You're reading an older article from ELECTRICAL CONTRACTOR. Some content, such as code-related information, may be outdated. Visit our homepage to view the most up-to-date articles.

For the past 50 years, ELECTRICAL CONTRACTOR has surveyed its readers every other year to get a snapshot of the industry and pinpoint emerging trends, opportunities and other changing dynamics. This 26th biannual survey, the 2012 Profile of the Electrical Contractor, reveals new markets, shows how once-emerging trends have become ingrained, and provides guidance to industry participants. We look back, while also looking forward. The following is merely a summary of the whole report, but it captures, essentially, what has transpired since the 2010 Profile of the Electrical Contractor.

Economic stabilization

The lingering effects of the Great Recession (2007–2012) resonated throughout the survey. However, savvy electrical contractors (ECs) found ways to boost revenue when traditional areas tightened or dried up. That adaptability positioned many ECs to reap the benefits of recent market stabilization and prepare for tomorrow’s opportunities.

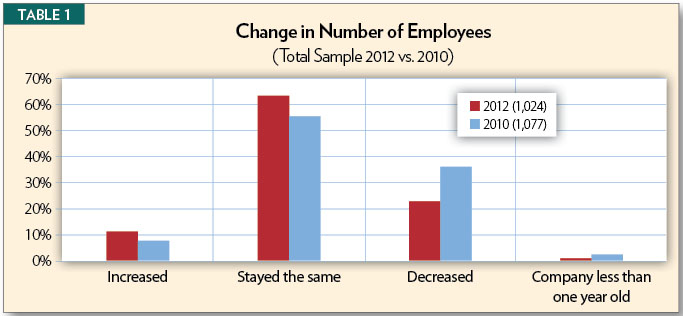

Fewer ECs reported laying off employees in the 2012 Profile, which queried contractors about their work in 2011, while more companies added workers or kept labor levels the same. That positive momentum is a welcome improvement from the recession years. With many electricians sitting on the bench over the last six years, this rebound will put them back on job sites. Let’s delve deeper into the labor data to see where the patterns lie.

Labor pool

The percentage of firms reporting that they added staff rose from 7 percent to 12 percent—not quite double but significant. More important, though, the percentage of firms that reported shedding employees dropped to 24 percent from an alarming 36 percent in the 2010 Profile, which queried ECs about their work in 2009. Don’t misunderstand; a quarter of the respondents reporting decreases in staff is still high, but the improvement indicates a reversal in the labor stats from two years ago (see Table 1).

Breaking it down by company size, the numbers are particularly encouraging. For example, among large firms (10-plus employees), the percentage reporting a decline in the number of employees plummeted from 61 percent in 2010 to 35 percent in 2012. This represents an economic correction; employers with 10-plus employees were also the hardest hit during the recession.

The story line among firms with fewer than 10 employees also points to stabilization; more companies shifted into the “stayed the same” category from the “declined” category.

Revenue and the economy

The distribution of annual revenue also steadied among firms with fewer than 10 employees. However, companies with 10–19 and 20–99 employees now are more likely than two years ago to report earning more than $1 million per year. Note that, in the 2010 Profile, a significantly higher percentage of ECs indicated their annual revenue was less than $250,000, compared with 2008, while fewer reported having annual revenues of between $1 million and $10 million.

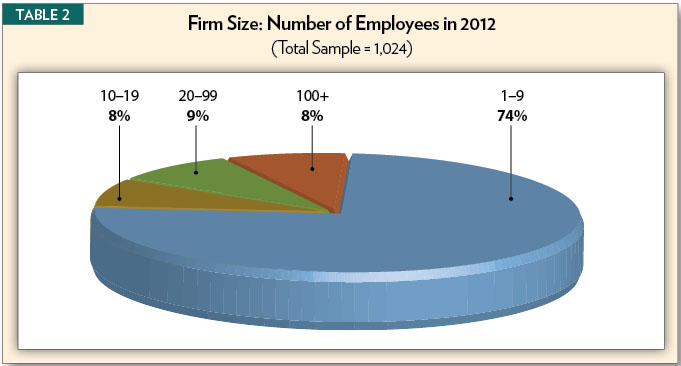

Overall, however, the sample matches the 2010 Profile: about three-quarters of respondents (74 percent) work for firms with fewer than 10 employees, and about three-quarters of electrical contracting companies (73 percent) have annual revenues of less than $1 million. Those figures are consistent with the 2010 Profile and closely resemble the 80/20 rule, in which the top 20 percent represent about 80 percent of the revenue, while the market’s majority occupies the lower tier in terms of revenue (about 20 percent).

Although the rise in the percentage of small companies may have leveled off a bit in the 2012 Profile, the number of small companies has risen dramatically from 62 percent in 2006 to 74 percent in 2012 (see Table 2). About 67 percent of ECs in the 2008 Profile had fewer than 10 employees, and small firms accounted for 72 percent of the companies in the 2010 Profile (2009 results).

Aging leadership

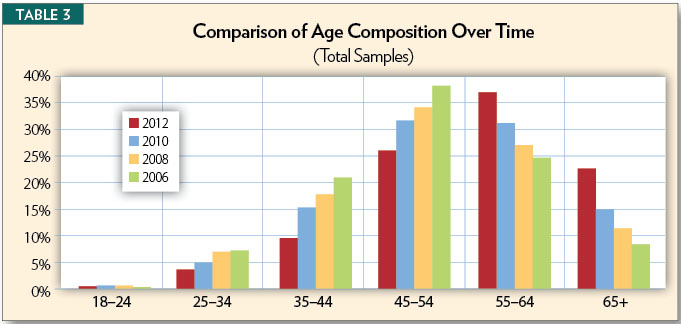

While the labor and revenue data is largely attributable to the ebbs and flows of the economy, the age distribution of the participants in the industry has changed over the last two decades. In general, the age of respondents is getting older.

However, about 35 percent of the ECs are between the ages of 35 and 54, which is down from 47 percent in the 2010 Profile. Seventy-three percent are between the ages of 35 and 64, which is down from 78 percent in 2010 (see Table 3).

The situation is tempered when looking at the level of responsibility by age. For example, the average age of field management personnel is 50.5, while the average age of owners/top management is approaching 57, which bears out over many other industries.

Another factor regarding overall age relates to the size of the firm. Specific breakouts of firms with 1–4 employees show that they trend overwhelmingly older. Sixty percent of all firms have 1–4 employees. Among those firms, 66 percent are older than 55 (57.5 years). Among larger firms (10-plus employees), just 45 percent are 55-plus. This factor skews the overall sample.

Education

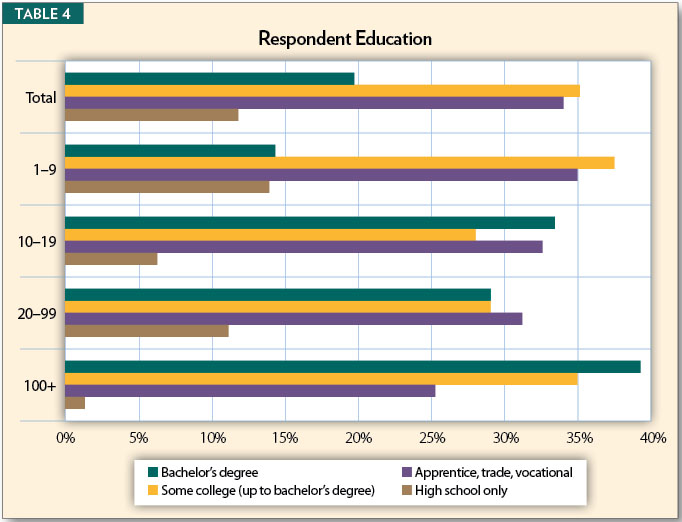

Another interesting aspect of the 2012 survey shows that 54 percent of the respondents have some college education. Respondents in larger firms (10-plus employees) are significantly more likely to have attended college than those in firms with fewer than 10 employees (64 percent versus 51 percent). In particular, 26 percent of the 10-plus-employee companies indicated that they had a bachelor’s degree, compared to 11 percent of respondents from contracting firms of fewer than 10 employees.

Respondents in smaller firms (fewer than 10 employees) are more likely to have only apprenticeship, trade or vocational school training, compared to those in firms with 10 or more employees (35 percent versus 30 percent). These educational findings are consistent with the 2010 survey (see Table 4).

However, in the 2012 Profile, 39 percent of ECs working in firms with 100-plus employees have at least a bachelor’s degree, compared with 33 percent in the 2010 Profile and 23 percent in the 2008 Profile. The increase is significant and points to a larger commitment among the wealthiest of the big firms to educate their employees or hire personnel with post-high-school educations. It could also point to the market dictating stiffer competition in the work force, enabling larger firms to pick the cream of the crop in a tight economy.

Technology is forcing contractors to hire a more skilled group of employees. ECs in larger companies, for example, are embracing the latest project management and modeling tools. Therefore, technological know-how would be a more prevalent trait for future electricians, technicians, project managers and estimators.

Now that we have an idea who makes up the electrical construction industry, let’s examine what kinds of work they are doing and what makes them successful.

Types of work

In the 2012 Profile, electrical/power distribution work declined again, this time from 56 percent to a surprising 39 percent of average revenue. Some of this monumental decline may be tied to the decreased level of new construction in a recovering economic environment, but it may also be due to a change in the 2012 Profile study in which “lighting” was broken out into a separate category. Lighting alone accounted for 20 percent of average revenue in the survey. Another possibility is that contractors have diversified from the traditional work channels, and more of their revenue is now being supplemented by projects in many other building systems (see Table 5).

In addition, some of the decline may be attributable to the fact that ECs continue to do more value-added work. For example, “electrical/power distribution” has dropped steadily in survey results since 2004 when it was 69 percent of revenue (not shown).

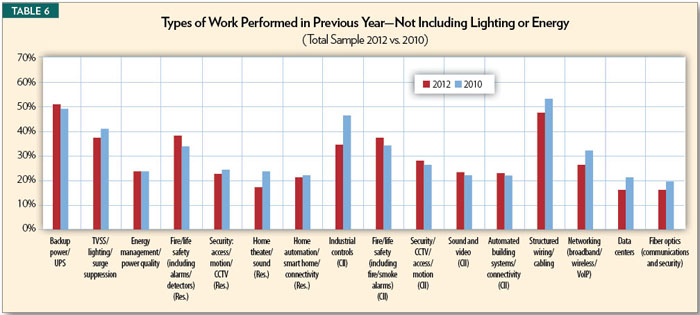

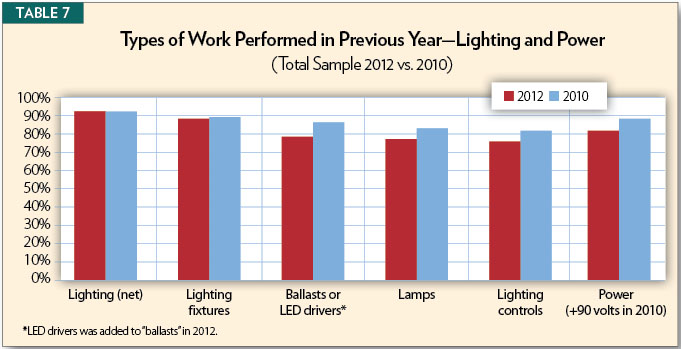

As in the past, nearly all of the companies participating in the survey performed traditional power and lighting (95 percent)—92 percent for lighting (see Table 7). No surprises there; power and lighting are the EC’s bread and butter. About 60 percent worked in power quality, communications systems, connectivity and/or commercial/industrial/institutional (CII) automation and controls. About 50 percent worked on residential automation, controls and/or green and sustainable building or alternative energy (see Tables 5 and 6).

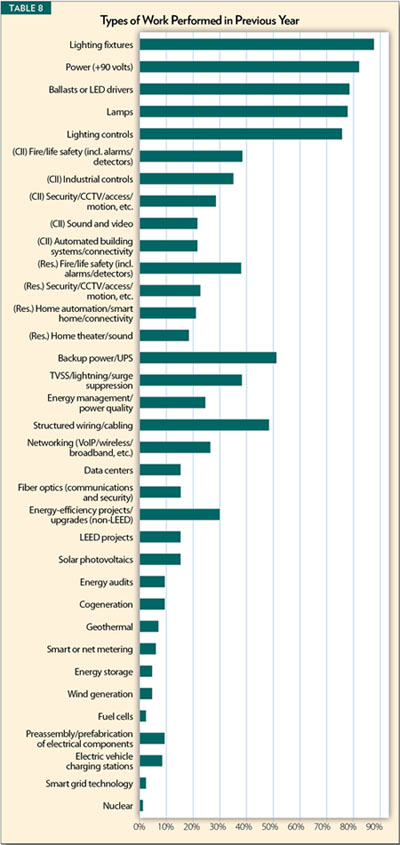

Of the types of work added in 2012, about 8 percent reported working on electrical vehicle (EV) charging stations (see Table 8). Not surprisingly, the percentages are substantially higher among the largest firms (15 percent of companies with 100-plus employees) that indicated they work on EV charging stations. About 13 percent of companies with 20 to 99 employees said they did work on vehicle charging stations. With auto emissions and environmental laws permeating the country (led by California), these charging stations provide a nice niche for ECs willing to accept the challenge.

In addition, about 2 percent of respondents said they work on smart grid technology (see Table 8). About 13 percent of the 100-plus-employee group work on smart grid technology (not shown). About 6 percent of respondents in the very largest companies said they worked on nuclear power compared with a mere 1 percent of all ECs surveyed. These trends indicate the enhanced level of sophistication of the larger companies, delivering the wherewithal to tackle some of the latest emerging opportunities. Perhaps these large firms adapted to take on this emerging work to offset losses endured in traditional power and some aspects of lighting during the Great Recession.

With the good, however, comes some bad news as well. Compared to the 2010 Profile, the percentage of ECs that reported working on communications systems/connectivity declined significantly in the 2012 Profile. In fact, there was a lower percentage of ECs that reported having worked in each of the four components of communication/connectivity: structured wiring/cabling, networking, data centers and fiber optics. This red flag for communications work is a reversal from the 2010 Profile. However, it could be because that work is just not being done during the economic recovery (see Table 6).

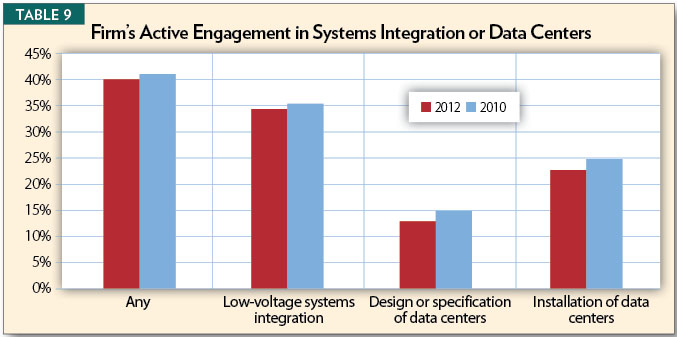

That being said, about four in 10 EC firms are actively involved in systems integration and data center work. Low-voltage systems integration was mentioned most often. Larger firms (20-plus employees) are significantly more likely to engage in these types of work than smaller firms (see Table 9).

Compared to 2010, a significantly higher percentage of ECs reported having worked on residential fire/life safety (including alarms/detectors), while fewer reported having worked on residential home theater/sound. This could be attributed to the recession repercussions, as life safety work tends to be more vital thanhome theater/sound (see Table 6).

A higher percentage of ECs report having worked on CII fire/life safety (including alarms/detectors) while fewer report having worked on industrial controls.

Sector breakdown

When looking at the sectors, on average, maintenance/service/repair on a combined basis now accounts for a substantially larger percentage of revenue (42 percent) than new construction (31 percent). Modernization/retrofit accounts for an average of 27 percent of revenue. New construction plays a proportionally larger role for firms with 10-plus employees than it does for smaller firms, while maintenance/service/repair (on a combined basis) accounts for a proportionally larger share of revenue among smaller firms.

Maintenance contracts, however, play a proportionally larger role among larger firms than among smaller firms. The average percentage of revenue from maintenance/service/repair (on a combined basis) spiked to 42 percent from 38 percent in the 2010 study and from 31 percent in the 2008 study (not shown).

Not surprisingly, maintenance and repair work tends to increase when new construction slumps. Contractors have to recover losses in new construction with maintenance contracts. The correlation is uncanny. For example, new construction dropped significantly to 31 percent of all work performed in 2012, down from 34 percent in the 2010 study and from 43 percent in the 2008 study. You can clearly see a replacement of revenue by sector out of sheer necessity.

Another example of this replacement-by-necessity approach is growth in CII work with the tanking of the residential construction market. The bursting of the housing bubble forced the hands of many ECs to seek opportunities in other sectors.

Across the total sample, ECs continue to get more of their average revenue from CII (53 percent on average) than from residential projects (42 percent). Nonbuilding projects (transportation/lighting and utility) continue to account for about 5 percent of business. These results are consistent with the 2010 Profile findings.

However, there are dramatic differences in types of work performed by larger versus smaller companies. The percentage of residential work declines smoothly and the percentage of nonbuilding increases smoothly as company size increases. In contrast, in the case of CII, there is a big jump between firms with fewer than 10 employees where average revenue is 45 percent and firms with 10-plus employees where average revenue is substantially higher. Nonbuilding continues to be the province of very large firms.

Although, on average, the greatest portion of electrical contractors’ revenue comes from CII work, single-family housing accounts for the single largest source of revenue (36 percent).

As was the case in 2010, within the broad CII category, a greater percentage of ECs’ average revenue is from commercial construction (27 percent) than from industrial (17 percent) or institutional projects (10 percent).

While single-family projects account for a high percentage of revenue across the total sample, this type of work is most important to ECs with fewer than 10 employees. These small companies derive almost half of their revenue from single-family projects. ECs with 10-plus employees derive the greatest percentage of their revenue from commercial projects. ECs with 100-plus employees get a disproportionate percentage of their revenue from industrial and institutional projects and from utility/nonbuilding work (not shown).

Trusted collaborative partners

There are numerous indications of the far-reaching influence that ECs have in design/build and brand and product specification. Let’s explore how valued ECs are in these phases of construction.

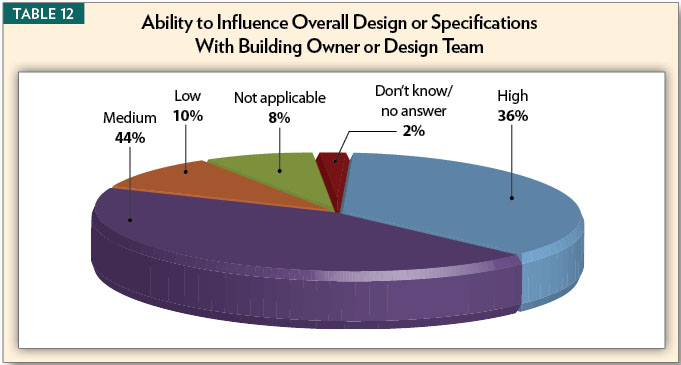

Eight in 10 ECs report having a medium or high ability to influence the overall electrical design and specifications with building owners or design team members. More than four in 10 describe their level of influence as “medium,” while 36 percent characterize their level of influence as “high.” This showcases the growing level of influence and collaboration on behalf of ECs in the design and construction process (see Table 12).

About 80 percent of ECs report receiving “any” plans and specs that are incomplete (that is, where their firm is responsible for completing the design documentation). They report, in total, that plans and specs are incomplete 46 percent of the time.

Survey respondents were asked how the percentage of incomplete plans and specs changed from five years ago. The most frequent answer was “about the same,” followed by “more often now,” and then by “less often now.”

Compared to three to five years ago, 20 percent report getting involved earlier; 54 percent report “no change,” and 12 percent say they now get involved later in the process. The remaining 11 percent say the question is “not applicable” or they “don’t know.”

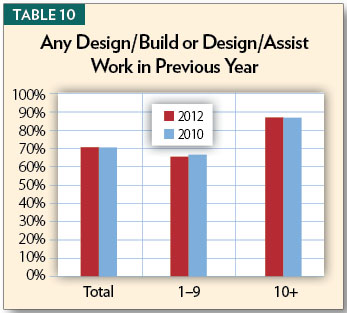

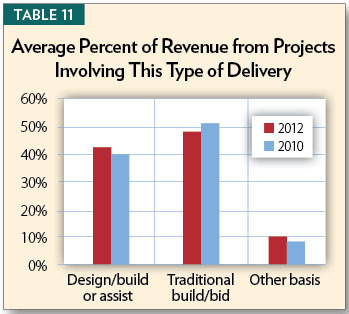

According to the survey, 70 percent of respondents performed “any” design/build or design/assist work in the previous year (see Table 10). As in the past, larger firms are more likely to have engaged in design/build or design/assist work. On average, 43 percent of revenue comes from design/build or design/assist work. This is statistically unchanged from the 2010 level of 41 percent. Between the two construction methods, the vast majority was garnered as design/build (31 percent) rather than design/assist (12 percent).

While 66 percent of ECs with fewer than 10 employees performed “any” design/build or design/assist work in 2011, “any” design/build or design/assist work was performed by 85 percent of companies with 10 or more employees. Compared to two years ago, there is a significant increase in the percentage of “any” work being done on a design/assist basis (from 39 percent to 44 percent). This increase was driven by companies with less than five employees, where “any” design/assist work is now 36 percent compared with 30 percent twoyears earlier (not shown).

Less than half (47 percent) of ECs’ average revenue comes from traditional bid/build projects. The average percentage of revenue from traditional bid/build, however, declined compared with the 2010 Profile Study (from 51 percent to 47 percent). Clearly, ECs are being trusted more with their design/build and specification capabilities (see Table 11).

Why and how they spec and buy

When it comes to brand specification, ECs continue to have a high level of brand choice and decision-making influence. In the study, respondents were shown a list of four options and asked what percentage of the specifications their company receives fall into each category. On average, a “single” brand is specified about one-quarter of the time. In all other cases, other factors—multiple brands, “or equal to” or performance specified—come into play. The importance of this is that the electrical contractor is positioned to make the final brand decision.

The mean for single or proprietary brands rose significantly among firms with 100-plus employees; it is up to 26 percent from 19 percent two years ago. During the same period, the mean for performance-specified brands among firms with 20–99 employees rose to 15 percent from 8 percent two years ago.

Respondents were then asked how much discretion they have in making a brand substitution. Overall, contractors are able to make brand substitutions about two-thirds of the time.

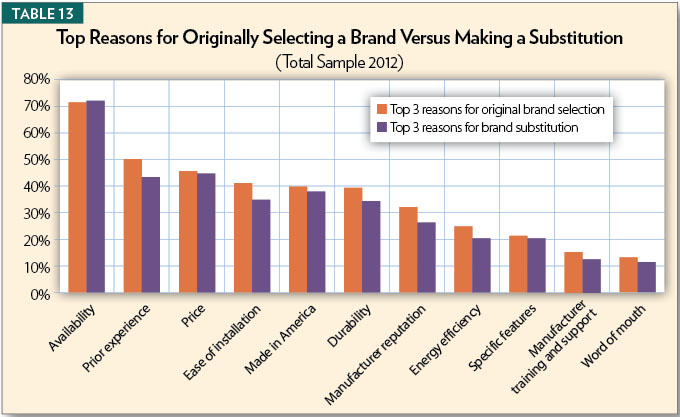

But why did they choose those products originally? Among the total sample, availability trumps price and all other attributes as both the top reason and, on a combined basis, in the top three reasons for original brand selection (see Table 13).

Prior experience, price, ease of installation, “Made in America” and durability form a second tier; each was chosen by between about 40 percent and 50 percent on a combined basis as top reasons for initial brand selection. “Made in America” was asked in the survey for the first time in 2012. Interestingly, energy efficiency was only chosen by about one-quarter of ECs as one of their three top reasons for original brand selection.

Manufacturer reputation emerges between the second tier and the lower tier of reasons that were chosen by about 20 percent or fewer as the main reasons for original brand selection.

Compared with 2010, price declined substantially and significantly as a top-three reason for original brand selection, while prior experience, energy efficiency and word of mouth were significantly more likely to be cited.

When it comes to substituting a brand, among the total sample, availability again trumps price and all other attributes as both the top reason and, on a combined basis, in the top three reasons for brand substitution. Price and prior experience form a second tier, followed closely by “Made in America,” ease of installation and durability as the three top reasons for brand substitution. Manufacturer reputation emerges between the third tier and the lower tiers. Only about 20 percent of ECs chose energy efficiency as one of their three top reasons for brand substitution. Once again, it is somewhat surprising that energy efficiency does not play a larger role.

Compared to 2010, price declined dramatically (and significantly) as a top-three reason for brand substitution; ease of installation also posted a significant decline but one that was not as large. Prior experience and durability were significantly more likely to be cited as a top-three reason for brand substitution in 2012 than in 2010.

Small EC companies need more reassurance, and, more often, they cited attributes such as ease of installation, durability, (strong) manufacturer reputation, manufacturer training and support, as key reasons for brand choice. “Made in America” and energy efficiency are also more important to small firms than to larger firms.

This finding suggests that manufacturers and marketers communicate a message of reassurance and support particularly in product lines that are sold to small ECs. In addition, “Made in America” appears to be highly important to the smaller contractor and rates as equally mentioned as price. In contrast, the only area that is more important to larger firms than to their smaller counterparts is price. However, availability tops all other attributes.

As noted above, there is a strong relationship between firm size and age of the survey taker. This is apparent in the importance given to reasons for brand selection.

“Made in America” is dramatically more important to contractors age 65 or older. It makes the top-three-reasons list for 57 percent of that group, compared to about 42 percent for those ages 35–64.

Ease of installation and, to a lesser degree, word of mouth are also more likely to be on the list of top-three reasons for the over-65 EC. Ease of installation makes the top-three list 53 percent of the time compared to 45 percent for ECs who are younger than 54. In the case of word-of-mouth influence, the comparison is 20 percent of those older than 65 to 13 percent of ages 35–54.

Among contractors aged 35–54 (who are far more likely to work in firms with more than 10 employees), price is overwhelmingly the attribute that is more likely to make the top-three-reasons list (50 percent vs. about 40 percent for those 55-plus). Specific features are also important but to a much lesser extent.

Training

Seven in 10 ECs say they, or someone in their firm, have taken a training program in the past 12 months or plans to be trained in the next 12 months to improve or broaden skills or for certification. This training could be in the form of online, correspondence or classroom training. There is no difference between the respondents that took training (69 percent) or who plan to take training (69 percent). Furthermore, there is no change in the percentage taking training or planning to take training versus two years ago (not shown).

National Electrical Code (NEC) changes is the most popular topic among respondents who have or will take training (60 percent). The most popular topics in the next 12 months for training include lighting (48 percent), automation/controls (43 percent) and grounding/bonding (40 percent).

For each of the following subject areas, the interest in the next 12 months is significantly higher than the level of interest in the past 12 months. The desired courses in high-tech areas include the following:

- Lamp technology

- Automation controls/commercial automation systems

- Electrical vehicle charging stations

- Energy use regulations

- Energy storage

- Various aspects of cabling

- Electrical systems design or building information modeling (BIM)

- Systems integration

- Sound and video (res. and commercial)

Compared to two years ago, a higher percentage of ECs now plan to take training in safety (electrical/personal/on-site/job site). Conversely, fewer plan to take training in “green,” and specifically in the U.S. Green Building Council’s Leadership in Energy and Environmental Design (LEED) certification or sustainable building/energy audits in 2012 compared to 2010. Perhaps there is a correlation between the economic woes and participation in LEED projects. With fewer new construction projects, it may be that fewer LEED-certified buildings are being constructed.

Compared to the 2010 survey, significantly more ECs reported having taken training in the past 12 months (in 2011) in the following:

- Ballasts/LED drivers

- Safety (electrical/personal/on-site/job site)

- Power quality

- Design/build

- Electrical system design or BIM

Organizations/associations are among the most frequently mentioned sources of training. Not surprisingly, ECs in small companies (fewer than 10 employees) are more likely to mention only one training source compared to those in larger firms.

It makes sense that people who work with their hands for a living prefer hands-on training. In this survey, 53 percent favor hands-on training as the single method of learning how to use new products, technology or systems. Nevertheless, hands-on training preference dropped significantly from two years ago when it was 61 percent. There was no single type of training preference in the results that rose significantly to account for the decline.

Classroom and one-on-one training are useful to about 50 percent of the contractors surveyed when asked to include all of the types of training that they find helpful. In terms of the total, however, online course/modules are viewed as more helpful among larger EC firms (those with more than 10 employees) compared with smaller firms.

Education and training have become increasingly critical to EC success because of all the changing technology and emerging opportunities. One such opportunity that is sticking around, by all accounts, is BIM.

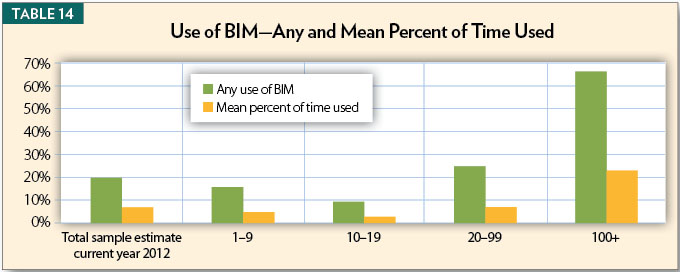

The BIM revolution

According to the 2012 Profile, about 20 percent of ECs say they currently use BIM and that, on average, they use it on about 6 percent of projects. Firms with 100-plus employees are the most likely to use BIM and to report using BIM a higher percentage of the time. It is also interesting to note that past and current BIM use appears to be particularly low among firms with 10–19 employees. EC companies with between 10 and 19 and those with 20 to 99 employees anticipate using BIM substantially more in the future (see Table 14).

ECs were asked to estimate BIM use for the current year (2012), for two to three years ago, and for two to three years into the future. The results demonstrate the need and desire among ECs to embrace this technology, perhaps due to pressure from general contractors or because ECs are becoming more integral in the design phase of construction.

About 20 percent report using BIM, while not quite 15 percent used it in the past two or three years. Twenty-six percent expect to use it two to three years in the future. However, 43 percent of those in firms with 10-plus employees said they would use it in the next two to three years. That is a ringing endorsement for the technology and its usefulness to the industry—not to mention the relationship between ECs and general contractors.

Final thoughts

You should now be able to better gauge where your company fits into the industry. While ECs have adapted well to survive during historically difficult economic times, perhaps the biggest concern for the coming two years is bouncing back to thriving levels.

About The Author

Joe Kelly, is currently senior editor in the Periodicals Group at the American Bankers Association, has been a magazine editor and writer for the bulk of his career. In 1998, Kelly became associate editor of ELECTRICAL CONTRACTOR magazine and was named editor in January 2000, a position he held until May 2003. He was instrumental in the 2002 ELECTRICAL CONTRACTOR magazine redesign and the 2003 ECmag.com Web site redesign. In addition, he helped launch Security + Life Safety Systems, in March 2003.

Kelly currently lives in Baltimore with his wife and two children and frequently contributes to ELECTRICAL CONTRACTOR.