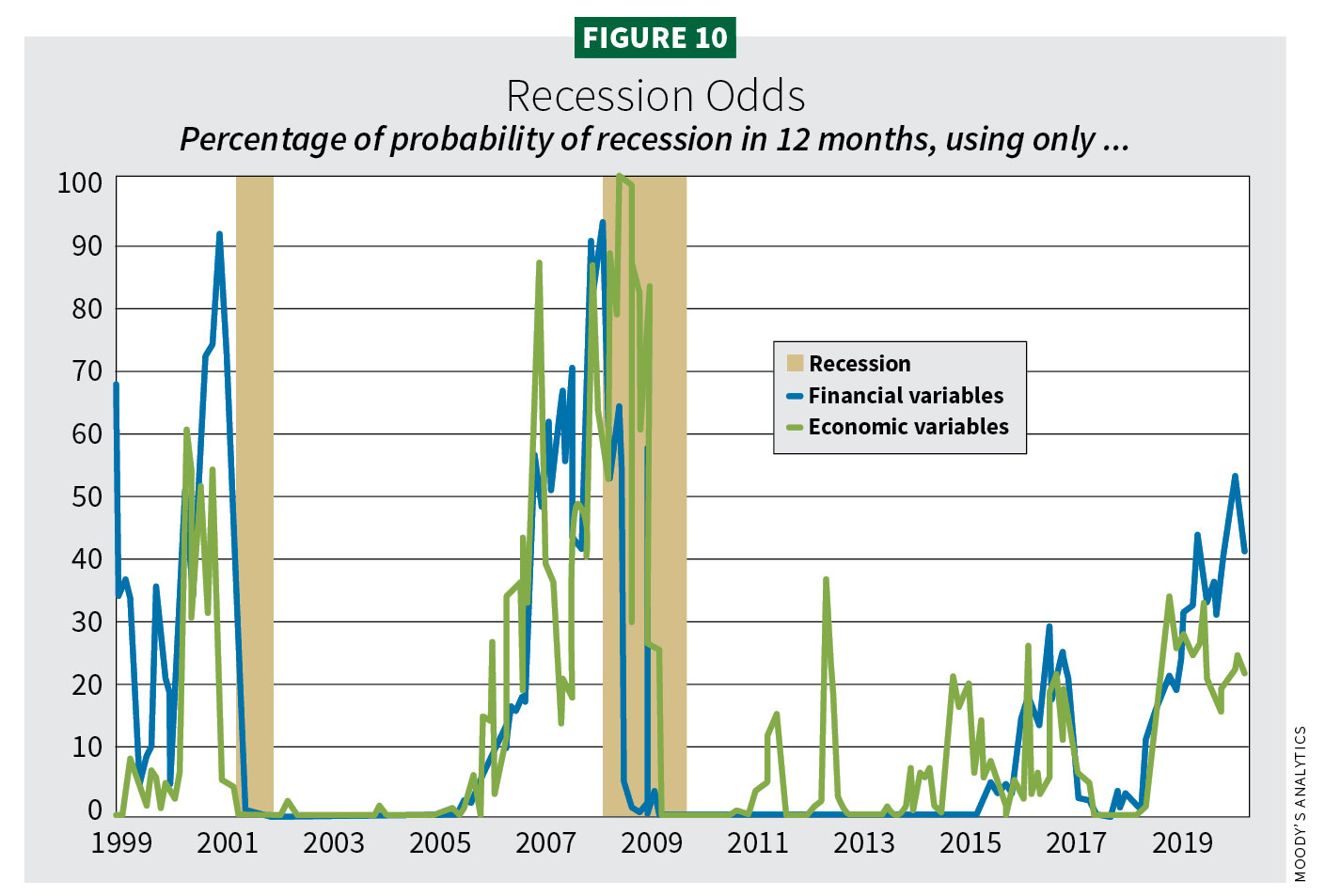

DeRitis and others see several warnings on the economic horizon. Carrick of ConstructConnect said, “I don’t know if I’ve ever found so many caution flags as I do for 2020.” (see Figure 8).

Externals appear to be the biggest stressors due to trade disputes and a slowing global economy, particularly the trade war with China. An interim deal was still pending in December. If it falls through, a 15% duty on goods from China (roughly $111 billion) would remain with a potential 5-point increase (25-30%) on $250 billion worth of goods. A 15% levy on another $150 billion worth of goods could be added. To date, China has retaliated with $75 billion in tariffs on U.S. goods. If tariffs remain, Dodge sees a “dampening” of GDP with growth shrinking to 0.5–1.0%.

Dodge expects economic momentum to wane in 2020 “as negative influences on the economy begin to overwhelm the positive, slowing growth,” Branch said.

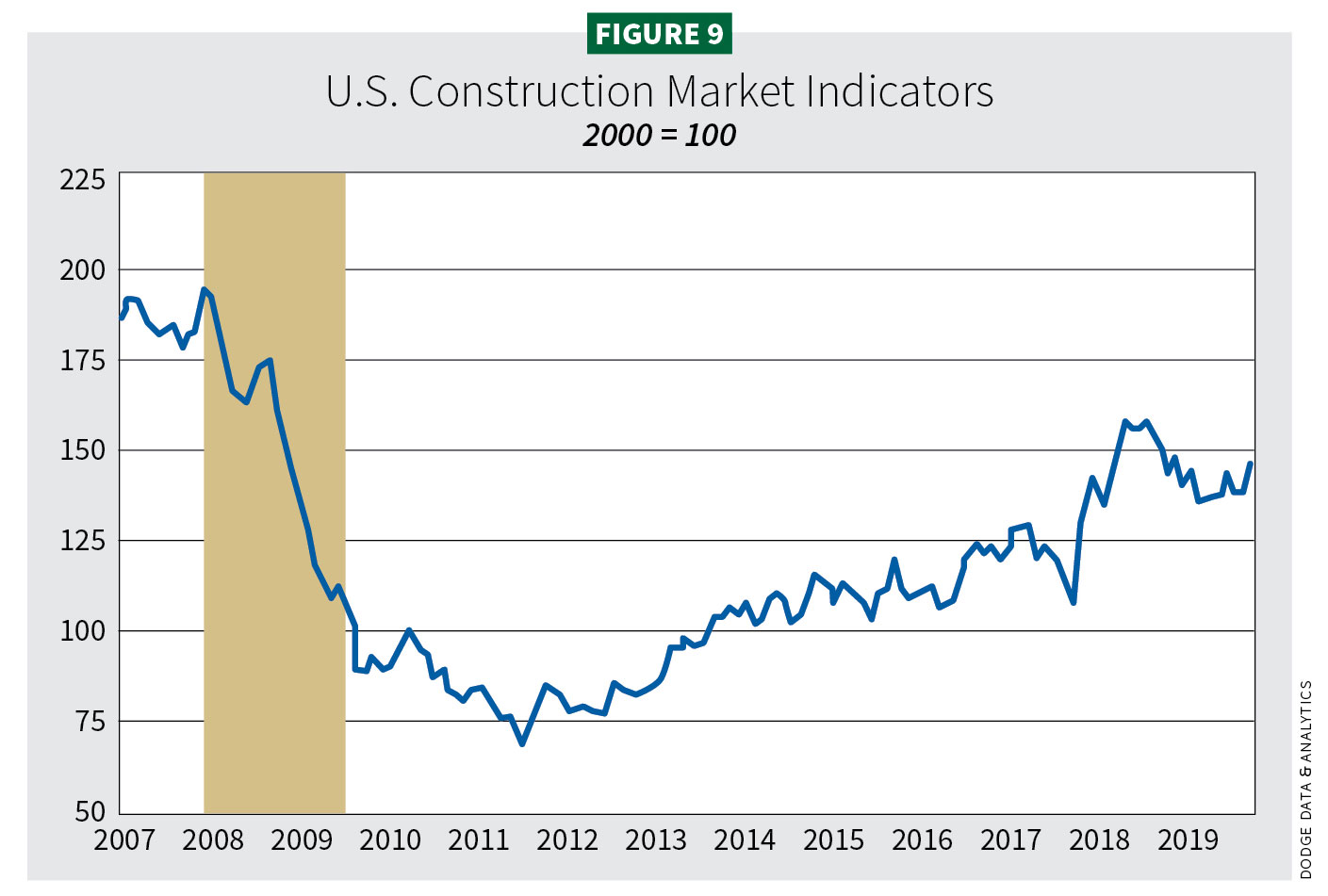

Figure 9 tracks the initial report for nonresidential projects in the planning stages, which has trended lower since fall 2018.

Branch and deRitis agree that sentiment and uncertainty, i.e., consumer confidence, will challenge the next 12 months.

“If consumer confidence is affected, we may have a problem,” deRitis said. “Next tariffs may be more consumer-related. Hopefully, we strike a deal, maybe in phases. We need to address this trade issue sooner than later.”

China aside, in October 2019, the United States approved tariffs against the World Trade Organization on certain goods, including 10% on airplanes and 25% on foodstuffs and single-malt scotch whiskey. Related to construction, the tariff would also apply to certain European-made hand and pneumatic tools and self-propelled backhoes. Meanwhile, the House of Representatives has approved the United States--Mexico-Canada (USMCA) deal. The Senate vote was pending at the time of this writing. Meanwhile, NAFTA remains in place.

“Have tariffs improved the U.S. trade deficit? Not in the least,” Carrick said.

The weakness in U.S. manufacturing may also build to a larger negative for the economy, Dodge reports. Other possible threats to U.S. economic health in 2020 are a growth slowdown in Canada and in Eurozone industrial output.

Carrick identified additional caution flags, including decelerating job growth. For its part, Branch projects employment growth to half in 2020, signaling a pullback by employers.

Also, “the stock market is increasingly having real-world impacts,” Carrick said. “Worldwide economic performance can impact its numbers. Consumer confidence can also be affected, based on pension plans and mutual fund performance. It’s true stock markets have increased remarkably with NASDAQ up 500% and Standard & Poor’s up 300%. But these indices reached their peak a couple years ago. The stock market has been moving sideways over the last 1.5 to 2 years.”

Carrick’s other caution flags include the size of the U.S. national debt: $23 trillion. Federal Reserve Chairman Jerome Powell warned lawmakers in November that the ballooning federal debt could hamper Congress’ ability to support the economy in a downturn.

“Are we going to have a recession?” is the question economists get asked most. “It depends” is their honest response.

“There is no need to panic; things are not falling apart,” deRitis said. “A recession is highly unlikely in the next 12 months.”

Carrick, Simonson and Baker agree. A trade agreement with China and older millennials ready to become homebuyers are two potentialities that could keep economic growth going (see Figures 8 and 10).

“Looking back as far as 1994, then moving forward, fundamentals suggest the next recession won’t be severe,” deRitis said. “We modeled likely severity. Given the current fundamentals, [a recession] would likely be the shortest, least severe recession on record. I would expect a duration lasting maybe three to four consecutive quarters.

The wildcard is whether fundamentals are the only driver. Changes in fiscal policy could be a spoiler. A world of negative rates is untested. Policy could make a recession worse than it must be. I would add nothing says we couldn’t keep growing. Look at Japan [which had a 28-year stretch of economic growth].”

Sector Performance and Forecasts for 2020

Starts information is supplied by Dodge Analytics, followed by ConstructConnect, unless otherwise noted. Due to differing market categorization between the two forecasts, performance numbers can diverge. We try to reconcile those differences or cite them when they occur.

RESIDENTIAL

Holding its own

Residentional construction won’t likely recover to pre-Great Recession heights because those numbers reflected an overheated market. Today’s single-family market is maybe 40% smaller compared to prerecession activity, giving it lots of room

to grow. During this expansion, the strength of multifamily helped carry a residential recovery. The single-family sector has been steadily recovering too, but slowly. Total housing starts reached a peak in 2018 (1.375 million units/$330 billion).

In 2019, total starts were expected to fall 6% (1.29 million/

$314 million).

Single-family

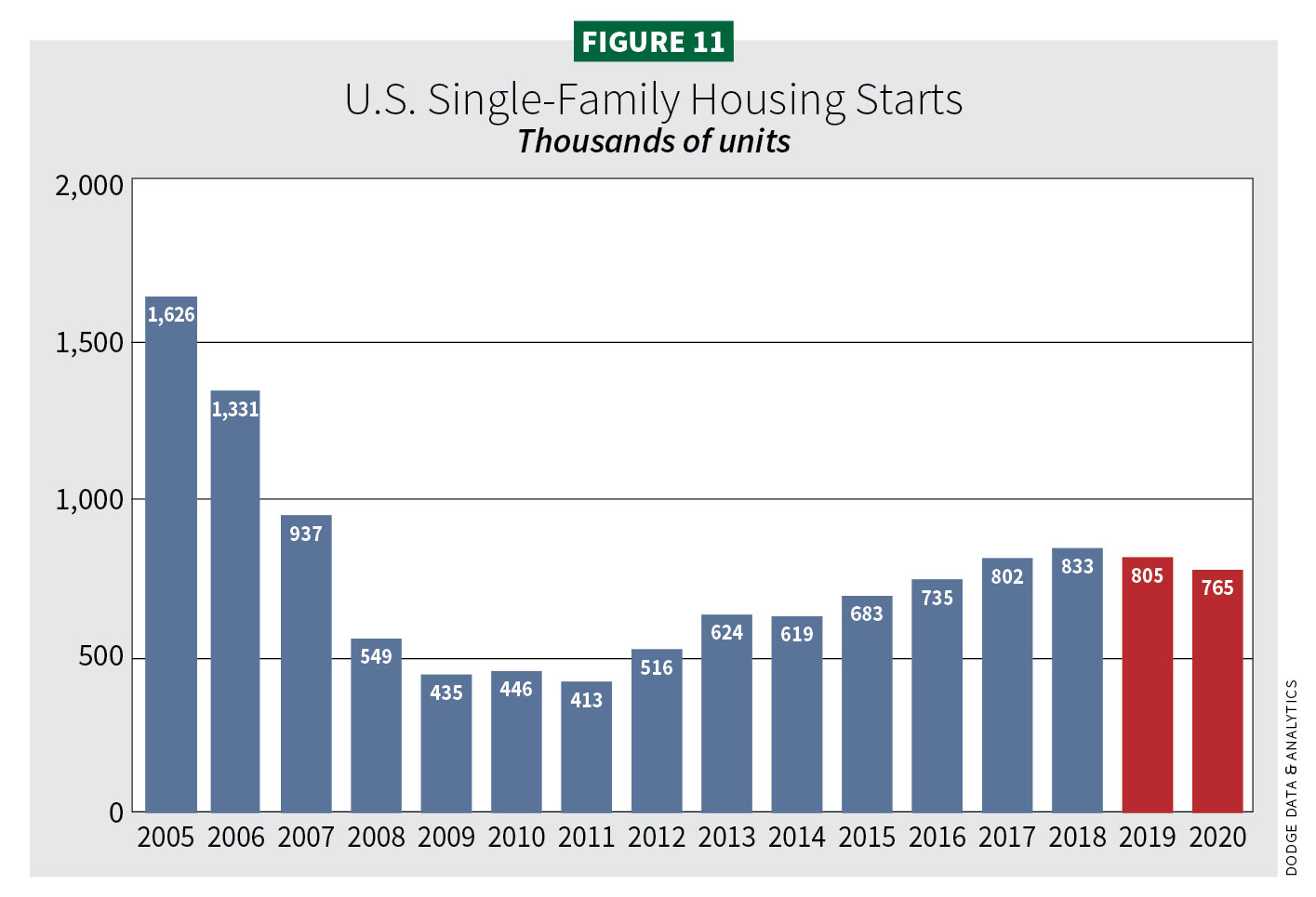

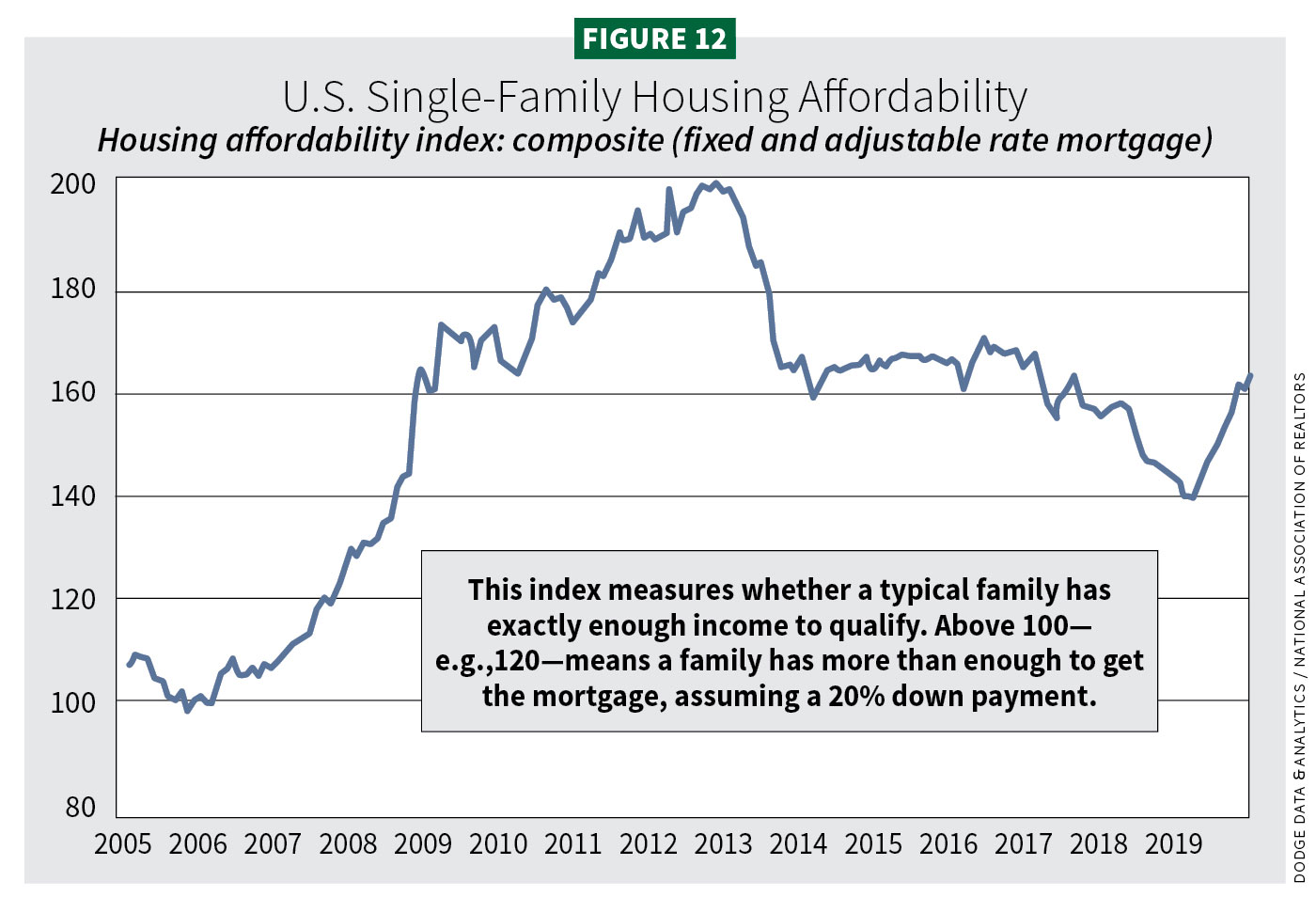

Let’s put the best news first. While AGC found PIP dollars for single-family fell 5 to 7% in 2019, it sees a rebound this year with growth between 5-10%. It attributes expansion fueled by low interest rates, rising income and wealth. Branch said that growth in -single-family construction usually happens after a recession. The United States is at half the market of 2005. There is a lack of entry-level single-family homes.

This year, Branch expects housing starts to fall (765,000 units) 8% below their 2018 peak and, in dollar values ($217 billion), 6% below peak (see Figures 11 and 12). Dodge terms this 2020 downturn as mild and likely short-lived. The National Association of Homebuyers’ (NAHB) numbers are more optimistic for 2020, showing an increase over 2019 (873,000 units). Low mortgage rates are expected to average under 4% for 30-year fixed. While higher personal incomes and wages give this market room to grow, the tight housing supply, demographics and the need for a larger construction worker pool continue to challenge this sector.

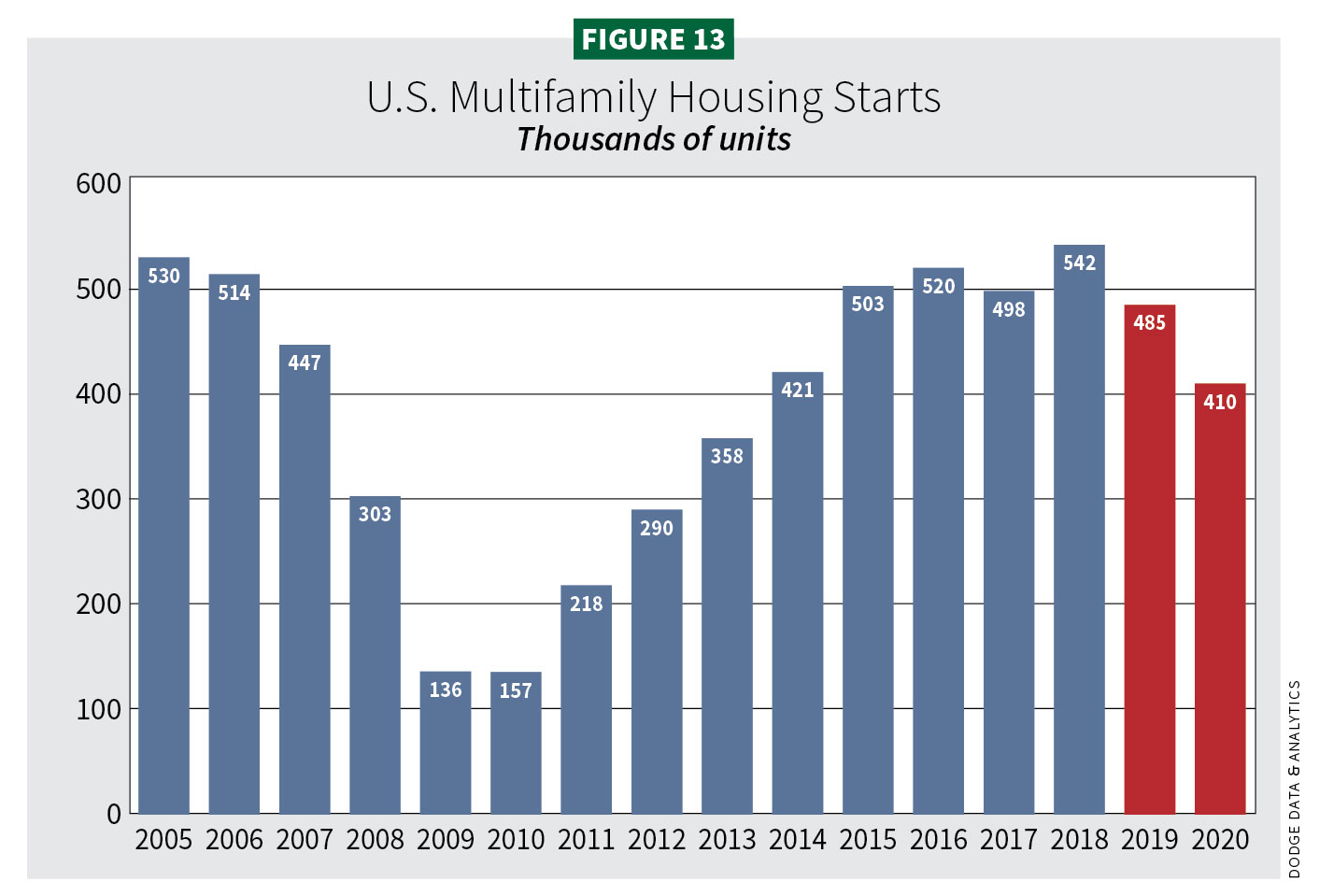

Multifamily

Multifamily has been a strong performer. In 2018, this sector reached 542,000 units, an increase of 298% from 2009. Representing a $100 billion achievement, starts rose ($443 billion) (see Figure 13).

“Millennials and boomers drove this, including senior housing,” Branch said. “The years 2015–2018 roughly saw the same level of growth. Multifamily starts have however followed a slowing economy in 2019.”

Last year, Dodge found starts fell 11% (485,000 units). Dollar values dropped 9% ($91 billion). ConstructConnect placed 2019 dollars lower ($75.5 billion). Of note, NAHB (383,000 units) for 2019 was almost 100,000 less than Dodge. A contraction is expected in 2020. Dodge anticipates 15% fewer starts (410,000 units/$78 billion). NAHB 2020 unit estimates (385,000) are closer to Dodge.

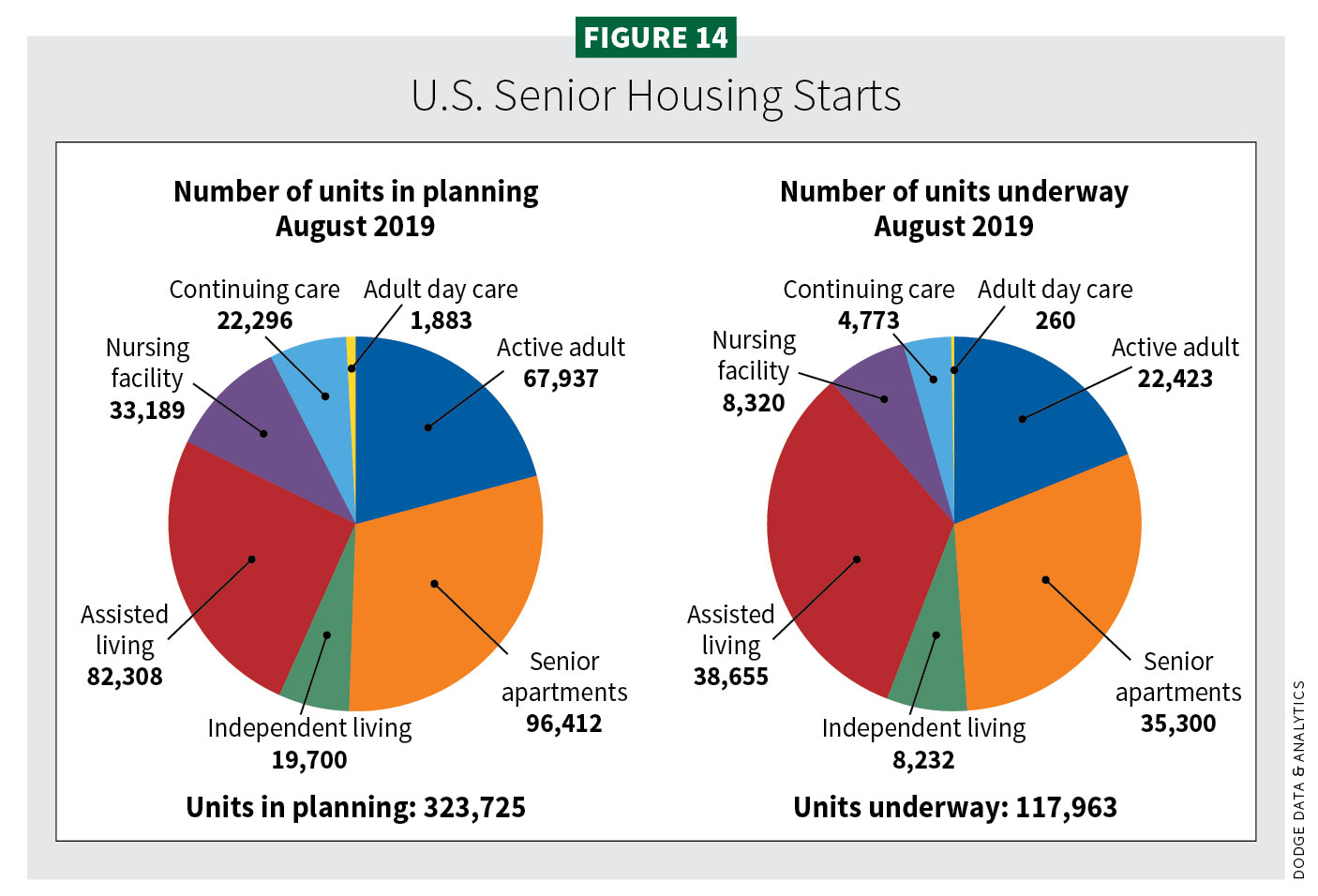

“Demand and supply have matched up over the past years,” Branch said. “Within this sector, assisted living and senior apartments in planning look very promising. Recent tax changes will also help support multifamily housing with investors. Together, these will help cushion multifamily, even if planned work doesn’t all come through” (see Figure 14).

The share of multifamily projects over $100 million remains above normal thanks to New York, Branch shared, adding. “High rises over 16 stories is also driven by New York City and notable projects in San Francisco and Dallas.”

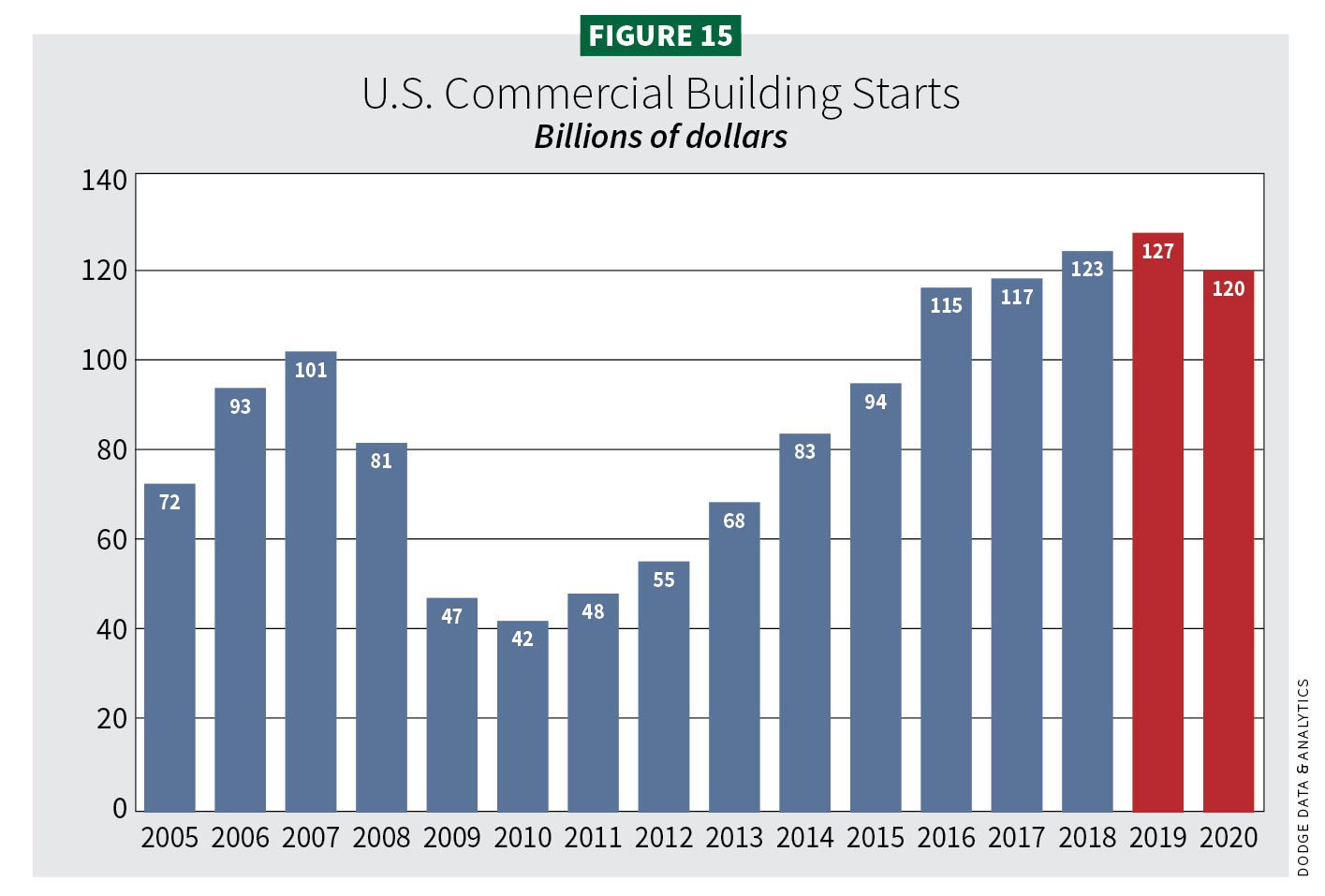

COMMERCIAL

Enjoying its round up

We may be enjoying what will be the zenith for commercial construction in this economic cycle. Square footage growth probably peaked in 2017 at 770 million square feet (msf). Dollar value (before adjusting for inflation) likely peaked in 2019 ($126.6 billion). Starts were expected to retreat 2% last year (741 msf) or 4% below 2017. Dollar values gained 3%. Figure 15 measures stores, offices, warehouses, hotels and parking garages. This year, Dodge expects a decline in square footage and dollar value. Commercial square footage will lose 10% (670 msf) and fall 6% ($119.5 billion).

ConstructConnect measures commercial with fewer markets (e.g., offices, parking garages and transportation terminals) and so its estimates are not a complete match to Dodge. As such, its 2019 starts showed a 9.1% increase ($41.1 billion). ConstructConnect, using fewer sectors, projects a total start increase of 8.1% ($44.4 billion) this year.

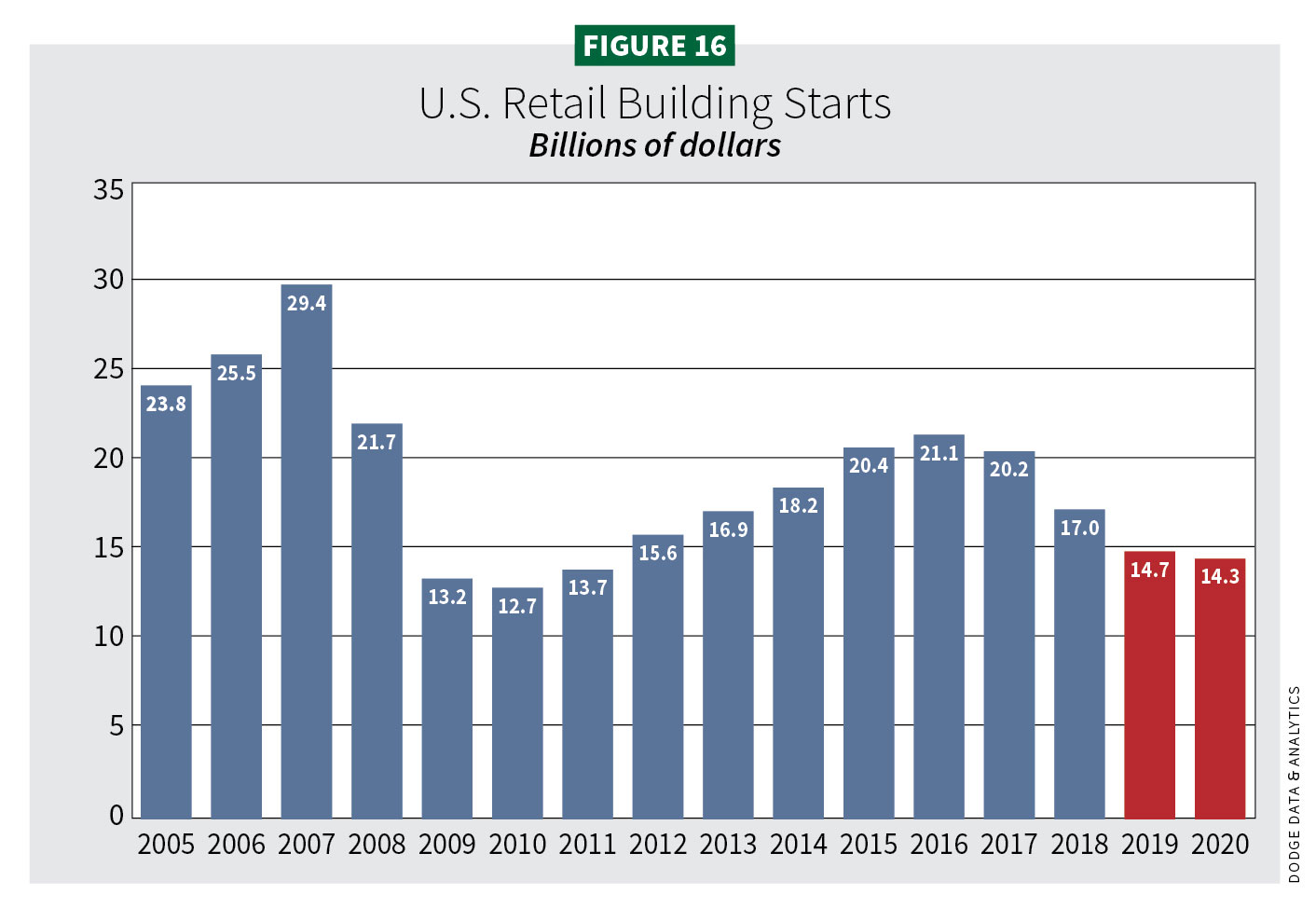

Stores and shopping centers

Online retail is truly disrupting the retail landscape. The U.S. Commerce Department reported e-sales reached $146.2 billion in 2nd quarter 2019 compared to 3.2% growth for traditional retail. For perspective, e-commerce represents just 10.7% of all retail sales. Capital investment, however, favors e-commerce. Last year, retail starts were expected to drop 18% (66.5 msf) with dollar values decreasing 14% ($14.7 billion). ConstructConnect concurs. In 2020, starts are projected to fall another 3% (64.4 msf) and 3% in dollar value ($14.3 billion) (see Figure 16).

Recent tariffs on Chinese imports could dampen retail construction and consumer spending. U.S. Bancorp (USB) estimates tariffs could put $40 billion in sales and 12,000 stores at risk. AGC’s Simonson added that retail’s distress is compounded by a record number of store closings. Business Insider reported more than 7,000 store closings were announced last year. Coresight Research, a consumer analytics group, anticipated numbers

to rise to as many as 12,000. Companies closing stores included Gap, Victoria’s Secret, J.C. Penney and Abercrombie & Fitch. Amazon is counterintuitively—or shrewdly—adding investment in its bookstores and other bricks-and-mortar concepts, including Amazon Go convenience stores.

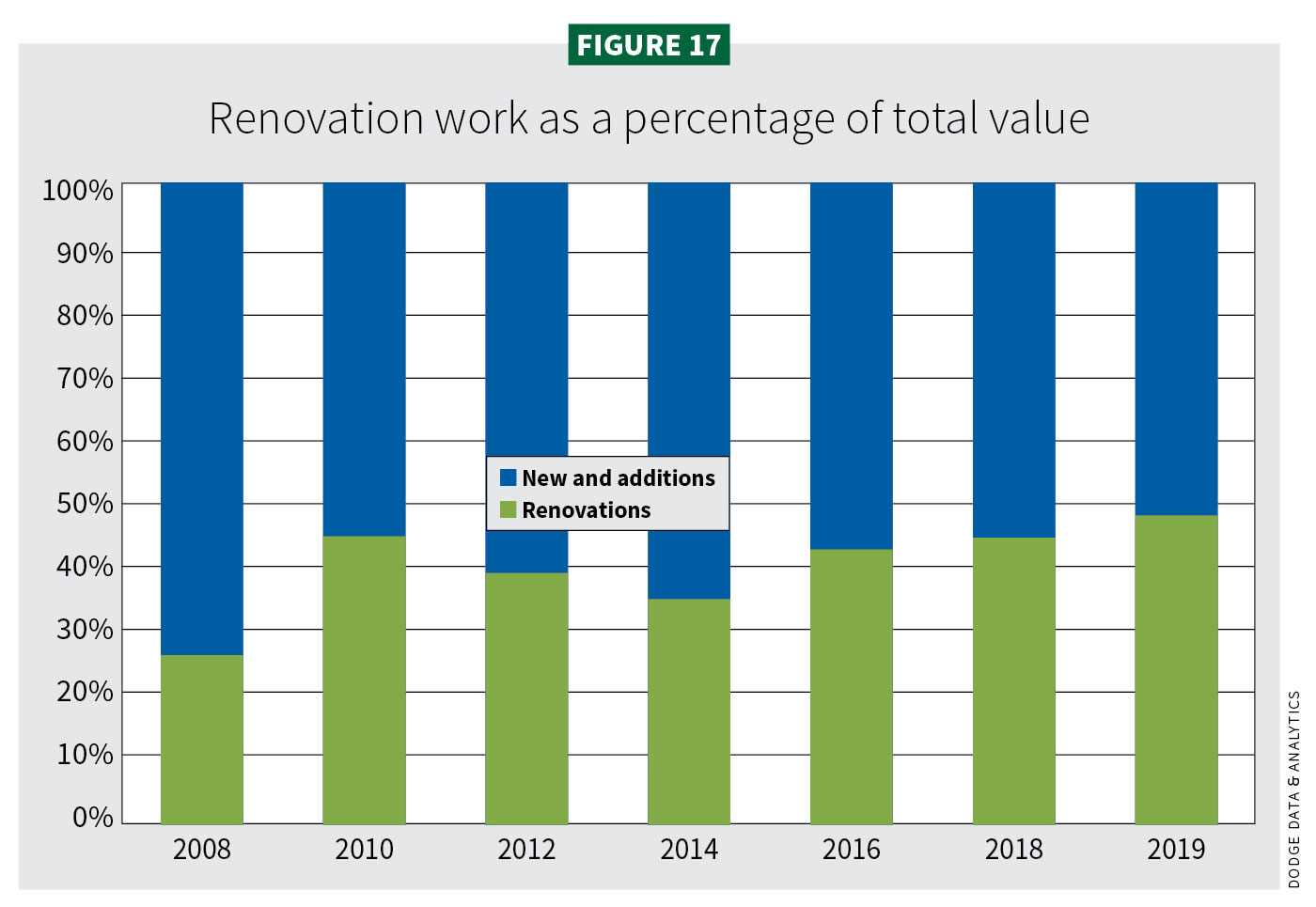

Dodge reported U.S. retailers’ expansion of store footprints has also “dramatically decreased.” Walmart is still the largest constructor, followed by Target and Aldi, Branch said. An upside to a lack of new construction in retail is a steady amount of store renovation (see Figure 17).

“Approximately 40-45% of retail starts are now renovation,” he said.

Commercial warehouses

Warehouse construction was off to the races between 2011 through 2017, increasing by double-digits each year (510%). Starts began to slow in 2018, showing a 2% decrease in activity. Vacancy rates remain low and regional distribution centers are driving growth, Branch said. Last year, dollar values rose 7% ($25.3 billion), but square footage contracted 2% (288 msf). ConstructConnect showed $19.1 billion. In 2020, a 10% contraction in dollar value ($22.8 billion) is projected, including a decrease of 13% in square footage (251 msf).ConstructConnect projects $17.3 billion.

The largest warehouse starts have generally come from online retailers such as Amazon, but brick-and-mortar has entered the warehouse space to service online business. In the first nine months of 2019, 34 warehouses broke ground sized at least 1 msf representing a total of 48.3 msf. This, however, was an 8% decrease from 2018. Of note to ECs, many retail and warehouses and distribution centers are becoming increasingly automated, providing new power installation opportunities beyond lighting and HVAC. In addition, warehouses are increasingly accommodating e-grocery shopping.

“Amazon may change how it builds warehouses,” Branch added. “For same-day delivery, urban warehouses that are smaller (500,000 to 1 million msf) are emerging. Amazon and other firms are also renting warehouse space instead of building.”

Four of the top five warehouse projects were for Amazon (Prime Air Hub at CVG Airport, Hebron, Ky., $750 million, 3,350 thousand square feet (tsf); Project Arrow, Oak Creek, Wis. (2,600 tsf); and distribution centers in Bakersfield, Calif. (2,600 tsf), and Stone Mountain, Ga. (2,463 tsf), all for $200 million).

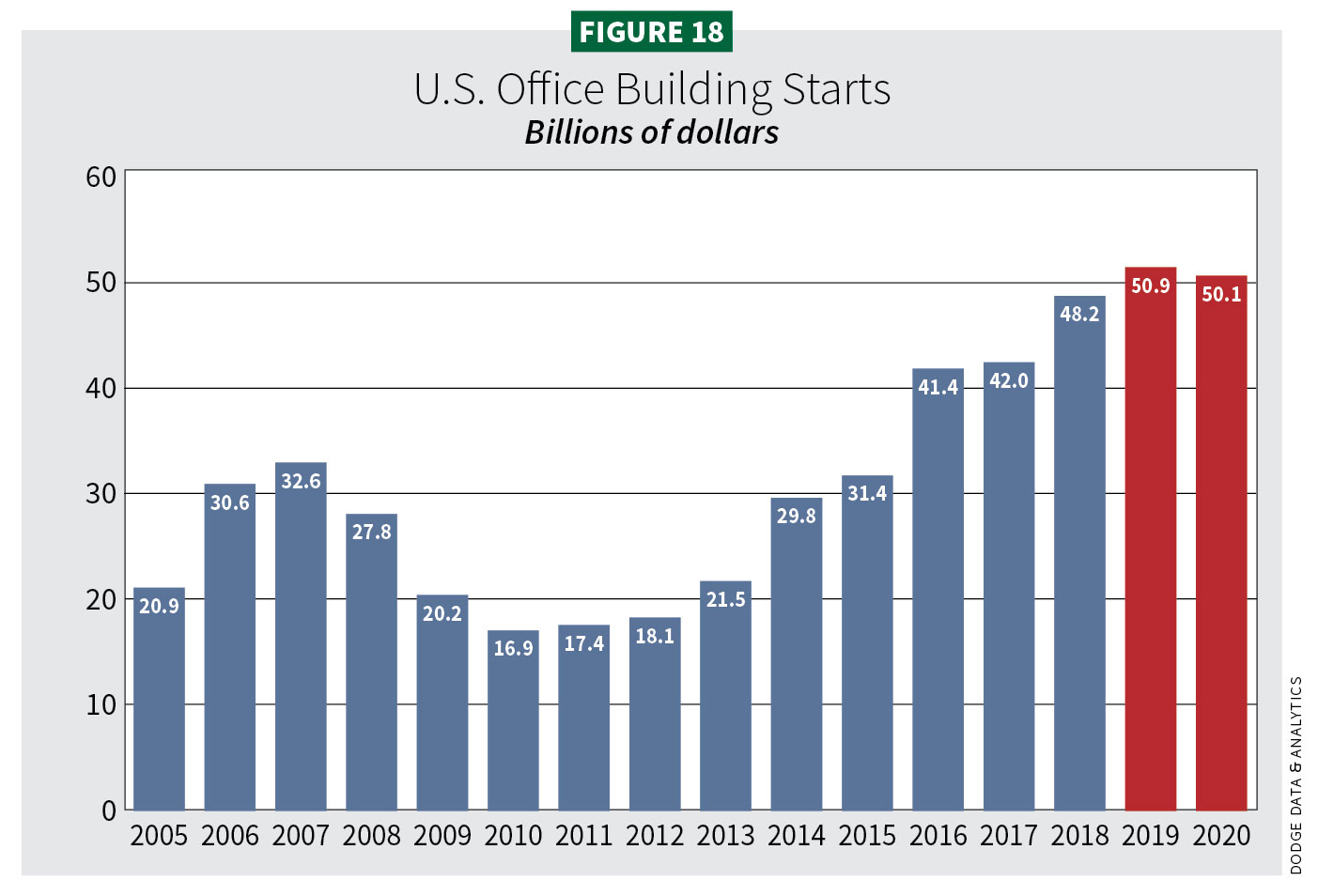

Office buildings

Office construction continued to show strength in 2019, building off 2010–2018, where starts grew 140% in square footage (137 msf) and 186% in dollar value ($48.2 billion). Last year, office construction grew 2% (139 msf) and advanced 6% in dollar value ($50.9 billion). ConstructConnect evaluated the private-only office sector at $28 billion. This year, Dodge expects square footage to retract 4% (133 msf) and dollar values growth of 2% ($50.1 billion) (ConstructConnect, $30 billion/private office) (see Figure 18).

Branch ascribed some of the growth in office to data centers. In the first nine months of 2019, construction began on 57 data centers. Dodge labels data centers a “structural change” to the office sector.

“Through September 2019, $6.1 billion of office starts were data centers,” he said. “Virginia, Texas and Iowa lead in data centers with many pursuing green power.”

ConstructConnect’s Carrick said that office growth may be helped by the rise in high-tech jobs. In “United States Office Outlook–Q3 2019,” commercial real estate firm Jones Lang LaSalle reported, “High-growth tech, creative and life sciences tenants continued to drive occupancy gains.” Also, “Despite new supply hitting the market, vacancy currently rests at just 14.2% nationally.”

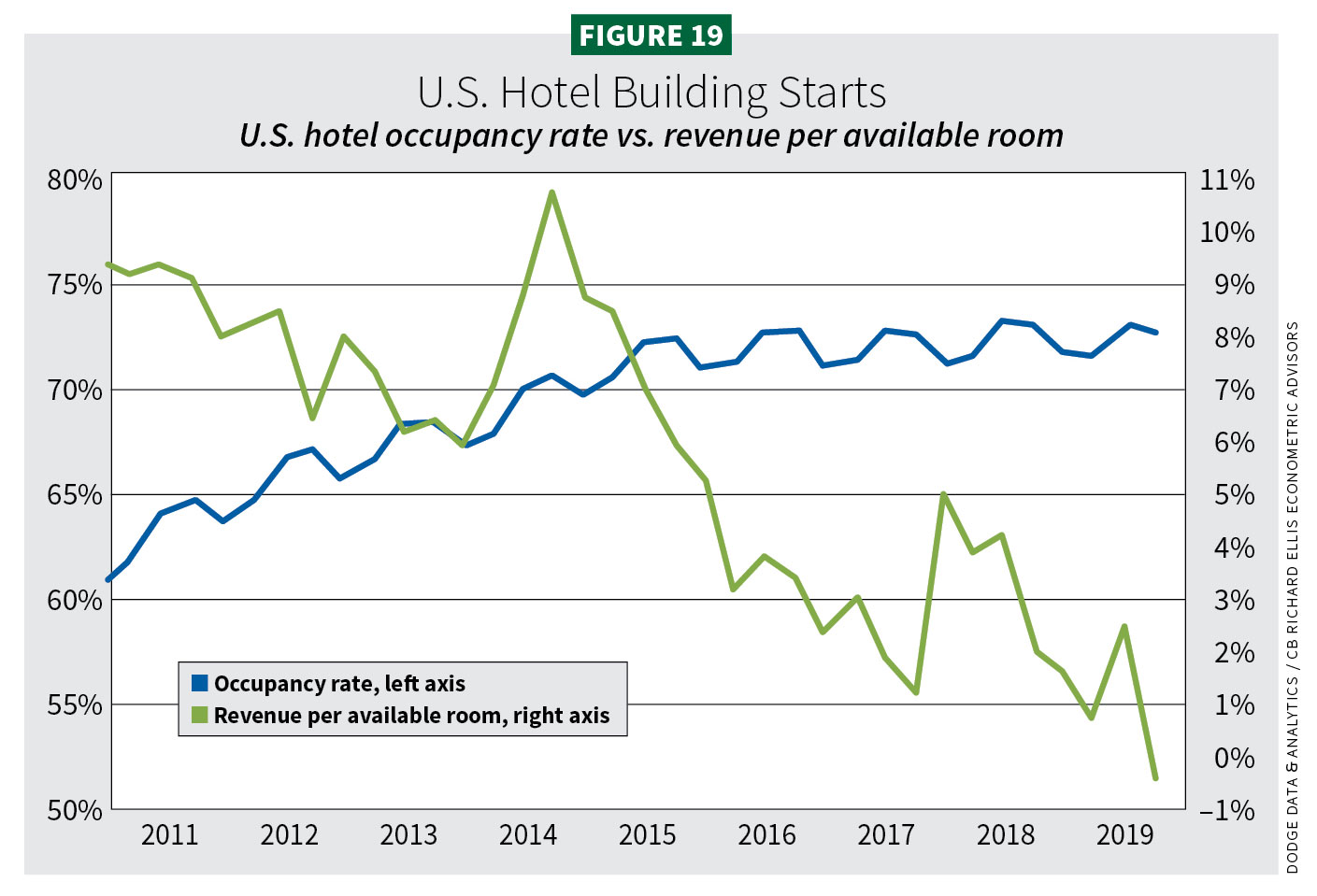

Hotels and motels

Between 2010–2018, hotel starts climbed 368% (nearly 80 msf) and dollar value 440% ($19.1 billion in 2018). After a 10-year expansion, growth weakened in 2019 as business and leisure travel softened. Hotel square footage dropped 6% (75 msf) and 4% in dollar value ($18.4 billion). In 2020, expect a deeper pullback to 15% (63 msf) and dollar values reduced another 11% ($16.3 billion). ConstructConnect, $18.1 billion.

“Occupancy rates are good, but revenue growth is negative,” Branch said. “So, hotel construction is starting to slip back but remains strong. Its decline puts it back to where it was in 2016-2018, which was strong. RevPAR (revenue per available room) is now affecting this sector” (see Figure 19).

Statista, a German statistics database, reports RevPAR in the U.S. lodging industry increased by roughly 3% from 2017 to 2018. Between 2019 and 2020, RevPAR is predicted to advance 1%.

The largest projects were the TSX Broadway Hotel in New York; Broward Convention Center in Fort Lauderdale, Fla.; and Las Vegas Circa Resort.

Branch added that, as the economy slows, so will convention center development, which often has associated hotels.

INSTITUTIONAL

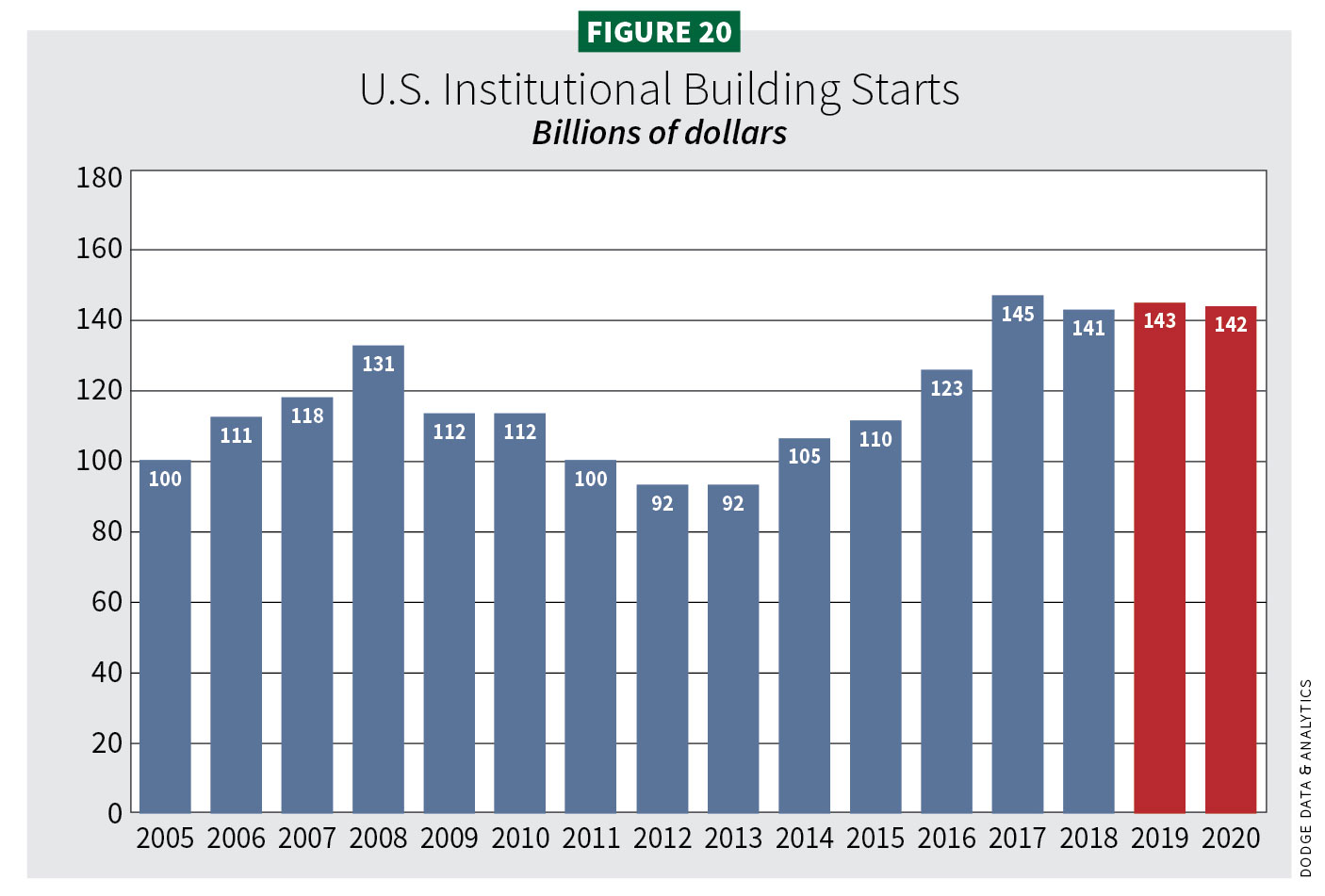

Back by public demand

Whether it’s a school, hospital, airport or rail terminal, the institutional sector is buoyed by public sector money or hurt by lack of it. Last year was solid for institutional, which gained 2% ($142.7 billion) and backtracked 1% in square footage. Starts this year are expected to be flat ($142.5 billion) with square footage declining 4% (323 msf) (see Figure 20).

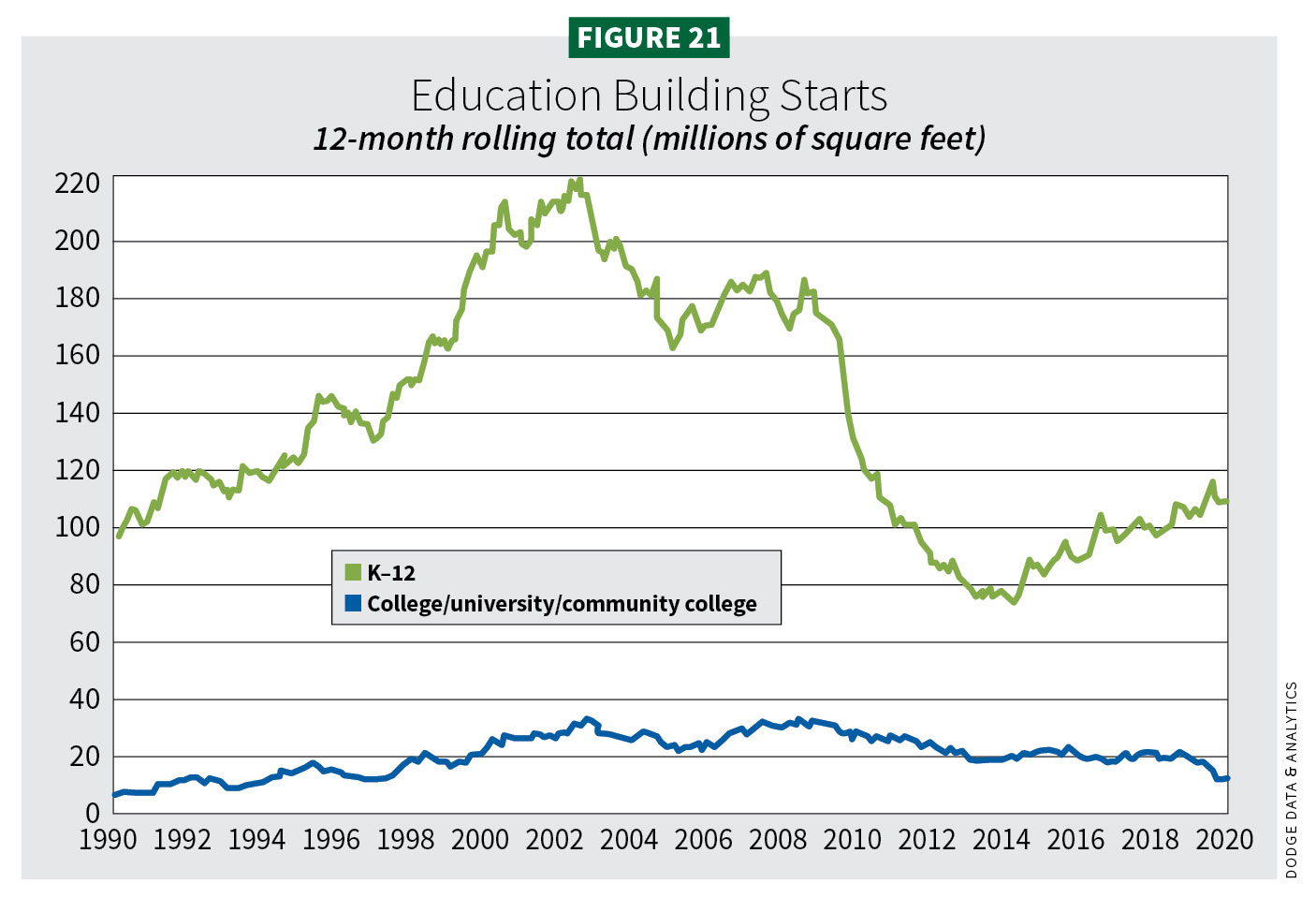

Education buildings

Education construction starts in 2018 rose appreciably by 8% ($62.9 billion) and in square footage 3% (140 msf). Last year, starts remained positive but slowed to 3% ($64.6 billion) while rising 1% in square footage (142 msf). This year, expect growth at 2% ($65.7 billion) marking the slowest pace since 2013. Square footage will fall 2% (139 msf). ConstructConnect’s numbers were $71.8 billion for 2019 and a projection of $74.1 billion for 2020 (see Figure 21).

“I see growth in K-12 supported by bonds,” Branch said. “Demographics will hold this back in the future. Public school enrollment is strongest in South and West, negative in the Midwest and Great Lakes, but that doesn’t mean construction is stopped. There is demand despite lower enrollments.”

Dodge reported nine of the 15 largest projects breaking ground in 2019 were senior high schools, citing the $247 million renovation/addition of Belmont (Mass.) High School. Three of the four largest projects are in Massachusetts.

Community college, university and laboratory/museum/library starts declined. The largest project was the Wellesley College (Mass.) Science Center ($159 million).

According to the National Center for Education Statistics projections, K–8 schools will see a smaller growth over the next few years, reflecting that millennials over 30 are waiting longer to marry and have children.

Branch finds growth in college enrollments won’t offset a projected easing in endowments.

Bond measures continue to support the education sector. During the November 2018 election cycle, voters in California and Texas approved bonds, $17 billion and $5 billion, respectively. This year, California will put forward another bond measure ($15 billion) to renovate aging facilities.

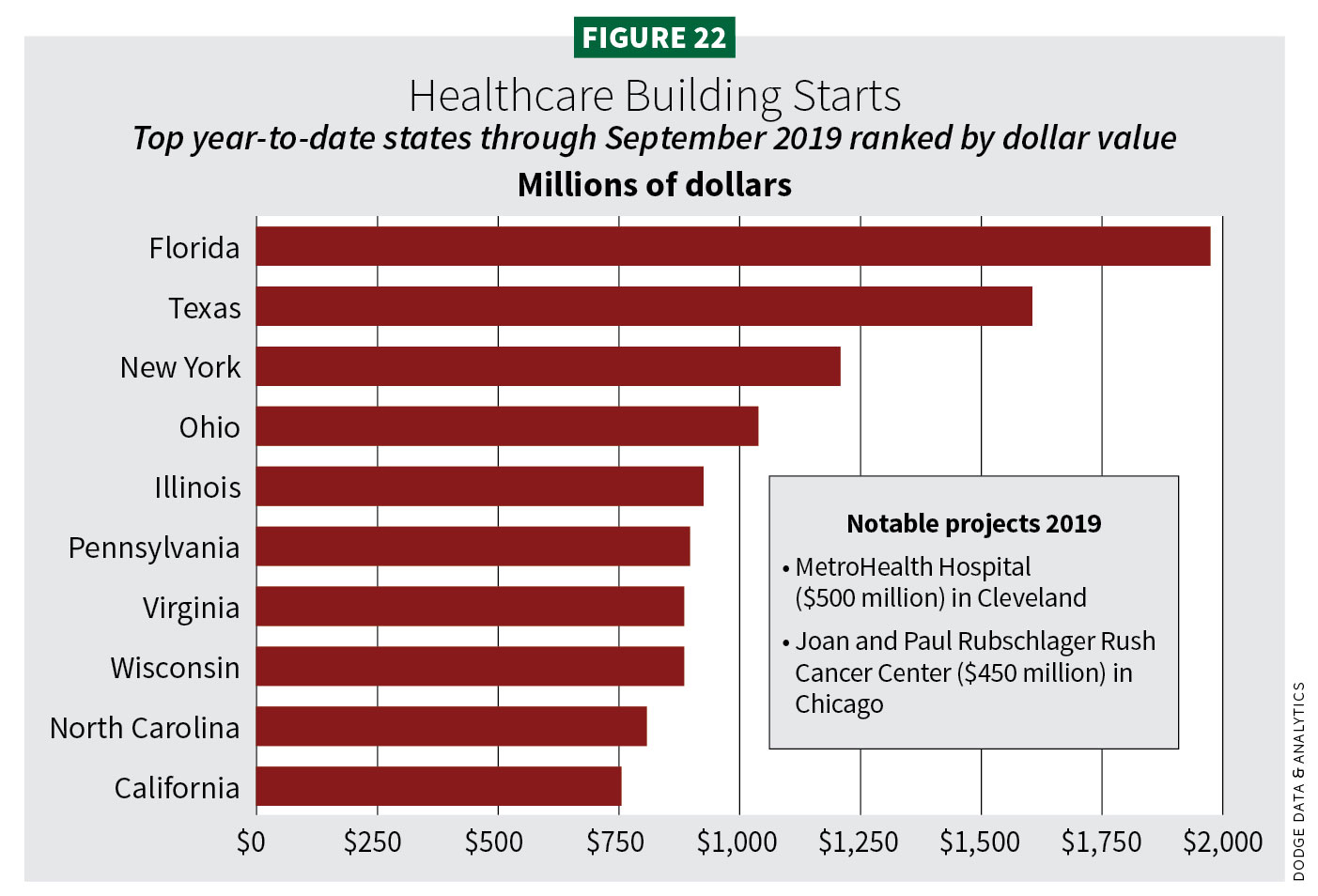

Healthcare buildings

Healthcare construction remains weak. In 2019, square footage fell 6% (76 msf) but gained 1% in dollar value ($27.6 billion). ConstructConnect saw starts differently,

dropping 13.9% but with a high dollar value ($33.2 billion). This year, square footage will lose another 3% (74 msf) but dollar values will advance 3% ($28.6 billion). ConstructConnect, $36.1 billion.

In 2010, 13% of the U.S. population was over the age of 64. By 2030, it will reach 20%, according to the U.S. Census Bureau. Longer lived boomers will have medical problems, which could lead to more medical facilities.

“There is a pent-up demand supported by demographics and new tech,” Branch said. “Construction of clinics and nursing homes are the greatest share of healthcare starts as hospitals pull back. This move is broad-based across the country.”

He said the gap widened in the 1990s as a shift toward private clinics took hold. It narrowed in the recession but has since widened again. See Figure 22 for the top 10 states in healthcare starts.

Meanwhile, healthcare policy remains turbulent, affecting construction growth. With the House of Representatives controlled by Democrats, it seems unlikely the Affordable Care Act (ACA) will be repealed. What traction Medicare for All holds remains unknown.

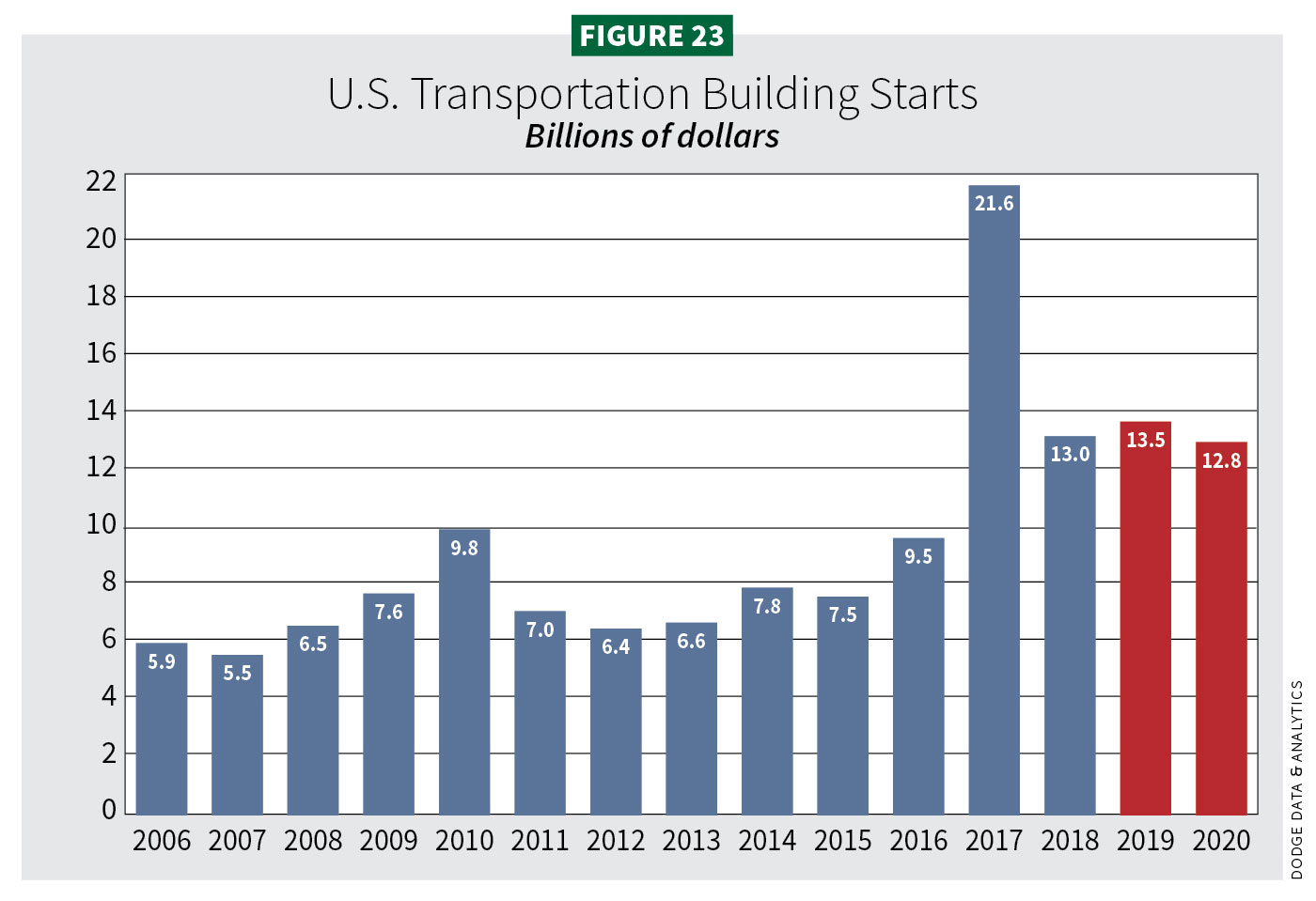

Transportation buildings

These past few years have delivered strong in transportation starts. Many have been $10 billion or more since 2016. Though starts fell some 40% in 2018 ($13 billion), they did include a $2.1 billion reconstruction project at Denver International Airport and the $1.4 billion Terminal One project at Newark International Airport. In 2019, starts increased again by 4% ($13.5 billion) with square footage jumping 17% (29 msf) (see Figure 23). ConstructConnect placed starts lower at $7 billion. Continued strength is predicted for 2020 with 5% growth ($12.8 billion) but with a drop of 8% in square footage (27 msf). ConstructConnect predicts $9.2 billion.

“This sector is stabilizing based on Fed policy,” Branch said. “Rising air traffic and revenue is also spurring airport rehabs, which grew 4% (2018), though they may slip 5% this year (2019). Fed funding is generally positive.”

The Federal Aviation Administration Reauthorization Act of 2018 maintains the FAA through 2023. Within this, the Airport Improvement Program will fund $3.35 billion in grant dollars for airport improvements. The act also provides discretionary grants

of more than $1 billion for small to medium-sized airports. An additional $17.5 billion was set aside by Congress for the FAA. It also introduced a bill for another $10.6 billion/FAA’s FY2020 budget.

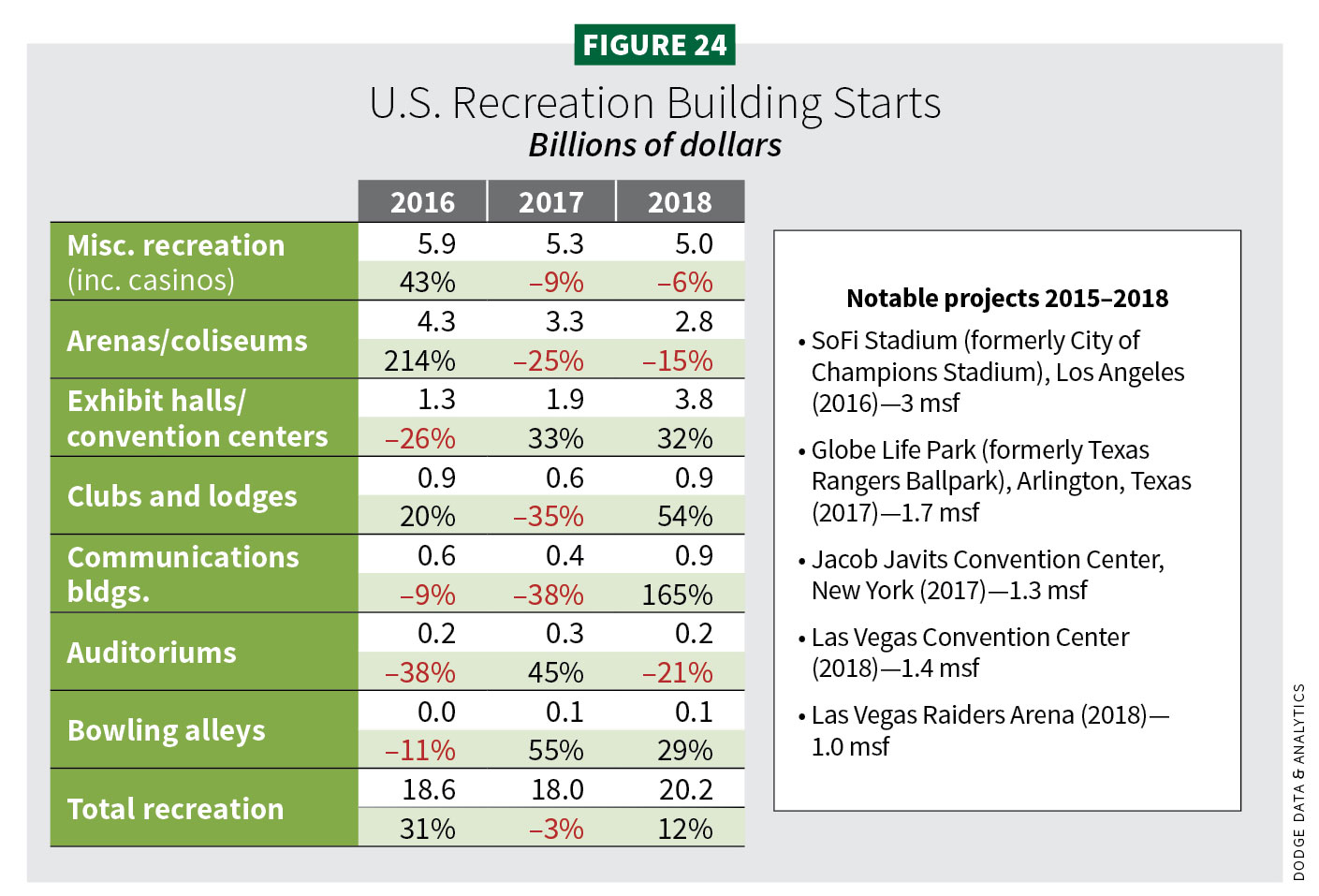

Recreation buildings

In 2019, starts dipped 12% (43 msf) and dollar value dropped 9% ($18.4 billion). Unlike Dodge, ConstructConnect doesn’t include campus athletic and student centers under “Recreation.” As such, its dollar value for 2019 stood at $8.3 billion. A slowing economy and dampening demand for business and leisure travel will hit this sector this year. Square footage will lose 12% (38 msf), and dollar value of starts will recede 8% ($170 billion). ConstructConnect sees largely flat growth.

Other factors contributing to declining starts is a depletion of big projects. In 2018, construction of convention centers drove growth. Total starts increased 12% ($20.2 billion) adding 3% square footage (49 msf).See notable projects in Figure 24.

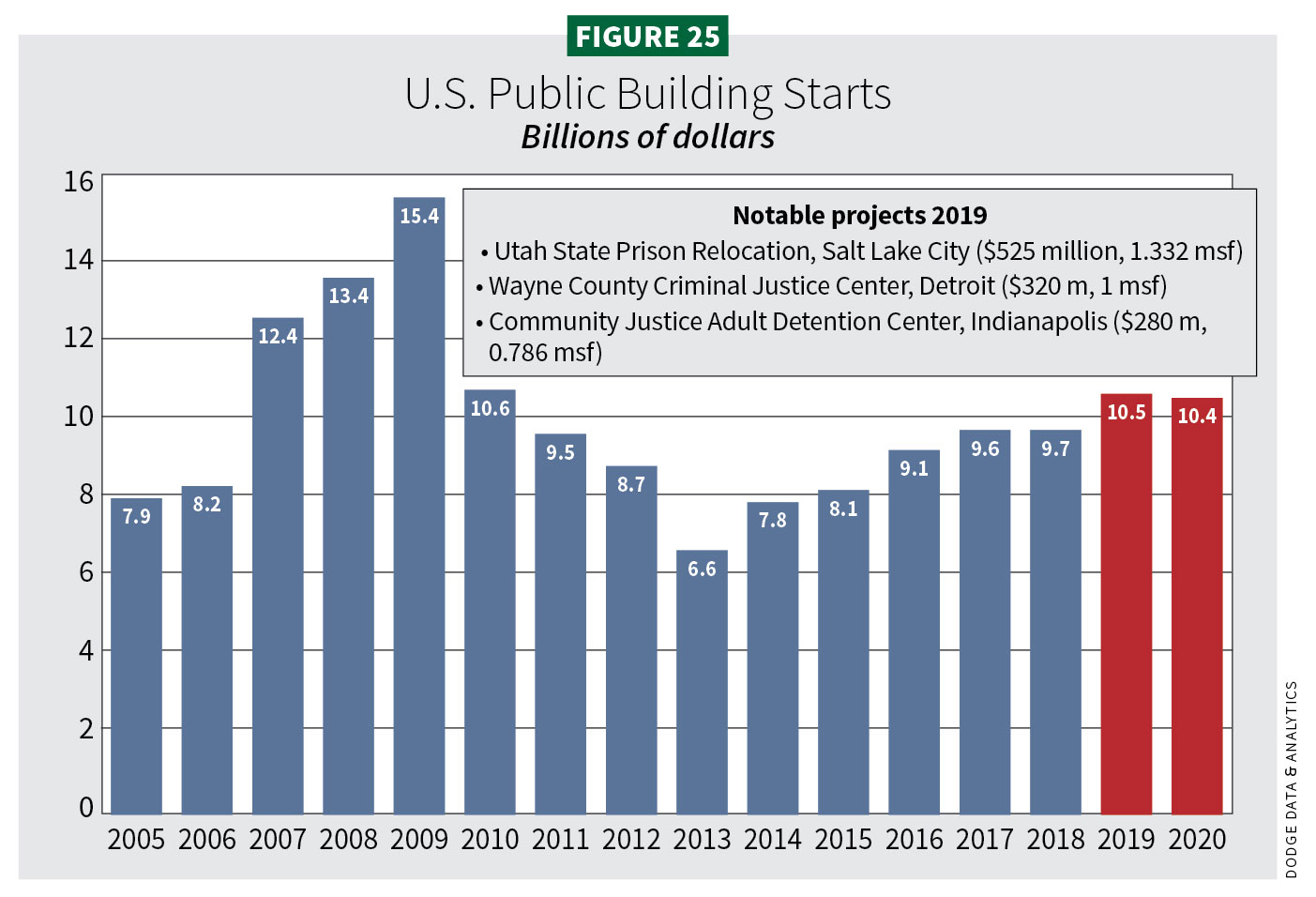

Public buildings

Public building construction includes capitols, courthouses, police and fire stations, and other public administrative facilities. This sector has had difficulty gaining traction. Last year brought good news. Starts rose 5% (20 msf) and 8% ($10.5 billion), a peak during this recovery. This marked the first time in almost 10 years where this sector’s dollar value surpassed $10 billion (see Figure 25). ConstructConnect had larger start numbers though a contraction of –3% ($18.5 billion). Some modest declines are expected this year. Square footage will fall 3% (20 msf) and lose 1% dollar value ($10.4 billion). ConstructConnect expects growth of $19.5 billion.

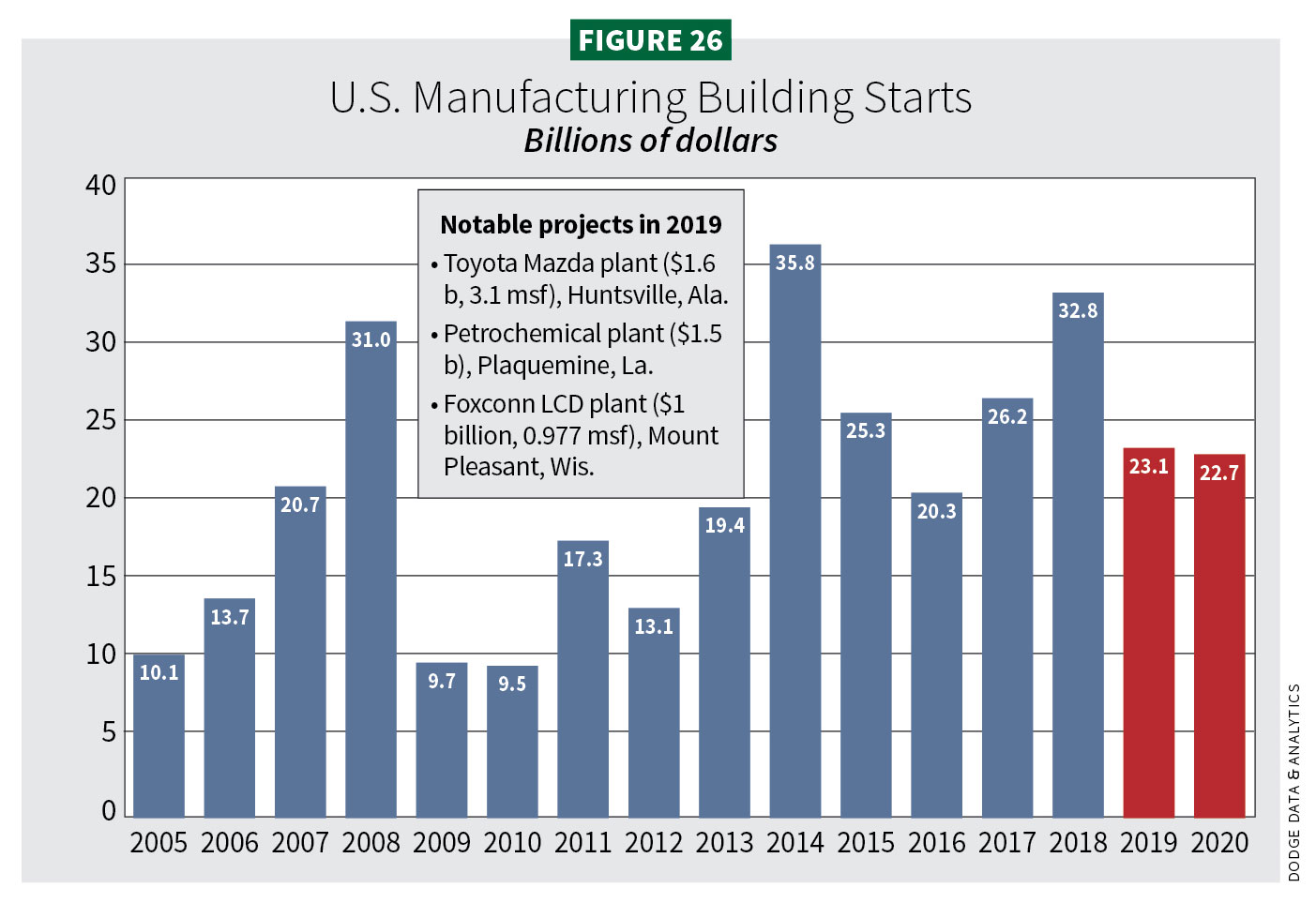

MANUFACTURING

Facing a struggle

With the U.S. Department of Energy’s $6.5 billion uranium processing facility in Oak Ridge, Tenn., project in the rear-view mirror, 2019 manufacturing starts in square footage declined 16% (71 msf) and dollar values fell 29% ($23.1 billion). ConstructConnect placed starts at double that of Dodge ($54.8 billion). This year, starts will decrease 2% ($22.7 billion). ConstructConnect expects a drop but a healthier number ($36.9 billion) (see Figure 26).

The trade war, slower GDP growth, and decelerating economic growth in Canada, the European Union and China crimp this sector. During the first nine months of 2019, the production of motor vehicles fell 5.4% year over year. Nondurable goods dropped 1.4%. Manufacturing capacity utilization went from 77.3% in 2018 to 75.3% by September 2019.

In better news, the Manufacturers Alliance for Productivity and Innovation (MAPI) Foundation surmised capital growth and higher exports boosted 2019 manufacturing, allowing for a projected production growth of 3.9%. This year MAPI forecasts lesser growth at 2.4%.

NONBUILDING

Public works and power utilities

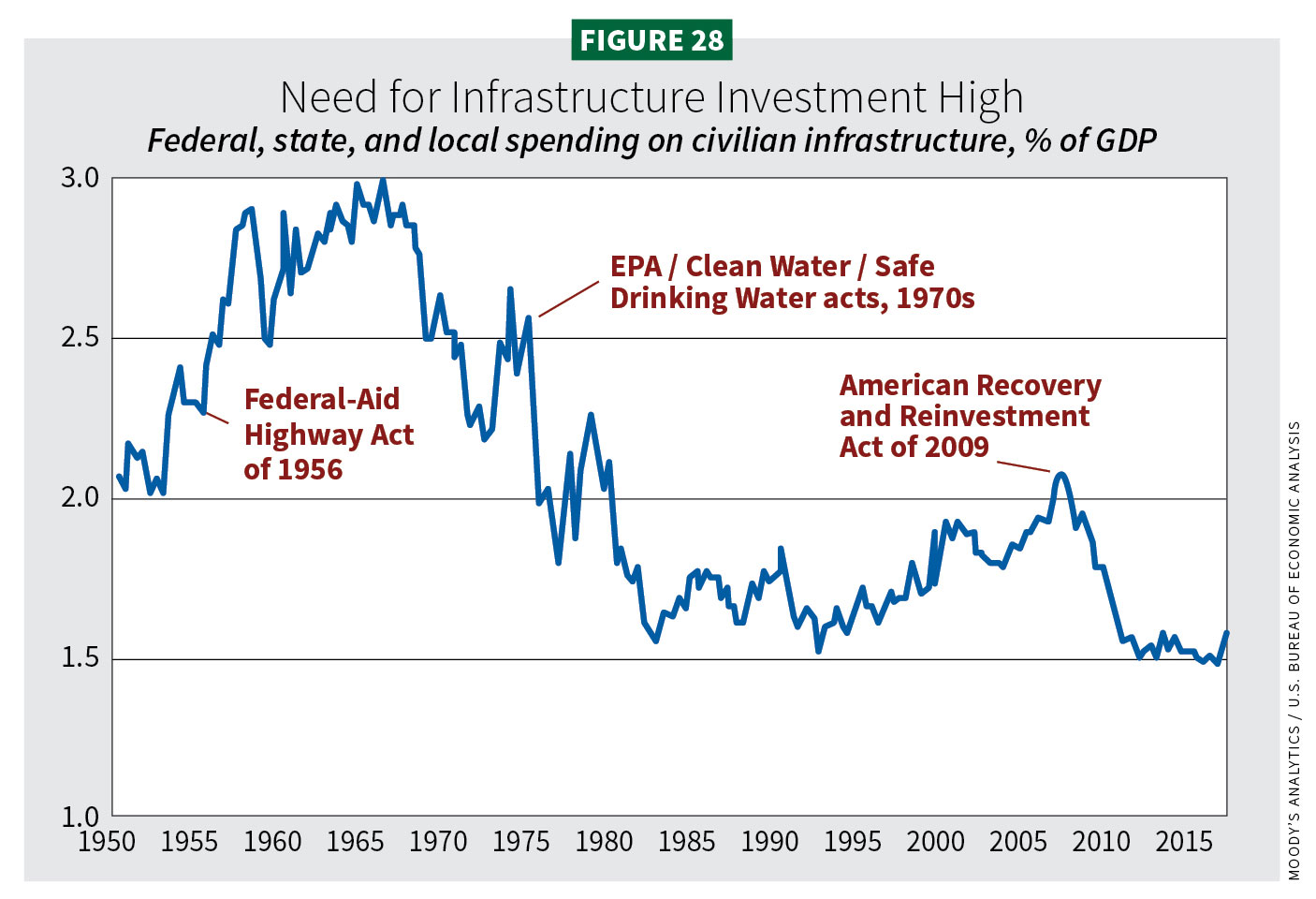

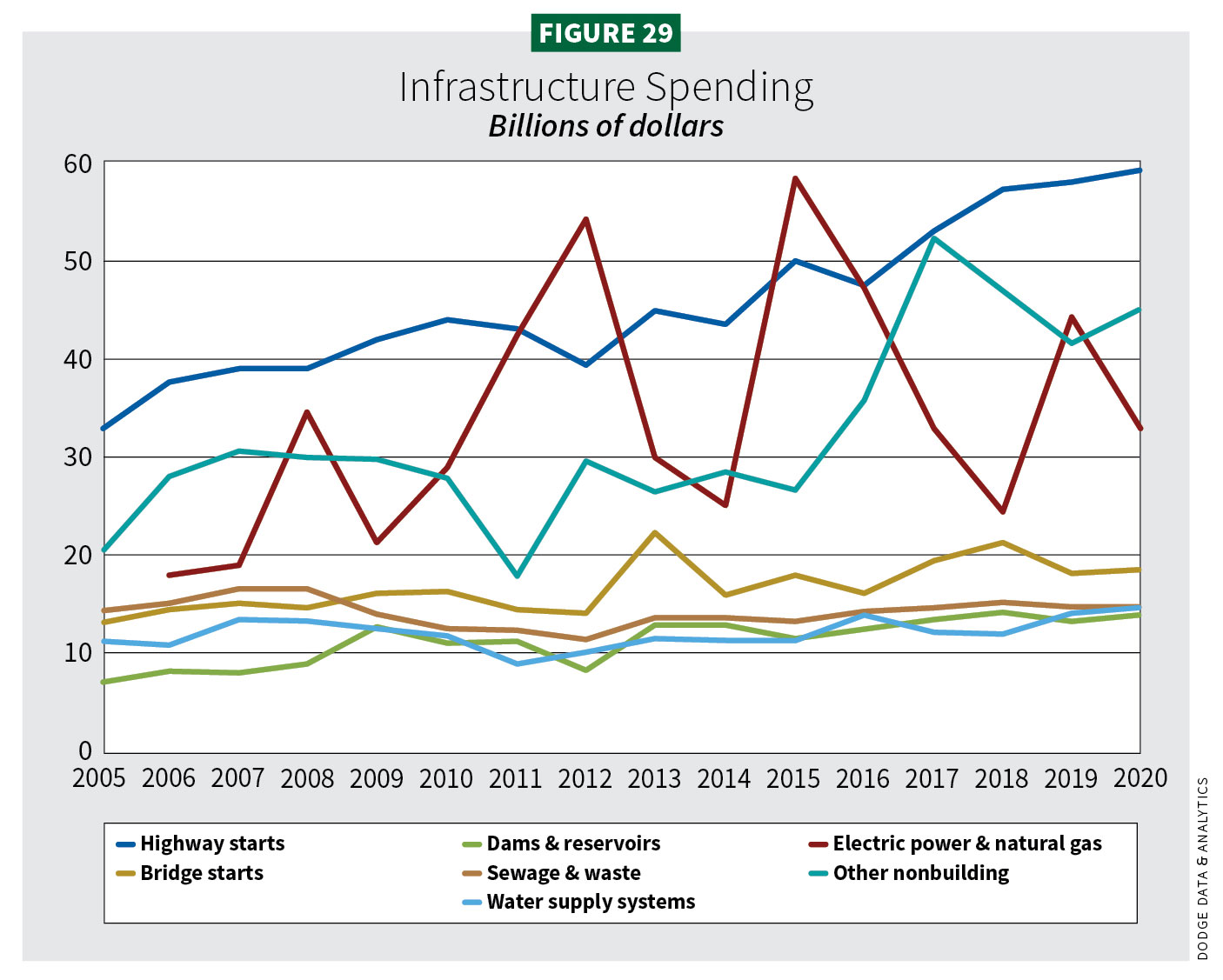

In important ways, the public works and power utilities sectors stand alone as a construction sector. More than economic trends, this sector is influenced by legislation and regulations. Last year, they worked in this sector’s favor. In 2019, electric power/gas plant starts soared 83% ($44.2 billion), in part thanks to liquefied natural gas (LNG) construction. For several years, this sector’s poor performance held back overall construction performance totals. Public works in 2019 did decline 4% ($157.9 billion) due to some weakness in bridge and pipeline construction. Public works will gain 4% ($164.3 billion) in 2020. Power/utility starts will fall back to a respectable 27% gain ($32.2 billion). Total nonbuilding starts will drop 3% ($196.4 billion) this year (see Figures 27, 28 and 29).

Street and bridges

Construction starts for streets and bridges slipped 2% ($75.8 billion) in 2019. ConstructConnect had stronger numbers ($89.5 billion). In 2020, street and bridges will see a rise of 2% ($77.5 billion). ConstructConnect, $94.7 billion.

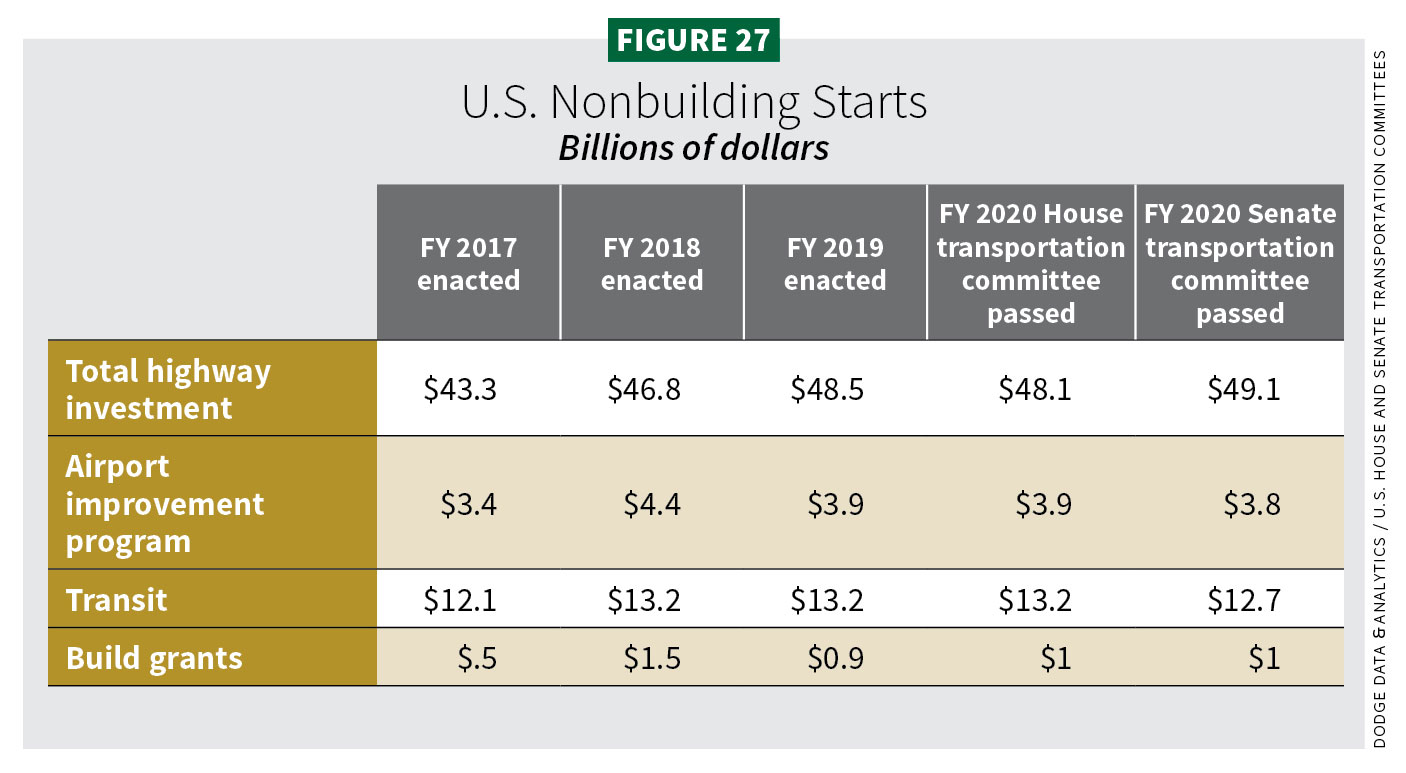

This year marks the end of the Fixing America’s Surface Transportation (FAST) Act, though the U.S. Senate has proposed America’s Transportation Infrastructure Act of 2019. It would authorize $287 billion over five years (+27%). That vote (as of this writing) is still pending. More investment is needed.

In lieu of wavering federal funds, a dozen states have raised their gas tax to boost transportation infrastructure spending.

Environmental public works

Environmental public works involves water supply, sewers/hazardous waste, and water resources. Construction starts for this sector rose 5% ($41.2 billion) in 2019. ConstructConnect has a narrower sector definition (water and sewage treatment). Their starts were thus lower ($29.9 billion). This year will see another 2% gain ($42.2 billion). ConstructConnect, $31.8 billion.

Environmental public works construction starts were helped by a $19.1 billion disaster relief bill passed in June 2019 targeting flooding, damage from tornadoes and hurricanes and other natural disasters. Under the America’s Water Infrastructure Act of 2018 (AWIA), was the reauthorization of the Water Resources Development Act (WRDA), which approved $3.7 billion for the U.S. Army of Engineers to use in dredging, flood control and other projects. AWIA also provides funding for state revolving loans funds. Though more comprehensive funding for environmental public works is needed, additional pockets of funding have helped. The Army Corps of Engineers received an additional $43.3 billion for flood and hurricane protection projects. Also, the EPA got $349 million to improve resiliency for state water systems vulnerable to natural disasters.

Other nonbuilding

The other nonbuilding sector includes pipelines, rail lines and large sports venues without roofs, strangely enough. Robust pipeline activity (2016–2019) is starting to weaken, which softened total nonbuilding starts. Rail line activity showed some strengthening. Last year, this sector fell 14% ($40.9 billion). ConstructConnect captured pipeline starts ($25.6 billion). Things look better in 2020 as nonbuilding will have a 9% increase ($44.6 billion). [ConstructConnect, $24.7 billion (pipelines only)].

Notable projects in 2019 included the Landside Access Modernization project at Los Angeles International Airport ($2.7 billion). Work also began on the Permian Highway Pipeline project ($2 billion) and a natural gas pipeline ($1.8 billion), both in Texas. In 2020, work is expected to begin on a Line 3 Replacement pipeline ($2.1 billion) across North Dakota, Minnesota and Wisconsin. Beginning phases of a 420-mile Dallas-to-Houston High Speed Rail Project ($10 billion) should commence, as well.

Electric power and gas plants

It was a very good year for the electric power and gas plant sector in 2019. Starts rose 83% ($44.2 billion). ConstructConnect doesn’t specifically call out gas plants but captures work under “industrial.” Electric is under “civil’ as power infrastructure. So, the numbers did not fully match. As such, their 2019 starts were roughly $38.3 billion. This year will see a decline of 27% ($32.2 billion). ConstructConnect sees $70.3 billion (a rough calculation combining its industrial and power infrastructure).

Key projects last year included the Calcasieu Pass LNG export plant ($4.2 billion) and the Sabine Pass Trains 5&6 ($2.5 billion) both in Cameron, La. As of September 2019, the Federal Energy Regulatory Commission (FERC) approved eight LNG projects with nine more applications pending.

Several renewable-energy projects, (notably wind) were expected to emerge as developers planned for the phase-out of the production tax credit (PTC) by the end of 2019. There may be a reprieve. On Nov. 19, the House Ways and Means Committee

introduced the draft Growing Renewable Energy and Efficiency Now Act, designed to maintain the wind energy PTC at 60% for five years and extend the investment tax credit for solar and offshore wind for the same duration. The American Wind Energy Association reported that, in 2019, wind generation totaled 3,667 MW, a 123% increase over the first three quarters of 2018.

Summary

Construction will see a slowdown but enjoy gains in most sectors. There’s plenty of work in the pipeline, so it is a time of opportunity. Focus on how you and your company can work smarter, faster and be more technologically proficient. Your customers may expect it. Training and finding qualified workers will also remain an ongoing effort. Expand what “qualified” can mean to your business. Finally, the more clearly you can see your project landscape (in hand and opportunity), the better you’ll navigate through a blurry 2020. Time to get a new prescription.

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].