You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

If the 2013 economy were a horse race, it often trotted more than galloped.

This fifth year of recovery was modest. Construction stayed in the race and reflected an economy that expanded in different ways. Sometimes growth continued to rise, sometimes it leveled, and sometimes it was strong enough to bolster some red balance sheets closer to black. Projections for 2014 indicate more of the same but with hope for an even stronger year holding fewer self-inflicted wounds.

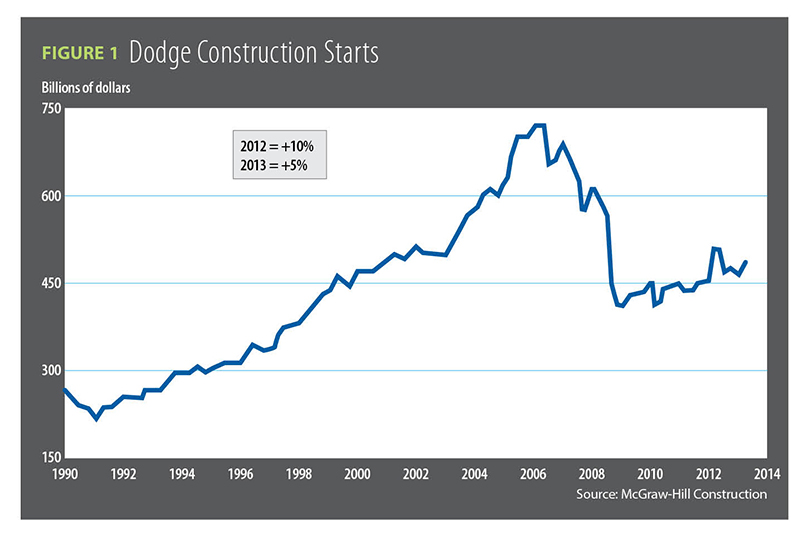

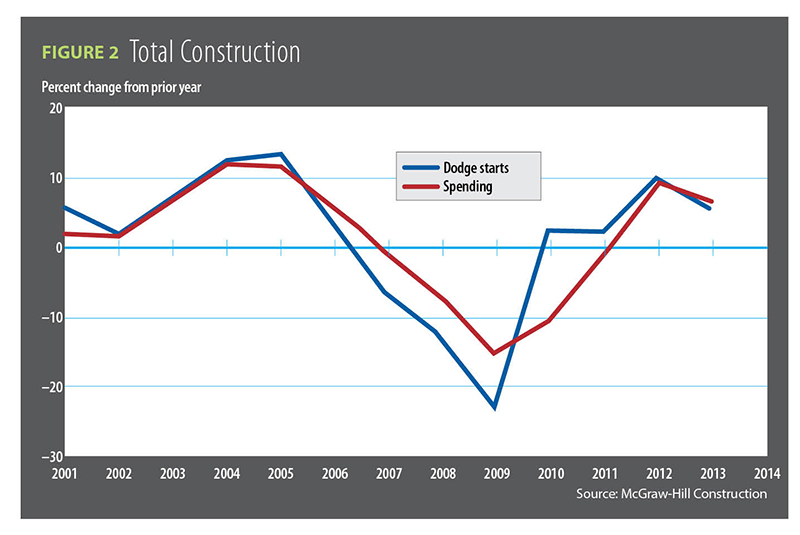

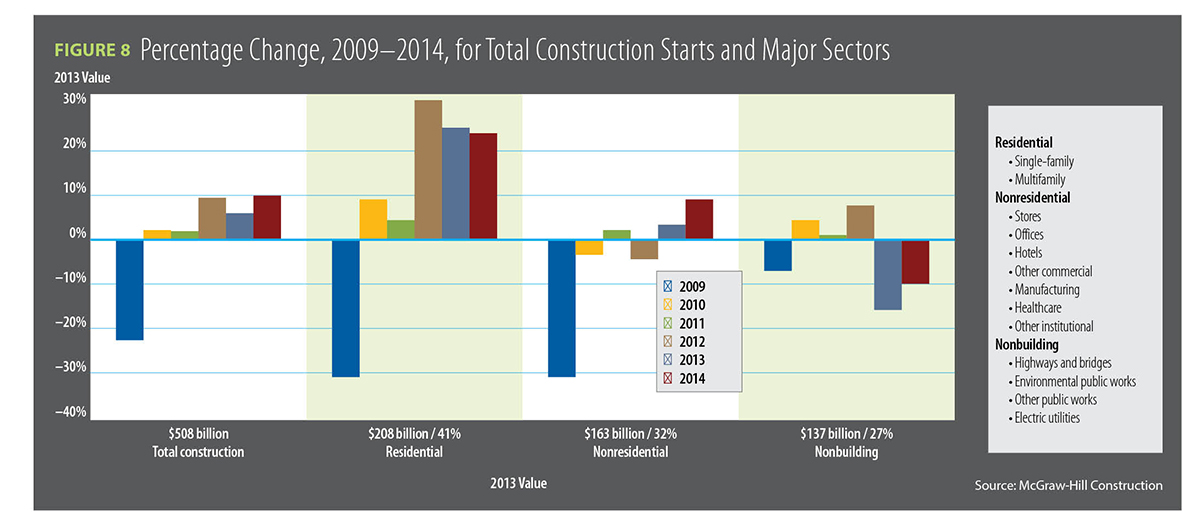

In short, a hesitant economy played a role in decelerating construction momentum. Adding it up, total starts rose 5 percent ($508 million) in 2013. They rose 10 percent in 2012 (see Figure 1). However, McGraw-Hill Construction’s Robert Murray, vice president of economic affairs, doesn’t see the regression as a retreat.

“Rather, I think we hit a pause,” he said. “We’ll be back up to 9 percent ($555 billion) this year in line with a construction upturn that is subdued and selective.” Murray spoke at McGraw-Hill Construction’s Outlook 2014 Executive Conference held in October 24–25, 2013, in Washington, D.C.

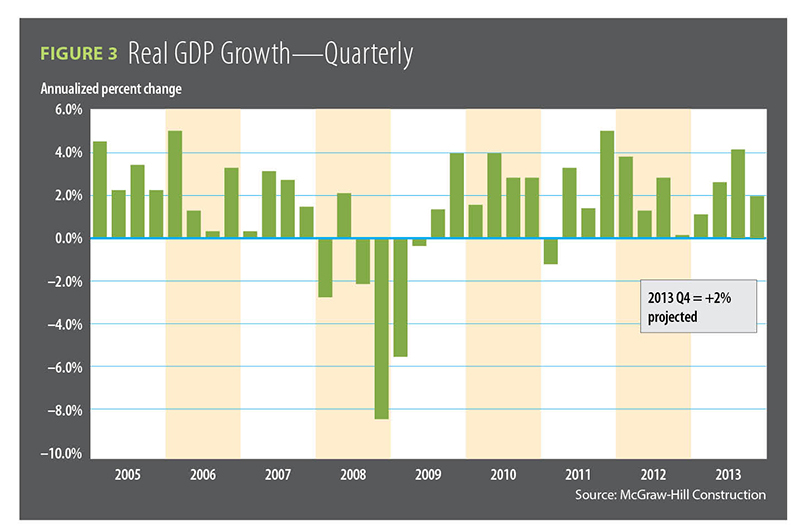

While slow U.S. economic growth was frustrating in 2013, everything seemed to move in the right direction. The gross domestic product (GDP) grew 1.8 percent in the first quarter, then 2.5 percent in the second quarter and an unexpected upward revision to 4.1 percent in the third quarter (see Figure 3). Unfortunately, fiscal drags out of Washington took aim.

The government shutdown was estimated by some to stifle fourth-quarter growth. At press time, final figures were pending, but economists projected a 2 percent growth. The shutdown and a race toward fiscal default slowed an economy wanting to take off. A lack of agreement in initially crafting a budget and the resulting sequester drew negatives, as well.

In its 2014 economic forecast webinar, “Emerging Opportunities for Construction,” held in October, Reed Construction Data’s Chief Economist Bernard Markstein said, “Certainly, some of our [economic] problems are of our own making. So, when I look at this year’s outlook, growth will continue but will be slow, especially if the U.S. government continues on its dysfunctional track, which only breeds uncertainty and diminishes investment.”

Speaking at the McGraw-Hill Construction’s Outlook 2014 Executive Conference, Beth Ann Bovino, chief U.S. economist at Standard & Poor’s, said, “In 2013, we saw a 1 percent loss of growth due to austerity measures. The end of the stimulus and the fiscal fog created by lawmakers created an uncertainty tax that constrained this economy.”

GDP in 2014 is forecast for 2.7 percent. Murray sees a 5.7 percent growth if Washington-driven headwinds recede.

Some encouragement was found in December with the signing of the Bipartisan Budget Act of 2013.

“While not a grand bargain by any means, the agreement does provide clarity in federal budgetary spending for the next two years,” said Marco Giamberardino, executive director, Government Affairs, National Electrical Contractors Association. “Congress now has a plan to appropriate spending dollars and set priorities within each agency budget. This represents the first bipartisan budget deal brokered under divided government since 1986 and gives us some serious hope that Congress can work together, cut through partisan gridlock, and address some key priorities.”

STRAIGHT TALK ON OTHER HEADWINDS

Bovino added that other variables could serve as a drag, including a further slowing of exports, spiking oil pricing and any Federal Reserve move that would remove liquidity sooner than expected. And while the U.S. government debt is dropping at a steady pace, Bovino said tackling entitlements will be imperative; she said Medicare and Medicaid represent 40 percent of the federal budget and will increase to an estimated 60 percent in the ensuing decades.

UNEMPLOYMENT IN 2013

For Bovino, a robust labor force is essential to a stronger economy.

“It’s all about the jobs,” she said. “When people are out of the market, they aren’t paying taxes. Unemployment also dampens confidence.”

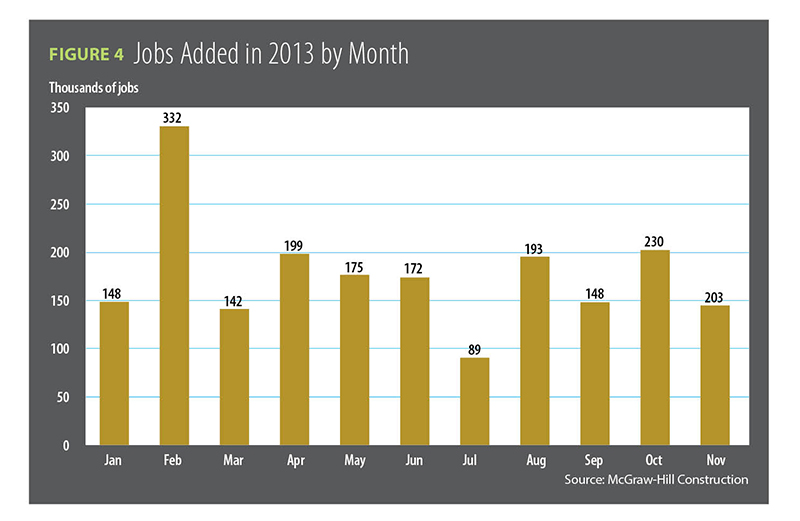

The October 2013 unemployment report saw a slight uptick to 7.3 percent but also a robust job growth of 230,000 jobs, and the November numbers were better than expected: 7 percent unemployment and 203,000 jobs added (see Figure 4).

“We are about two-thirds of the way back from the 9 million dropped from the labor force,” Bovino said. “Those numbers do hide some weakness, including part-timers and those who dropped out. As workers return, it is important to ask what kind of job will they have and at what salary?”

Employment specific to construction continues to rise but faces its own conundrum. As work returns, trained construction labor is hard to find. Many individuals sidelined during the recession left the profession.

“We [are] in for a challenge,” said Ken Simonson, chief economist for the Associated General Contractors of America. “The good news is we saw construction employment rise in 37 states year-to-year from July 2012 to July 2013. North Dakota and Louisiana were particularly strong.”

Simonson was part of the Reed Construction Data webinar economic forecast.

BUILDING ON GOOD NEWS

In the 2014 Dodge Construction Outlook, the authors added this perspective: “Construction is in the midst of a cyclical upturn, and is not stuck in an extended bottom (which many who focus on nonresidential building or the institutional sector might believe). The initial years of recovery following a financial crisis generally turn out to be slower than other recoveries.” They added this recovery could use a “second-stage” boost by 2015 or 2016, which they posit will come from the “emerging energy boom” created by U.S. natural gas exploration and extraction, including shale oil. Reed Construction also covered this, calling it “the shale gale.”

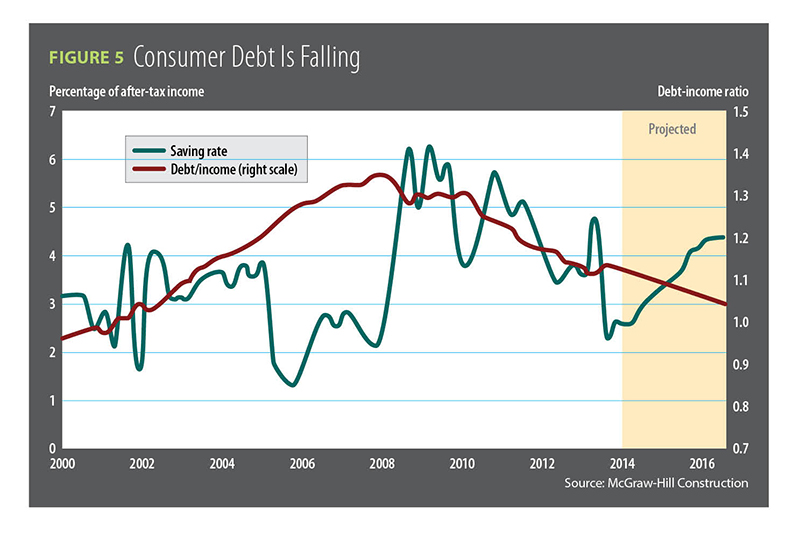

Bovino sees other positives, too. She cited a “robust” private demand for goods, higher housing prices, manufacturing coming back to the United States, a return of equipment production, and Fed policies that continue monthly bond-buying to keep interest rates down. She added that consumer debt is down and savings are projected to continue (see Figure 5).

“All of this suggests to me that we are turning a corner,” she said.

Two significant indicators point to momentum for construction in 2014. Architecture billings are one of them.

“We see a sustainable recovery due to the growth in billings over the last 12 to 13 months,” said Kermit Baker, chief economist for the American Institute of Architects (AIA), part of Reed’s economic panel. “All major sectors are growing, with commercial and industrial accelerating the fastest. Institutional is showing some modest gain, as well. As the economy grows, everyone seems to be showing positive billings.”

Though a work backload of eight months would provide the most confidence, Baker said firms are showing at least five months, which is allowing them to maintain their staff levels.

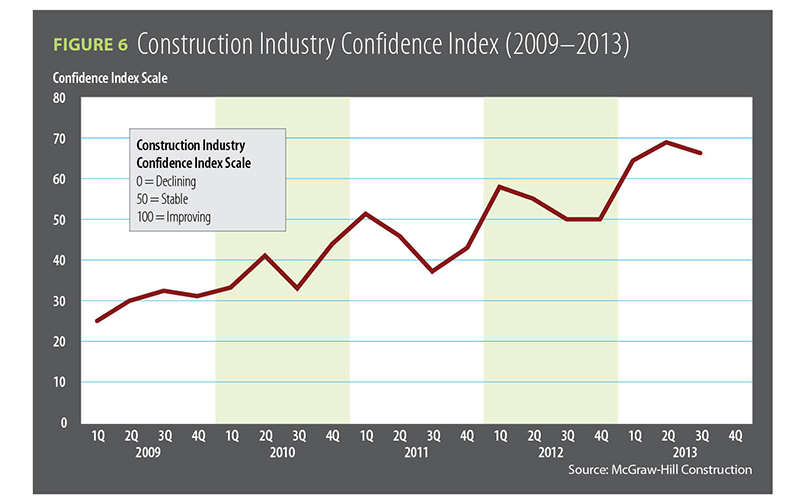

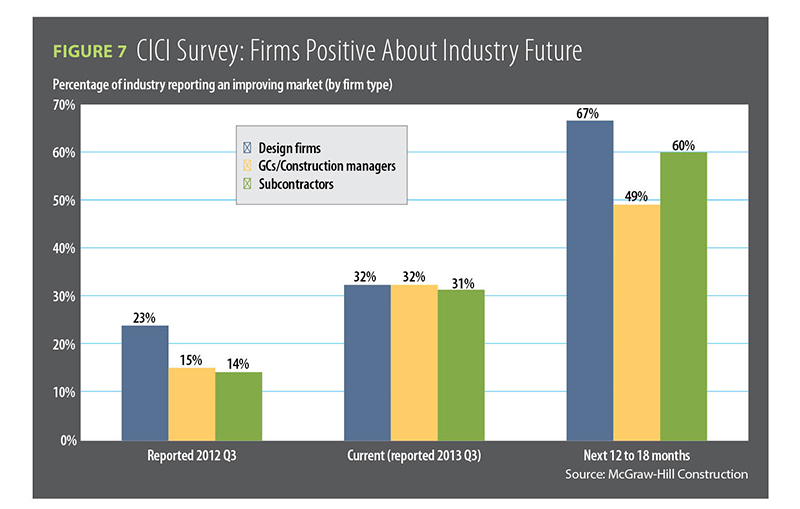

Another positive indicator is the Construction Industry Confidence Index (CICI) that measures confidence among designers, architects, contractors and subcontractors (see Figures 6 and 7).

“We’ve seen a one-third gain from third quarter 2012 to 2013 with a slight decrease in the later third quarter [2013] as budget negotiations in Washington had an effect,” said McGraw-Hill Construction’s Harvey Bernstein, vice president of industry insights and alliances, at its conference.

THE YEAR OF PAUSE AND BEYOND: AN OVERVIEW

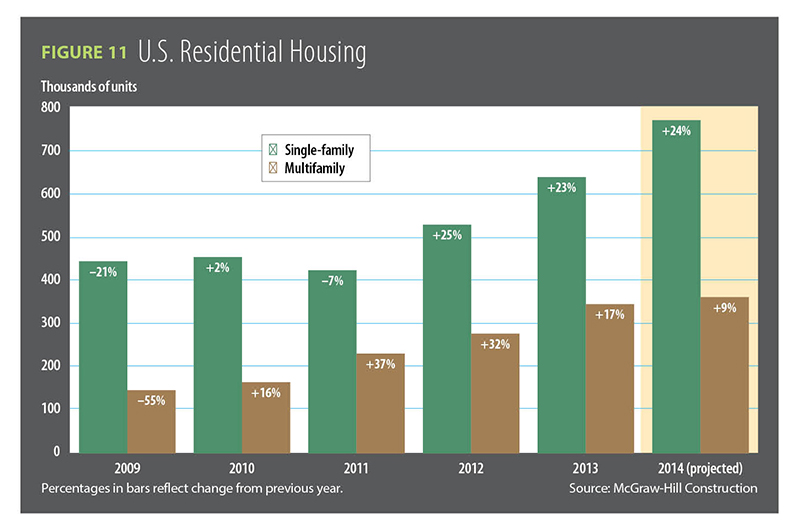

During 2013, single-family and multifamily housing continued their gradual ascent, rising 25 percent. The upward trends are expected to continue. An easing in foreclosures, low mortgage rates, and a rise in home prices will continue to help growth in single-family construction for 2014. Some easing in bank lending has begun, though it remains very tight. Meanwhile, the multifamily market slowed after four consecutive years of leading gains, though growth will continue in 2014.

According to CoreLogic, which collects and measures property and related financial data, foreclosures are moving quickly downward. Between 2009 and 2011, they reached an astounding 1.1 million. Last August, foreclosures dropped an impressive 34 percent from 2012. Homes facing threat of foreclosure fell 22 percent. While housing is not yet out of danger in this regard, the foreclosure drop has been precipitous.

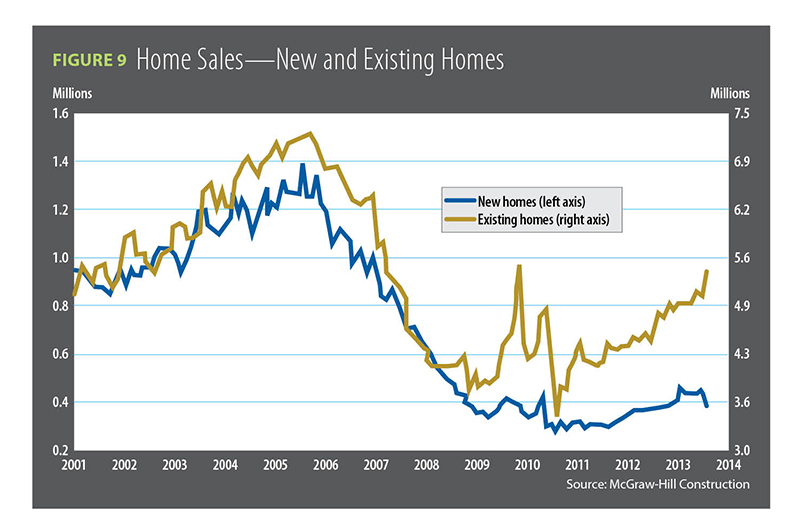

Sales figures were encouraging, too. The National Association of Realtors (NAR) reports an increase of 59 percent or 5.48 million existing homes sold as of August 2013. New home sales grew 56 percent or 421,000 homes. These sales mark a return of 76 percent for existing homes and 30 percent for new homes (for more from NAR’s report, see Industry Watch, page 12, and Figure 9).

Commercial buildings made gains, as well. The moderate growth is expected to continue this year, especially if more dollars for commercial property development emerge. This past year marked a 73 percent increase in square footage and a rise of 48 percent in dollars. Manufacturing-related construction also grew in dollar terms. There’s good news in institutional construction, too. Dodge expects this market to turn around in 2014, no longer serving as a drag on nonresidential.

In total, 2013 nonresidential was expected to show a 4 percent gain.

In public works, while federal funding may not be strong, 2013 showed strength in recent local and state project bond funding that may help lift construction. The National Association of State Budget Officers’ spring 2013 “Fiscal Survey of the States” shared that total general fund revenue for states rose 4.2 percent. Spending caution remains, but state and local governments are pursuing their own workaround through public and private partnerships.

Electric utilities will remain a sore spot for the construction marketplace. Dodge economists’ said that, if the negative performance in electrical utility starts were removed, overall 2013 total construction performance would stand at a 12 percent gain versus 5. That figure is dispiriting in one way but remarkable in another.

FROM TRENDS TO PRACTICE

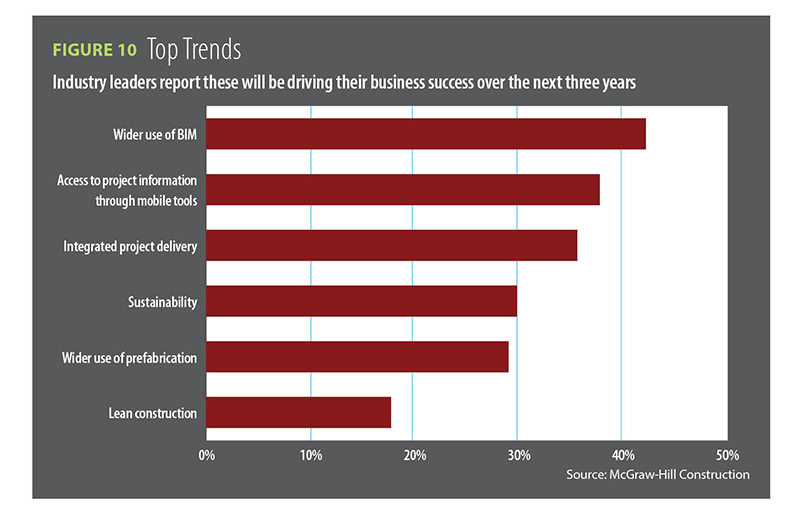

A number of construction trends took hold in 2013 and are expected to increase over the next three years.

“We are certainly seeing a wider use of BIM [building information modeling],” said McGraw-Hill’s Bernstein. “Some 42 percent of respondents said they use it, citing how this tool was reducing project duration and cost and encouraging repeat business” (see Figure 10).

Mobile access to project information is another growing trend. Some 38 percent surveyed said they tap into the cloud and other means to grab project information on-site. This includes pulling up BIM files.

“We are seeing a steady decline in PDFs, paper documents and drawings, and handwritten notes,” Bernstein said.

Thirty-six percent of respondents also indicated they are regularly involved in integrated project delivery. Another 30 percent said they often work on projects that promote sustainability.

“Green is now a standard practice, and it’s on the move,” Bernstein said.

Green building accounted for 44 percent of all U.S. nonresidential projects in 2013 and is expected to represent almost 50 percent in 2014. Last year, 56 percent of all office projects and 51 percent of all school construction were green, as well. McGraw-Hill identified green projects as those that pursued LEED certification or incorporated sustainable design near that standard.

Smaller trends included an increase in prefabrication construction projects, lean construction and an adherence to safety to reduce project schedules and budgets. BIM plays a role here, too, because of its design clash detection ability that can also serve as hazard detection.

Finally, several speakers at the McGraw-Hill conference spoke to growing U.S. opportunity—involvement in the global construction marketplace. Bernstein said that construction makes up 36 percent of the world’s GDP with that number growing to 70 percent by 2025. “Dollars” spent on high speed rail, water, electricity and highways were examples. On the high end, Brazil is spending $225 billion per year followed by China at $167 billion and India at $125 billion.

“Embrace the new global players, and study them,” said Roger Flanagan, professor and chairman, Steering Committee for International Affairs and School of Construction Management and Engineering, University of Reading. Flanagan was the luncheon keynote speaker at the 2014 McGraw-Hill conference.

“Today, the developing world is moving faster than the developed one. The U.S. needs this ‘other’ market. See who is innovative, are fast learners, and embrace integrated delivery. Being green will be a given. Communicate how your company is different,” he said.

THE NUMBERS MARKET BY MARKET FROM 2014 DODGE CONSTRUCTION OUTLOOK

RESIDENTIAL BOTH HEATS UP AND COOLS DOWN

Snapshot: in 2014, single-family starts will grow 24 percent, multifamily 9 percent.

The Dodge report states, “Single-family housing is finally moving solidly in the right direction.” In 2012, starts grew by 25 percent and another 23 percent in 2013—a 90 percent increase from 2011’s 413,000 units. This year, 2014, should add 24 percent (785,000 units) and grow 26 percent in dollar terms to $201 billion (see Figure 11).

The West will see the biggest start gains at 29 percent. The South-Atlantic should clock in at 25 percent. Other regions will also fare well, with South-Central at 22 percent, the Northeast at 21 percent and the Midwest at 18 percent.

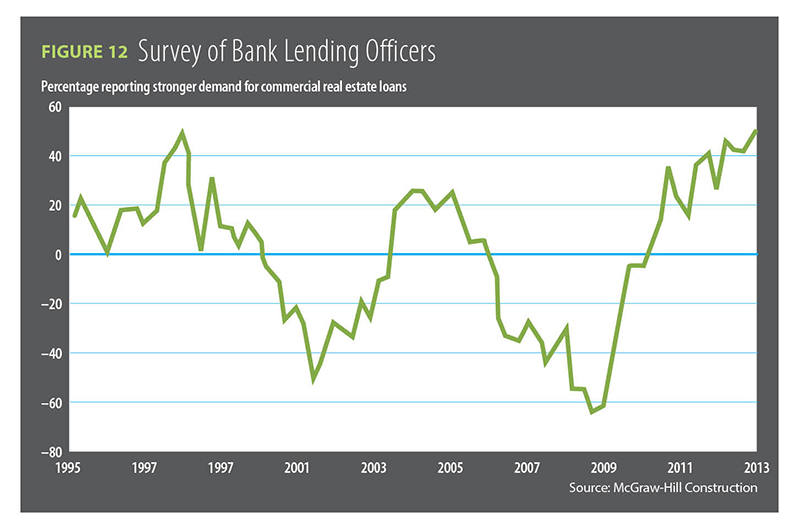

While lending remains tight (buyers needing an average credit score of 700 or higher), Dodge economists feel this may surprisingly force banks to begin loosening their underwriting standards to maintain their bottom lines and generate new business. Though 30-year fixed rate mortgages have risen from a low 3.35 percent in late 2012, they held at 4.2 percent last October. Rising rates and their effect on home sales and starts remains unclear, according to Dodge authors. (See Figure 12.)

Multifamily housing has led the way in the housing recovery beginning in 2010 with starts increasing by 16 percent. In 2011, starts shot up 37 percent and added another 32 percent in 2012. Last year, the market cooled but grew 19 percent. This year, starts are expected to advance 9 percent or 365,000 new units. Dollars will increase 11 percent (roughly $53 billion). Multifamily is definitely tempering (see Figure 11).

CB Richard Ellis Econometric Advisors say rental property growth is one culprit; they expect it to mature and settle in at a 3 percent annual rate. Condos, however, showed strength during the first nine months of 2013. Of the 10 largest multifamily projects around the country, four were condominium efforts that were also the largest in project dollar value. Two of the biggest were located in New York. They included the $390 million Greenwich Lane Condos and the 625 West 57th Street Apartments ($365 million). Boston followed with the $334 million condo portion of the $460 million mixed-use Millennium Tower. Miami had big projects, as well.

Regionally, 2014 growth is expected to stabilize in the Northeast, which enjoyed a 45 percent surge last year. The South-Atlantic gained 22 percent and is expecting 17 percent growth this year. The West increased 15 percent and is expected to maintain growth at 11 percent. Meanwhile, the Midwest showed a 21 percent increase last year but will drop to 6 percent in 2014. The only region that slid in 2013 was South-Central at 4 percent. It is expected to advance slightly in 2014 to 7 percent.

COMMERCIAL SHOWS MODERATE GROWTH

Snapshot: Commercial building will grow steadily up to 18 percent.

Commercial sector activity rose 16 percent (483 million square feet) in 2013. That represented $62.4 billion; a 73 percent increase from 2010 in terms of square-footage and 48 percent in dollars. This year’s forecast for commercial buildings will be similar. The market is expected to increase 18 percent (568 million square feet) and 17 percent ($72.7 million). Helping this market are better occupancies and rents, stronger property values, and more lending.

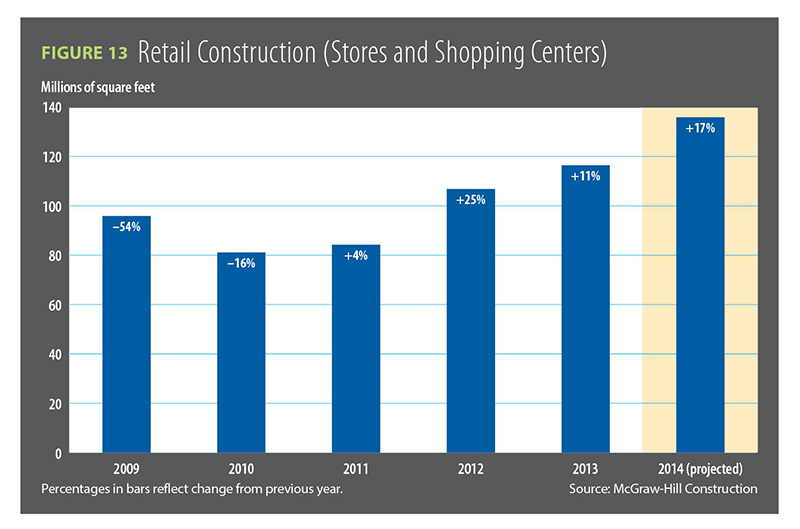

Stores and shopping centers remain a commercial puzzle. On the positive side, the Consumer Confidence Index grew from 61.9 in March 2013 to 79.7 in September. The double-digit housing starts have encouraged this market, as well. Unfortunately, the “uncertainty tax” coming out of Washington and January 2013’s lost tax advantages (raised payroll tax and higher tax rates for couples and single households in certain income brackets) chilled spending but not confidence numbers. That all translated to retail sales of 4.5 percent in the first eight months of 2013, compared to 5.4 percent in 2012. All of this drove growth in store construction: 11 percent in 2013 (117 million square feet) and an expected 17 percent increase (137 million square feet) in 2014 (see Figure 13).

Top cities leading the charge in growth in the first nine months of 2013 were Kansas City at a whopping 280 percent, followed by San Antonio (99 percent), New York (79 percent), Dallas (25 percent) and Chicago (15 percent). Big discount chains did their part. Walmart began construction on $1.8 billion worth of projects. Dollar Tree embarked on projects totaling $169 million, and Family Dollar was close behind at $167 million. Outlet centers broke ground across the country, representing $263 million in 2013—an increase of $55 million.

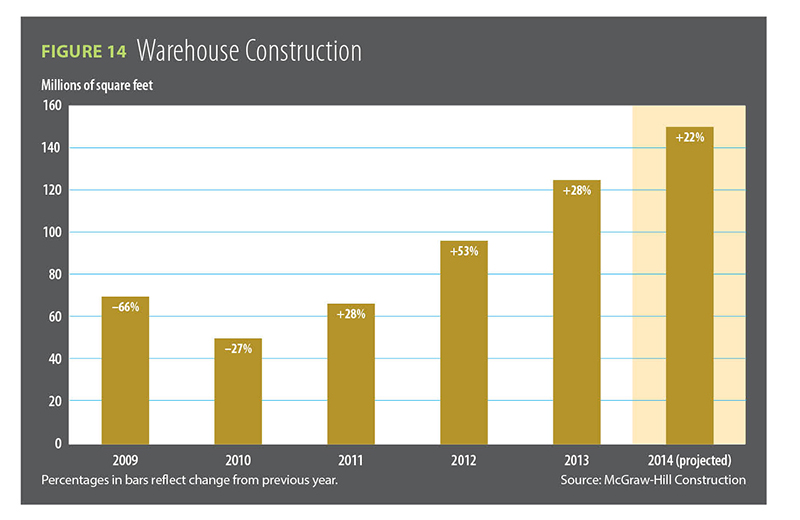

Commercial warehouse starts in 2013 crossed a 100-million-square-foot mark not seen since 2008. At 28 percent (123 million square feet), the year showed continued recovery from a boom in 2012 that saw starts rise a remarkable 53 percent. That year, Amazon.com led the way with 10 added distribution centers. Last year, it added four more. In 2014, starts are expected to dip slightly to 22 percent (see Figure 14).

Other project leaders in 2013 included a Nike warehouse expansion in Memphis (1.7 million square feet), DuPont Corporate Park in Seattle (1.6 million square feet) and Helen of Troy, also in Memphis (1.2 million square feet).

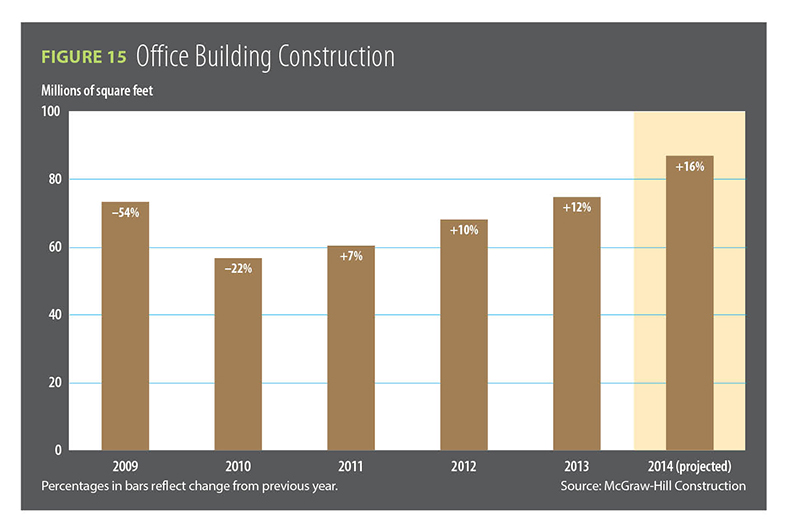

In a year of mild increases after steep declines, the office market continues to climb back. In total, 2013 starts rose an estimated 12 percent (75 million square feet). In 2014, expect a modest 16 percent (87 million square feet) gain (see Figure 15).

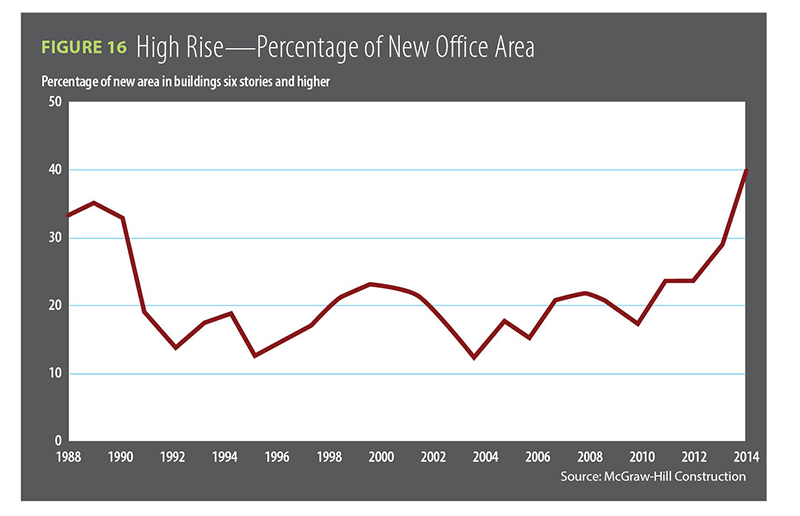

High-rise and large-scale developments took hold in 2013. The largest office high rise was the $850 million, 1.4-million-square-foot Hudson Yards South in New York. Office building projects ranging from $65 million to $100 million were spread across cities. Noteworthy data centers included an $861 million installation at Fort Meade in Maryland and a $500 million installation for Facebook in Des Moines, Iowa. The top three metro office performers included Dallas increasing 191 percent, Houston at 68 percent and Boston enjoying a 26 percent rise (see Figure 16).

While hotel growth has cooled from its 56 percent gains of 2011, 2012 and 2013 saw healthy growth at 23 and 18 percent, respectively (see Figure 17). Gains of 19 percent (46 million square feet) are expected this year as new projects begin and hotel fundamentals keep improving. For example, revenue per room advanced 5.8 percent in the first eight months of 2013. Occupancies rose to 61.4 percent.

During this time, several major hotel projects broke ground, including the $250 million Cabana Bay Beach Resort in Orlando and $165 million Ameristar Casino resort in Lake Charles, La. Major renovation also made the news. The largest was a $415 million remodel to the SLS Hotel and Casino in Las Vegas.

SOME GOOD NEWS FOR INSTITUTIONAL

Snapshot: The institutional market will turn a corner and grow 2 percent.

After suffering declines for five years, budget conditions are slowly improving for this market. In fact, this market has steadily been shedding its negatives since 2011 from –11 percent to last year’s –4 percent. Forecasters expect this market to return to black in 2014, gaining 2 percent ($89.1 billion).

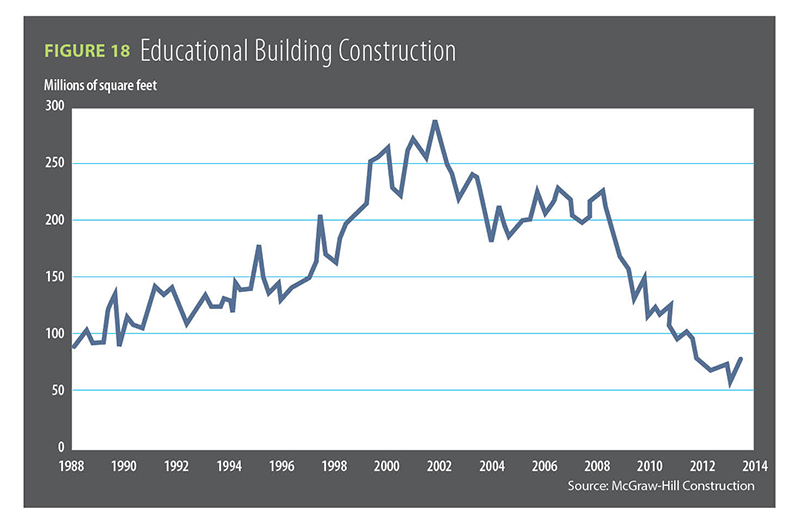

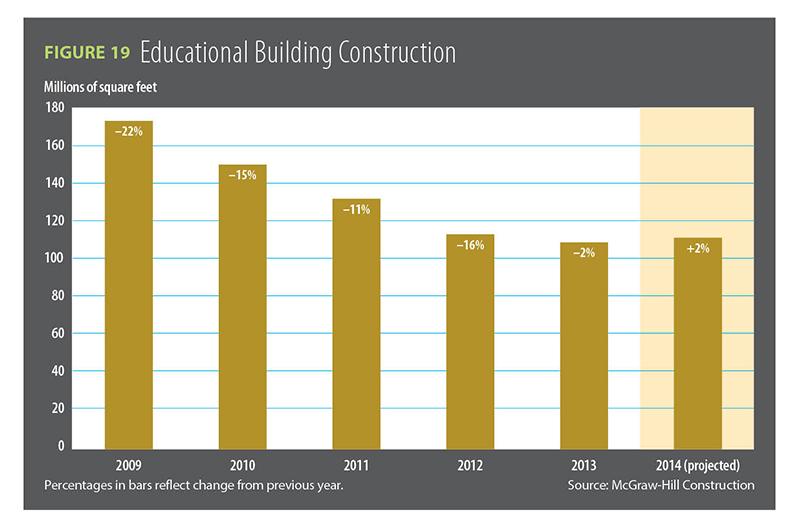

In year-to-date performance over the past four years, the educational building market has improved, though mixed. In the first nine months of 2013, construction starts declined in senior and junior high schools by 7 percent and 12 percent, respectively. Primary schools, however, increased 3 percent. Vocational school starts grew by 7 percent. Measured by expanded footage, community college construction grew by 2 percent, universities by 7 percent, and the laboratory/research and development sector by 13 percent. (See Figures 18 and 19.)

Larger projects included the $252 million New York City College of Technology’s Klitgord academic building in Brooklyn. Other noteworthy ventures were budgeted between $100 million and $218 million.

A number of 2012 bond measures will lead to construction starts this year, as well. For example, Miami-Dade County is embarking on $1.2 billion repair and renovation program for its schools. Houston is following suit with a $1.9 billion program. Upward enrollment trends in many states could open the door to construction down the road.

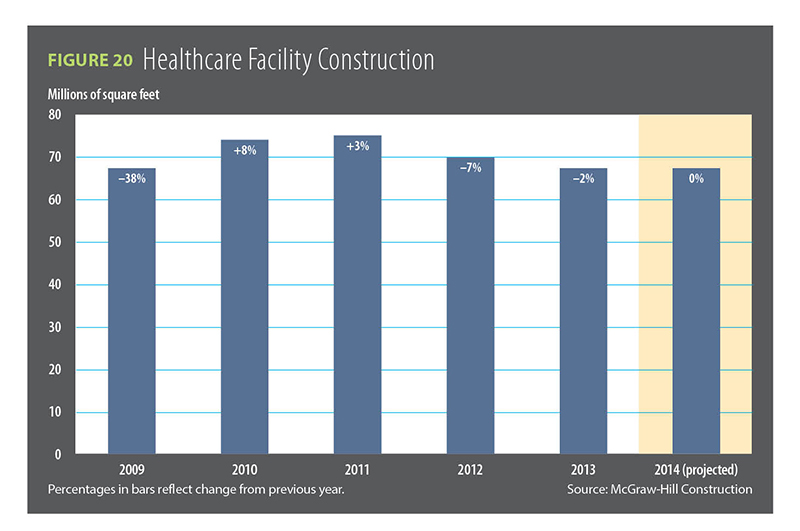

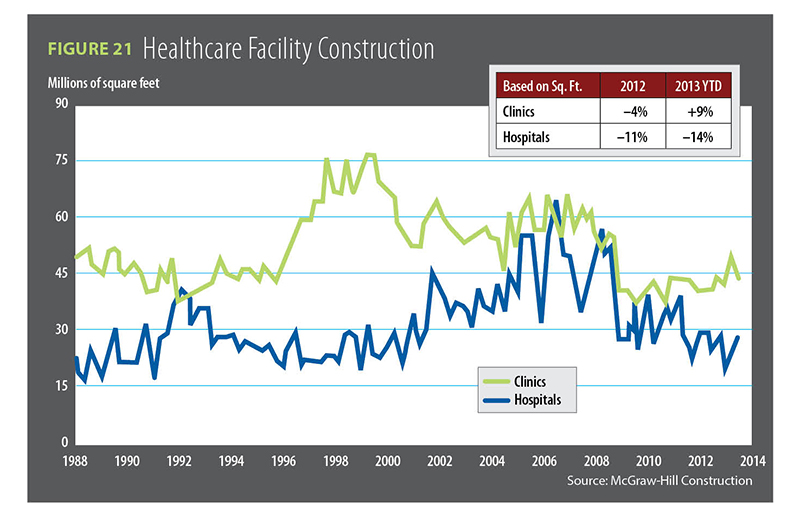

Hesitancy has ruled the hospital and other health treatment facility market for a few years. The uncertainty and battles over the Affordable Care Act (ACA) have kept large projects from moving to start stage. Before the recession and ACA, 39 project starts valued at $100 million or more broke ground in 2008; the largest projects totaled $7.6 billion and 19 million square feet.

In contrast, 2013 saw only 21 healthcare projects valued at $100 million or more. The largest ones represented a total of only $4.9 billion and 7.7 million square feet. Last year, starts slipped 2 percent. In 2014, starts will remain unchanged in square footage (68 million square feet) but will grow in dollar value by 2 percent as public financing becomes more readily available and the turmoil over ACA dissipates (see Figure 20).

Healthcare clinics, in particular, are showing growth over hospital construction (see Figure 21). Noted projects in 2013 included the $830 million Stanford University Medical Center Hospital in Palo Alto, Calif., and the $537 million Fort Bliss Replacement Hospital in El Paso, Texas. Replacing aging facilities and serving a growing aging population should add some strength to this market in the coming years.

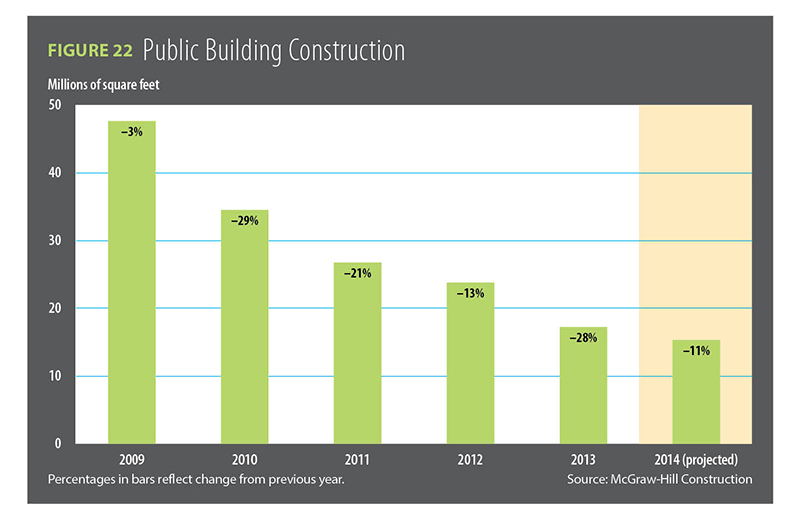

Public buildings in 2013 saw some appreciably rising negatives. Police/fire stations were down 11 percent, military work fell 60 percent, and detention facilities dropped 41 percent. Courthouses lost 25 percent. In total, 2013 public buildings projects represented 17 million square feet, a decline of 28 percent from 2012. The pressures of reduced federal spending, most notably drastic cuts (34 percent) to the General Service Administration’s new construction account, will keep this market in decline by 11 percent with activity averaging 15 million square feet (see Figure 22).

Noted projects in 2013 included the $222 million San Diego County Women’s Detention Center in Santee, Calif., and the $137 million Capitol Building restoration in St. Paul, Minn.

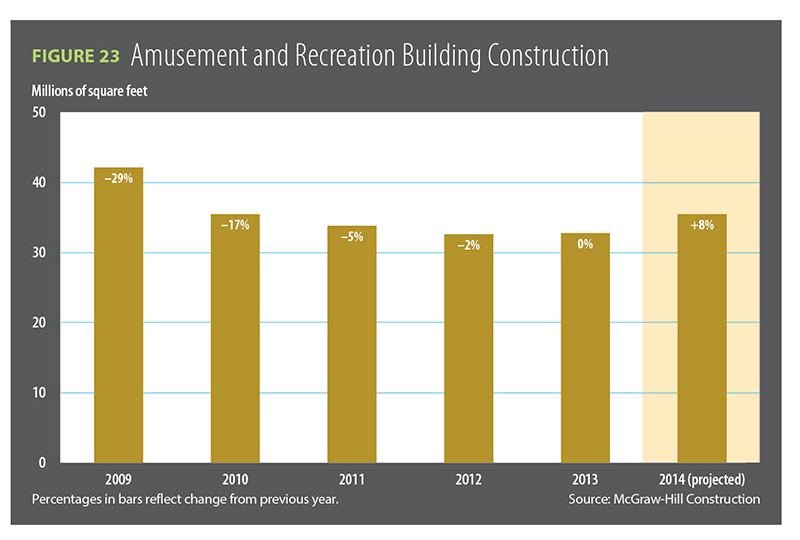

Other declines included religious building starts dropping a further 13 percent. A smaller slide will continue this year at 4 percent. After falling six consecutive years, amusement-related construction stabilized (33 million square feet) thanks to strengths in auditorium construction (up 125 percent) and theaters (11 percent).

A $650 million retractable-roof stadium for the Minnesota Vikings in Minneapolis helped bolster the final quarter of 2013. This market category is expected to grow a bit more quickly in 2014 with an expected 8 percent rise (35 million square feet) (see Figure 23).

Finally, railroad terminal growth exploded in growth by 182 percent, while bus and freight terminals grew 33 percent. Phase 2 work ($650 million) of the Third Street Light Rail–Central Subway Station in San Francisco was one of several key projects that broke ground in 2013.

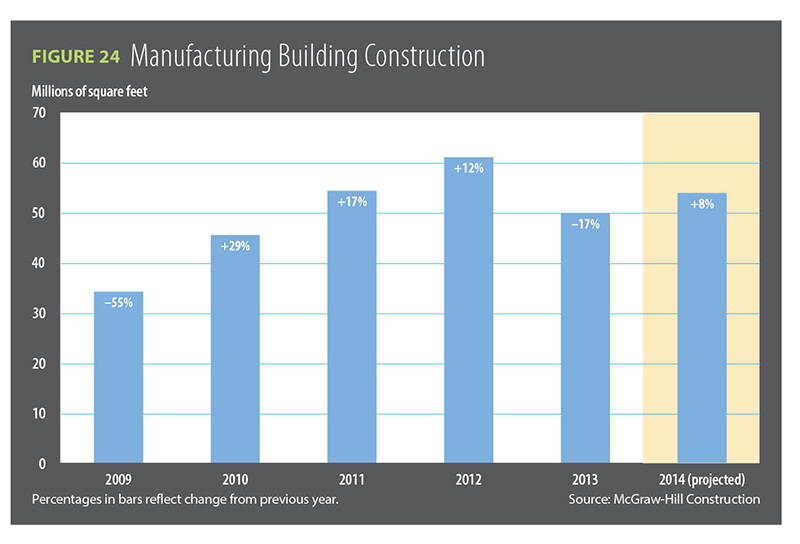

Manufacturing plant construction rose in dollar terms by 6 percent ($13.8 billion). Because Europe represents almost one-fifth of U.S. exports, its weak economies slowed acceleration in this market segment. Capacity utilization did climb to 77.3 percent in February 2013 and held to 76.8 percent in August. For 2014, manufacturing construction is forecast to grow 8 percent (54 million square feet) with an 8 percent dollar gain of $14.9 billion (see Figure 24).

A MIXED PICTURE FOR PUBLIC WORKS AND A PLUNGE FOR ELECTRIC UTILITIES

Snapshot: Lack of infrastructure funding will drop public works by 5 percent.

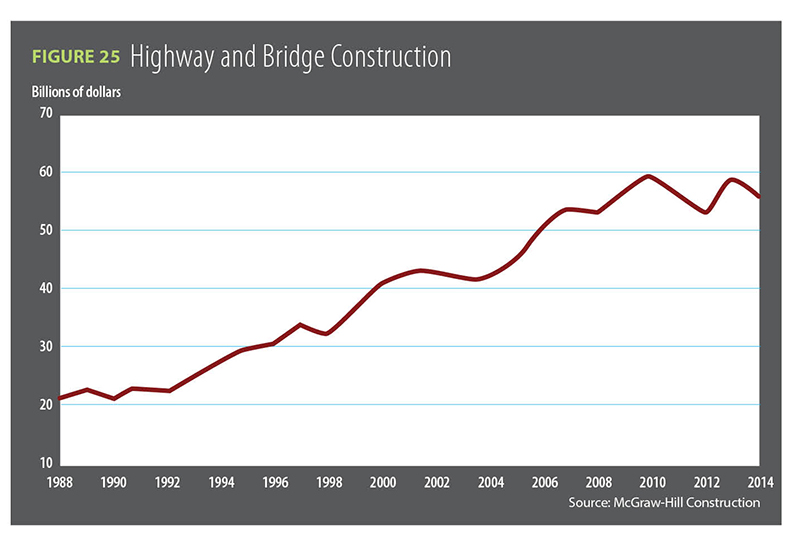

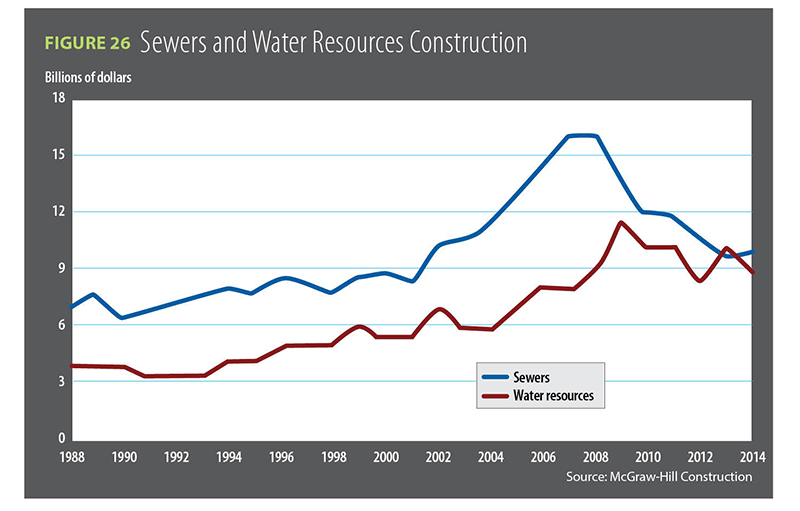

Let’s start with the good news. In 2013, public works projects rose 3 percent to $114.3 million. Within that, highway and bridge construction increased 12 percent (see Figure 25), and environmental projects grew by 8 percent. Those gains offset a plunge of 17 percent largely from a loss in pipeline construction. Starts are expected to slip in 2014 by 5 percent, representing $108 billion, especially if the sequester remains in place. Better general revenues and higher municipal tax receipts may ease state and local budget spending pressure.

Newsworthy projects in 2013 include the $1.6 billion Ohio River Bridge project; the $776 million Poseidon Resources Desalination Plant in Carlsbad, Calif.; and the $1 billion BridgeTex pipeline from Texas to the Gulf Coast.

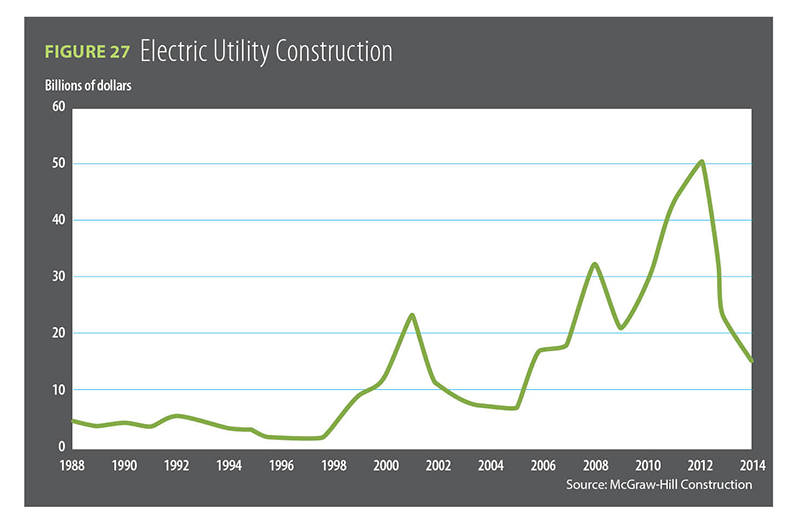

For electric utility construction, 2012 was its year as the market reached a record $50.9 billion. What a difference a year makes. In 2013, starts dropped 55 percent. Surplus generating capacity and ample natural gas weighed this market segment down. This year, some of the negatives will lessen, but a drop of 33 percent looms (see Figure 27). Providing some upward direction may be the demand for electricity in the South-Central region of the country. Capital investment in improved distribution and transmission will continue thorough smart grid initiatives. Renewable energy mandates still unmet in many states may spur work, as well. Notable projects in 2013 included the largest project of the year, a $2.3 billion Antelope Valley Solar Power Plant in California, a $1.9 billion wind energy farm in Iowa, and a $1.2 billion in pollution abatement upgrade for the Mill Creek Generating Station in Kentucky.

Economic forecasters may not see a boom year for 2014, but if certain fundamentals are addressed and we don’t get in our own way, maybe hitting a stride is within this economy’s grasp.

About The Author

GAVIN, Gavo Communications, is a LEED Green Associate providing marketing services for the energy, construction and urban planning industries. He can be reached at [email protected].