You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

Last month, we defined money and its relative value in the marketplace. This month, we’ll analyze who benefits when the value of money changes. Keep in mind that the laws of physics also apply to the value of money: what goes up must come down.

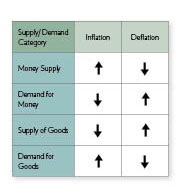

Inflation

Economists say inflation occurs when demand exceeds supply at current prices, and prices are “bid up.” Some people say this is “too many dollars chasing too few goods,” and it means the prices increase as a result of excessive spending, which is financed through borrowing from banks. Like a big auction, competitors outbid each other because they have the money. Borrowing drives inflation, not credit.

History shows that chronic inflation is a recent problem. Until the late 1940s, severe inflation usually accompanied times of war: the government overspent tax revenues and covered the difference by selling bonds to the banking system or printing paper money, resulting in quick price hikes. That is why we believe government deficits cause inflation.

Between the late 1700s and the late 1940s, though, prices fell more often than they rose, except during times of war. For example, prices at the start of World War I in 1914 were actually lower than at the end of the War of 1812. Prices dropped because supply outgrew demand during the large expansions of infrastructure related to the industrial revolution and the growth of railroads and steamship lines.

Following World War II, consumer borrowing rose drastically with the widespread availability of credit. This produced growth in residential construction and the production of cars and other goods. Business borrowing also increased.

The average rate of inflation for about the last hundred years is 3.42 percent, and more information can be found online.

Deflation

During periods of deflation, production exceeds demand, inventories are stockpiled and prices drop. Excess capacity and falling prices eventually cause business failures, loss of jobs and reduced buying power, while also dampening the growth of savings and other investments. Eventually, excess capacity is absorbed, demand outpaces supply and prices rise, stimulating production and growth as well as interest rates.

Stagflation

British politician Iain MacLeod is credited with coining the term “stagflation” to describe the simultaneous occurrence of inflation and economic stagnation. Although macroeconomic theory dictates that inflation and recession are mutually exclusive, economist John Maynard Keynes cited government price controls combined with printing of money as the causes of inflation and economic stagnation that occurred after World War I.

Stagflation is caused by a shock to the supply chain, such as a sudden increase in oil prices accompanied by a drop in oil production, by rapid increases in the money supply condoned by centralized banks, and from excessive government regulation of goods and labor. This results in the type of runaway wage-price spiraling that occurred in the 1970s. The solution is to restore the supply of materials, at least theoretically.

Winners and losers

Debtors are the primary beneficiaries of inflation, since they will repay their obligations with cheaper future dollars. The losers are the lenders, such as banks, because they will receive a defined number of dollars, which are individually worth less.

Savers and investors also are potential losers. Your bank deposits, cash value of life insurance policies, bonds or real estate investment trusts will be cashed out in dollars that are worth less than the ones you invested. If inflation is 10 percent and you receive a return on investment (ROI) of 10 percent, you merely break even. Leaving principal intact and living off of interest may not be enough, unless your ROI is high enough. For example, you would need nearly a 20 percent ROI if inflation is 10 percent and you have a 20 percent tax rate, earning 4 percent. Even if you reinvest all interest earned, you still need about a 15 percent ROI to break even.

If you buy a bigger house with a giant mortgage, you win because inflation increases home prices, and equity grows. If you cash in at the right time and pay off the debt, you are a double winner. Small-town real estate investors also benefit, as people leave large cities in bad times.

As the largest borrower, the federal government is the biggest winner, spending the money before it filters through the economy and drives up prices.

Next month, we’ll see whether the government wins or loses when it tries to manage the economy.

NORBERG-JOHNSON is a former subcontractor and past president of two national construction associations. She may be reached at [email protected].

About The Author

Denise Norberg-Johnson is a former subcontractor and past president of two national construction associations. She may be reached at [email protected].