If the economy went in for a checkup, the doctor would likely say, “Keep doing what you’re doing.” Overall, things are positive with no surprises. We’re at full employment. Inflation is in check. The stock market is confident. Personal and disposable income is up, as is personal savings. While averaging 2.4 percent since 2013, gross domestic product (GDP) has rallied to 3.0 percent or higher in the second and third quarters of 2017. An overall GDP of 2.6 percent is forecast for 2018. In addition, the fourth quarter of 2017 showed the highest level of consumer confidence in nearly 17 years as reported by the New York-based Conference Board. Wage growth, too, is turning a corner.

Taken together, the economy’s good health will provide continued growth for the construction industry in 2018 as the expansion matures.

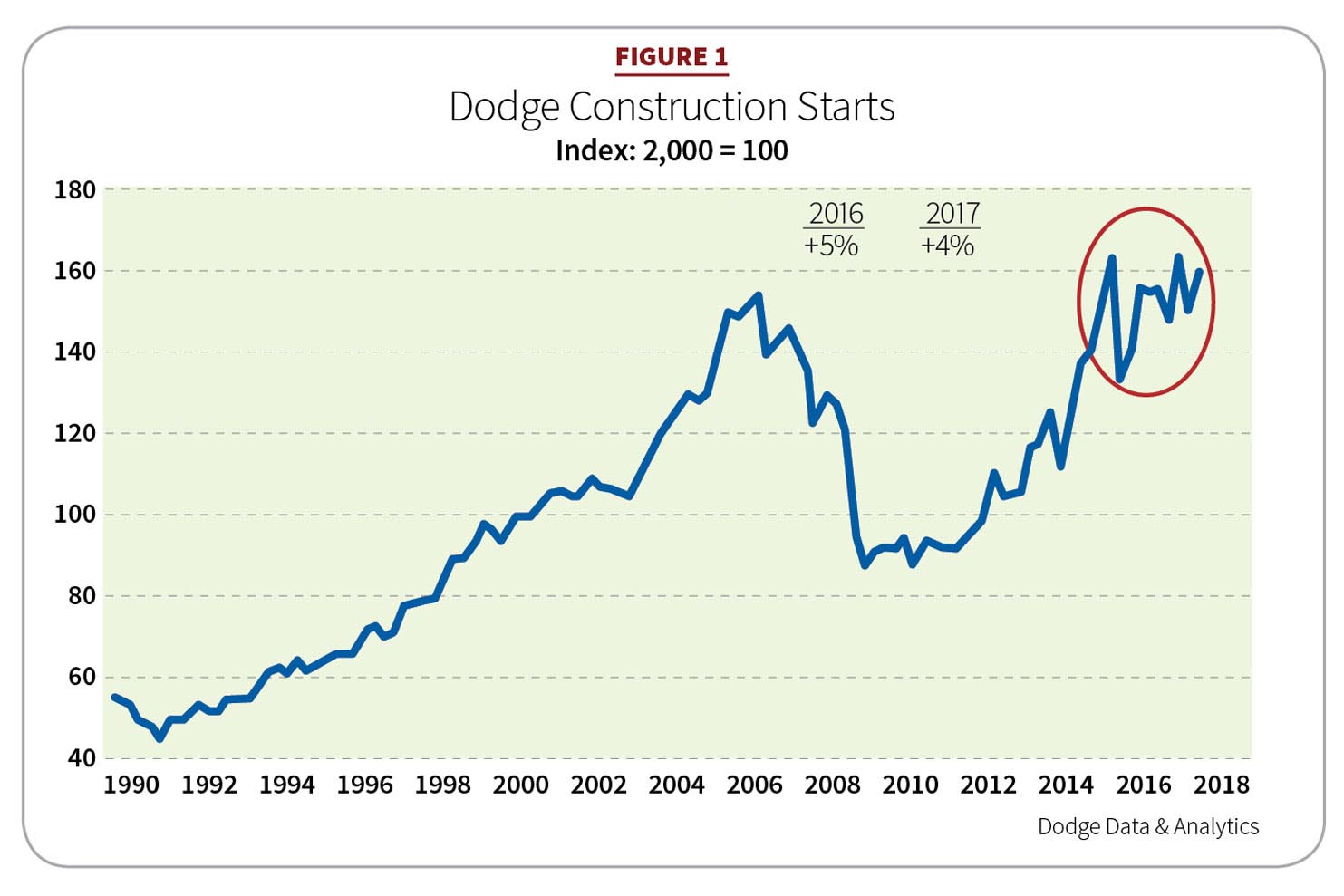

Dodge Data & Analytics predicts total U.S. construction starts in 2018 will climb 3 percent to $765 billion. That breaks down to a 4 percent gain in residential and 2 percent in nonresidential. Nonbuilding will gain 1 percent after a rough couple of years (see Figure 1).

The firm’s findings were shared at the 79th annual Dodge Construction Outlook forecast on Nov. 2, 2017, in Chicago. On Nov. 1, chief economists from ConstructConnect, co-sponsored by the American Institute of Architects (AIA) and the Associated General Contractors of America (AGC), put forth their 2018 growth estimate of 4.8 percent. Its “2018 Design & Construction Outlook” was its ninth annual fall economic webcast.

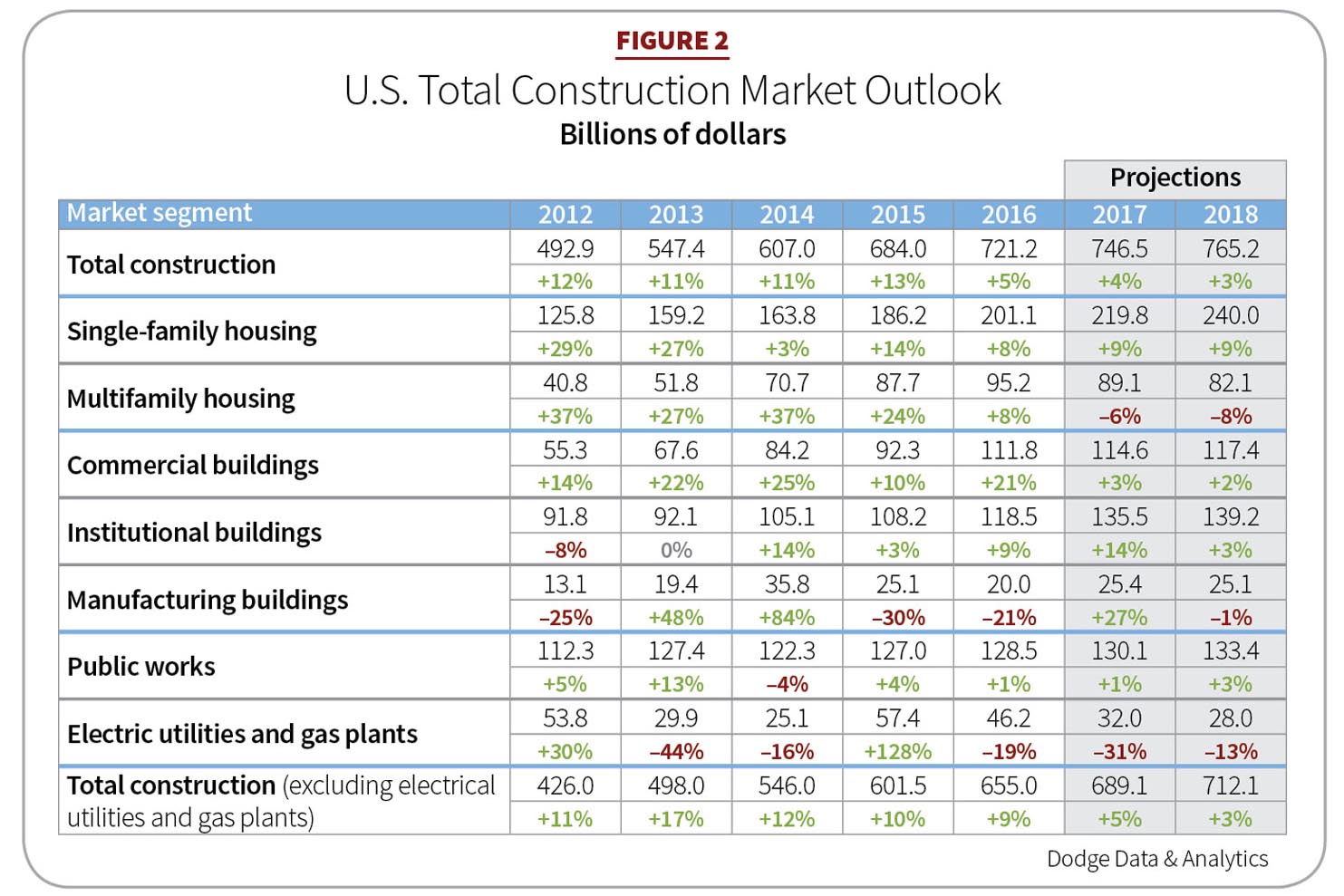

The modest forecast for 2018 largely mirrored 2017, for which Dodge estimated a 4 percent gain ($746 billion). That represented a strong 10 percent improvement in nonresidential, a 4 percent rise in residential construction, and a 7 percent loss in nonbuilding construction due to weak electric utilities/gas plant construction and relatively flat growth for public works projects. The heady advances of 11 to 13 percent per year from 2012 through 2015 have receded. Forecasters at ConstructConnect reported similar gains (4.5 percent) for 2017 but revised them in November to 7.9 percent on the strength of some major civil engineering infrastructure projects that were started in the fourth quarter (see Figure 2).

“A mature stage of expansion” is how Robert Murray, chief economist for Dodge Data & Analytics, characterized today’s construction industry. “For 2018, there are several positive factors which suggest that the construction expansion has further room to proceed. The U.S. economy is anticipated to see moderate job growth. Long-term interest rates may see some upward movement but not substantially. While market fundamentals for commercial real estate won’t be quite as strong as [2017], funding support for construction will continue to come from state and local bond measures.”

Alex Carrick, North American chief economist for ConstructConnect, said during his firm’s webinar, “There’s a synchronous world expansion, the first in over a decade. North America, Japan, China and Europe are all experiencing GDP growth. [The Dow Jones Industrial Average] and Standard & Poor’s 500 are up 250 percent compared to their recession low points. NASDAQ is up 400 percent since 2009. Also, a lot of hope has been put on millennials [individuals born between 1981 and 2000] who are now starting to enter the workforce in greater numbers.”

After four months of declines in 2017 (June through September), the Dodge Momentum Index rose 13.9 percent in October to 131.3 from September’s 115.6. It again advanced 13.9 percent in November, climbing to 149.9. The index is a monthly measure of the first (or initial) report for planned nonresidential building projects, which have been shown to lead this construction spending by a full year. The index has gained nearly 21 percent from November 2016–November 2017 with commercial up 24 percent and institutional 17 percent.

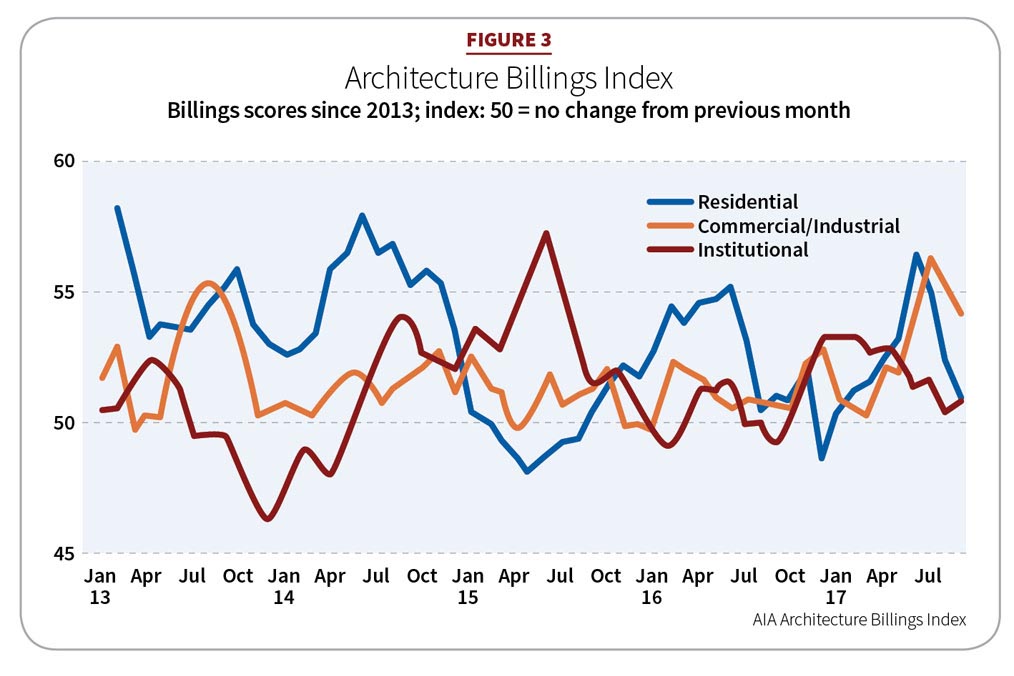

The Architecture Billings Index (ABI) is another measure of economic activity for construction. It reflects the 9–12 month lead time between architecture billings and construction spending. The ABI score in October 2017 was 51.7, up from 49.1 the previous month (see Figure 3). Any score above 50 indicates an increase in billing.

“Our architecture billing index was trending down mid-year 2015 and 2016, but then picked up in early 2017,” said Kermit Baker, chief economist, AIA. “It bounced around a bit throughout the year but overall has been quite strong. Billing should remain positive.”

More economic underpinnings

At the Dodge conference, Cristian deRitis, senior director, Moody’s Analytics, said he sees more “good” than “risk” in the economy going into 2018.

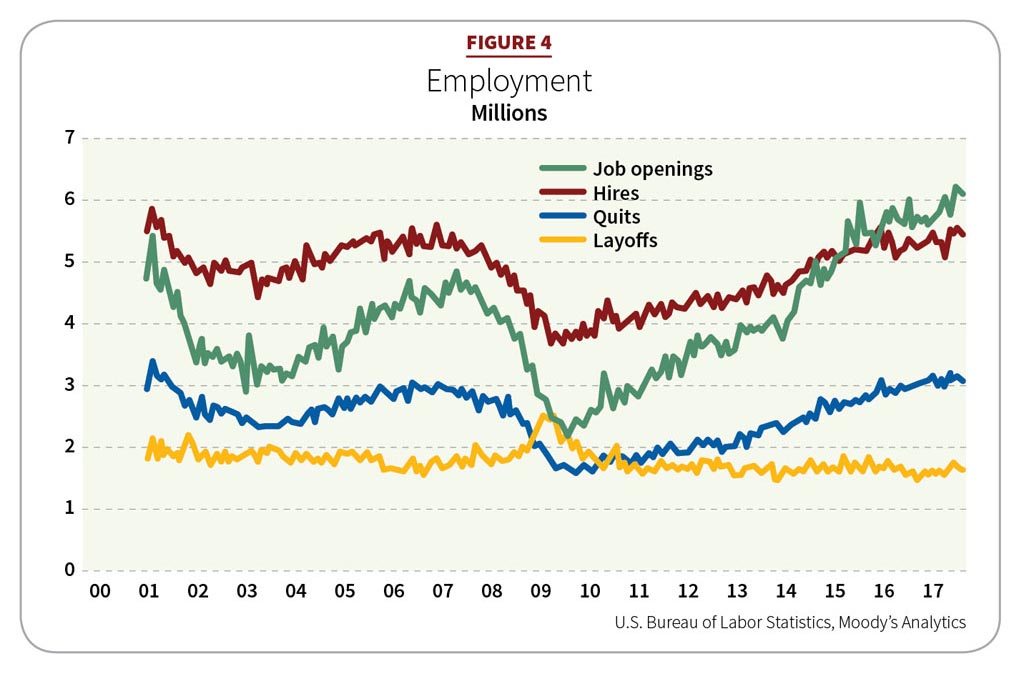

“The labor market helps us focus on how the economy is doing,” deRitis said. “The 1.6 million job openings is a record and points to the strength of the economy.”

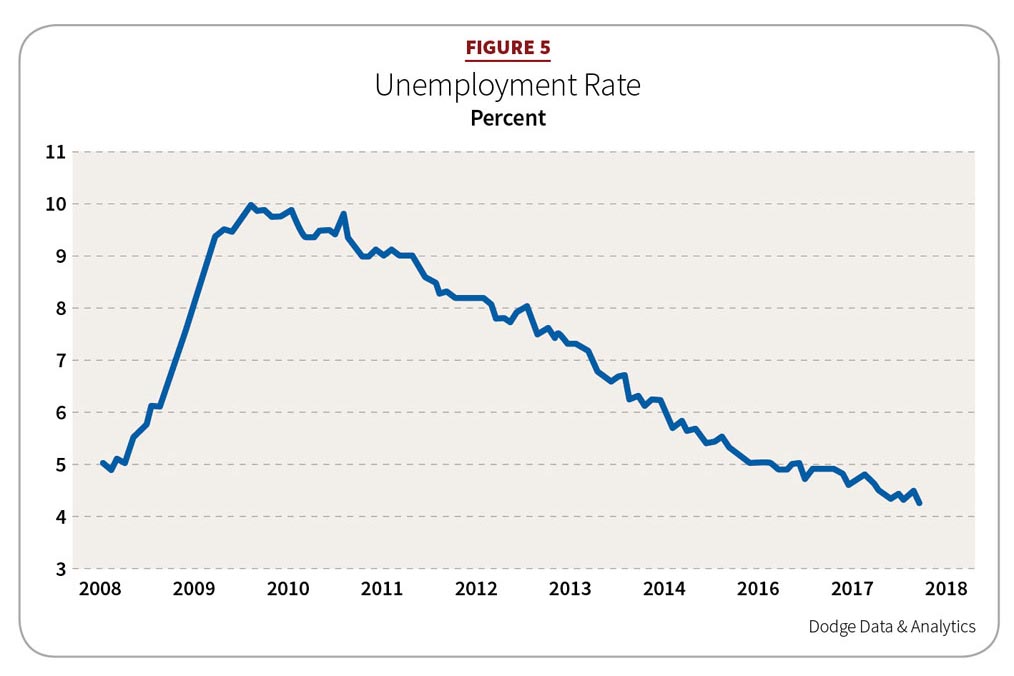

Though a skills mismatch is playing a role with 6.2 million unemployed, hires are up. Quit rates are up, too, a strong indicator of consumer confidence, especially among millennials who are leaving one job for a better one (see Figure 4). Overall, the unemployment rate is down (see Figure 5).

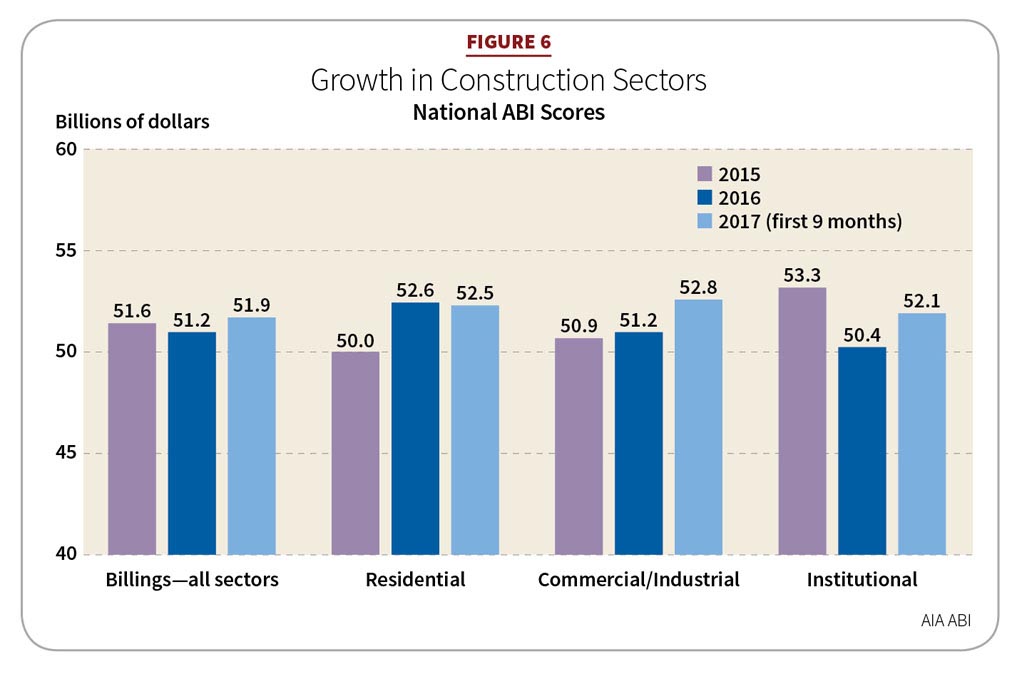

“Consumer confidence is helped by rising home value (home equity), which has lifted spirits,” deRitis said (see Figure 6). “There is demand for residential construction. Small business optimism has shot up after the election. Less regulations are also driving this feeling.”

The Employment Cost Index reported wages and salaries rose 2.6 percent from September 2016 to September 2017.

Lending has tightened across sectors, but it stood at just 15 percent of bank lending officers surveyed by the Federal Reserve in July 2017. The Mortgage Bankers Association reported commercial and multifamily mortgage loans increased 15 percent year-over-year during the first half of 2017.

In another area for optimism, deRitis pointed to a strong global economy.

“China and Asia are doing well,” he said. “No one is in a recession. Europe has seen 2 to 3 percent growth. China progress slowed but stood at 6.5 percent. Global performance lifts confidence in the U.S.”

Some clouds, but not overcast

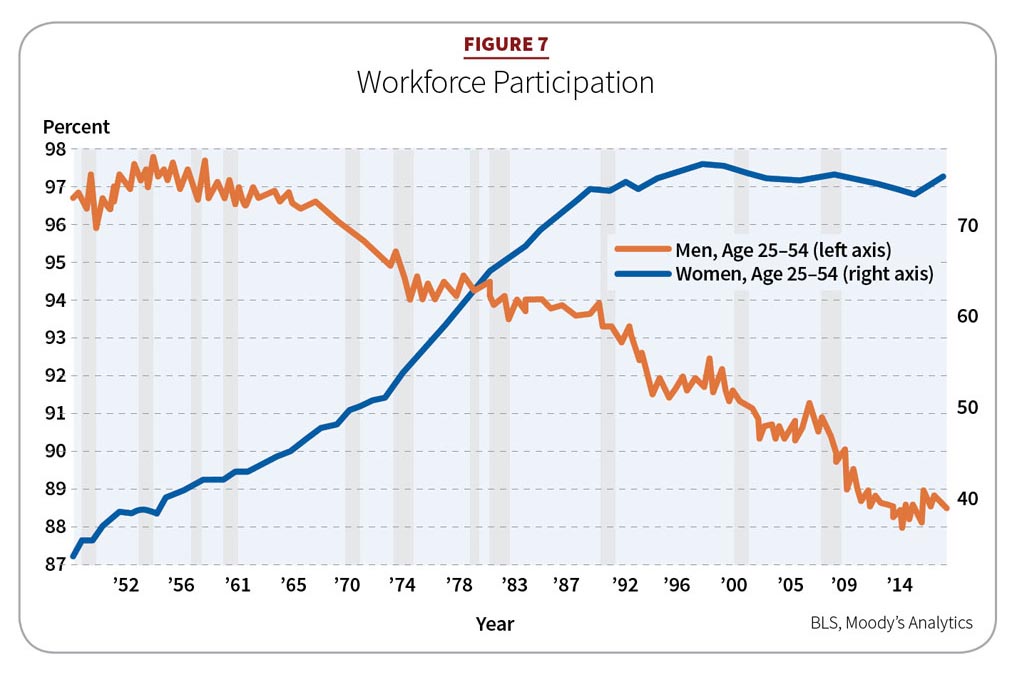

Today’s “what ifs” and risks shouldn’t derail the economy, but they are worth outlining. The declining participation of men in the labor force is one. It has steadily trended downward for men ages 25 to 54, deRitis said (see Figure 7). Also, there is a heavy reliance on younger and foreign workers.

“Men with or without a high school education may need new training to improve prospects,” he said.

Women in the same age range are actually a growing labor force. For the electrical contracting community and other trades, here is an opening for outreach to a potential workforce.

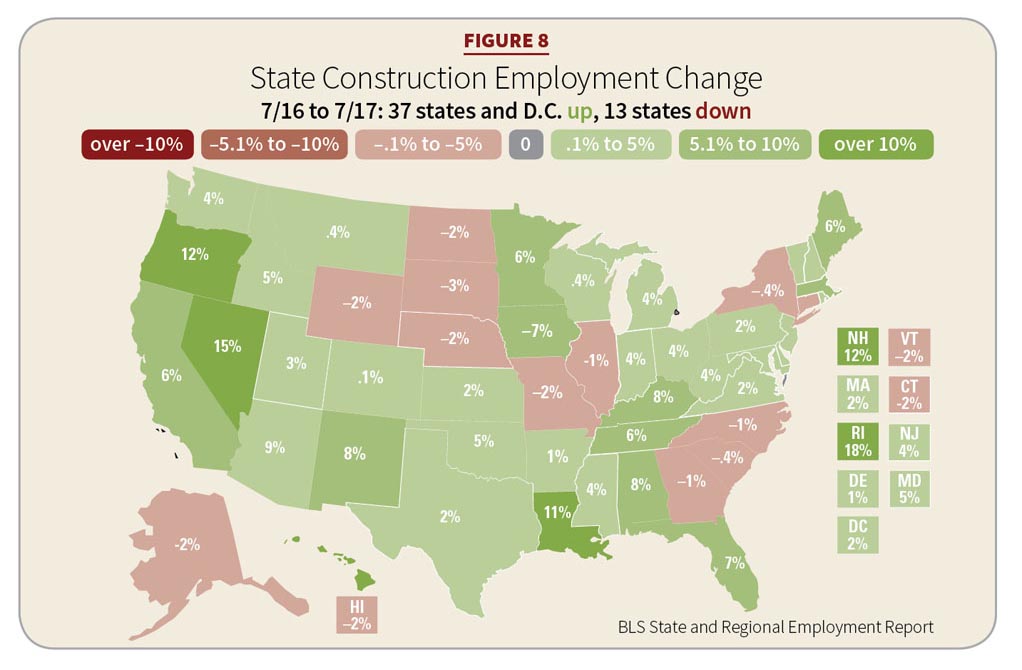

There was some tempered good news in 2017’s construction employment picture. The AGC reported 41 states added construction jobs between October 2016 and October 2017, while 26 states added construction jobs between September and October, continuing a pattern of widespread, but uneven, growth (see Figure 8). Construction employment in November rose to the highest level since November 2008. Employment totaled 6,955,000 in November, a gain of 24,000 for the month and 184,000, or 2.7 percent, over 12 months.

Ken Simonson, AGC chief economist, pointed out that the year-over-year growth rate in industry jobs was nearly twice the 1.4 percent rise in total nonfarm payroll employment.

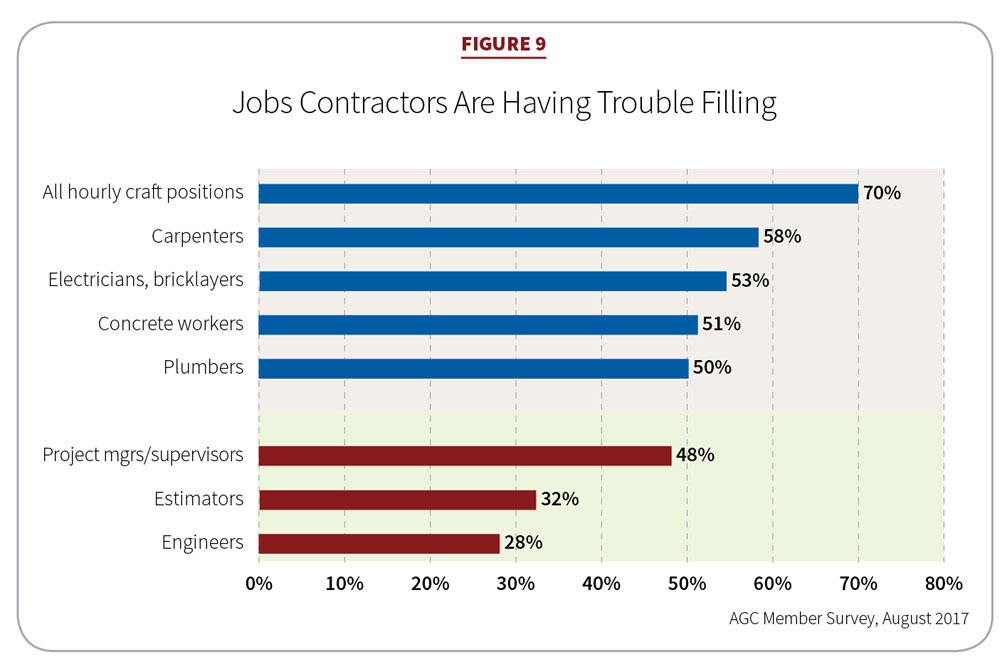

“Although construction employment has risen over the past year, many contractors report difficulty finding workers with the right skills,” he said. Employment totals would probably have been higher if workers were available (see Figure 9).

One persistent drag on the economy has been productivity. Steve Jones, senior director of Industry Insights research for Dodge, sees this issue to be particularly acute in the construction industry, and he shared statistics that reveal a struggle with project delivery.

An estimated 61 percent of typical construction projects were shown to be behind schedule, with half over budget. Even 20 percent of best-run projects were over budget and behind schedule. Embracing integrated project delivery, building information modeling (BIM) and new work-site technologies were examples of ways to shore up project delivery and compensate for persistent trained labor shortages.

In fact, Murray said, the skilled labor shortages may have a dampening effect on the construction market as many contractors face trouble filling jobs.

Moody’s economic model projects Federal Reserve fund rates rising quickly in 2018 but at low, modest levels—maybe 2 percent at best by year’s end. The Fed anticipates three rate hikes in 2018. In December 2017, it raised its benchmark lending rate by a quarter point to a target range of 1.25 percent to 1.5 percent.

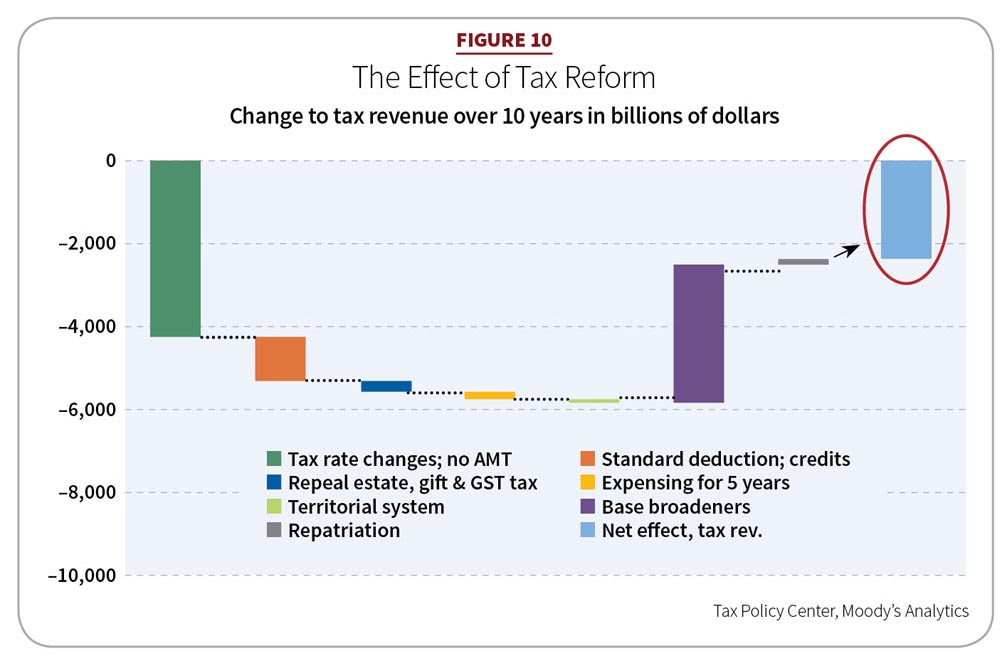

These rate hikes should not negatively affect the stock market, deRitis said. However, the Fed’s actions curbing inflation could slow growth going into 2019 and 2020. Action or inaction in Washington regarding infrastructure spending and tax reform could also impact the economy. The idea of an infrastructure bank has already taken a back seat to tax overhaul efforts. A tax rewrite could stimulate the economy and add to the deficit. The number of estimated deficit dollars created by a tax rewrite vary as of this writing; however, figures range in the trillions over 10 years (see Figure 10).

The impact of a deficit is perhaps overstated, according to deRitis.

“Global investors have been willing to buy our debt at 2 to 2.5 percent,” he said. “We can certainly pay off the interest. Right now, we are the gold standard as a safe haven. If investor mood changes, then U.S. deficits may be more problematic. I am more concerned with state and local government debt problems than federal.”

While potential geopolitical events could have an economic impact, deRitis felt it would likely by subdued based on U.S. job market strength and consumer confidence. Moves toward protectionism or trade barriers could be a threat bumping up against an integrated world economy.

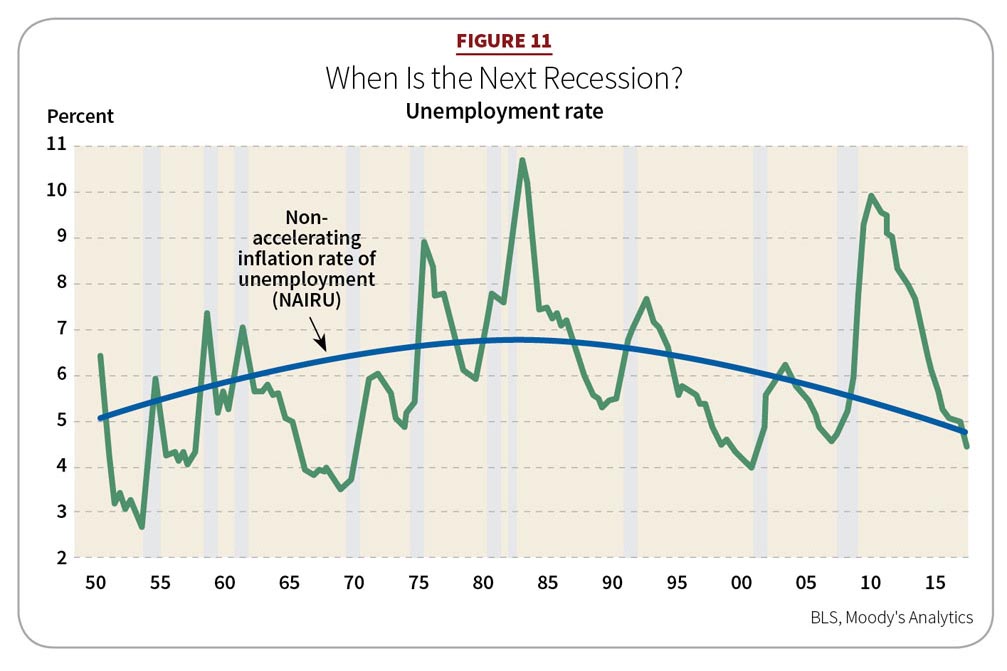

Finally, after an economic expansion comes the inevitable recession. But when should we expect it? Moody’s sees growth continuing over the next two years.

“Right now, it’s hard to identify a sector that is out of balance,” he said. “So, 2020 may be the best estimate. A sustainable employment rate that changes or interest rates rising too aggressively would serve as indicators. In 2020, if the Fed rate rises to 3.5 percent, it could expose the economy to a recession. That recession would be garden variety—maybe eight to nine months offering lesser GDP contraction or drop in employment” (see Figure 11).

The following sections cover sector performance and 2018 forecasts. They are based on Dodge Data & Analytics’ estimates unless otherwise stated.

RESIDENTIAL

A resurgent single-family housing grows, multifamily matures

Single-family housing growth will firmly surpass multifamily in 2018. The solid run for multifamily during this recovery has now matured and is trending down. Multifamily’s activity is anticipated to be roughly half or less than that of single-family.

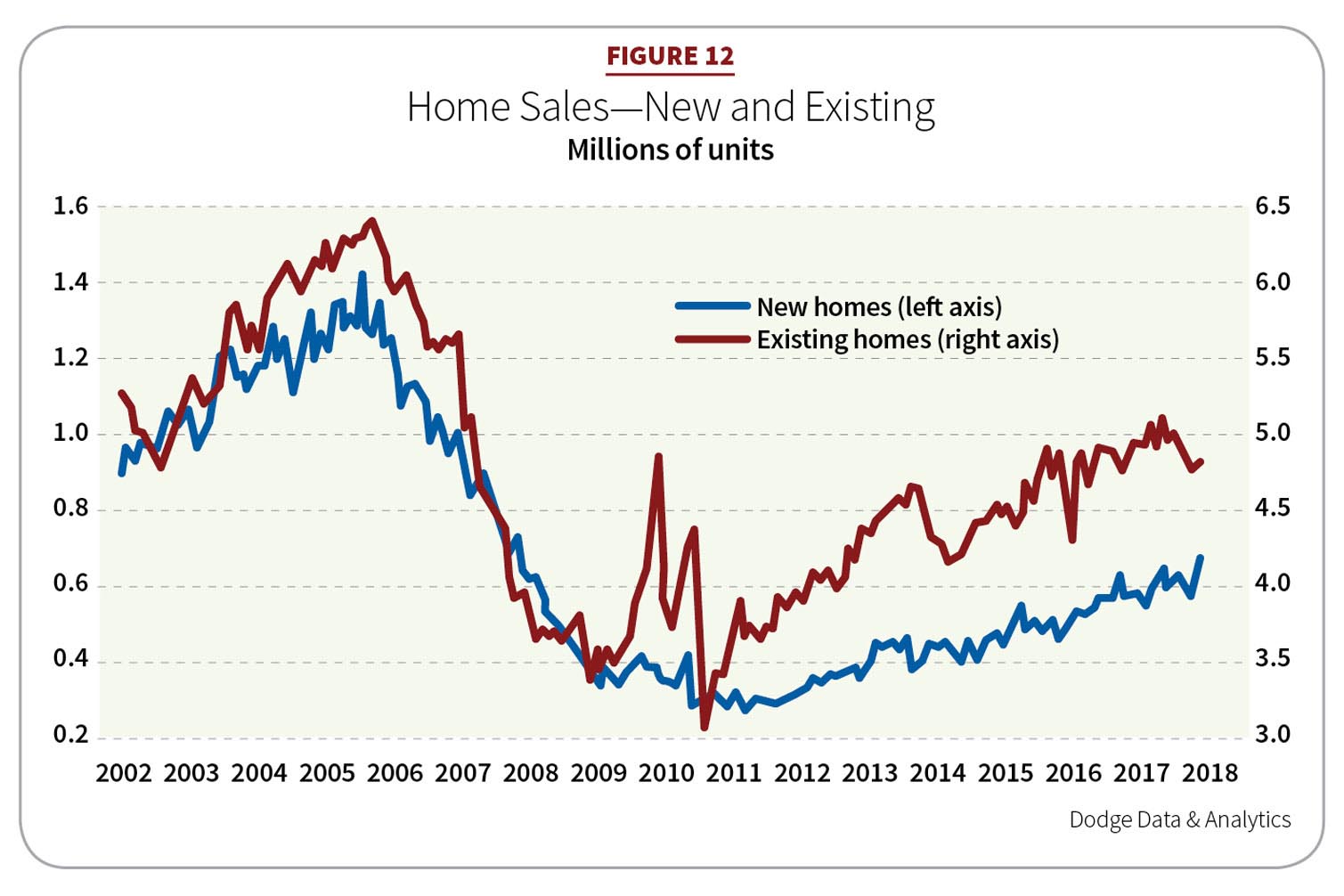

Home sales are volatile but trending up (see Figure 12). In 2017, total housing starts rose an estimated 2 percent (1.270 million units). This year, Dodge’s total residential starts is forecast to be essentially flat at 1.275 million units. Growth in square footage, having increased 5 percent for total residential in 2017, is expected to advance another 3 percent in 2018. Contract value stood at nearly $315 billion in 2017. This year, growth is forecast to be $322 billion. ConstructConnect assessed 2017 gains higher at 10 percent and 6.7 percent for 2018. Home prices are nearing the late 1990s peak.

Remodeling is also performing well. The National Association of Home Builders (NAHB) reports this residential subsector grew 6 percent in 2017 and is expected to add 3 percent in 2018. Energy-efficiency upgrades remain popular, as do aging-in-place modifications. Like the rest of residential, remodeling is constrained by tight housing inventory and labor shortages.

Single-family

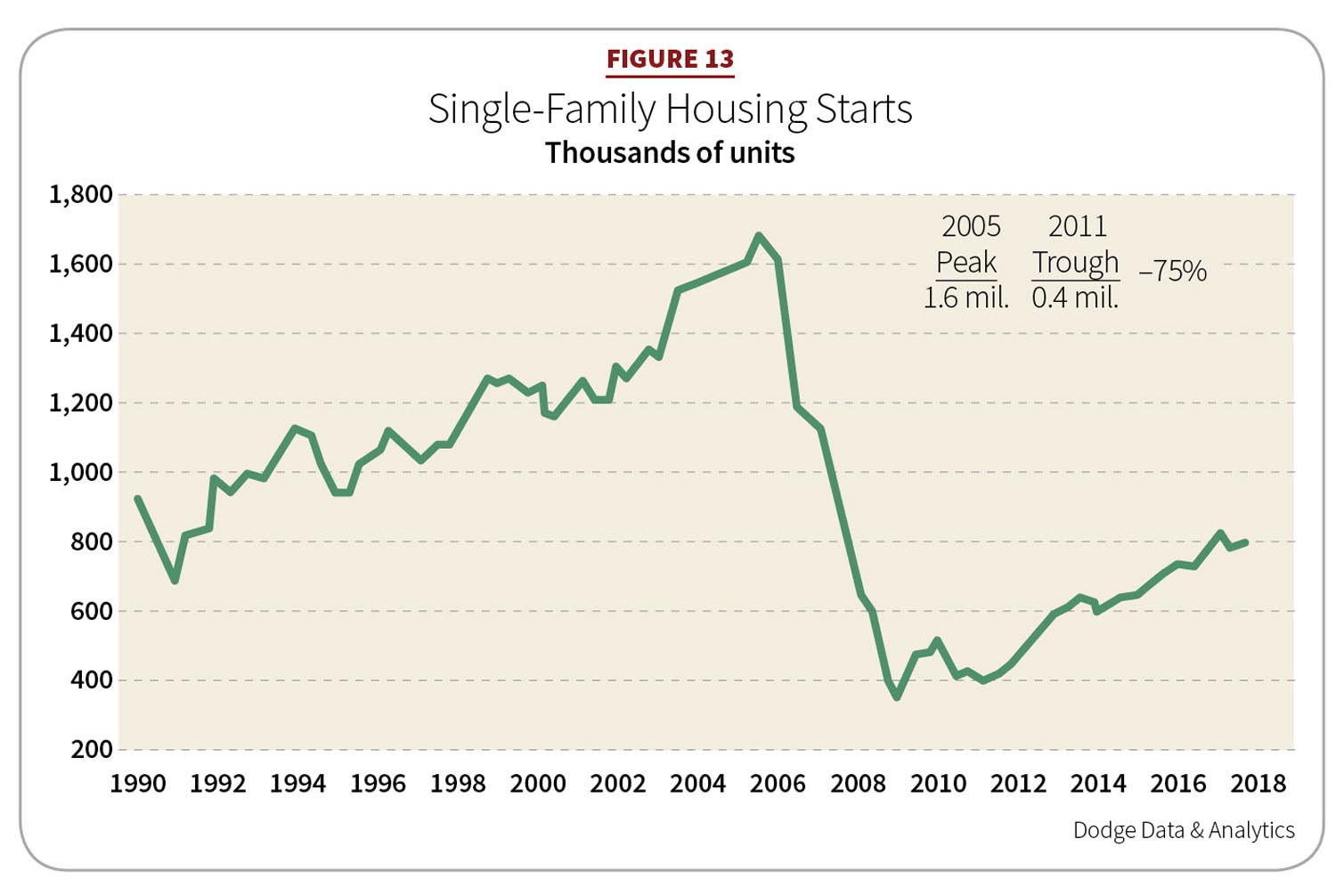

The recovery of single-family housing continues. In 2017, starts rose an estimated 8 percent, or 795,000 units. The NAHB estimates higher at 840,000 units (see Figure 13). Dodge forecasted a 9 percent contract dollars increase in 2017 of $219.8 billion. In 2018, advances will continue. Starts are expected to increase another 7 percent (850,000 units). The NAHB projects 930,000 units, putting it closer in line to ConstructConnect’s estimated 8.8 percent gain. This year, dollar values should climb 9 percent to $240.0 billion. Looking out to 2019, the NAHB predicts starts will break that important 1-million-unit threshold (1,075,500, a 13 percent increase).

Robert Dietz, chief economist, senior vice president, NAHB, said 2019 will bring this sector within 83 percent of “normal,” which constitutes 1.3 million single-family starts needed to meet population growth. NAHB builder confidence rose 2 points to a level of 70 in November 2017. This is the highest report since March of last year and the second-highest on record since July 2005.

Strong employment and home ownership interest by millennials in their 30s is helping drive gains. Rebuilding efforts in Texas and Florida after hurricanes Harvey and Irma may also stimulate activity in this sector with an estimated 10,000 new starts. However, the impact of the storms on 2018 construction spending remains elusive, because uninsured losses are difficult to ascertain, making repair/replace activity harder to forecast.

“A Housing and Urban Development [HUD] 2010 study looked at damage from Katrina,” Baker said. “Four-and-a-half years after the storm, 40 percent of housing was rebuilt and 30 percent were not. Storm damage repair is clearly a measure in years, not months.”

While the recession slowed down home formations, so did millennials, more than 35 percent of whom lived with their parents in 2015. This demographic represents the largest generation in history, surpassing post-World War II baby boomers. Between 2010 and 2015, Dodge estimates this group formed up to 7.6 million households. That number is expected to grow over a decade (2015–2025), adding 13.6 million households. The National Association of Realtors sees increasing numbers of millennial buyers in existing home sales. In addition, in the first eight months of 2017, new homes sales rose 7.4 percent over the same period in 2016.

Thirty-year fixed mortgage rates fell in 2017 from 4.17 percent in February to 3.81 percent in September. If rates rise, they will slowly rise from historically low levels so as to not impact the housing market in a major way. The NAHB estimates a fixed rate at 4.72 percent in 2018. This is the best news for homeowners, but the worst for first-time home buyers.

Multifamily

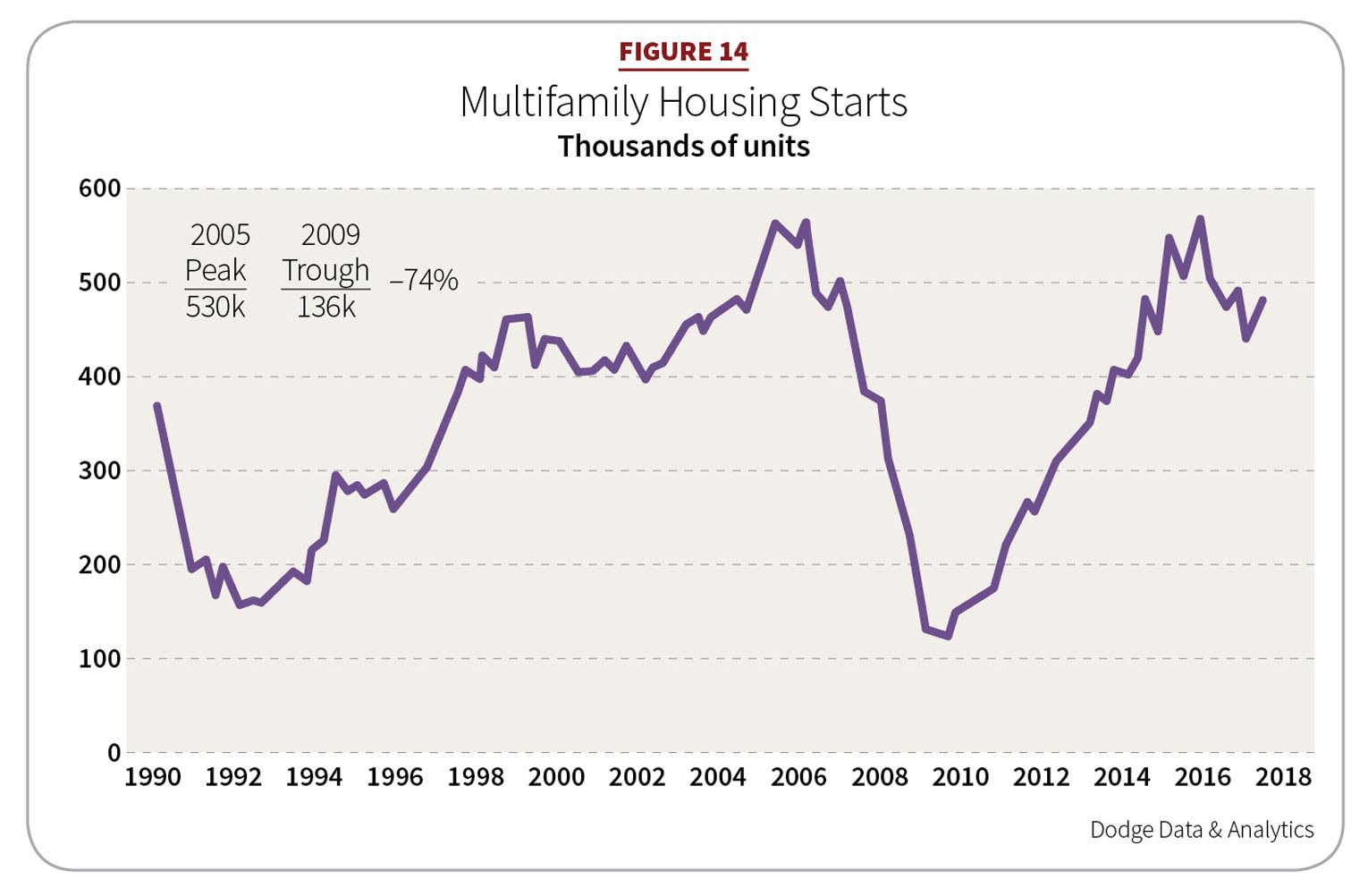

Multifamily housing has done a yeoman’s job in driving a residential housing recovery (see Figure 14). It is supported by both young adults and empty-nesters. Dodge reports multifamily starts jumped a whopping 266 percent in the years 2009 to 2015. Dollar values jumped 390 percent (largely due to luxury projects in New York City). By 2016, starts dropped to 2 percent. Last year, starts lost another 7 percent to 475,000 units and 6 percent in dollar value ($89.1 billion). ConstructConnect puts total dollar growth at 11 percent for 2017. In 2018, expect starts to drop 11 percent to 425,000 units and 8 percent in dollars ($82.1 billion). That is a total dollar growth of 2.1 percent, according to ConstructConnect.

The role of large-scale projects weighs heavily on the fortunes of the multifamily sector. In the first nine months of 2017, projects valued at $100 million or more represented 20 percent of this sector’s starts and 8 percent of units. The top three largest multifamily projects in the first nine months of 2017 were the One Grant Park high-rise in Chicago ($615 million), the Wall Street Tower multifamily high-rise in New York ($450 million), and the City Point Apartment Building in Brooklyn, N.Y. ($423 million).

COMMERCIAL

Smaller gains

A 21 percent jump in commercial construction in 2016 slowed in 2017. Small, but positive, last year saw a 3 percent dollar gain ($115 billion). Square footage advances came close to 2016’s 10 percent advance but fell to 1 percent (723 million square feet [msf]) in 2017. This year, growth is forecast at 2 percent ($117. 3 billion) and 725 msf. ConstructConnect saw 2017 as a dollar loss of 5.8 percent but sees greater gains in 2018 of 3.2 percent.

Offices

Office construction in downtown markets helps buoy this sector. In 2017, office construction grew 11 percent both in square footage (137 msf) and contract value ($44.3 billion). In 2018, numbers are forecast for a 6 percent gain (145 msf) and a rise in contract value estimated at 5 percent ($46.7 billion). ConstructConnect estimates 2017 starts lower at $25.3 billion and anticipates 2018 at $28 billion.

Recent office expansions have largely been high-rise projects. In 2017, an estimated 40 percent of the new office square footage involved projects of six or more stories. The New York metropolitan region still accounts for 16 percent of all U.S. starts, though activity fell an some 32 percent ($4.5 billion) in the first nine months of 2017. Activity in San Francisco soared 159 percent, placing it second to New York. This market may be peaking; other big performing cities saw fewer starts in 2017. Washington, D.C., was down 9 percent, with Dallas dropping 21 percent and Atlanta 8 percent.

Data centers have been a driver for this sector. Dodge reports, from 2014 to 2016, such projects cumulatively averaged more than $3 billion each year. During the first six months of 2017, starts stood at $2.2 billion largely due to two Facebook data centers valued at $800 million combined. That company is in the midst of additional projects, as is Google. Colocation—where a third-party data center hosts multiple companies’ servers—also is becoming common.

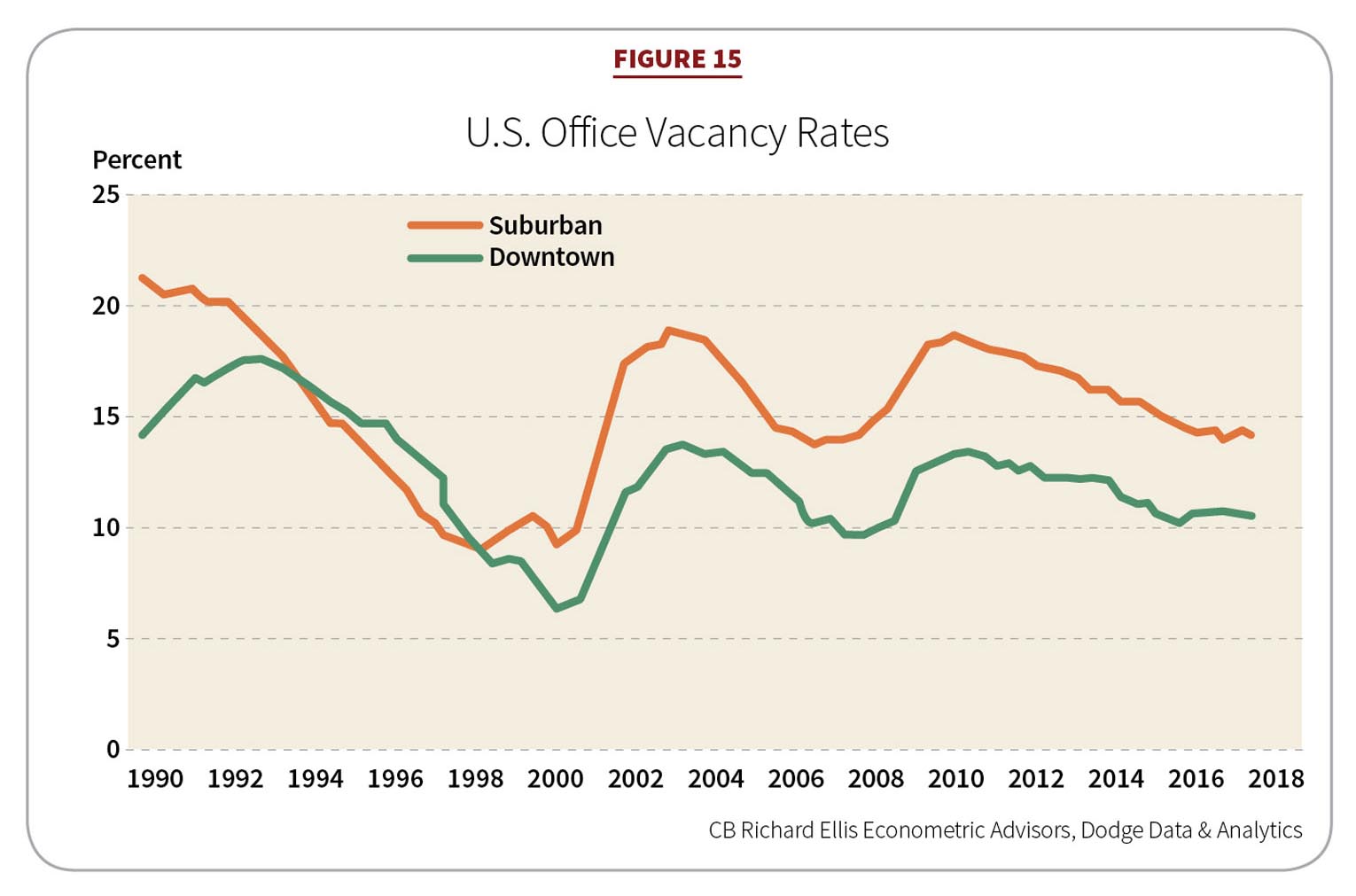

Finally, stabilizing vacancy rates are helping support this market. The CB Richard Ellis Econometric Advisors (CBRE-EA) reported a rate of 13 percent for the first half of 2017 and 12.9 percent in the third quarter. Of the 63 markets the CBRE-EA covers, the firm saw third-quarter-2017 vacancy rates fall in 38 of its markets, rise in 20, and remain unchanged in 5. Downtown vacancy rates stood at 10.6 percent, and suburban vacancy rates were 14.1 percent, which is a more gradual manner than prior expansions (see Figure 15).

The top three projects for 2017 were 50 Hudson Yards office tower ($1.7 billion) in New York City, the office portion ($780 million) of the $1.3 billion Oceanwide Center Tower complex in San Francisco, and the LG headquarters complex ($300 million) in Englewood Cliffs, N.J.

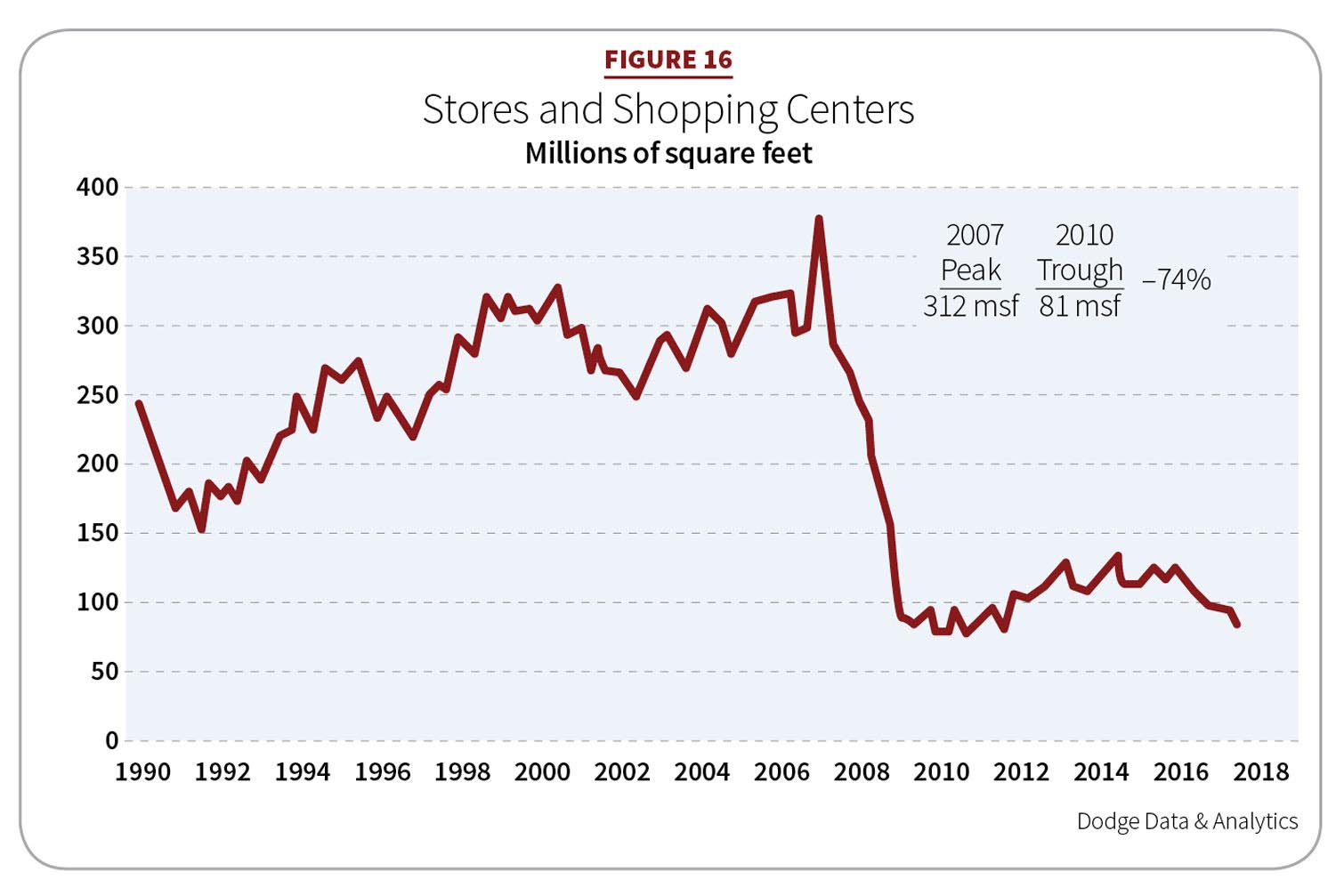

Stores and shopping centers

Stores and shopping centers largely missed recovery and expansion. Last year, starts in this sector withdrew an estimated 16 percent (92 msf) (see Figure 16). Dollar values were expected to retreat 10 percent ($18.4 billion). ConstructConnect forecasted this sector contracting severely to 49.2 percent, seeing a lack of brick-and-mortar more acutely.

In 2018 will show some improvement. Starts will grow 1 percent (93 msf) and gain 3 percent ($19.0 billion). ConstructConnect sees an improvement in dollar value, but still a 4.5 percent contraction.

While consumer confidence has returned, the sector’s continued weakness is due in part to the structural changes of online shopping. By second quarter 2017, e-commerce sales were up 16 percent ($111.5 billion) from a year earlier. Online shopping represented 8.9 percent of total retail sales, nearly a percentage point higher from the previous year. Though such numbers seem smaller when set against the entire retail industry, capital investment is being directed toward digital shopping. Walmart is a prime example. In 2015, its $1.3 billion brick-and-mortar construction represented an 18 percent decline. In 2017, it was $1.0 billion. Walmart is engaged in a three-year strategy to strengthen its U.S. and e-commerce businesses and compete with Amazon.

The top three projects for 2017 were the SoNo Collection Shopping Center Shell ($200 million) in Norwalk, Conn.; the $143 million retail portion of the $900 million Seminole Hard Rock Hotel and Casino in Hollywood, Fla.; and the Dania Point Retail and Entertainment Complex in Dania Beach, Fla. ($109 million).

Warehouses

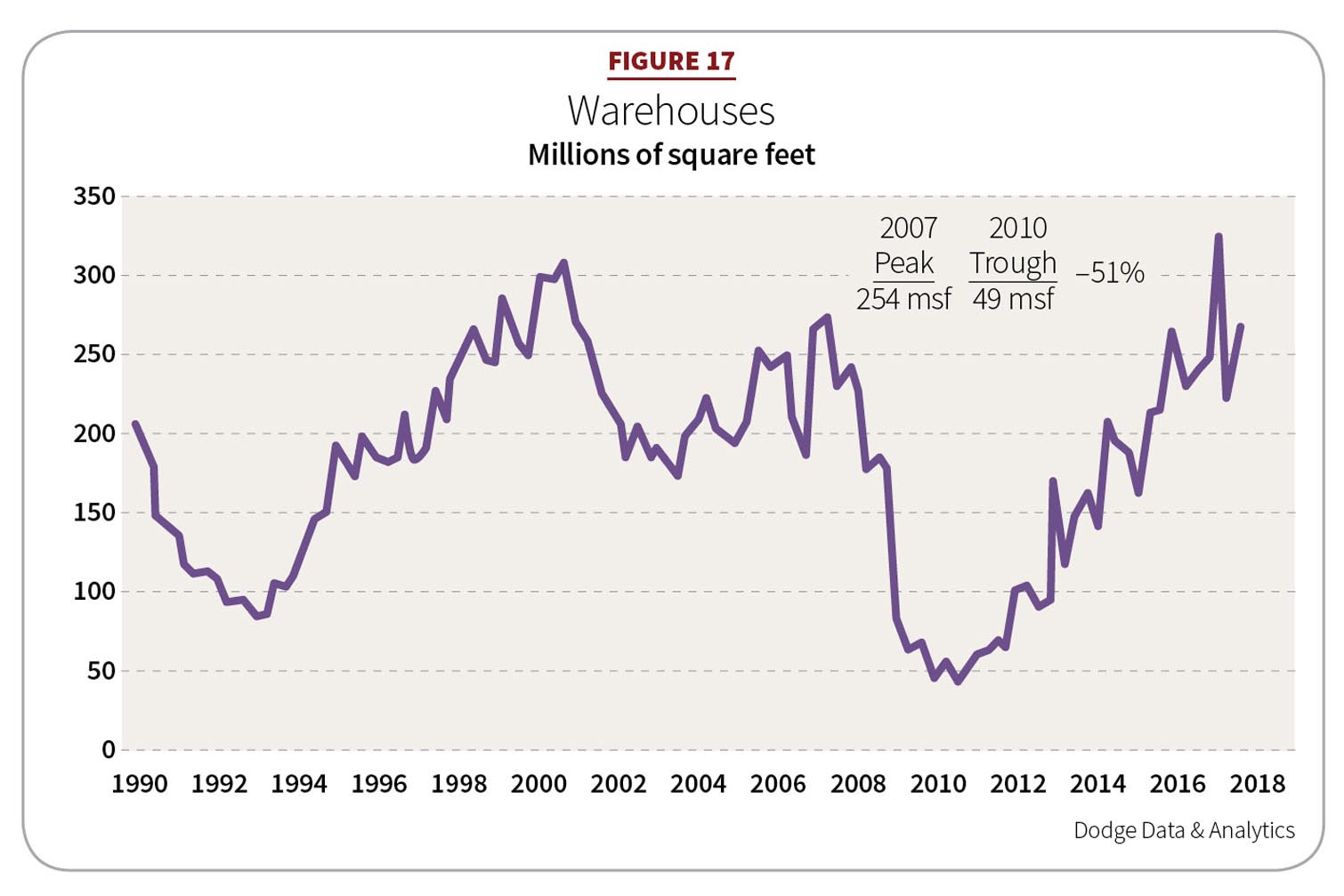

Warehouse construction has been supported by greater e-commerce demand, which has outpaced supply. Vacancy rates were 7.7 percent in the third quarter of 2017. Total square footage in 2017 rose an estimated 9 percent and is projected to increase another 2 percent in 2018, reaching 265 msf (see Figure 17). Contract dollars in 2017 also rose 9 percent and will add another 4 percent this year to reach $21.6 billion. ConstructConnect estimates a robust 21.7 percent dollar gain in 2017.

In 2016, 25 warehouses of more than 1 msf broke ground. In the first nine months of 2017, 31 more projects joined the club (41 msf). Warehouse construction is expected to be nearing its peak, but Murray said there is a continued need for updated facilities to handle improved inventory management practices.

A growth segment to watch for is online grocery shopping. The Food Marketing Institute and Nielsen reported that, by 2025, the share of online grocery spending could reach 20 percent, representing $100 billion in annual consumer sales.

The largest projects in 2017 included two Walmart distribution centers (3.0 msf and 2.5 msf) in Mobile, Ala.; a UPS Majestic Logistics Center (2.8 msf) in Atlanta; and the Northport Commerce Center (1.7 msf) in the Savannah, Ga., area.

Hotels

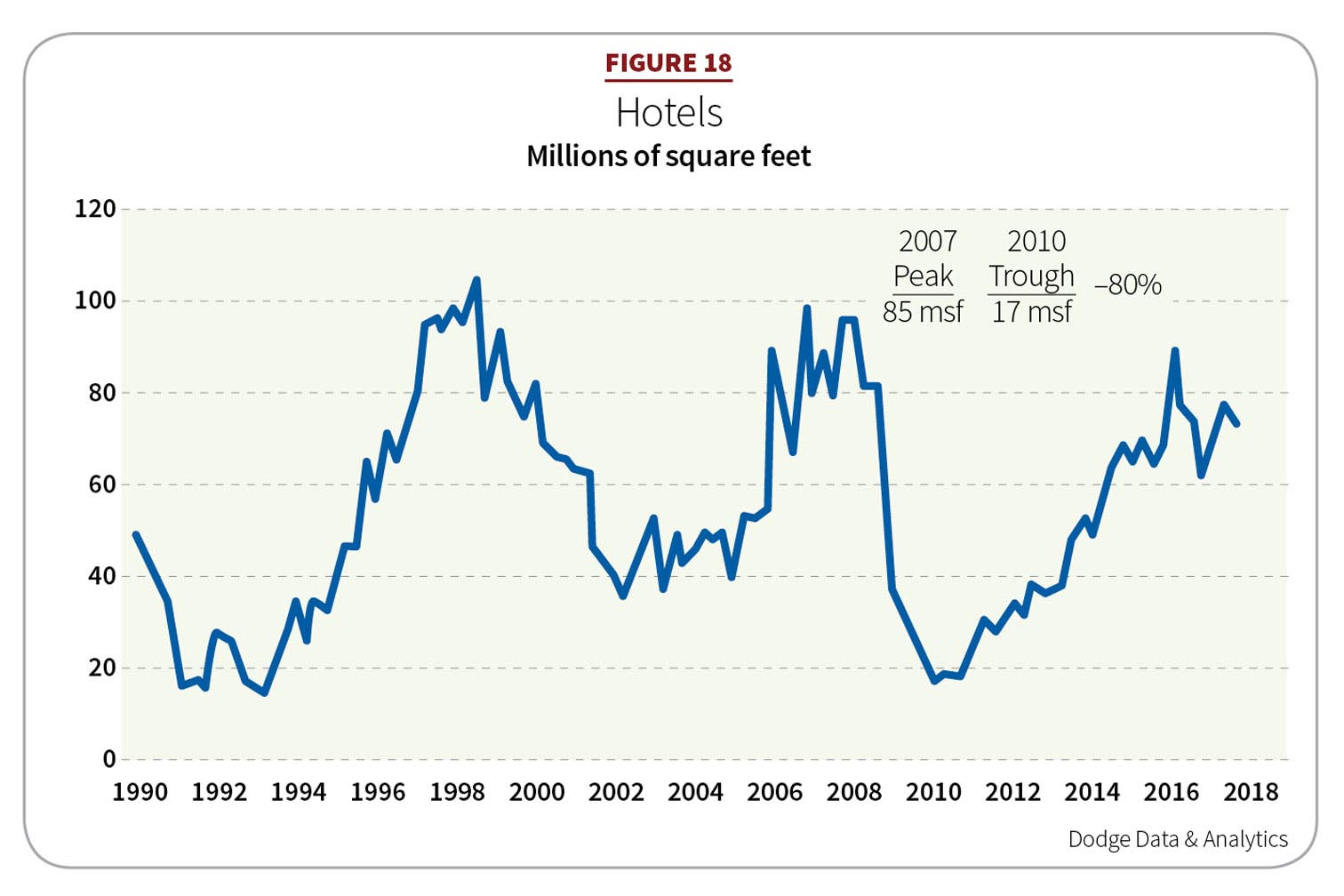

Hotel construction is softening from its 2016 peak. There was an estimated 4 percent contraction in both square footage and contract value (72 msf/$16.6 billion) in 2017 (see Figure 18). ConstructConnect estimated $18.4 billion. A steeper decline is forecast in 2018 of 7 percent (67 msf) and 4 percent ($15.9 billion). ConstructConnect is less severe, anticipating a contraction of 1.9 percent in dollar value in 2018.

Stimulating construction and renovation in this sector has been a large demand for business meetings and conventions as well as strong leisure travel. Connected to that is legalized gambling that has resulted in Native-American-owned casinos in 30 states and another 20 allowing commercially owned casinos. In the first nine months of 2017, 15 hotel projects valued at $100 million or more broke ground—five hotel/casinos and two convention centers.

The CBRE-EA reported that occupancy rates in the second quarter of 2017 gained 30 points, a stabilizing rebound but tempered with an unremarkable revenue per available room gain of 2.7 percent.

The top three projects of 2017 were the hotel portion ($575 million) of the $900 million Seminole Hard Rock Hotel and Casino expansion in Hollywood, Fla.; the hotel portion ($342 million) of the $500 million Resorts World Hotel and Casino in Las Vegas; and the Hyatt Hotel ($224 million) at the Oregon Convention Center in Portland, Ore.

INSTITUTIONAL

Strong 2017, positive 2018

The institutional building market grew noticeably stronger in 2017, gaining an estimated 5 percent in footage (327 msf) and a strong 14 percent advance in dollar value ($135 billion). Staying positive in 2018, gains in square footage should land at 5 percent (342 msf) and dollars advancing 3 percent ($139.2 billion). Construction in education, healthcare and transportation-terminal projects will continue to offer opportunities.

Education

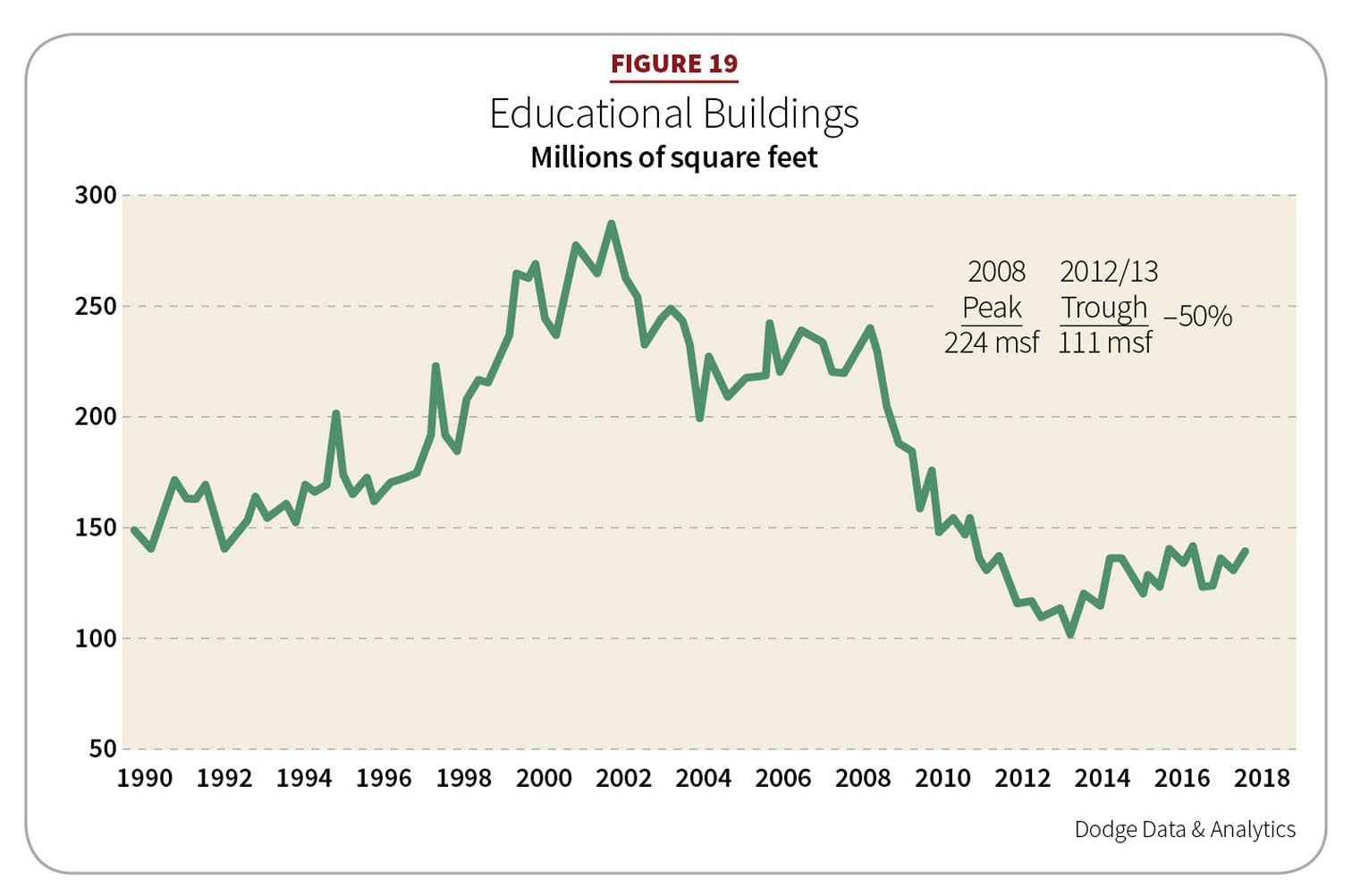

This sector should see more substantial growth next year thanks to recent school construction bond measures. In 2017, it gained 3 percent (133 msf) over 2016. Expect an added 8 percent (144 msf) in 2018. In terms of contract dollars, 2017 saw a healthy 7 percent ($54.4 billion) bump over 2016 (see Figure 19). ConstructConnect estimated 2017 dollars advancing higher at 10 percent. This year, education construction should see even stronger growth at 11 percent ($60.3 billion). ConstructConnect places growth a bit lower at 6.5 percent.

The state and local funding picture, while improved, remains mixed. Many states still face sluggish revenue growth. The National Association of State Budget Officers’ “Spring 2017 Fiscal Survey of States” found general fund revenues grew 2.5 percent in 2017 but were down from 5.0 percent in 2015. Weaker performance forced 23 states to make midyear budget cuts for fiscal 2017. States are forecasting 3.1 percent revenue growth in 2018 but fund expenditures rising only 1 percent, the slowest rate since 2010.

Reported in last year’s outlook, a number of substantial bond measures passed in 2016 that will play out in subsequent years. Examples included California’s Proposition 51 ($9 billion bond for K–12 and community college new construction and renovation) and measures in the Texas cities of El Paso, San Antonio, Pearland and Corpus Christi, totaling $1.5 billion. In 2017, approved bonds included $790 million in Portland, Ore., to modernize schools; $737 million for the Lewisville, Texas, Independent School District; and $250 million to build an Early Learning Center and rebuild three schools in Shoreline, Wash.

Meanwhile, billion-dollar-plus funding for long-term public-school construction and renovation projects was announced for Boston, Chicago and Philadelphia.

Investments in rehabbing existing K–12 structures will also help fuel education construction. The American Society of Civil Engineers estimates a $38 billion gap between necessary yet actual investment in public school facilities. It projected more than 53 percent of schools in need of renovation will require significant upgrading.

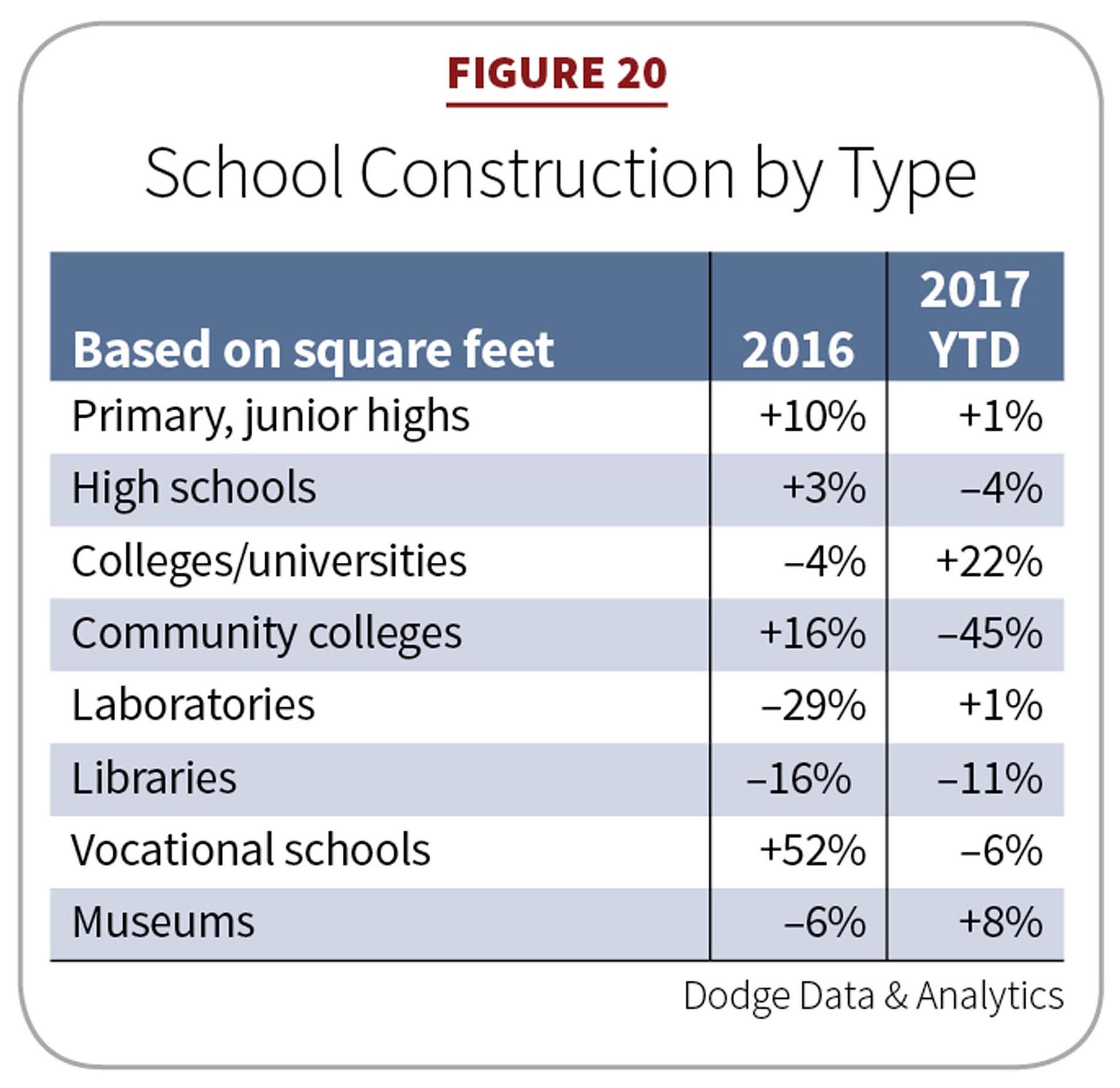

The construction picture is looking up for colleges and universities. In 2017, construction starts were up 22 percent in square feet and 20 percent in dollars, which helped steady weaker performance for K–12 school construction. College and university construction momentum should continue this year, contributing growth in the education building sector (see Figure 20). An improving picture for endowments also should help.

Top education construction projects in 2017 included the John A. Paulson School of Engineering and Applied Sciences ($327 million) at Harvard University in Cambridge, Mass.; the Chem-H building at Stanford University ($252 million) in Palo Alto, Calif.; and the Zipper Building ($218 million), New York University’s Greenwich Village expansion.

Healthcare

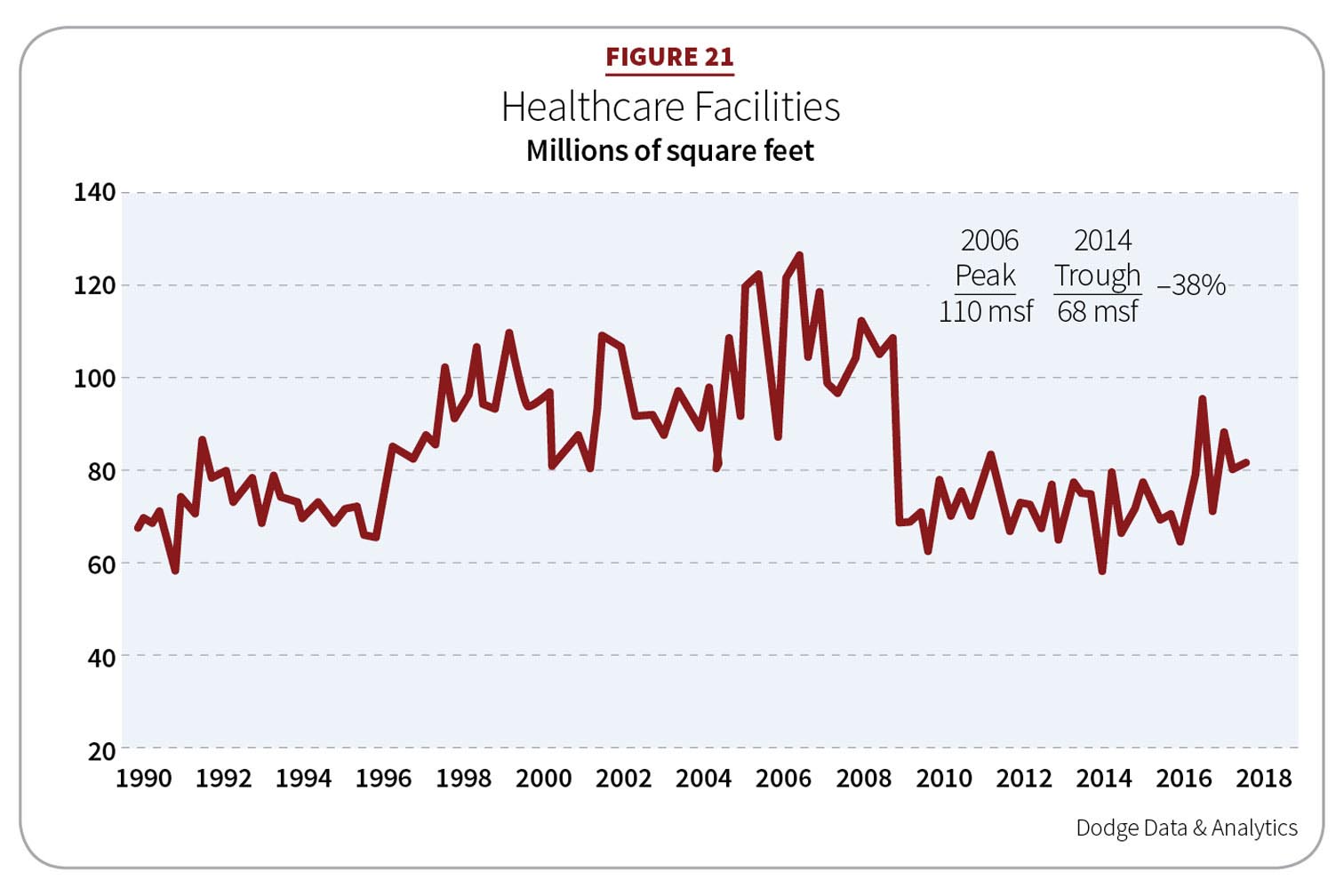

Healthcare facilities in 2017 made progress with several large hospital projects. Last year saw a 7 percent gain (81 msf) over 2016. That was a breakthrough after seven years of square footage gains of less than 76 msf. Contract value rose 5 percent ($27.2 million). This year, footage will retreat 1 percent (80 msf) but add 2 percent in dollars ($27.7 million) (see Figure 21).

While pent-up demand might have helped this struggling sector, the doubt about the future of the Affordable Care Act dampened advances. Adding to the uncertainty were possible healthcare mergers and the growth of store-front clinics. Potential for this market is strong because nearly 28 percent of the U.S. population is older than 55. The number will grow as baby boomers age.

By the end of September 2017, 36 healthcare projects broke ground valued at $100 million or more. These included the Penn Medicine Patient Pavilion ($1.4 billion) in Philadelphia, a $550 million medical center in St. Louis, and the Marcus Tower ($465 million) at Piedmont Hospital in Atlanta.

Transportation

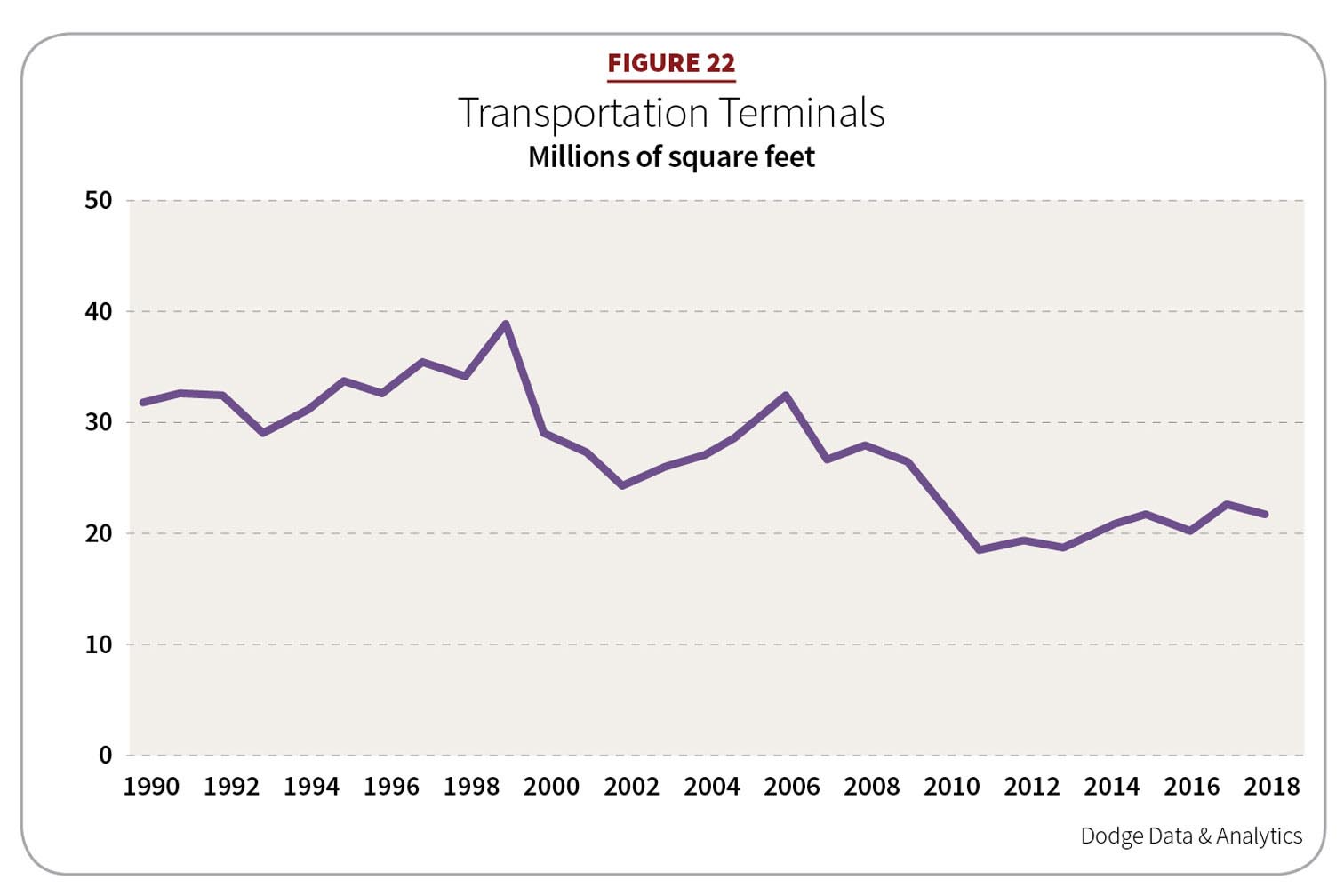

Dodge reports transportation-terminal starts were the “highlight of the institutional building sector” in 2017. Building off healthy gains in 2016, square footage in this market grew 13 percent (22.3 msf) and dollars surged 120 percent ($20.6 billion) (see Figure 22). ConstructConnect estimates $27.4 billion. In 2018, this sector will contract 4 percent (21.5 msf) with a dollar value gain of 23 percent ($15.8 billion).

The top three projects last year were the new Delta Airlines terminal facility ($4 billion) at LaGuardia Airport in Queens, N.Y., in addition to the airport’s Central Terminal Building project ($3.4 billion); the Delta relocation to Terminals 2 and 3 ($1.9 billion) at Los Angeles International Airport; and the South Terminal C project at Orlando (Fla.) International Airport ($1.2 billion).

Amusement

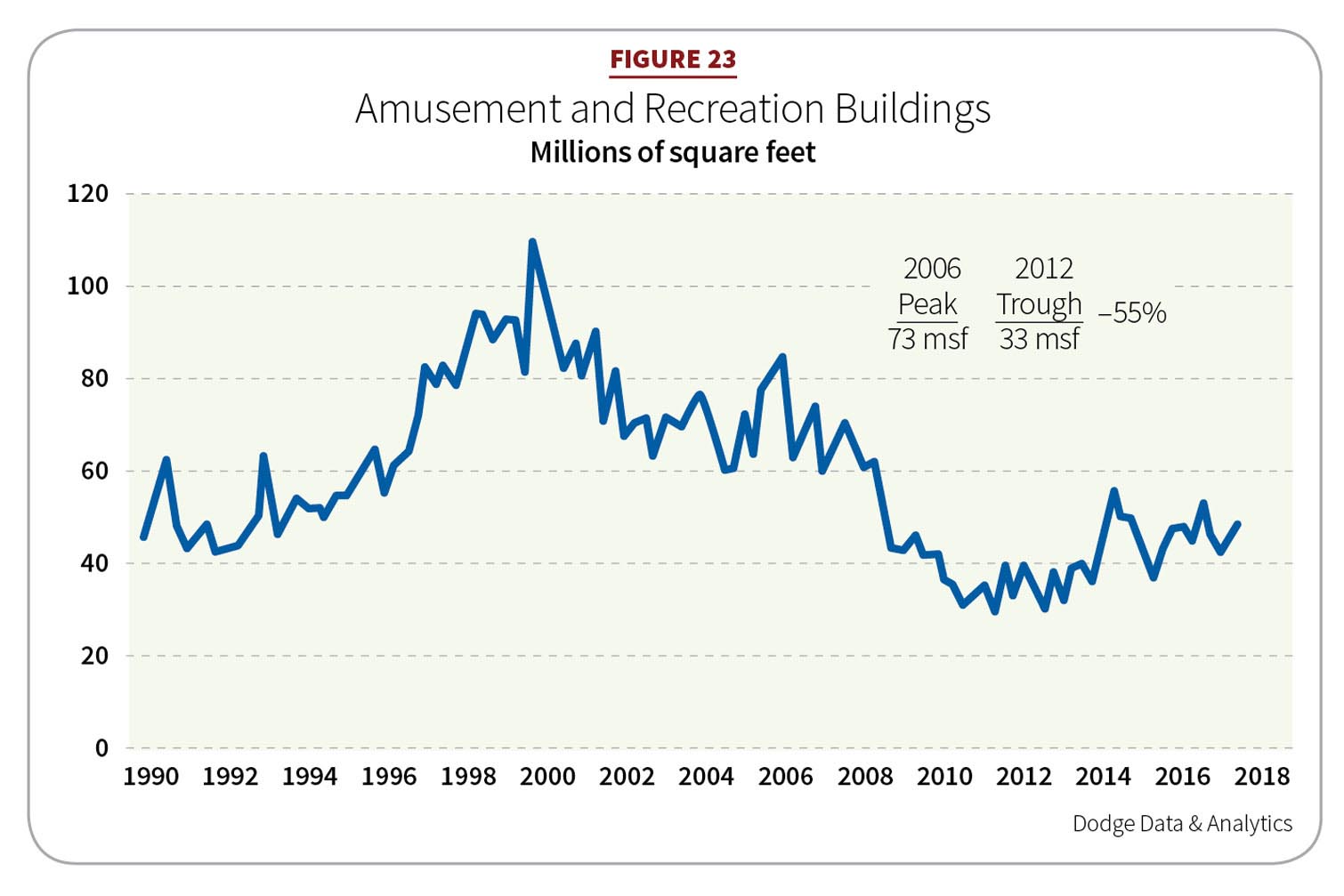

After a drop in 2017 of 1 percent (46 msf) and a dollar value contraction of 3 percent ($17.4 billion), expect a rebound in 2018 of the amusement sector, with 5 percent growth (48 msf) and a 6 percent dollar gain ($18.5 billion) (see Figure 23). Notable 2017 projects were the Javits Convention Center expansion ($1.2 billion) in New York; the arena portion ($562 million) of the future Golden State Warriors home at the $1 billion Chase Center complex in San Francisco; and the Dickies Arena ($390 million) in Fort Worth, Texas.

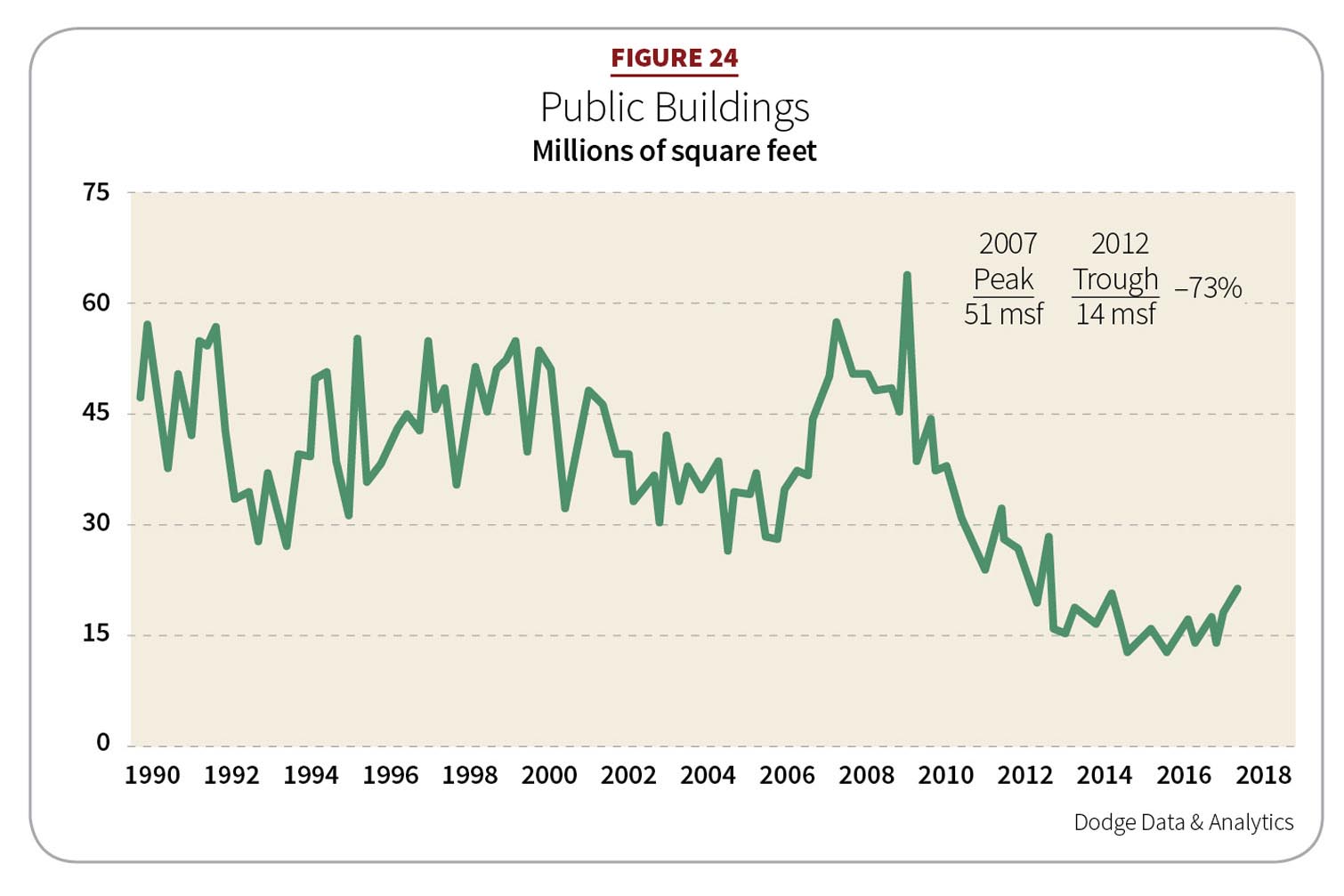

Public buildings

After 10 years of volatility representing capitols and courthouses, police and fire stations, and detention and other public administration facilities, this sector is showing needed growth. Square footage doubled in 2017 estimated at 14 percent (17.3 msf) (see Figure 24). This year, starts should add another 3 percent (17.9 msf). Dollar values in 2017 of $8.4 billion will advance to $9 billion in 2018.

Almost half of the public building starts in 2017 were police and fire stations. In the first nine months of 2017, 504 police and fire stations, 352 capitals and courthouses, 159 armories, 110 detention centers, and nine post offices broke ground.

The top three projects were the Multnomah County Central Courthouse ($210 million) in Portland, Ore.; the Orange County Civic Center/Building 16 ($125 million) in Santa Ana, Calif.; and the Inmate Intake Transfer & Release/Detention Facility ($125 million) in Phoenix.

Religious

Religious building construction turned a corner in 2017. Starts rose 3 percent (9.1 msf), and dollar values rose 10 percent ($1.9 billion). This year, the market will further strengthen, with an anticipated 10 percent gain in footage (10 msf) and an added 9 percent in dollars ($2 billion). According to Giving USA, religious contributions in 2016 increased 3 percent or an estimated $122.94 billion across all faiths. Figures for 2017 were not available as of this writing.

MANUFACTURING

Coming off a strong year

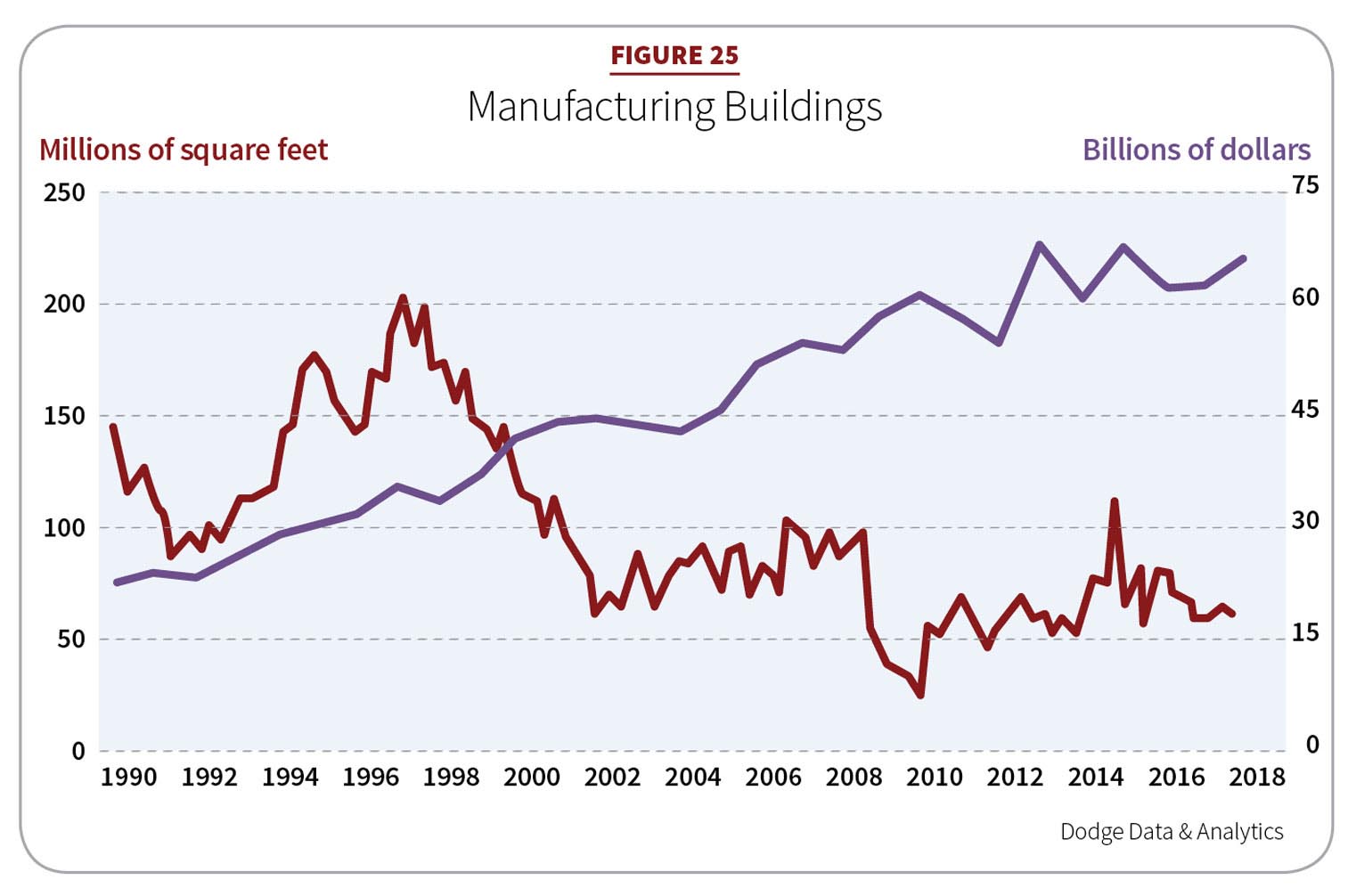

While manufacturing plant construction in 2018 may recede 1 percent ($25.1 billion), that’s not bad after a healthy 27 percent ($25.4 billion) gain last year due to a number of substantial petrochemical projects. Square footage retreated an estimated 9 percent (62 msf) but is expected to rise 6 percent (66 msf) this year (see Figure 25).

An important headwind to this sector is capacity utilization, which is lower than the 80 percent level needed for companies to comfortably expand manufacturing facilities. It appears incentives for manufacturers to maintain production stateside, improving exports, and the easing of the U.S. dollar have helped this sector. Stable oil prices (averaging $50 per barrel) are aiding energy-related project investment. Other help will come from auto manufacturers such as Toyota and Mazda’s planned joint $1.6 billion U.S. assembly plant, Foxconn’s flat-panel LCD monitor plant in Wisconsin, and LG’s $25 million manufacturing facility in Michigan for electric car battery packs.

Top energy projects in the first nine months of 2017 included an ethane cracker facility ($6 billion) in Monaca, Penn.; a methanol plant ($1.8; billion) in Vacherie, La.; and a polyethylene plant ($1.1 billion) in Beaumont, Texas. Large nonenergy-related projects included three pharmaceutical facilities, three lumber/wood/paper plants, a biotech plant, and a Mercedes-Benz van manufacturing plant.

PUBLIC WORKS

Further progress

Public works construction has been volatile for a number of years, finally stabilizing a bit in 2016 with strong pipeline activity. Last year, public works saw a 1 percent gain ($130.1 billion). In 2018, advances are expected to further rise to 3 percent ($133.3 billion). If an infrastructure program emerges this year with some shovel-ready projects, this sector might see an additional boost extending into 2019.

Highways and bridges

For 2017, this sector stabilized ($61.5 billion). This year, construction should see 5 percent growth ($64.8 billion), supported by state and local bonds and federal 2017 appropriations (Oct. 2017–Oct. 2018). Federal funding, as authorized by the 2015 Fixing America’s Surface Transportation (FAST) Act, will help promote growth, too. It authorized $230 billion for highways over a five-year period. The 2018 appropriations budget is facing congressional resolutions that could negatively affect highway funding mechanisms. That said, ConstructConnect is more bullish, estimating a 16.1 percent gain for 2018.

All 50 states received additional funding in 2017 as the result of unused highway funding totaling $3.1 billion supplied by the Federal Highway Administration.

Noteworthy projects in 2017 included the I-395 High-Occupancy Toll Lanes project ($460 million) in Alexandria, Va.; the I-285 Interchange project ($457 million) in the Atlanta area; and a renovation project ($452 million) on the George Washington Bridge in New York City.

Environmental

Though 2017 federal appropriations provide funding for environmental public works, they didn’t come early enough to have a positive effect. As such, this sector saw an estimated 11 percent drop to $29.6 billion. Funding for reconstruction efforts related to hurricanes Harvey and Irma could improve activity in this sector, as could funding support in the current federal appropriations bill. The forecast for 2018 is stronger, with a 9 percent rise ($32.3 billion) expected.

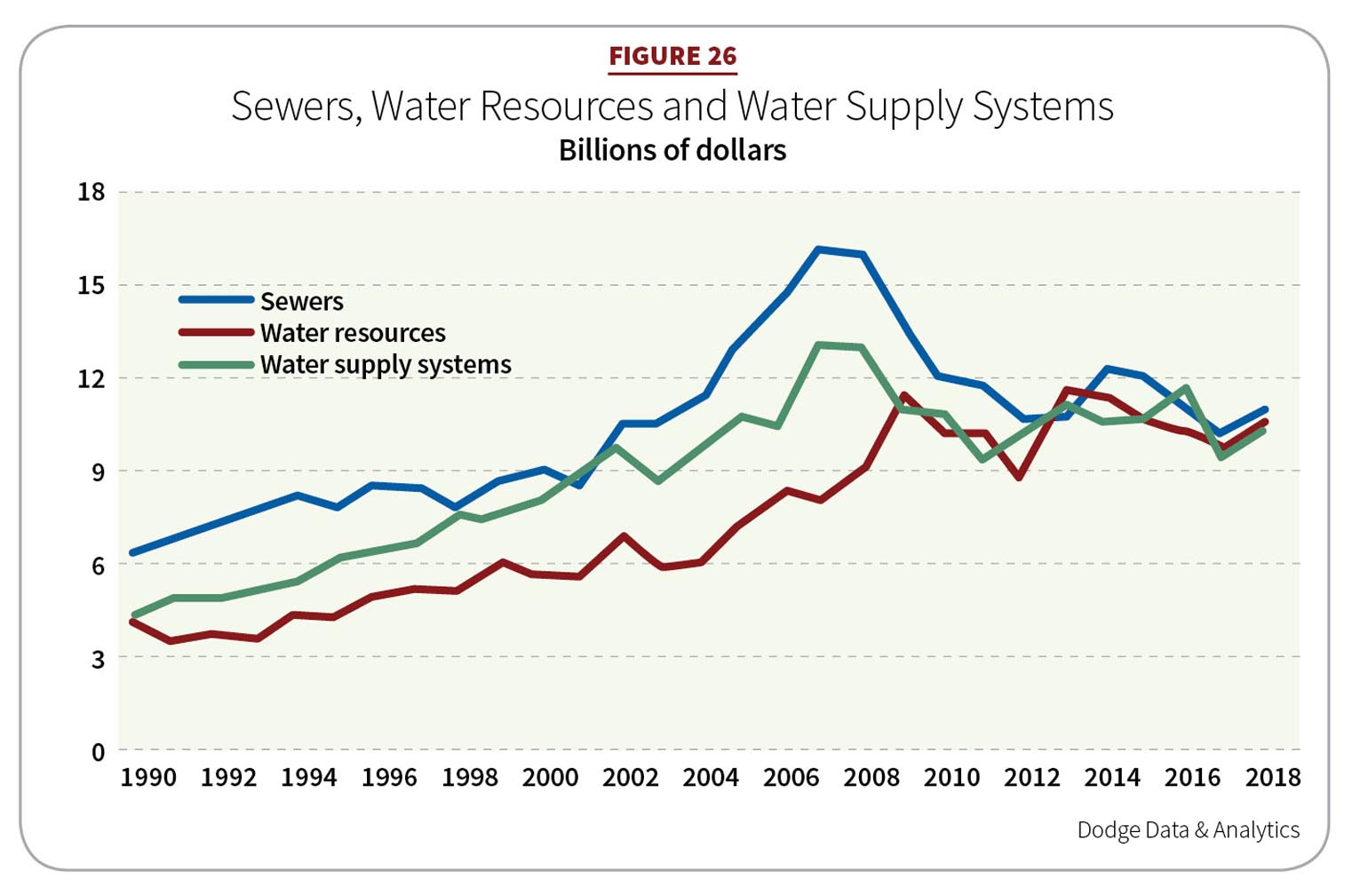

Helping in 2018 is a $1 billion increase for federal Water and Infrastructure Act loans, a 1 percent increase in the Army Corps of Engineers construction account, and the recently enacted Water Infrastructure Improvements for the Nation (WIN) Act. Growth in this construction sector extends to river/harbor development (10 percent/$10.8 billion), sewer (8 percent/$10.8 billion) and water supply construction (9 percent/$10.6 billion) (see Figure 26).

The top projects in 2017 included the Vista Ridge water supply pipeline project ($844 million) in San Antonio; an upgrade to a waste water treatment facility ($422 million) in Baltimore; and the EchoWater Primary Effluent Pumping Station ($415 million) in Elk Grove, Calif.

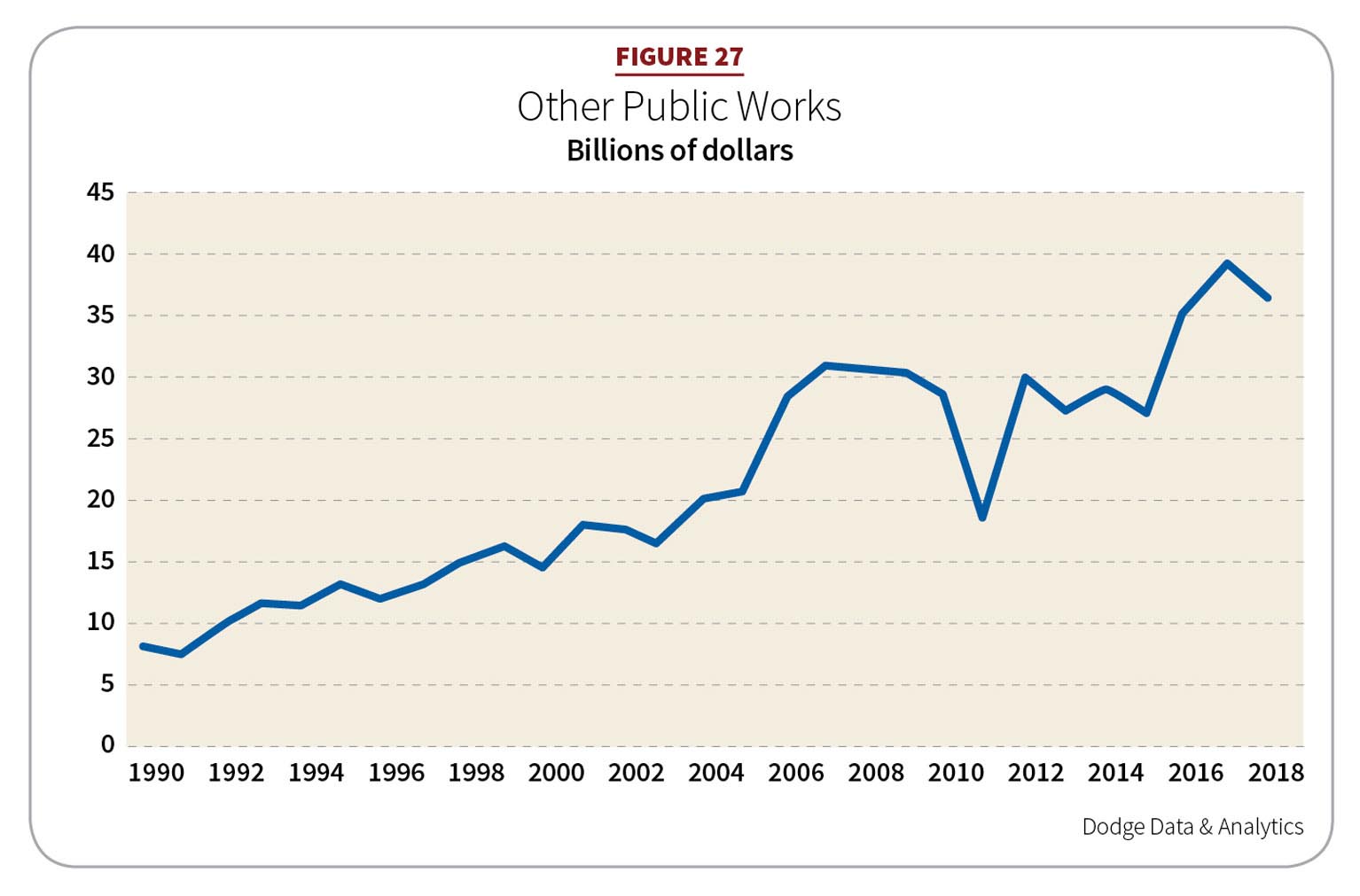

Other public works

This sector, including pipelines, mass transit and outdoor sports stadiums, advanced an estimated 13 percent ($39.0 billion) in 2017. A big 46 percent gain in pipeline construction helped, despite some delayed pipeline approvals by the Federal Energy Regulatory Commission (FERC). This year, pipelines won’t provide quite the lift, creating a 7 percent contraction for “other public works” ($36.3 billion), though still a healthy number (see Figure 27).

Some important projects in 2017 included the Rover natural gas pipeline in Michigan, Ohio, Pennsylvania and West Virginia ($4.2 billion) and the California High Speed Rail Authority’s Central Valley construction project ($1.4 billion).

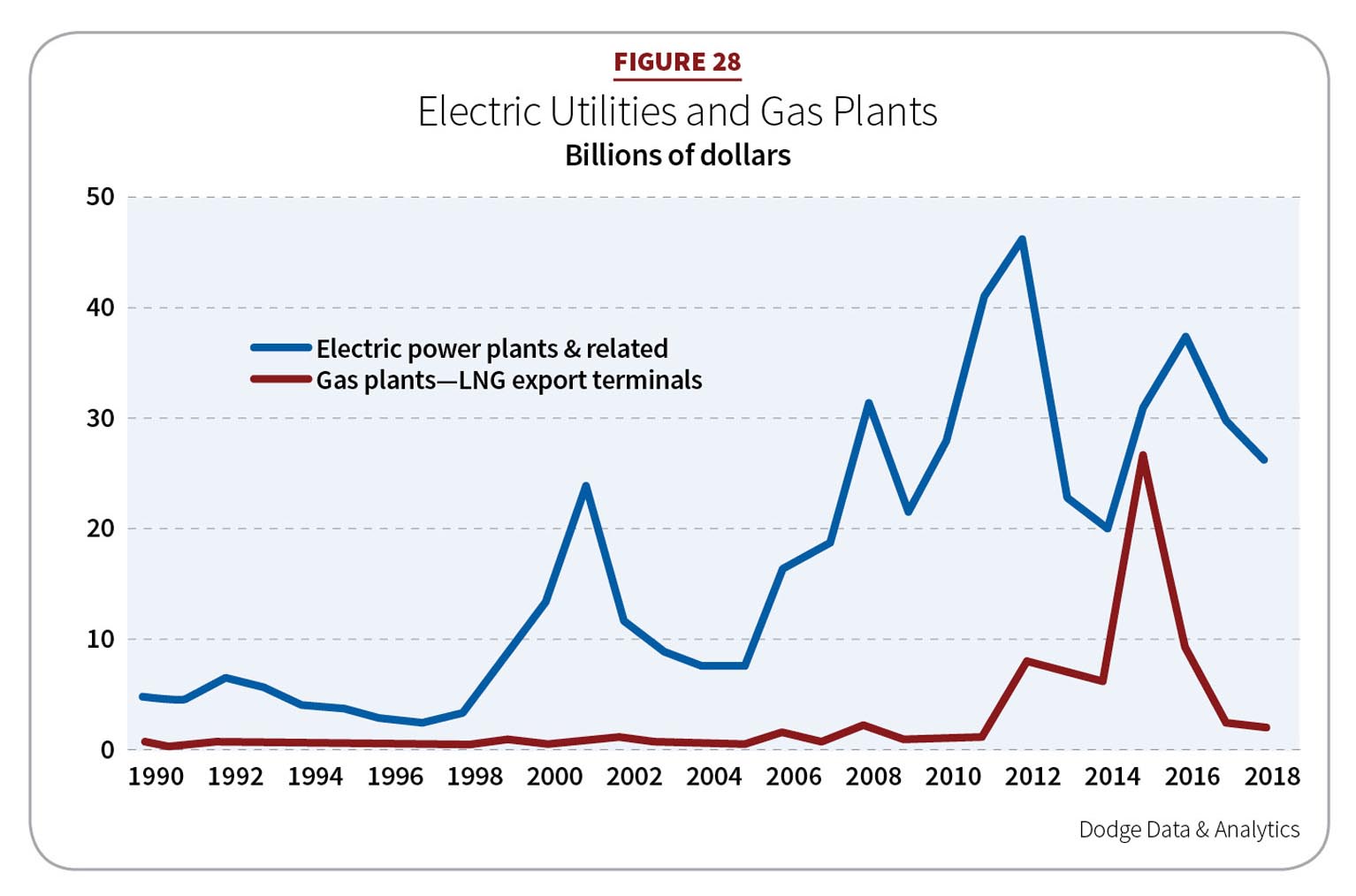

Electric utilities and gas plants

Last year, this sector continued its decline, falling an estimated 31 percent ($32 billion). The descent from a robust 2015 continues to negatively impact total construction start numbers each year. Unfortunately, no major liquefied natural gas (LNG) terminal projects were built in 2017 as they faced delays by FERC.

LNG-fired power plant construction held its own. In 2018, electric utility and gas plant starts will decline, but less steeply at 13 percent ($28 billion) (see Figure 28).

Working in this sector’s favor is a good capacity utilization rate for electric power and generation of 75 percent. State portfolios mixing electricity generation (e.g., natural gas, wind, solar and so forth) should help incentivize new power plant projects.

For now, the impacts of efforts to eliminate the Clean Power Plan and promote coal power are unclear. The fairly low price of natural gas will make it hard for coal to compete. Meanwhile, solar and wind power credits extend through 2019.

The big projects in 2017 included two California natural gas-fired plants: Carlsbad Energy Center ($2.2 billion) and AES Alamitos Energy Center ($1.3 billion). The Cricket Valley Energy Center in New York ($1.6 billion) was third.

Can we beat expectations in 2018?

The strength of civil engineering work in 2018 remains to be seen. It was healthy enough for ConstructConnect to change its 2017 construction totals from 4.5 percent to 7.8 percent.

Then, there’s the residential market led by the resurgent single-family sector. The NAHB anticipates 2019 will be a breakthrough year, putting that sector within reach of normal performance. That will lessen the sting from a multifamily sector that has peaked.

Nonresidential has its own bright spots. Education construction is getting better support with approved state and local bonds. Retail may be shaky, but online shopping continues to make gains for warehouse construction.

Areas of retraction are showing some growth, including healthcare, religious buildings and amusement. Stronger manufacturing plant construction will continue. With solid pipeline and natural gas plant construction, and positive movement out of Washington regarding infrastructure, the healthy nonbuilding sector could help 2018 surpass its total construction forecast. All in all, this is an economy that still has some spring left in its step.

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].