You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

What happened to the recovery experts predicted in 2010? “That early stage of recovery has been pushed back,” said Robert Murray, vice president of economic affairs at McGraw-Hill Construction.

The slow recovery predicted for the end of 2009 and into 2010 will instead begin in earnest in 2011. It might take a few years. With the depths of declines in most sectors during the “Great Recession,” experts predict double-digit growth in some areas in 2011. However, that growth must be interpreted within the context of some of the greatest declines in a generation. This recession was the longest and deepest economic crisis since the 1930s, so its impact will linger for years. One running theme throughout this article is that there was nowhere for the numbers to go but up.

“Construction is the last sector of our economy that is still stuck in recession,” said Kermit Baker, chief economist for the American Institute of Architects (AIA). Now the recovery begins.

This article delivers an economic and construction forecast for 2011. The information that follows comes from various resources. Chief among them is the Oct. 28–29, 2010, McGraw-Hill Outlook 2011 Executive Conference, and the Oct. 21, 2010, Market Insights Webcast “After the Fall: When and Where Construction Will Rebound,” hosted by Reed Construction Data.

Let’s first examine the macroeconomic landscape to discern where construction fits into that larger picture. After looking at the 30,000-foot view, we’ll drill down into more specific trends to find areas of concern and opportunity.

DOUBLE DIP

Economists fear the U.S. economy is flirting with a double-dip recession, leaving top forecasters rather nervous about their 2011 prognostications. In addition, because so many thought leaders missed on the rate of growth in 2010, they are being much more cautious about their predictions for 2011. As the overall economy teeters on the brink of a double-dip recession, economists and executives are wary of what could happen if anything—oil prices increase, a terrorist attack, another financial market lockup—sways the balance in one direction or the other. The economy is that fragile right now (Figure 2).

In the November/December 2010 issue of ABA Trust & Investments magazine, Keith Leggett, vice president and senior economist for the American Bankers Association (ABA), wrote that recent research from the San Francisco Federal Reserve indicates there is a 50 percent probability that the U.S. economy will slip into another recession within the next 18 to 24 months. He further wrote that the current level of jobless claims is more typical of a recession than one year into a recovery.

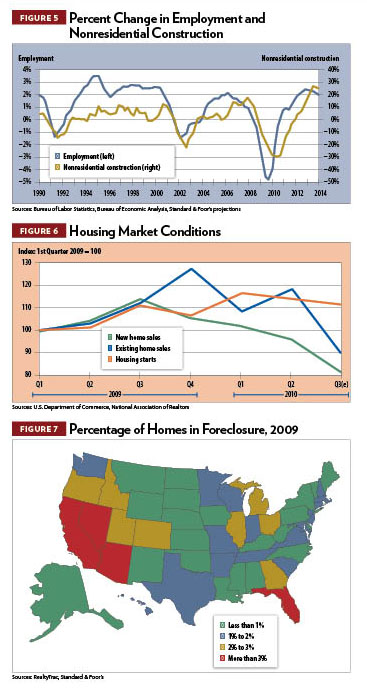

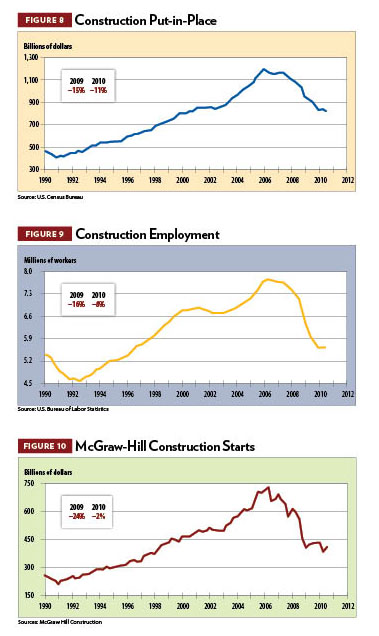

Construction was hit harder than most sectors when it comes to unemployment (Figures 3, 4 and 5). According to the AIA’s Baker, construction jobs fell by almost 27 percent during the recession (Figure 4).

According to Grant Thornton LLP’s 17th Bank Executive Survey, conducted in conjunction with Bank Director magazine in September 2010, only 15 percent of bank executives believe the U.S. economy will improve in the next six months. A quarter of those bank directors believe it will actually get worse. This is a big swing from six months prior, when 45 percent said they expected the economy to improve. While the financial services industry thinks a double dip is a bona fide possibility, other economists are a bit more optimistic.

“The worst of the recession is over,” said Kathleen M. Camilli, president of Camilli Economics, speaking at the McGraw-Hill Outlook 2011 Executive Conference. “We are well into the first year of recovery.”

At the same conference, Keith Fox, president of McGraw-Hill Construction, agreed. “We believe the worst is over,” he said.

Camilli said the recession appears to have ended in the third quarter of 2009, but the housing sector had been in a recession for three years and has taken longer to show signs of recovery. That now seems to be stabilizing as well, she said.

FORECLOSURE WOES

Saying “the worst is over” was popular in late 2009, too, but the fluctuations in the housing inventory trumped those forecasts. Between an overabundance of existing housing inventory, a burgeoning foreclosure market, and a lurking shadow inventory of potential home sellers, the housing stock has been a steady drag on the entire economy (Figure 6).

“Foreclosures are a huge problem because they keep adding to the inventory,” said the AIA’s Baker during the McGraw-Hill conference (Figure 7). Conservatively, he said, there are 1 million units in the housing sector that need to be sold off before the housing market can turn the corner toward recovery. “We were building more homes than we needed for a long time,” he said.

According to RealtyTrac, which produces a monthly U.S. Foreclosure Market Report, one in every 389 U.S. housing units received a foreclosure filing during October 2010. October marked the 20th consecutive month in which 300,000 U.S. homeowners received a foreclosure notice. Those numbers would have been higher, but the fallout from the recent “robo-signing” controversy sparked a foreclosure moratorium among mortgage lenders.

“A housing recovery is taking place but will be choppy at times, depending on the duration and impact of a fore-closure moratorium,” said Lawrence Yun, National Association of Realtors (NAR) chief economist, in an Oct. 25, 2010, statement. According to the NAR, existing home sales, including single-family houses, townhouses, condominiums and co-ops, jumped 10 percent in September from the previous month but remain about 19 percent below the 5.6 million-unit pace from September 2009, when the $8,000 first-time homebuyer tax credit spurred sales. Perhaps that tax credit supplied some false hope for overall growth.

Jim Haughey, chief economist of Reed Construction Data, said during the Reed-sponsored webcast that the lingering foreclosure problem could add a couple more years to the normal recovery cycle.

“It’s not until the second half of 2011 that we will see any type of growth,” said McGraw-Hill’s Murray.

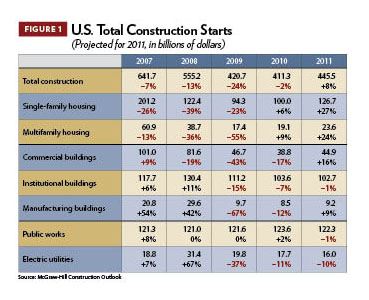

If you examine solely “construction put-in-place” data from the U.S. Census Bureau and construction employment figures from the U.S. Bureau of Labor Statistics, Murray said the downturn is still underway (Figure 8). The Census Bureau predicted that construction put-in-place would fall 11 percent in 2010, after falling 15 percent in 2009. As far as construction employment is concerned, a 16 percent decline in 2009 was followed by a 9 percent dip in 2010 (Figure 9). Those figures coincide with McGraw-Hill’s construction starts information, which declined by 24 percent in 2009 and only by 2 percent in 2010. However, stabilization must be taken in perspective. The 24 percent dip in 2009 was the steepest drop in the history of the McGraw-Hill construction starts series. The numbers had nowhere to go but up (Figure 10).

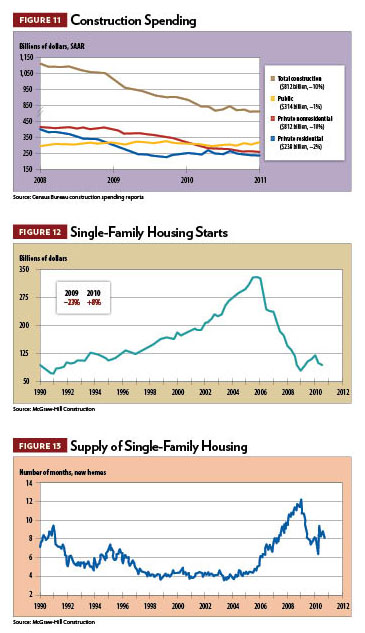

Clearly, the destruction caused by the recession is unprecedented in modern American history. It has affected all construction markets, some harder than others (Figure 11). No one was harder hit than the residential construction market—a very significant market for electrical contractors (Figures 12, 13 and 14). Let’s take a closer look at each of the construction areas, beginning with the residential market.

RESIDENTIAL

As a presenter during the Reed Construction Data Webcast, the AIA’s Baker said he thought the housing market hit its bottom in early 2009, only to see it slide again in the second quarter of 2010. Again, this is why leading industry experts worry about the looming possibility of a double-dip recession.

According to Reed’s Haughey, in housing starts, the industry endured a flat period at a very depressed level for about two years.

“We’re seeing some stabilization in the (housing) starts part of the market,” Haughey said. He added that by the end of 2012, the market would not quite return to its 2007 level, which was a dip from 2006. Haughey predicts a 10.1 percent increase in residential construction spending in 2011 and another 21.2 percent increase in 2012.

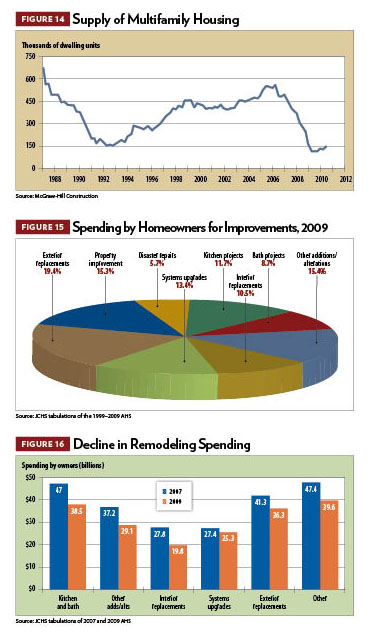

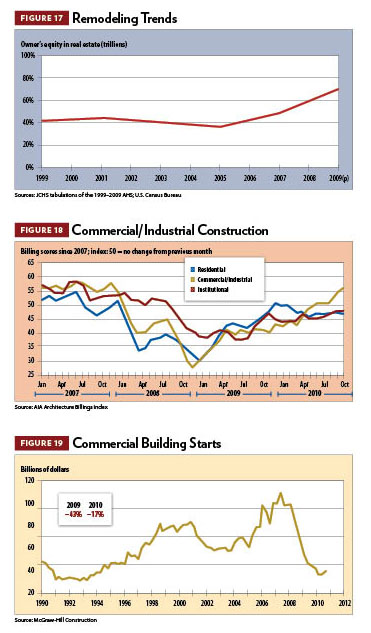

In single-family housing starts, McGraw-Hill’s Murray predicted a 4 percent increase in 2010 and a 25 percent increase in 2011 (Figure 12). His forecast is based on what he thinks is a combination of a shrinking inventory of new homes (Figure 13), historically low mortgage rates, and demographic demand, aided by the “echo boom” generation moving into their 20s.

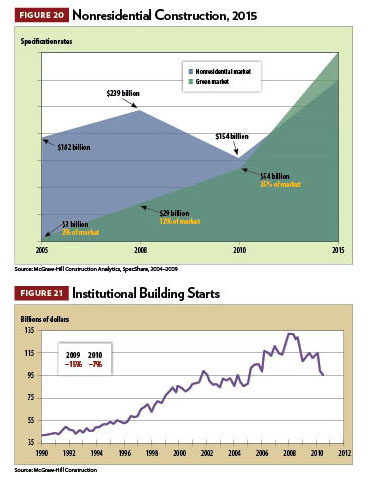

In multifamily housing (apartments and condominiums), Murray predicts a 23 percent growth spurt in 2011 to 170,000 units after a 5 percent increase in 2010. Those increases come on the heels of a combined 89 percent freefall in 2008 and 2009. Again, this reiterates the point that there’s nowhere to go but up in this sector (Figure 14).

Haughey envisions total housing starts (both single- and multifamily) combined to grow at a 24.7 percent clip in 2011 and by another 44.1 percent in 2012. He sees this trend as correcting the declines of the recent past.

All homebuilding sectors were clearly weak in 2009 and 2010, but there are some signs of hope, particularly in remodeling, according to data from the AIA’s Home Design Trends Survey.

Remodeling

Remodeling, which endured a significant decline during the recession (15 to 20 percent), appears to be recovering and should gain momentum in the coming months. That sounds significant until you understand that new homebuilding was down 75 percent during the recession. The greatest fall-off in remodeling came from high-end discretionary projects, Baker said. He said that remodeling niches, such as energy retrofits and renovating distressed properties, helped revive a weak home improvement market (Figures 15, 16 and 17).

“Houses built prior to 1973 are key targets for energy retrofits,” he said.

When you compare remodeling spending from 2007 and 2009, you can see a clear drop-off in discretionary spending in various categories. Kitchen and bath remodeling dropped from $47 billion to $38.5 billion, while interior replacements dipped from $27.8 billion to $19.8 billion. Exterior replacements slumped from $41.3 billion to $36.3 billion, and other additions/alterations declined from $37.4 billion to $29.1 billion (Figure 16). The most stable category in the remodeling market during that cycle was systems upgrades, which only fell from $27.4 billion to $25.3 billion. That is good news for electrical contractors who perform systems work.

According to data from the Joint Center for Housing Studies (JCHS) at Harvard University, the leading indicator of remodeling activity points to 11.8 percent growth in the first quarter of 2011 and another 12.8 percent increase in the second quarter.

Another point Baker made was about the residential market share that remodeling held in recent years. Remodeling was traditionally about 40 percent of the residential construction market, but the share grew to almost 70 percent during the downturn in the economy (Figure 17).

Now that we have a grasp of the residential market, let’s drill down into the nonresidential market to see what obstacles and opportunities lie within.

NONRESIDENTIAL

While the residential market took the biggest hit over the last few years, the nonresidential, or commercial/industrial/institutional (CII), market wasn’t immune. It, too, endured rough times (Figure 18).

Commercial

While commercial building construction (stores and shopping centers) reached an all-time high in 2007, the sector endured sharp declines in 2008 (34 percent), 2009 (53 percent) and in 2010 (17 percent). In terms of square footage, Murray expects 19 percent growth in 2011. In warehouse construction, Murray anticipates 30 percent growth in 2011. That sector endured major declines in the three previous years—25 percent in 2008, 66 percent in 2009 and 32 percent in 2010. Reed Construction Data’s Haughey predicts a 4 percent increase in retail space construction in 2011 and another 12 percent increase in 2012.

McGraw-Hill’s Murray also said hotels would experience a 13 percent increase in 2011. The hotel sector sustained a 64 percent decline in 2009 and another 37 percent dip in 2010. The 13 percent projected growth for 2011 is leveling off for that segment.

It might sound a bit odd and inappropriate, but natural disasters were a growth engine in this sector. Restoration projects in the hospitality industry, namely the flood restoration of the Opryland Resort Hotel & Grand Ole Opry in Nashville, Tenn., and the Hurricane Katrina rebuild of the Hyatt Regency Hotel in New Orleans, collectively account for $272 million worth of hotel-sector growth.

Haughey is much more conservative than Murray on the hotel market, saying it would grow by a mere 1 percent in 2011 and then by 22 percent in 2012.

Just as Murray predicts slight growth in recently depressed markets, he suggests the same for commercial office buildings (Figure 19). A 2011 projected 13 percent increase follows the terrible slump over the past three years. Office construction was down 27 percent in 2008, 55 percent in 2009 and 28 percent in 2010. Taken in perspective, the 13 percent gain doesn’t erase the declines of the recent past, thus proving we are in for a much slower climb than originally anticipated. Reed’s Haughey expects a 1 percent decline in office building construction in 2011 followed by a 19 percent increase in 2012.

The 2.2 million-square-foot World Trade Center Tower 3 in New York and the 1.3 million-square-foot U.S. Coast Guard Headquarters in Washington, D.C., top the list of major projects in the commercial office category. In office construction, the biggest gainers in the top 10 markets in 2010 included Phoenix, (105 percent), Atlanta (62 percent) and Chicago (61 percent). The biggest losers in the top 10 include Washington, D.C., (20 percent); Los Angeles (16 percent); and Boston (9 percent).

According to the AIA Billings Index, the commercial/industrial sector has eased into a solid recovery while residential and institutional remain flat. The AIA Consensus Construction Forecast Survey for 2010 and 2011, conducted in June 2010, indicates the total nonresidential market, which was down by 20.3 percent in 2010, will grow slightly by 3.1 percent in 2011. According to the same forecast, commercial construction is expected to grow by 5.2 percent, after slumping by 29.6 percent the previous year. The industrial market is expected to shrink by 2 percent in 2011 after declining by 21.3 percent in 2010. Institutional construction should grow by 4 percent in 2011, after declining by 12.3 percent in 2010.

In addition, lenders are starting to ease credit standards, allowing commercial projects to get rolling again. This sets the stage for future growth in commercial construction.

Institutional

In 2009 and 2010, institutional construction suffered 22 percent and 18 percent declines in terms of square footage, respectively. McGraw-Hill’s Murray expects another 6 percent decline in 2011, the equivalent of losing 133 million square feet. Reed’s Haughey is more optimistic, projecting a 4 percent increase in 2011 and another 12 percent increase in 2012 (Figure 21).

Healthcare buildings, which dropped by 38 percent in 2009, were flat in 2010.The tide is expected to turn, with a slight 6 percent increase in 2011, according to McGraw-Hill. This growth is anchored in a $500 million hospital, clinic and atrium project in Orlando, Fla., and the $394 million Wishard Hospital project in Indianapolis. Of the top 10 states in square footage for starts in healthcare, the leaders are Wisconsin, with a 110 percent increase from October 2009 to October 2010, and Pennsylvania, with a 77 percent increase.

In the public buildings sector of the institutional market, McGraw-Hill projects a 6 percent decline in 2011, which follows a 31 percent slump in 2010. And while detention facilities (24 percent), armories/military (42 percent), courthouses (40 percent), and police/fire stations (21 percent) sustained double-digit reductions in terms of square footage in 2010, post office construction increased by a whopping 130 percent. However, that jump has to be taken in context; that segment dropped by 77 percent the previous year, so it had nowhere to go but up.

McGraw-Hill data also predicts a modest 1 percent increase in the amusement/recreational segment in 2011. This comes after a 29 percent dip in 2009 and an 18 percent fall in 2010. Religious-building construction will be flat after falling by 30 percent in 2010, according to Murray. Airport and airport terminal spending is expected to slip by another 5 percent in 2011 to $2 billion worth of activity.

Industrial

According to McGraw-Hill’s Murray, plant construction is turning up, and the dollars will soon follow. He predicts an 11 percent increase in square footage in manufacturing buildings to 42 million square feet. He also envisions a $9.2 billion market for manufacturing buildings in 2011, a 9 percent increase from the previous year.

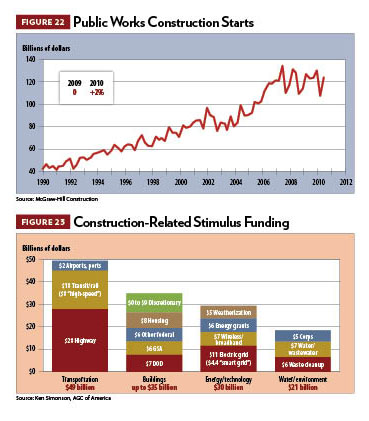

Fiscal appropriations in 2010 and a large boost from the 2009 stimulus act sparked a resurgence in the public works segment (Figure 22). Bridge and highway construction rose to $59.7 billion in 2010 but is expected to slip by 4 percent in 2011, as the initial push from the stimulus act fades. Mass transit could suffer from the same waning federal stimulus support. After a 62 percent jolt in 2009 from the stimulus act, mass transit increased by 15 percent in 2010. In 2011, Murray expects a much more modest 3 percent increase.

The financial rescue package also boosted electric utility construction and provided incentives for alternative sources of electric generation. However, spending on electric utilities has been dropping since its 2008 peak of $31.4 billion. Spending fell by 37 percent in 2009 and 11 percent in 2010. Expect another 10 percent decline in 2011.

Let’s take a closer look at how stimulus money trickled into construction and why it’s drying up.

STIMULUS OR FALSE HOPE?

“The hope was that the stimulus program would turn around the economy,” Baker said during the Reed Construction Data Webcast. “That has happened [but] nowhere near the degree we hoped it would be.”

The American Recovery and Reinvestment Act of 2009, enacted in February 2009, infused the economy with $862 billion, not all of which went into construction markets.

Ken Simonson, chief economist at the Associated General Contractors of America (AGC), speaking during the Reed webcast, said the $8,000 new homebuyer tax credit had a mixed impact. It spurred a little growth in 2009, but the market is depressed again. Construction-related stimulus funding, about $135 billion, was spread out mostly in transportation, buildings, energy/technology and water/environment. Let’s look at how that stimulus money broke down by sector (Figure 23).

About $49 billion went to transportation, $28 billion of which went to highways. Airports received $2 billion, and $18 billion went to transit/rail. Of the transit/rail dollars, about $8 billion went toward “high-speed” rail projects. Under buildings, $7 billion went to the Department of Defense, $6 billion to the General Services Administration (GSA), another $6 billion toward federal buildings, $8 billion toward housing and up to $9 billion in other discretionary spending. In the energy/technology sector, $11 billion was earmarked for electric grid projects, $4.4 of which was to go toward “smart grid” investments. Also included in the $30 billion energy/technology bucket was $7 billion for wireless/broadband projects and $6 billion in energy grants. Another $5 billion went toward weatherization.

According to McGraw-Hill’s Murray, there was also a surge in wind-power projects as a result of stimulus dollars.

Barring another round of stimulus funding, the plan will have fallen short of what it was intended to do: boost the economy out of recession. That doesn’t mean there were not opportunities in stimulus dollars and in green construction. Let’s explore green construction to see why it might be one of the leading areas of opportunity for contractors.

GOING GREEN

“If you’re doing business in the green area, you’re going to be able to weather the rough times,” said Harvey M. Bernstein, vice president of global thought leadership and business development for McGraw-Hill Construction. “The demand is there, and green is viewed as synonymous with quality.”

According to Bernstein, green construction is sustainable and affordable because the costs are competitive with traditional building; it also creates a better building.

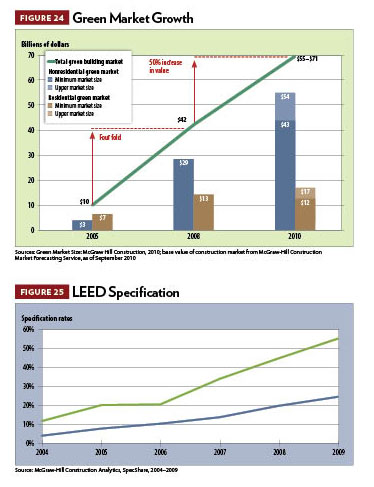

“Half of what’s going to be built in five years will be green,” he said (Figure 24).

The Leadership in Energy and Environmental Design (LEED) Green Building Rating System, according to Bernstein, is showing up in 71 percent of project specifications for projects over $50 million (Figure 25). He said LEED is strong, but other green building standards might emerge as alternatives. He suggests that competitive standards-making bodies emerging in the marketplace demonstrate how much the construction industry has embraced green building.

According to McGraw-Hill Construction, the green building market has grown six-fold in five years from $10 billion to $71 billion in 2010. The biggest growth is the nonresidential green market. In 2005, the residential green market accounted for about $7 billion, while nonresidential accounted for a mere $3 billion. In 2008, nonresidential jumped to $29 billion, surpassing the residential green market, which stood at $13 billion. In 2010, conservative estimates put the residential green market at about $17 billion, while the nonresidential green market climbed all the way to $54 billion.

Over the last five years, green construction has made serious penetration in the nonresidential market. In 2005, green projects made up a mere 3 percent of the $3 billion nonresidential market. By 2008, green building accounted for 12 percent of the $29 billion nonresidential market. In 2010, the green share of the $54 billion nonresidential market will be 35 percent. That’s a 33 percent and $55 billion increase for green construction in the nonresidential sector in five years. It has clearly caught on. The green share of nonresidential building in 2015 will climb to 48 percent of a $145 billion market, according to McGraw-Hill Construction projections. Three main trends are leading the green momentum in the nonresidential sector:

- Bigger projects are going green.

- Government mandates and policies are influencing markets (education and public buildings).

- There is a greater awareness of green construction and more experience with it in the marketplace.

Green’s share of the remodeling and retrofit market is also growing exponentially. McGraw-Hill predicts that green projects in remodeling and retrofit work will grow three-fold to five-fold by 2015.

Solar energy is also taking off. Even in a depressed economy, the U.S. solar- energy market grew in terms of both new installations and employment. Helping that, the White House approved a 1,000 megawatt (MW) solar project on public lands in October 2010. In addition, photovoltaic (PV) and concentrating solar power technologies climbed past 2,000 MW.

McGraw-Hill predicts a major surge in the market for light-emitting diode (LED) lighting in the coming years. By 2020, LEDs should cover 46 percent of the $4.4 billion U.S. market for lamps in the commercial, industrial and outdoor stationary sectors.

CONCLUSION

Many economists are cautiously optimistic about a recovery taking hold in 2011, but some business leaders think the mending process will take longer. According to a September 2010 economic survey of 900 graduates of the Harvard Business School, conducted by Zenais Marketing, more than two-thirds (68 percent) believe the economic recovery is at least two years away. Of those, 30 percent think it will take as many as five years for a recovery to occur. It’s not all gloom and doom, though.

“These findings, though sobering, do present a few bright spots,” said Paul D. Feldman, Zenais president. “More than two-thirds of the respondents believe that the economy is either stabilizing or improving.”

Reed Construction Data’s Haughey, who has more than 30 years of experience in crunching construction data figures, aggressively predicts that total construction spending will climb by 5.1 percent in 2011 and by another 12.8 percent in 2012.

“We will emerge from this economic downturn and see some growth in the latter part of 2011,” AIA’s Baker said. “It’s been a very painful downturn, but it’s possible that we can reach growth levels from five or six years ago.”

After sifting through mixed prognostications from industry experts, we can mine a few valuable nuggets of information. First, most people think the worst is over and that stabilization will pave the way for future growth. Second, the rate of growth is dependent on what happens to the volatile residential sector. Third, there are opportunities if contractors are willing to explore green building and areas experiencing better results. Fourth, this recovery period will be slow and gradual.

For traditional electrical contractors, expect another year of modest growth, as we continue to climb from the worst economic crisis in a generation. The numbers have nowhere to go but up.

About The Author

Joe Kelly, is currently senior editor in the Periodicals Group at the American Bankers Association, has been a magazine editor and writer for the bulk of his career. In 1998, Kelly became associate editor of ELECTRICAL CONTRACTOR magazine and was named editor in January 2000, a position he held until May 2003. He was instrumental in the 2002 ELECTRICAL CONTRACTOR magazine redesign and the 2003 ECmag.com Web site redesign. In addition, he helped launch Security + Life Safety Systems, in March 2003.

Kelly currently lives in Baltimore with his wife and two children and frequently contributes to ELECTRICAL CONTRACTOR.