You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

So, tell us, how the heck are you? Oh, wait, we already asked you that while conducting our recent Profile of the Electrical Contractor research study. More than 2,700 of you responded, using snail mail and the internet, and told us what it’s like to be an electrical contractor (EC) in this day and age.

(Editor's note: click here to read part 2 of the 2014 Profile.)

It’s been a couple years since we last checked in with you, so we figured it was time to ask you these questions again. Actually, the timing is not quite as arbitrary as that; every two years, ELECTRICAL CONTRACTOR surveys its readership to develop its Profile of the Electrical Contractor. The survey asks about the previous full year (for example, the 2010 survey asks about 2009). With the last two surveys (in 2010 and 2012), things seemed a bit dicey. It’s good to learn this year that many of you are beginning to do better.

Diversifying their scope of activity and becoming more familiar with green-energy offerings are among the strategies many firms—even smaller companies—are adopting in the face of a still-stagnant, new construction business. With more firms growing and fewer companies shedding employees, it seems those strategies just might be paying off.

In this article, and in a follow-up next month, we break down some of the study findings. However, this research is quite extensive, so if you wish you can read the full 2014 topline report. You can also view past survey results so you can see how they’ve changed over time. Let’s get started with our 2014 Profile, shall we?

Who are you?

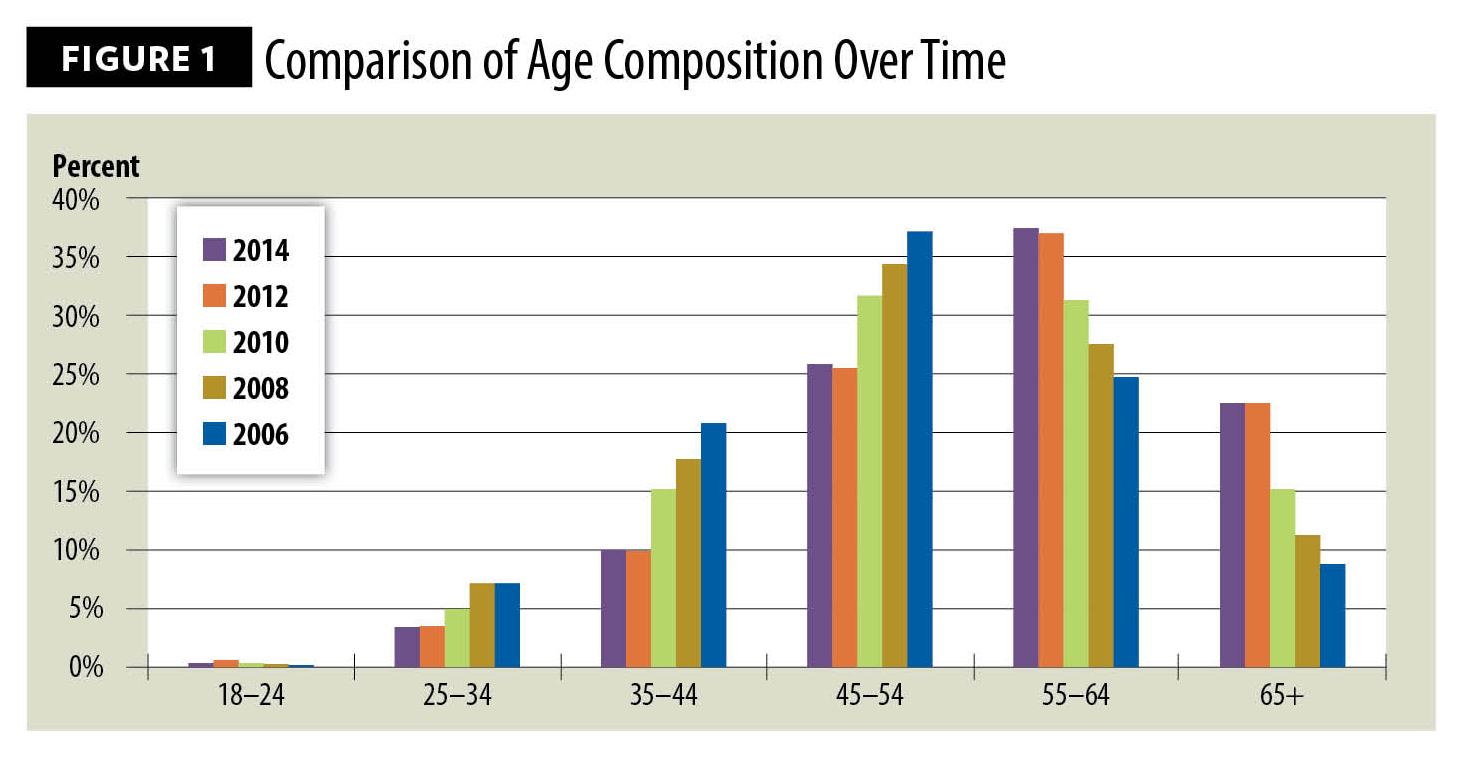

To start breaking down the results of the 2014 Profile of the Electrical Contractor, let’s begin with some basic demographics. Based on our sample, most electrical contractors are middle-aged, with an average age of 56.2 years, which is statistically unchanged from the 2012 survey. In fact, this year’s survey is the first since at least 2006 that the average age has held steady. Approximately 36 percent of respondents are between the ages of 35 and 54—unchanged from 2012 but down from 2010’s 47 percent (see Figure 1).

Retirements among the oldest ECs could be helping to slow the overall aging trend in the profession, along with an increase in hiring among firms in a range of sizes. Survey respondents from smaller firms (those with 1–9 employees) are older than those in larger companies, possibly because older ECs may have built up the knowledge necessary to hang their own shingles while spending their earlier career working for a larger company.

These age figures are likely related to the career level of the survey respondents, 78 percent of whom are company owners and top management. Twelve percent of respondents say they are master electricians (or hold an equivalent title), 4 percent are field managers and 5 percent say they have another title.

The majority of electrical contracting firms are smaller rather than larger, both in number of employees and in their revenue. Some 74 percent of firms interviewed have a staff ranging between one and nine employees, and 72 percent have annual revenues of less than $1 million. Both of these figures are statistically unchanged compared to 2010 and 2012 findings; they rose from 63 percent with one to nine employees in 2006 to 72 percent in 2010.

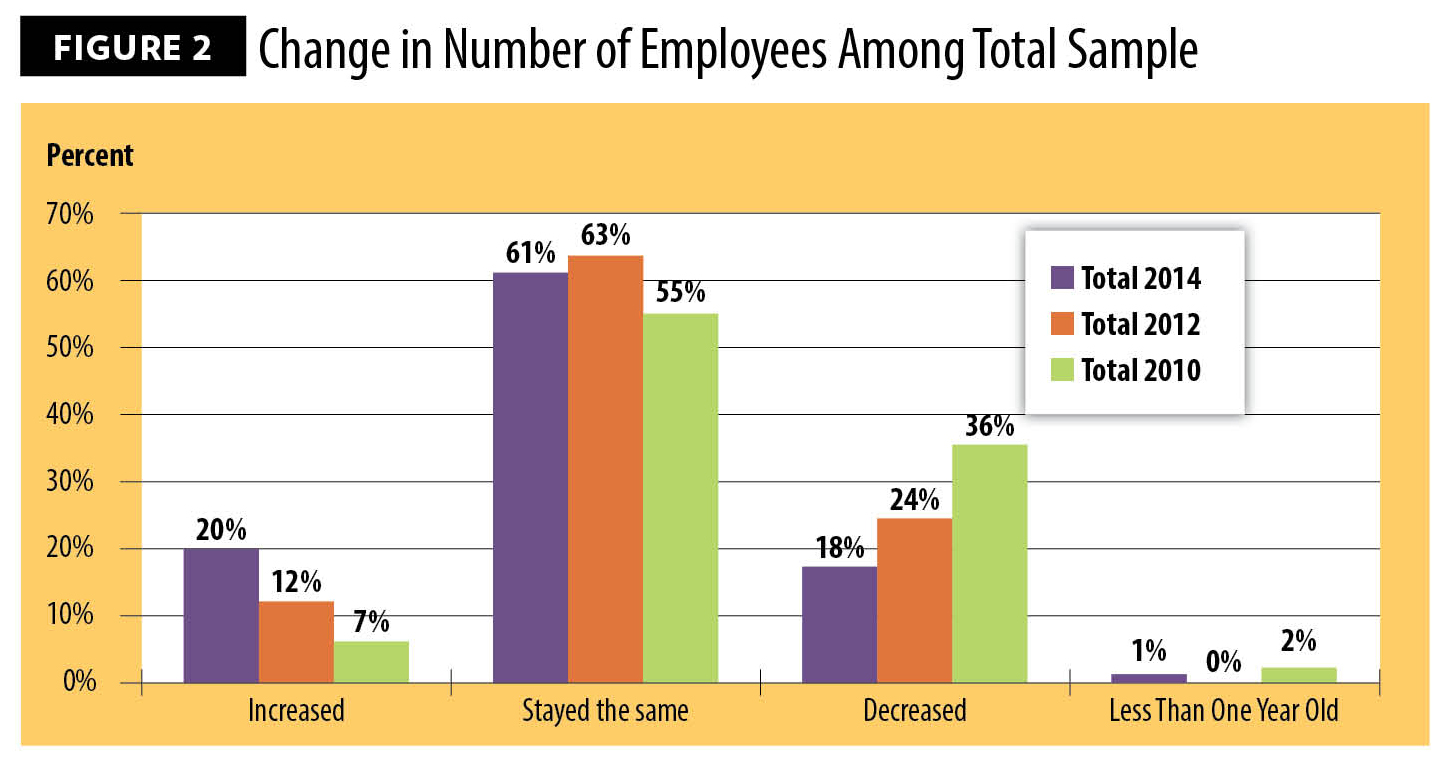

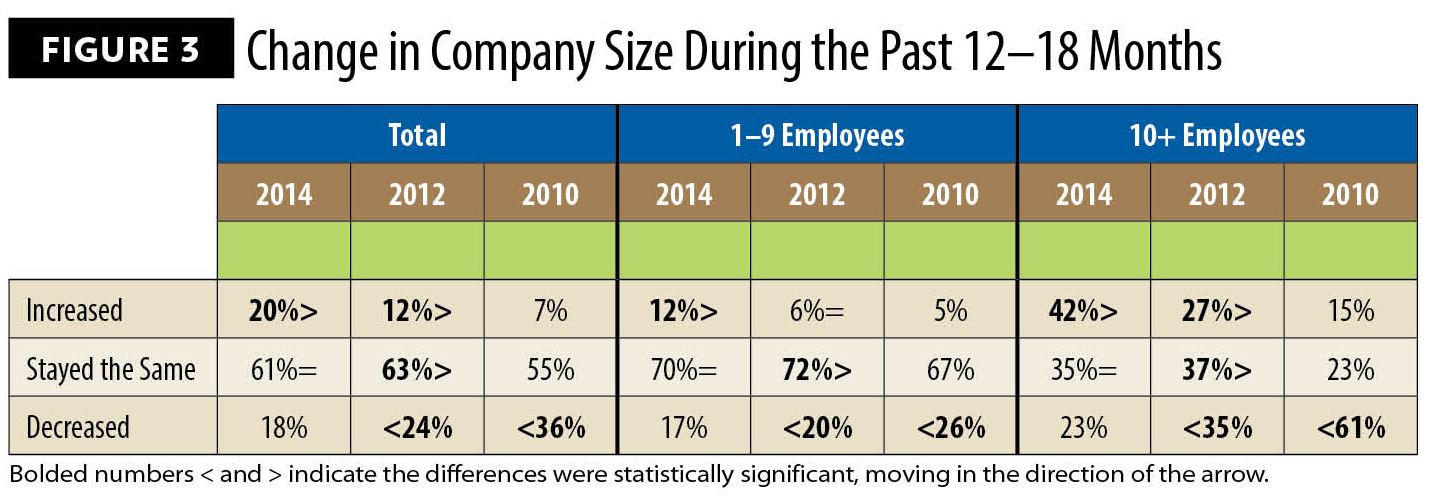

While it may seem a bit of a yawn that company sizes have remained steady in the last two years, there is some reason for hope behind the numbers. Twenty percent of firms added employees in the past 12–18 months (up from only 12 percent in 2012), and 18 percent lost employees (down from 24 percent in 2012 and an alarming 36 percent in 2010). When more companies are adding employees than shedding them, more ECs are taking home paychecks (see Figures 2 and 3).

Our researchers found some interesting facts about smaller firms (1–9 employees) in this most recent survey, which broke this group into the very small (1–4 employees) and the slightly larger (5–9 employees). Among these findings, the slightly larger firms exhibited significantly greater growth, with 34 percent reporting staff growth.

Throughout this report, we touch on some other areas where these not-quite-so-small companies resemble their much-larger counterparts.

What’s your educational background?

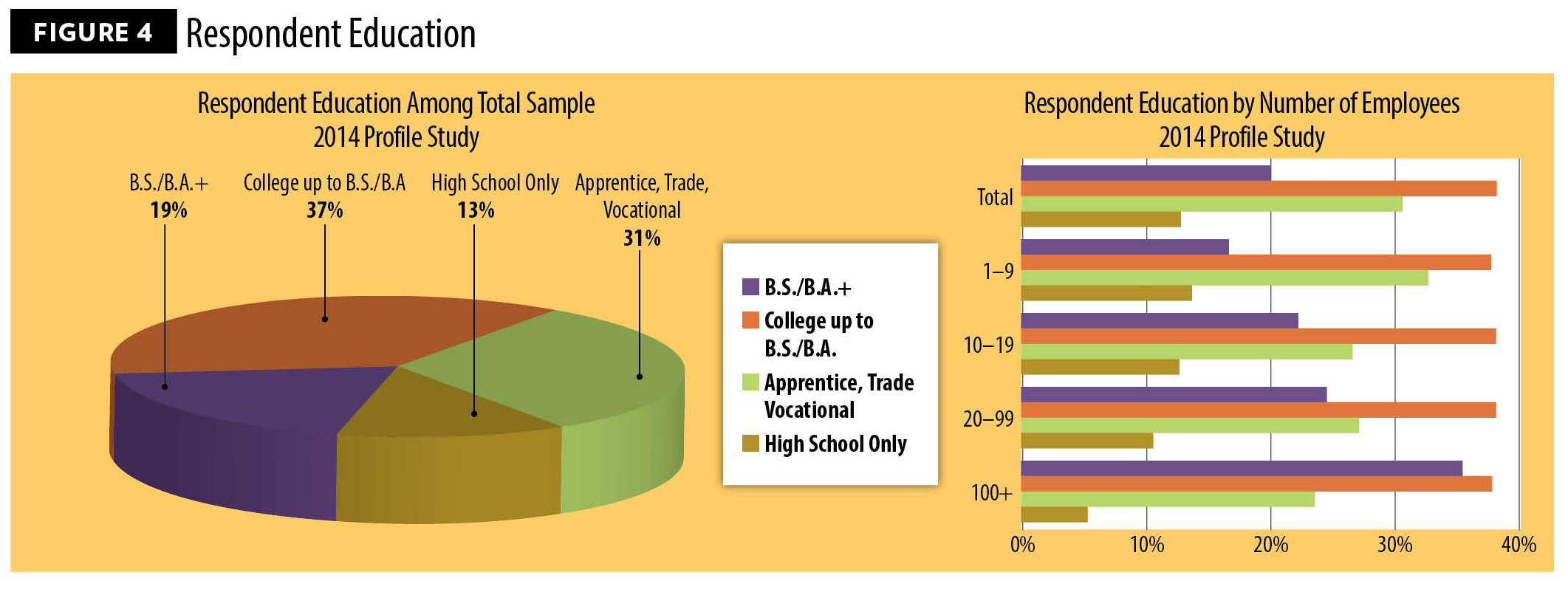

Not much has changed in the educational levels of responding ECs in the last two years. Across firm sizes, 56 percent of respondents have at least some college education, and 19 percent have at least a bachelor’s degree. These results are consistent with our last survey. Both college attendance and a bachelor’s degree (or higher) are more common for ECs working in firms of 10 or more employees than for those in smaller companies.

However, it seems overall education may be beginning to trend higher. Significantly fewer respondents reported having vocational, trade school or an apprenticeship as their highest level of education—31 percent in 2014, versus 34 percent in 2012. (By firm size, that figure is 32 percent in companies with one to nine employees and 25 percent in larger organizations.) No other single education level rose to balance out this drop-off. One possible conclusion: ECs who retired in the last few years may have fit into the non-college category. Further, educational levels among those in small firms rose slightly so that a significantly higher percentage now hold a bachelor’s degree or higher (see Figure 4).

What have you been up to?

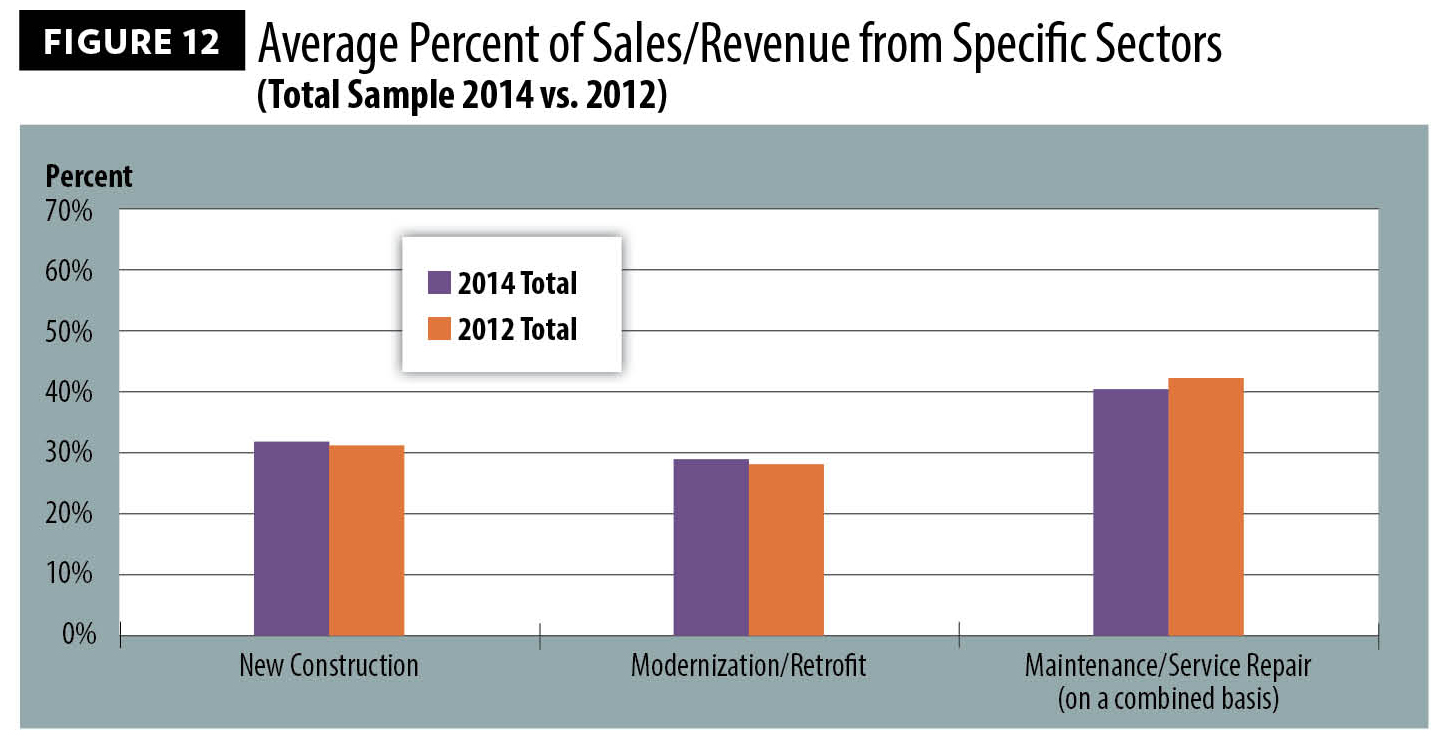

Where are today’s ECs finding work? The economy might be improving, but it’s been slow progress in the construction industry. It’s possible the economy is the reason maintenance/service and repair projects constitute 41 percent of contractor revenue, while new construction work remains stuck at a statistically unchanged 32 percent of revenue (see Figure 12).

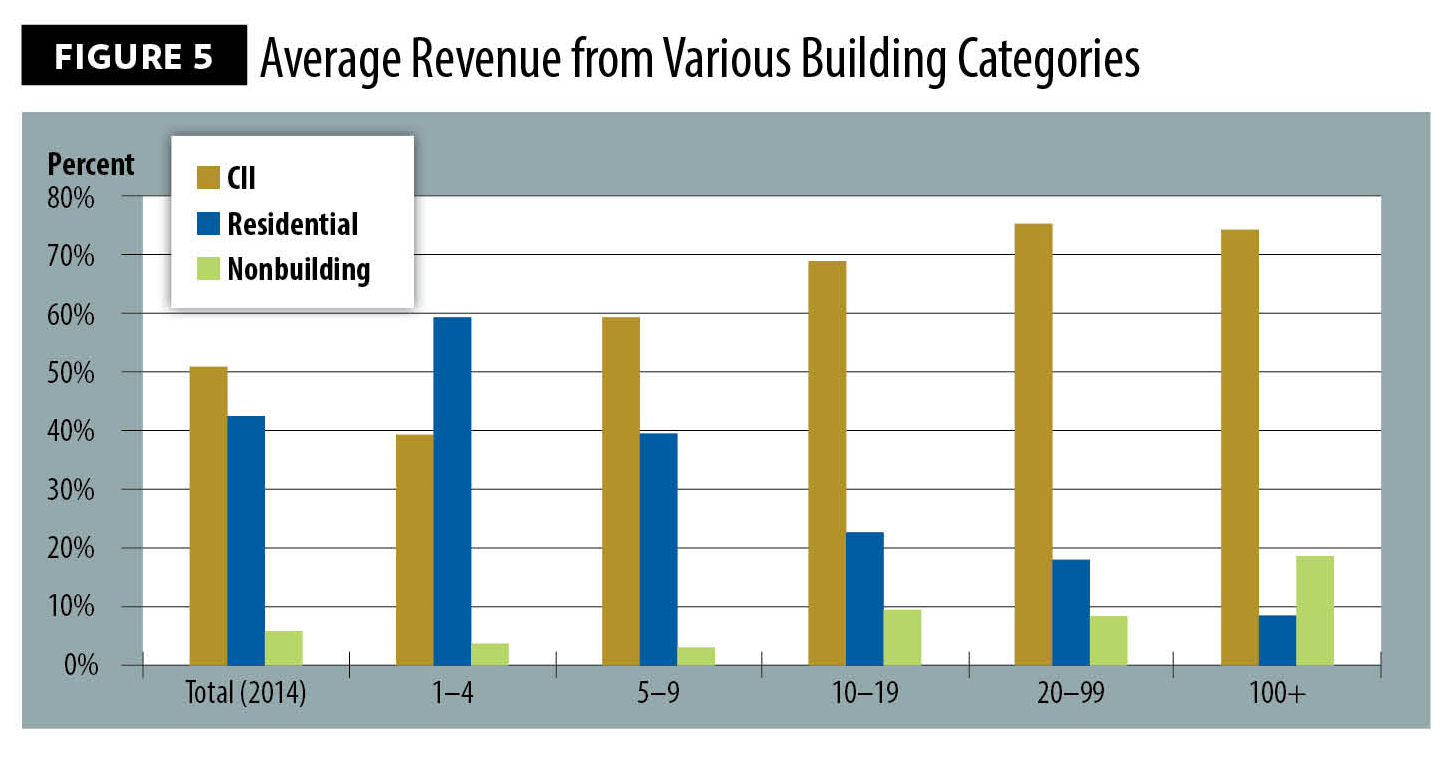

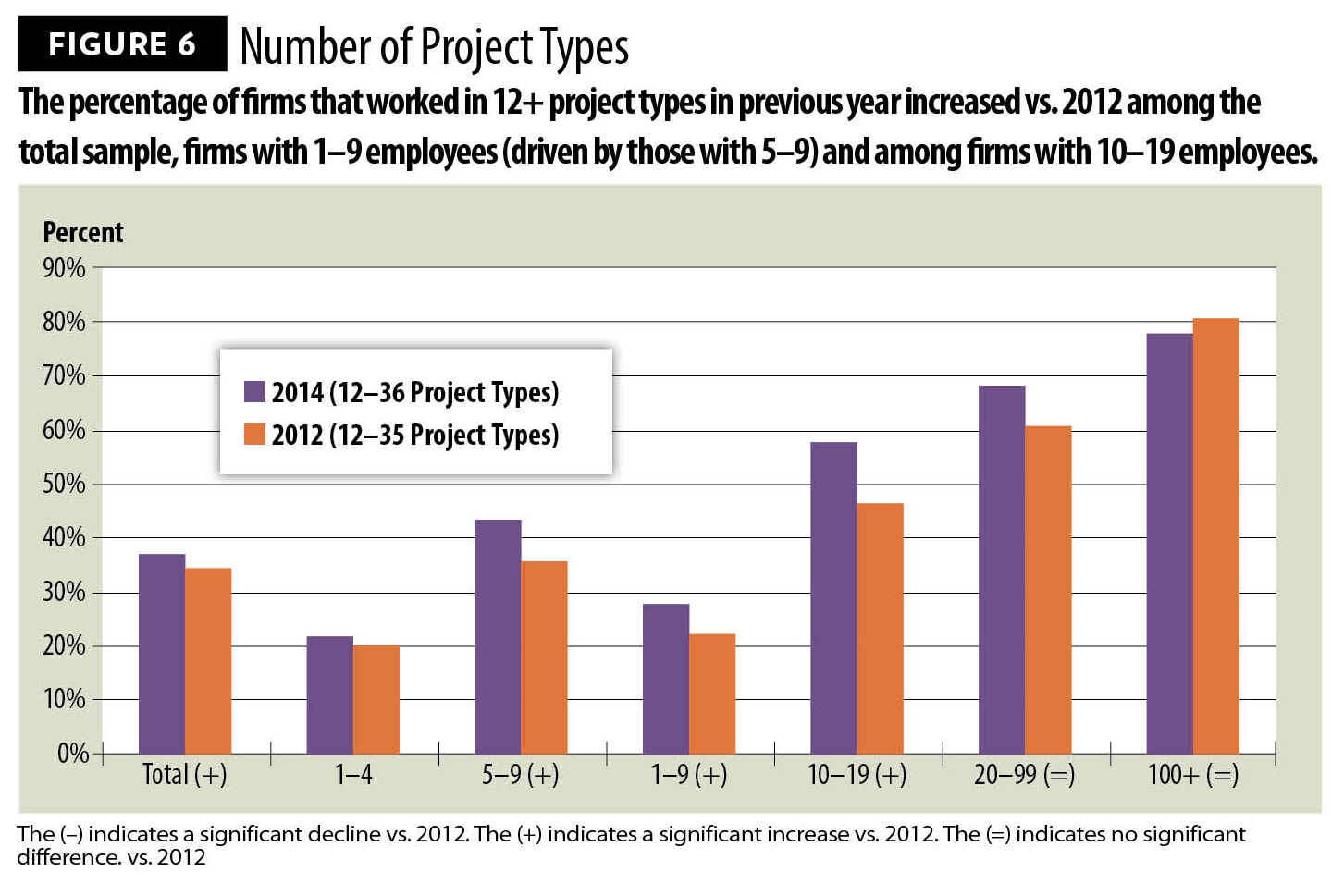

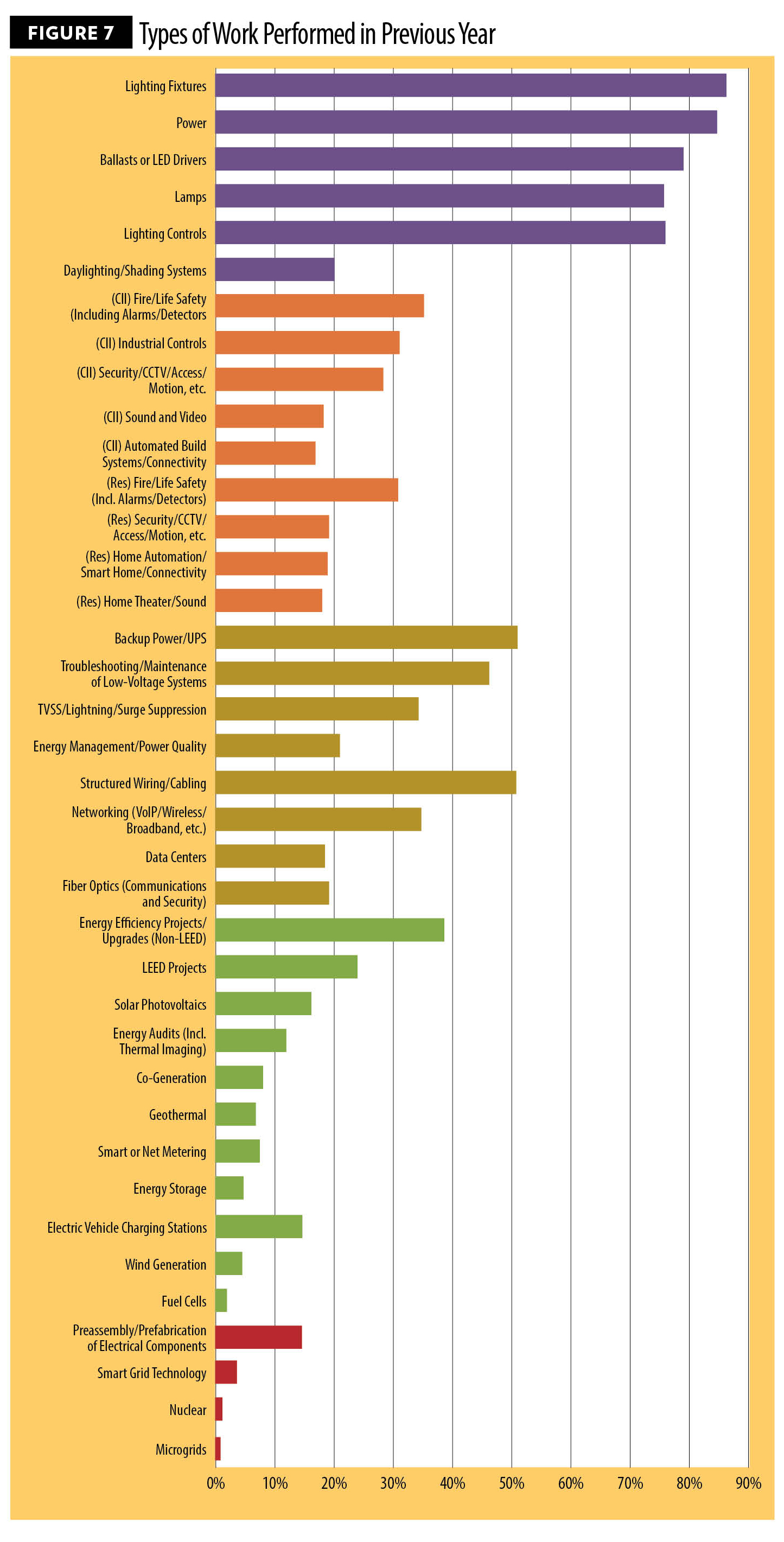

Smaller firms are more likely to get more revenue from residential work and larger firms from commercial/industrial/institutional (CII) (see Figure 5). Nonbuilding projects—assignments such as substation construction and transmission-line maintenance—also are more prevalent for larger companies. Our researchers polled respondents regarding their firms’ participation in any (or all) of a list of 36 different project types and found that ECs were working in more project types than in the past iterations of the survey (see Figure 6). For the first time, these project types were separated into residential and CII construction.

New to this year’s list of project types are daylighting/shading systems, troubleshooting/maintenance of low-voltage systems and microgrids (see Figure 7).

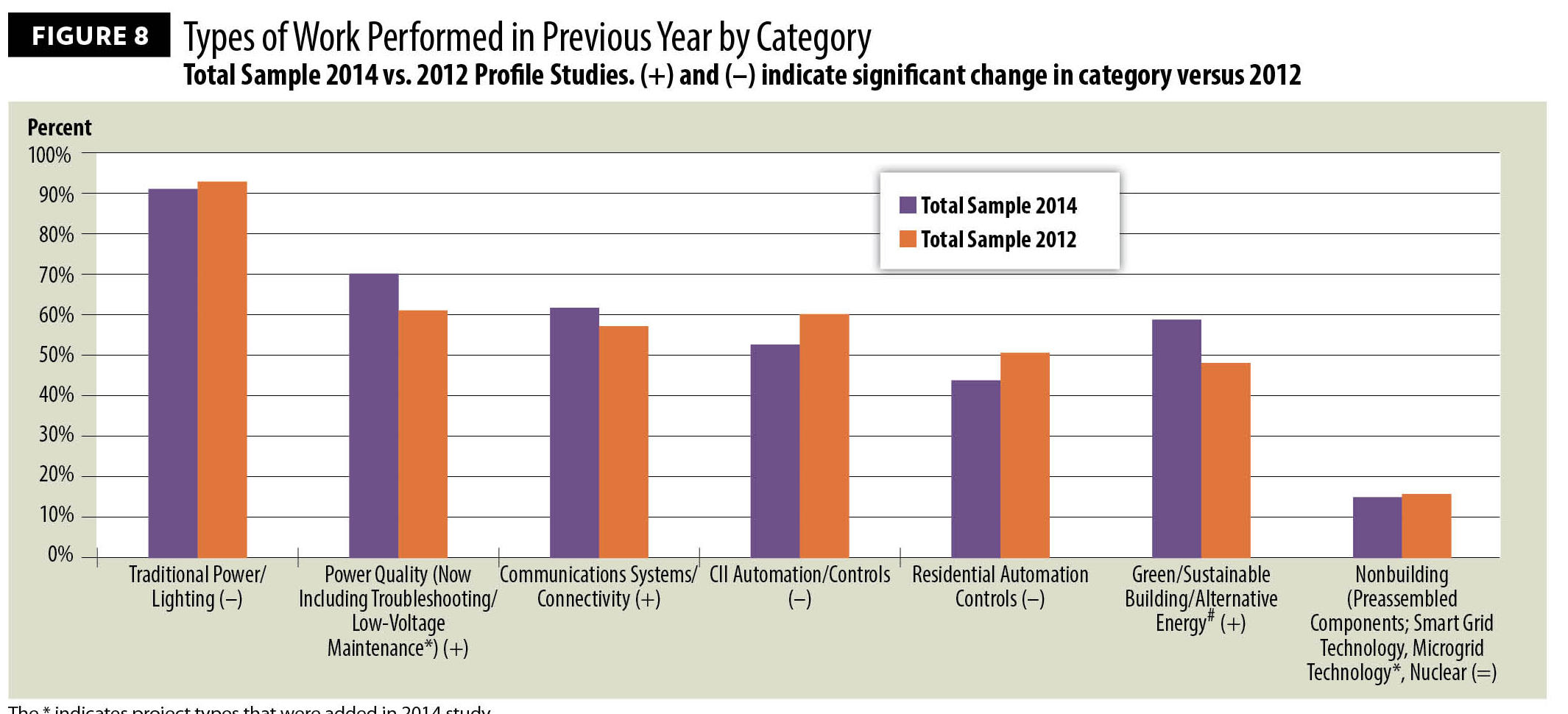

With the exception of traditional power and lighting, most types of electrical work are more likely to be done in a CII setting, but, because this is the first year questions were asked separately, trend information can only be drawn from combined residential/CII work. Some of the data is far from surprising, such as the fact that 92 percent of firms worked on power and lighting projects. Areas seeing growing interest include power quality (70 percent of firms did such work in the past year, up from 62 percent in 2012); communications systems; and the blanket category of green/sustainable technology/alternative energy (the latter categories rose significantly over 2012’s results) (see Figure 8).

In general, larger firms are involved in a wider range of project types than smaller companies, which is not a big surprise. However, this is one of the areas where splitting smaller companies into categories of 1–4 employees and 5–9 employees complicates such broad generalizations. Our researchers found that firms with 5-plus employees are more likely than smaller companies to work on power quality, communications systems/connectivity, CII automation/controls and the omnibus green-tech category.

In fact, the threshold for many types of work is moving down the company-size spectrum across the board, possibly the result of diversification strategies developed in the face of economic challenges. This tipping point is now 10-plus employees (or even 5-plus), instead of 20–99 employees or 100-plus. Two years ago, only seven project types were on the list for firms with 10+ employees; this year’s list contains 20 project types.

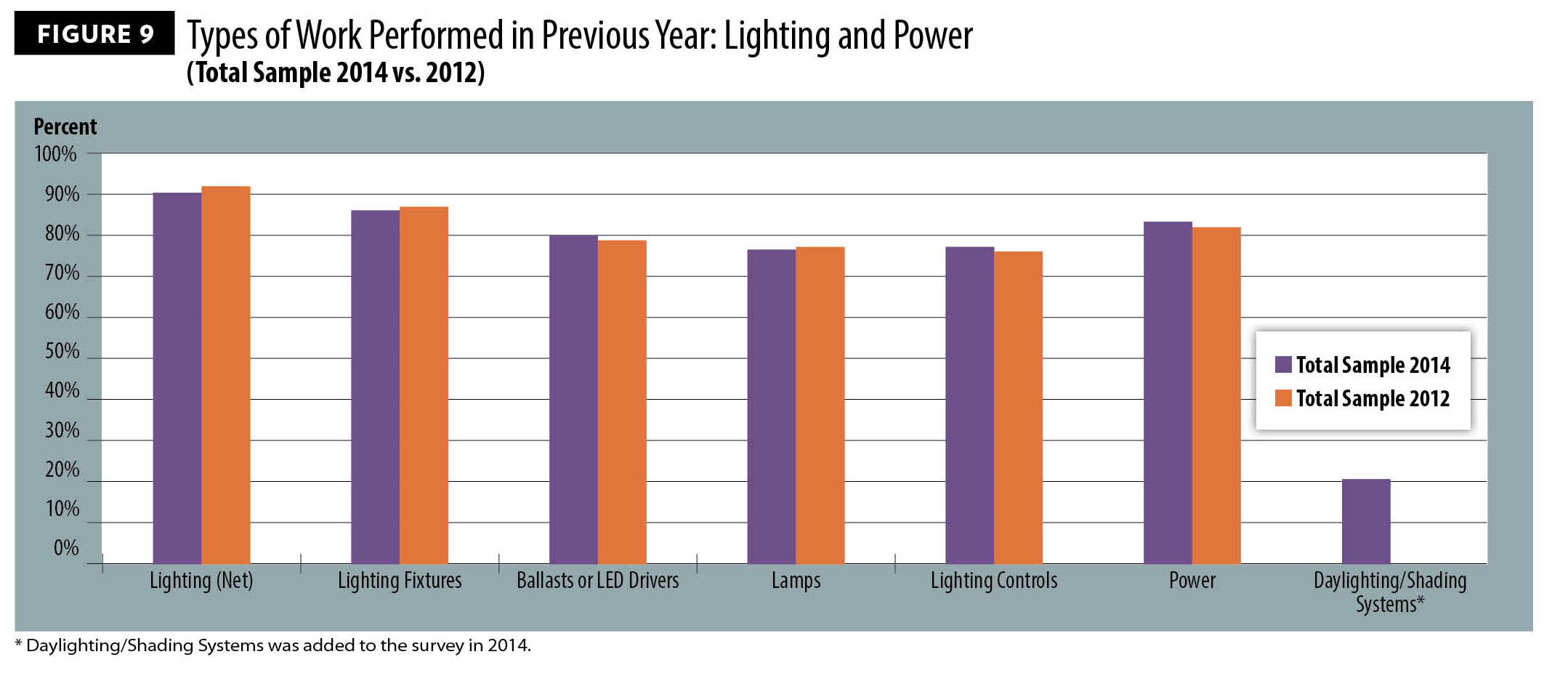

As shown in Figure 9, lighting continues to be a strong category for ECs, across the full spectrum of lighting systems. Data from a new lighting subcategory, daylighting/shading systems, adds further evidence that efficiency is becoming more important to their building-owner customers. Though 2014 is the first year our researchers have asked about daylighting and shading system business, already more than 20 percent of respondents reported working on related projects (see Figures 7 and 9).

Seeing green in green tech

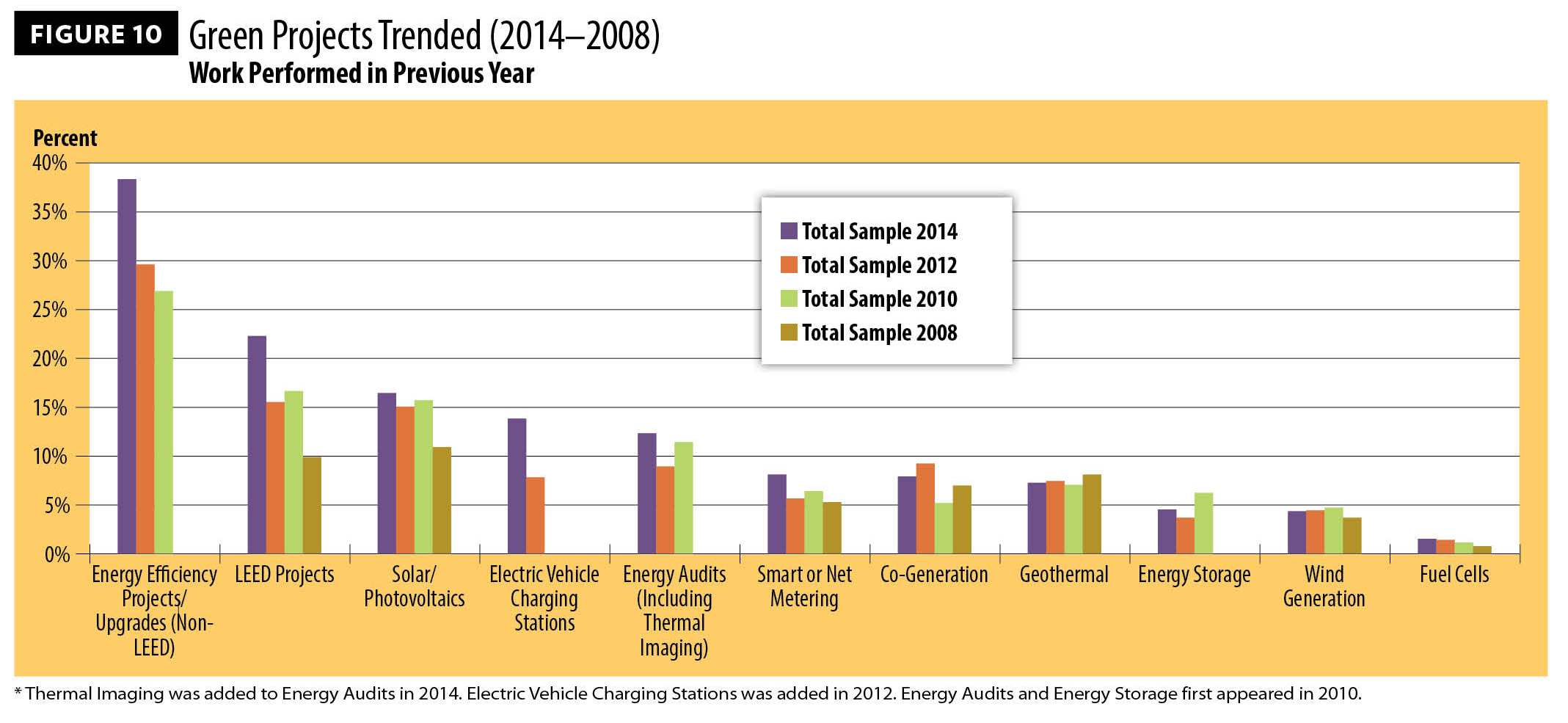

Included among the fastest growing project types are five of the 11 subcategories of green technology that have grown significantly since 2012. Topping these are LEED projects and non-LEED energy-efficiency upgrades; combined, 44 percent of surveyed ECs said they had performed one or both of these types in the last year. That’s up from 2012’s 34 percent. Non-LEED work, which could include simple lighting upgrades to more-sophisticated sensor and controls implementations, led this category, climbing to 38 percent from 30 percent in 2012. LEED-related projects rose to 22 percent from 15 percent two years ago (see Figure 10).

Energy audits, obviously not a new-construction category, also posted significant gains. Our researchers suggest this growth may be partially due to 2014’s inclusion of thermal imaging.

EC customers also appear to be more interested in accommodating efficiency on the road, with 2014’s survey showing a significant uptick in work with electric vehicle charging equipment. While the 14 percent of respondents who reported working on such projects might seem like a small number, that figure represents a 75 percent increase over 2012’s figure of 8 percent (see Figure 10).

Areas holding steady include wind and geothermal work.

Low-voltage buzz

Another area where a number of companies see growth potential is low-voltage projects in systems integration or data/telecom centers. About 40 percent of surveyed contractors work for companies involved in such projects. This figure is unchanged from 2012, but, in a question first asked this year, researchers found that 7 percent of companies (including 20 percent of companies with 10-plus employees) have a separate low-voltage division, and an additional 6 percent (including 9 percent of 5–9-employee companies) plan to set up such a division.

The added interest in low-voltage work also may play a factor in the uptick in power-quality work noted in this year’s survey. This category, which now includes troubleshooting and maintenance of low-voltage systems, provided at least some work for 70 percent of responding firms in this year’s survey, up from 62 percent in 2012 (see Figure 8).

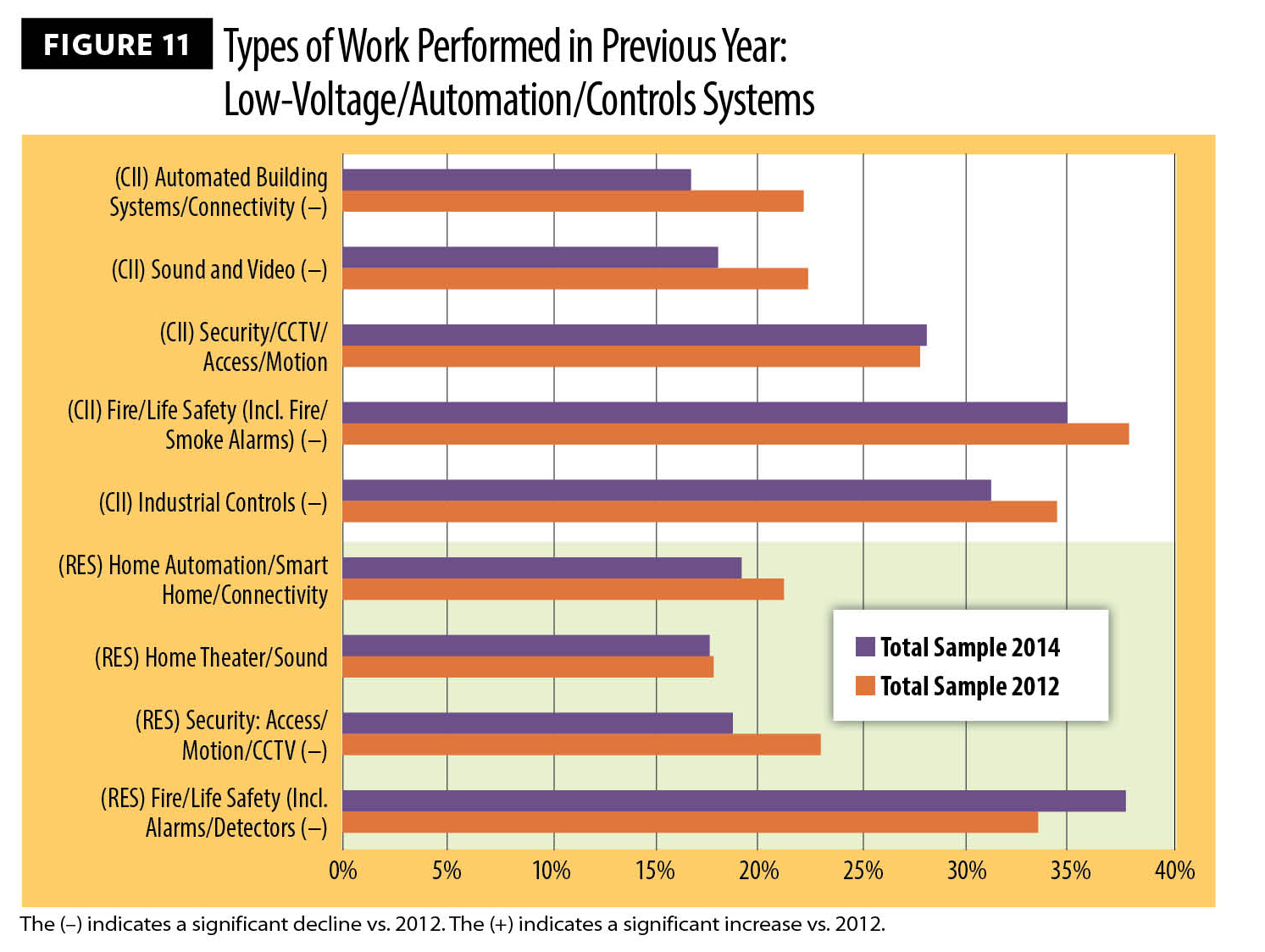

Automation and controls systems—called out in their own category separate from low-voltage—posted declines this year in both residential and CII applications. Interestingly, the fire/life safety subcategory was noted as a growth area in 2012, versus 2010’s results. Residential security business has also declined in the last two years, which might relate to the drop in new-construction work. However, there’s new competition for this business from cable TV companies bundling wireless home-security systems into larger Internet/cable TV packages for residential customers over the last two years.

Despite the small losses, numbers in the 20–35 percentile are still hefty, showing that many ECs are still working in fire, life safety and security capacities (see Figures 7 and 11). In 2012, when there was less electrical distribution work, perhaps more ECs sought out more low-voltage systems work. Now, with the electrical distribution work returning, they have spread their types of work, as the survey showed.

An uptick in total communications and systems/connectivity work provides some evidence against the notion that stagnant new construction is the sole reason for the slight drop-off in fire/life safety and security business. For example, the category of structured wiring/cabling—work most commonly completed for new-construction projects—posted small but statistically significant gains in this year’s survey. Also seeing growth were broadband/wireless/VoIP and fiber optics for communications and security. So ECs are seeing increases in low-voltage and fiber optic networking assignments, just not as strongly in fire/life safety and security projects specifically (see Figures 7, 8 and 11).

Revenue resources

Our Profiles look separately at the kinds of projects in which ECs participate and where these respondents earn their revenue. In the broadest terms, tracked revenue sources and percentages remain unchanged compared to 2012 in the three largest categories we study (see Figure 12):

- Maintenance/service or repair—41 percent

- New construction—32 percent

- Modernization/retrofit—27 percent

A range of project types span these three sectors, with electrical/power distribution responsible for 44.6 percent of ECs’ revenues, on average. This is a step up from the 39 percent total in 2012, and it represents the first uptick in this category since 2004 when it made up 69 percent of revenues. New construction is not the cause—as noted, that sector has remained flat since 2012. However, our researchers suggest it may be tied to the increase our respondents noted in smart grid technology or work in microgrids, which is a new category this year.

Systems integration also took a step up in importance. Losing ground were industrial systems and energy management/power quality in terms of revenue, though it may be because ECs are working in an increased number of categories of electrical work than ever before. Their revenue has spread out from traditional sources into a broader range of work types.

When firm size is looked at, smaller firms consider electrical/power distribution significantly more important, representing 47 percent of revenue, versus 38 percent for larger firms with 10 or more employees. Lighting and backup power are also more important to the smaller companies.

The percentage of revenue derived from residential versus CII work tracks directly with company size. Residential projects dominate the bottom line for ECs in companies with one to four employees. Once firms top five employees, however, CII work takes the top spot and becomes steadily more important as companies reach 100 employees (see Figure 5).

The shift from residential to CII as the dominant revenue contributor at five or more employees was especially notable to our researchers, as it continues a trend seen over the last three surveys.

“In 2010 and 2012, we hypothesized that firms with 10+ employees may now be the critical mass to work on CII projects,” the researchers state in a special note. “In 2008, the critical mass appeared to be 20+ employees. In 2014, however, the critical mass may be firms with 5–9 employees.”

Across the board, the percentage of revenue derived from residential work increased in the last two years, as the percentage from CII declined. Interestingly, and perhaps as a positive sign in the housing market, the residential revenue increase is driven more by single-family than multifamily housing. However, our researchers consider the difference between the categories’ performance to be “directional” rather than “significant.” In fact, single-family housing accounts for the single largest revenue source for all ECs, responsible for 38 percent of that total.

In the CII category, commercial construction, at 27 percent of revenue, beats out both industrial (14.1 percent) and institutional (9.1 percent) sectors. Industrial revenues dropped significantly among the total sample of firms of all sizes, compared to 2012 figures, in large part because of a drop in their contribution to the smallest firms’ bottom lines.

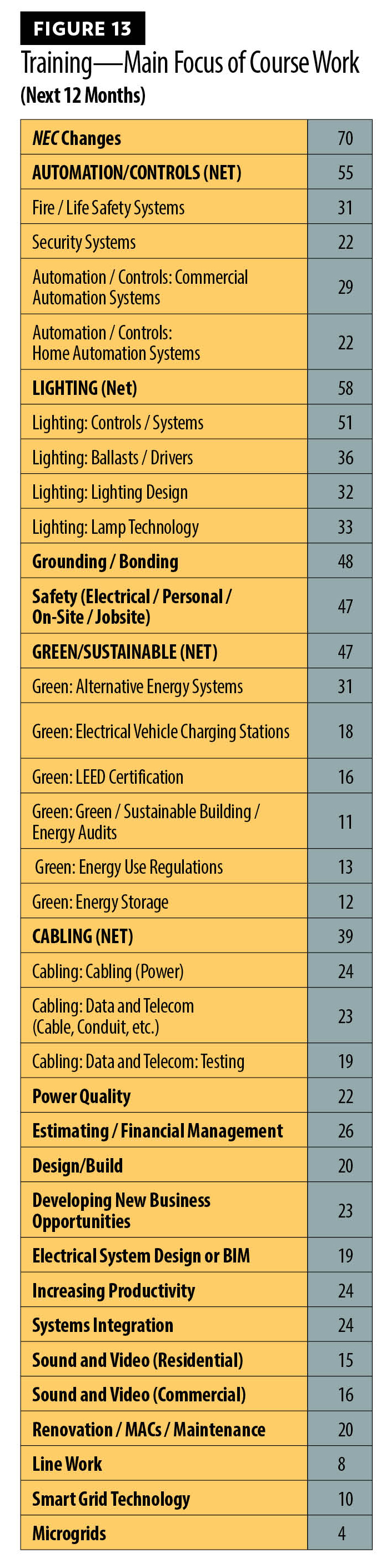

Training plans

With even smaller firms diversifying into new specialty offerings, it makes sense that training would be a part of many of your plans. Similar to 2012’s survey respondents, 75 percent of this year’s participants say that they, or someone in their firm, have taken training in the last 12 months. A similar percentage also say they or someone in their firm are planning to take training in the next 12 months.

It’s not a surprise that National Electrical Code changes are the No. 1 topic in future training plans, especially given that the updated 2014 edition of this EC bible was released just last October. Not surprising either: safety training is also important to ECs (see Figure 13).

The following are also high on the list of future study topics:

- Lighting (mentioned by 58 percent)

- Automation and/or controls (55 percent)

- Grounding/bonding (48 percent)

- Safety issues (47 percent)

- Green/sustainable issues (47 percent)

A range of high-tech issues ranked significantly higher in ECs’ future plans than they did in the list of topics studied in the previous year. These include a number of green-tech subject areas, including electric vehicle charging equipment, LEED certification, alternative-energy systems and energy storage.

Notably, for building pros aiming to thrive in an economy that’s still slow to bounce back, our EC audience is also looking to brush up on several business topics, including estimating/financial management, business development and methods for increasing productivity.

Organizations and associations are the most popular resource for training, followed closely by manufacturer-sponsored programs. For those organizations developing courses, it’s important to note that hands-on approaches win hands-down as the preferred learning method. Some 58 percent of respondents chose this option over classroom, one-on-one, self-paced videos and webinars.

But wait, there’s more!

We found out a lot more about how electrical contractors are working today, including the project arrangements they’re most likely to participate in—such as design/build, design/build/assist and more traditional bid arrangements—and how much flexibility they have in specifying and substituting products. But that information is more than we can fit into a single article, so our August issue will contain more coverage of the 2014 Profile of the Electrical Contractor. Look for it next month—there’s a lot more to learn.

METHODOLOGY

The survey was conducted by postal mail and through the Internet among a random sample of ELECTRICAL- CONTRACTOR subscribers. The survey was fielded in March 2014, and, as of May 7 (the deadline for the July 2014 article), 2,722 completed surveys were received—1,214 through the Internet and 1,508 through postal mail.

Each respondent who received the survey through the Internet was sent two follow-up emails. However, follow-up mailings were not made to non-responders in the postal mail sample. An incentive was offered for participation in the survey: For each completed survey, ELECTRICAL CONTRACTOR magazine would contribute $5 to charity.

The Internet option was first introduced in 2004. In 2004 and 2006, the proportion of surveys completed through the Internet versus postal mail was approximately 60/40. In 2008, 2010 and 2012 the proportion was closer to 50/50. In 2014, the data were weighted to equalize the influence of the two modes so that it was in line with the 50/50 split.

As was the case since 2004, the survey was produced in different versions. Starting with the 2008 Profile study, there were four versions of the survey, which differed from each other on fewer than 10 questions. The first four pages were common to all versions, while the differences among the versions occurred on the last page. The major difference was that, in the Internet portion, respondents were required in almost all cases to have percentage questions add to 100 percent. In addition, a few media-related questions were asked only in the Internet version.

In 2014, to accommodate a longer list of questions while, at the same time, lessening the burden on the respondent, the survey was shortened from five print pages to four. To accommodate all of the questions, the survey was produced in eight versions (up from four). This required a much larger sample size so that each of the questions would be asked of a large enough sample to allow for analysis—particularly by subgroups.

Tables and figures contained in this article come from the data generated by this year’s Profile of the Electrical Contractor Survey, which was conducted by New York-based Renaissance Research & Consulting Inc. (www.renaiss.com), an independent marketing research firm that has, as one of its specialties, market research for the construction industry.

Statistics

The margin of error on the total sample of 2,722 is ±1.5 for percentage points around 50 percent. That is, we are confident that a reported 50 percent will fall between 51.5 percent on the plus side and 48.5 percent on the minus side 90 percent of the time. Please note that different rules apply to testing of averages, which were also tested at the 90 percent level of confidence and are noted in the report.

About The Author

ROSS has covered building and energy technologies and electric-utility business issues for more than 25 years. Contact him at [email protected].